Indonesia B2B Telecom Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.88 Billion |

| Market Size (2026) | USD 1.91 Billion |

| Market Size (2031) | USD 2.05 Billion |

| Growth Rate (2026 - 2031) | 1.43% CAGR |

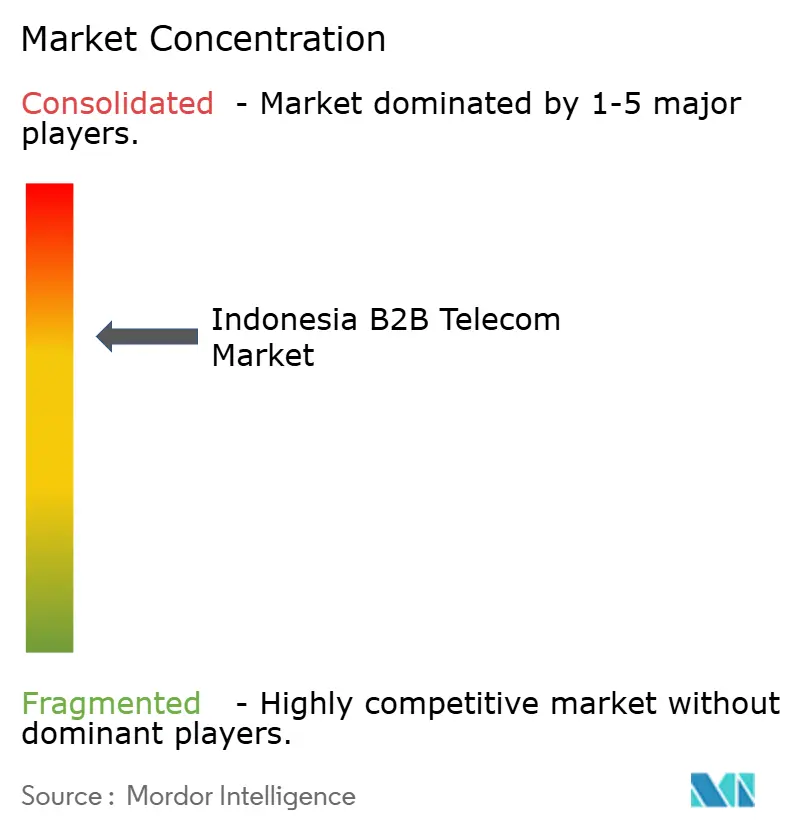

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia B2B Telecom Market Analysis by Mordor Intelligence

The Indonesia B2B Telecom Market size was valued at USD 1.88 billion in 2025 and estimated to grow from USD 1.91 billion in 2026 to reach USD 2.05 billion by 2031, at a CAGR of 1.43% during the forecast period (2026-2031). Modest growth reflects a maturing environment in which nationwide 5G and fiber backbones lower latency, while sovereign-cloud mandates and hyperscaler edge sites expand enterprise use cases. The archipelagic geography demands submarine cables, satellite backhaul, and edge nodes that collectively reshape service portfolios. Market consolidation, including the XL Axiata-Smartfren merger, compresses the competitive field even as pricing pressure rises after the 2025 Value Added Tax hike. Operators respond by bundling connectivity with managed security, cloud migration, and IoT platforms tailored to regulated verticals and SMEs.

Key Report Takeaways

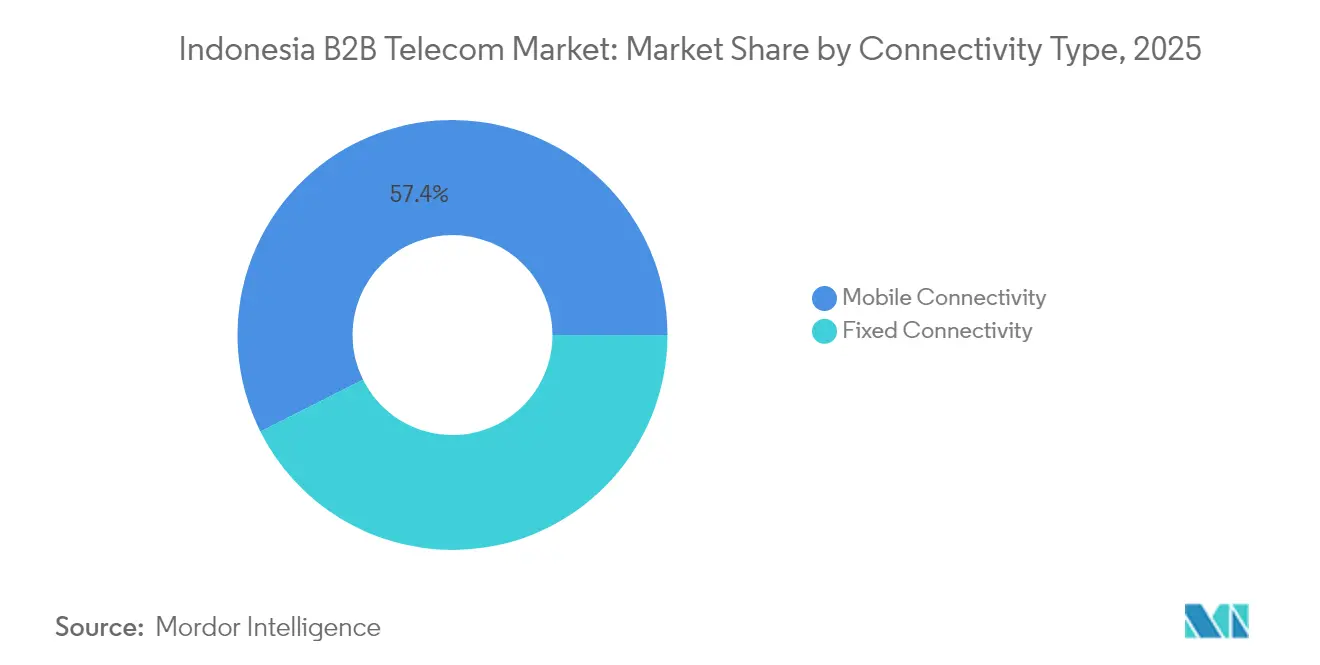

- By connectivity type, mobile connectivity led with 57.40% revenue share in 2025, while fixed connectivity is forecast to expand at a 6.05% CAGR to 2031.

- By enterprise size, large enterprises held 60.30% of the Indonesian B2B Telecom market share in 2025, while SMEs recorded the highest projected CAGR at 5.65% through 2031.

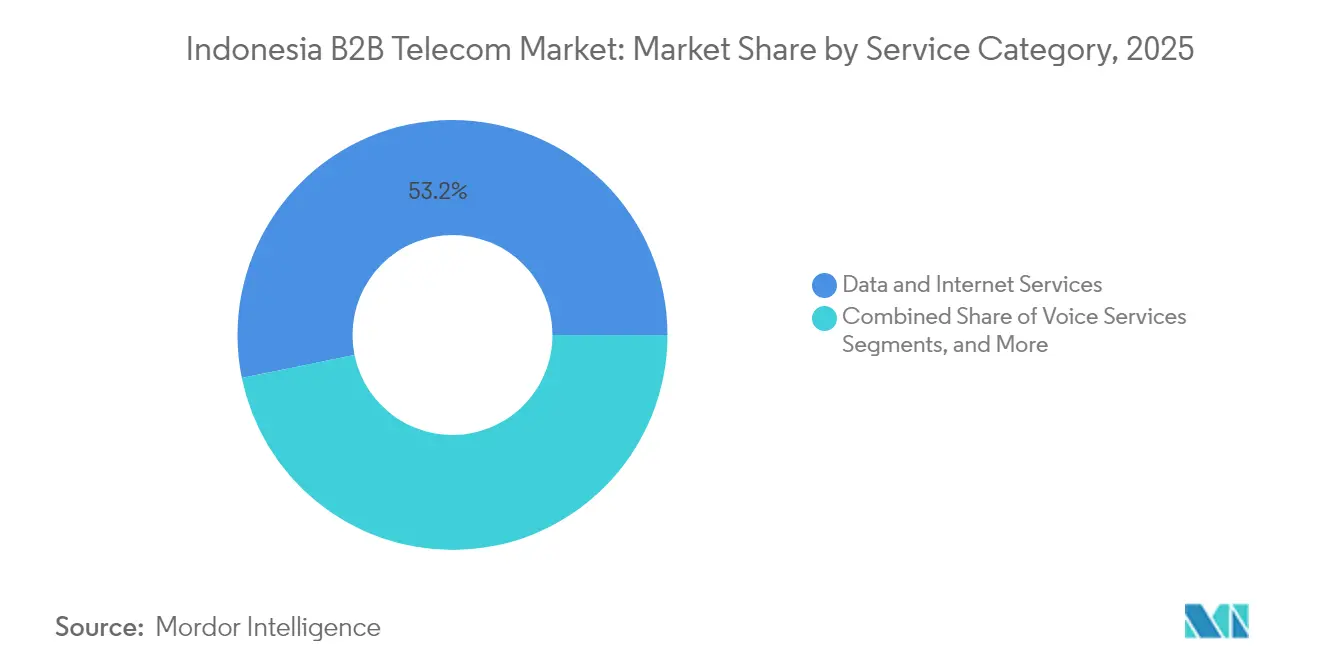

- By service category, data and internet services accounted for 53.20% of the Indonesian B2B Telecom market size in 2025, and managed and cloud services are advancing at a 6.45% CAGR through 2031.

- By industry vertical, BFSI led with 21.60% revenue share in 2025, while manufacturing is forecast to expand at a 6.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia B2B Telecom Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SD-WAN and Edge-Optimized Cloud Connectivity | +0.3% | National, with early adoption in Jakarta, Surabaya, Bandung | Medium term (2-4 years) |

| Surge in Enterprise IoT/Connected Devices | +0.4% | National, concentrated in manufacturing hubs Java and Sumatra | Long term (≥ 4 years) |

| Digital-Transformation Mandates Across Sectors | +0.2% | National, government-led initiatives across all provinces | Short term (≤ 2 years) |

| Nationwide 5G and Palapa-Ring Fiber Backbone Roll-out | +0.3% | National, prioritizing eastern Indonesia connectivity | Long term (≥ 4 years) |

| Sovereign-Cloud Compliance Push in Regulated Verticals | +0.2% | National, concentrated in BFSI and government sectors | Medium term (2-4 years) |

| Hyperscaler Edge-Zone Expansion in Tier-2 Cities | +0.1% | Regional, focusing on Medan, Makassar, Balikpapan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

SD-WAN and edge-optimized cloud connectivity

Demand accelerates as enterprises seek centralized traffic control, direct cloud paths, and lower MPLS expenses. Telkom Indonesia extended its SD-WAN portfolio with embedded edge nodes in 2025 to handle latency-sensitive workloads such as real-time analytics and remote quality inspection [1]Telkom Indonesia, “Enterprise SD-WAN Product Sheet 2025,” telkom.co.id. The architecture suits Indonesia’s dispersed islands because it overlays existing last-mile links without extensive civil works. Manufacturing plants adopt application-aware routing to prioritize IoT packets, while BFSI institutions value encrypted segmentation that meets Personal Data Protection Law requirements. The convergence with 5G slicing positions operators to upsell low-latency vertical solutions.

Enterprise IoT device surge

Mining, automotive, and palm-oil facilities deploy private LTE and 5G to link thousands of sensors that drive predictive maintenance and autonomous vehicles. XL Axiata’s deployment at PT Pamapersada Nusantara cut downtime and proved network resiliency in rugged terrain [2]Asian Business Review, “XL Axiata Business Solutions Receives Technology Excellence Award,” asianbusinessreview.com. Agriculture pilots now connect soil probes and drones, and Pegatron’s 2025 smart factory exemplifies near-zero-touch production on 5G backbones [3]Digitimes Asia, “Pegatron Opens World’s Largest 5G Smart Factory in Indonesia,” digitimes.com. These projects prove ROI, prompting new device certification programs and stimulating demand for secure device lifecycle management.

Digital-transformation mandates

The Ministry of Communication and Information Technology roadmap obliges public agencies to migrate to cloud systems by 2026, triggering predictable spending on secure connectivity and virtualized firewalls. Hospitals implement telehealth, and schools roll out hybrid classrooms that rely on symmetrical up-downlink broadband. Banks modernize core systems under the Personal Data Protection Law, boosting encrypted VPN and local cloud node demand. Subsidies for SME digitalization catalyze broadband upgrades and managed Wi-Fi adoption across retail chains.

Nationwide 5G and Palapa-Ring fiber roll-out

The 35,280 km submarine plus 21,807 km terrestrial Palapa Ring backbone finished in 2025, reducing latency gaps between Java and eastern provinces. Operators exploit the footprint for uniform service-level agreements, while 5G coverage unlocks augmented-reality maintenance, autonomous haul trucks, and UHD collaboration suites. Edge nodes at cable landing stations handle data localization needs and cut transit costs. The new capacity boosts Indonesia's B2B Telecom market competitiveness and supports cross-island enterprise networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Security and Privacy Concerns | -0.2% | National, particularly affecting multinational enterprises | Short term (≤ 2 years) |

| High CAPEX for Advanced Network Infrastructure | -0.3% | National, more pronounced in eastern Indonesia | Long term (≥ 4 years) |

| Fragmented Spectrum Allocation Across Islands | -0.1% | Regional, affecting inter-island connectivity | Medium term (2-4 years) |

| Scarcity of SD-WAN/Cloud-Networking Skill-sets | -0.2% | National, concentrated in technical roles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-security and privacy concerns

Enterprises hesitate to place sensitive workloads in shared clouds until clear compliance frameworks mature. The Personal Data Protection Law obliges onshore processing for specific datasets, compelling multinational subsidiaries to re-engineer architectures or pay for local data centers. Cyber incidents in large corporations elevate board-level focus on zero-trust networks, yet some firms favor in-house security rather than managed services. This caution slows cloud-first migrations and tempers Indonesia B2B Telecom market expansion, especially among heavily regulated players.

High CAPEX for advanced network infrastructure

Submarine cables, island microwave hops, and dense urban fiber rings require significant capital outlays. Operators prioritize Jakarta and manufacturing corridors where payback periods are shorter, leaving rural enterprises dependent on satellite backhaul or legacy xDSL. Private 5G licenses carry spectrum costs that can deter mid-sized manufacturers. Smaller service providers lack scale, limiting competitive pressure and delaying price reductions that would stimulate wider adoption. Over time, infrastructure-sharing regulations may ease the burden, yet near-term deployment budgets remain tight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connectivity Type: Mobile Networks Drive Enterprise Adoption

Mobile connectivity held 57.40% of 2025 revenue, underscoring enterprises’ need for rapid, flexible deployments across 17,508 islands. Operators upgraded existing towers to 5G non-stand-alone, shortening time to market and enabling low-latency use cases. Fixed connectivity grows fastest at 6.05% CAGR because fiber-to-the-premises secures bandwidth guarantees for critical applications. Network slicing allows blended mobile and fixed links with deterministic service levels, attracting manufacturers and fintechs. Fixed wireless access leverages 5G spectrum to deliver near-fiber speeds where trenching is costly, extending Indonesia B2B Telecom market reach beyond metro cores.

Growing submarine capacity and municipal dark fiber partnerships allow telcos to extend multi-gigabit circuits into secondary zones. Enterprises migrate from xDSL and cable modem to carrier Ethernet and GPON, seeking symmetrical throughput for cloud backups and video analytics. Operators bundle SD-WAN overlays that dynamically steer traffic among fiber, microwave, and cellular paths. These converged packages improve uptime commitments and monetize quality-of-service tiers, reinforcing Indonesia B2B Telecom market position against over-the-top players.

By Enterprise Size: SMEs Accelerate Digital Adoption

Large enterprises accounted for 60.30% of 2025 spend, leveraging scale to negotiate bespoke SLAs and invest in private 5G or multi-cloud fabrics. They demand advanced threat analytics, managed SOC, and direct cloud on-ramp gateways. SMEs post a 5.65% CAGR through 2031 as the government subsidizes digital tools and low-cost SD-WAN bundles lower entry barriers. Cloud marketplaces let SMEs activate SaaS with integrated connectivity billing, simplifying procurement. Local banks expand fintech services that require reliable broadband at point-of-sale terminals in micro-retail outlets, further boosting SME data traffic.

Operators design tiered product sets that match SME budgets while offering upgrade paths to premium features. Self-service portals automate provisioning, lowering operating expenses and improving responsiveness. Training programs help SME owners manage basic security, increasing retention. As SMEs expand online sales, inbound international traffic grows, raising the importance of content caching nodes deployed through the Palapa-Ring edge grid. This traffic mix shift supports incremental Indonesia B2B Telecom market size growth over the forecast horizon.

By Service Category: Cloud Services Transform Revenue Mix

Data and internet services generated 53.20% of 2025 revenue, yet their growth moderates as price competition intensifies. Managed and cloud services rise at a 6.45% CAGR and will erode the share of pure connectivity. Operators partner with AWS, Google, and Microsoft to host local regions that satisfy data-residency rules, capturing interconnect fees and managed migration projects. IoT connectivity gains momentum as manufacturers deploy sensor networks and logistics firms track fleets across islands using LPWAN overlays. Unified communications integrates voice, video, and team messaging, replacing legacy PBX and long-distance minutes.

Edge computing nodes at cable landing stations and regional data centers enable content delivery and AI inference close to users, reducing backhaul costs. Operators monetize these nodes through platform-as-a-service and analytics offerings. Bundled connectivity plus compute shifts value capture upstream, reinforcing Indonesia B2B Telecom market differentiation against pure-play ISPs. Voice services remain relevant in contact centers and compliance-driven sectors, but continue to decline in absolute revenue terms.

By Industry Vertical: Manufacturing Leads Digital Transformation

BFSI led with 21.60% share in 2025, reflecting digital banking, e-wallet growth, and stringent uptime mandates. Institutions deployed redundant MPLS-plus-internet circuits, multi-factor authentication, and DDoS scrubbing that elevate average revenue per line. Manufacturing posts a 6.78% CAGR through 2031 as factories embrace Industry 4.0. Private 5G networks power machine vision and AGV fleets in automotive plants, while IoT sensors optimize palm-oil cracking lines. Retail chains digitize inventory and customer engagement, relying on edge analytics for demand forecasting. Healthcare adopts telehealth and e-pharmacy services that demand HIPAA-like data protection, driving encrypted VPN growth.

Government agencies push smart-city platforms, creating demand for NB-IoT street-lamp monitoring and cloud-hosted citizen portals. Energy utilities deploy smart meters and substation telemetry that require ruggedized routers and secure APN configurations. These vertical diversifications balance revenue streams and insulate the Indonesia B2B Telecom industry from single-sector shocks.

Geography Analysis

Indonesia B2B Telecom market activity is heaviest in Java and Sumatra, which together generated roughly 69.75% of 2025 enterprise revenue. Jakarta’s corporate headquarters cluster buys premium dedicated internet and managed SOC services, pushing ARPU above the national average. Surabaya and Bandung trail but show rising demand for cloud on-ramps as hyperscalers add regional availability zones. Palapa-Ring completion levels the playing field by extending fiber backbones into Papua, Maluku, and Nusa Tenggara, allowing operators to publish national price books for the first time.

Tier-2 cities such as Medan, Makassar, and Balikpapan gain strategic importance as edge computing nodes reduce latency for interactive applications. Local governments court data-center investments through tax incentives, creating fresh backhaul contracts. Mining belts in Kalimantan need private LTE for autonomous haulage, driving microwave and satellite demand where terrain limits fiber. Fisheries in eastern archipelagos adopt IoT buoy tracking, requiring L-band satellite overlays tied into SD-WAN hubs in Java.

International connectivity improves after the Bifrost and INSICA cables boost trans-Pacific and regional capacity. Telin’s 2025 landing station in Jakarta anchors a new edge cluster that serves Southeast Asian content distribution. Enhanced transit routes make Indonesia a plausible regional interconnect hub, attracting cloud, fintech, and gaming firms that, in turn, increase local enterprise traffic. Regulators streamline right-of-way and tower sharing rules, reducing deployment cost variances across provinces and accelerating inclusive Indonesia B2B Telecom market growth.

Competitive Landscape

Telkom Indonesia, Indosat Ooredoo Hutchison, XL Axiata-Smartfren, and Telkomsel collectively account for about 75% of enterprise revenue, giving the market a moderate concentration profile. The XL Axiata-Smartfren merger, cleared in 2024, pools mid-band spectrum and tower assets, enabling aggressive 5G rollout and economies of scale. Telkom Indonesia counters with edge clouds co-located at Bifrost landing sites and an expanded SD-WAN catalog that integrates its data-center subsidiary’s assets. Indosat focuses on cloud partnerships, launching Google Distributed Cloud in Jakarta to capture regulated workloads.

Technology vendors carve out direct enterprise channels. Nokia deploys private 5G for automotive plants, while Huawei pilots campus networks in universities. AWS and Microsoft offer direct connect services that bypass traditional MPLS, prompting operators to reposition as integrators rather than mere access providers. Managed security becomes a battleground as cyber incidents raise customer sensitivity; Telkomsel opens a cyber-fusion center and markets AI-driven threat analytics to BFSI clients. Pricing dynamics intensify after the VAT increase, but operators defend margins through tiered service bundles.

Future competition may come from satellite broadband constellations as Starlink eyes maritime and mining contracts. Regulators require local gateways, which favors incumbents able to host landed traffic. Wholesale fiber players explore REIT structures to unlock capital for backbone expansion, potentially lowering leasing costs and stimulating regional ISPs. Collectively, these moves reinforce innovation while keeping the Indonesian B2B Telecom market rivalry within a disciplined pricing band.

Indonesia B2B Telecom Industry Leaders

PT Telekomunikasi Indonesia (Persero) Tbk

PT Telekomunikasi Selular (Telkomsel)

PT Indosat Ooredoo Hutchison Tbk

PT XL Axiata Tbk

PT Smartfren Telecom Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Telin completed the Bifrost cable landing station in Jakarta, adding 15 Tbps of international capacity and positioning Indonesia as a regional cloud hub.

- April 2025: Pegatron opened the world’s largest 5G smart factory in Indonesia, spotlighting private-network use cases across the manufacturing sector.

- March 2025: Indonesia raised Value Added Tax from 11% to 12%, prompting major operators to implement phased tariff adjustments for B2B plans while expanding bundled service offers.

- December 2024: XL Axiata and Smartfren secured final approval for their USD 6.5 billion merger, creating a carrier with roughly 25% enterprise share and targeted cost synergies of USD 300-400 million.

Indonesia B2B Telecom Market Report Scope

B2B telecommunication providers operate systems that facilitate the transmission of data, text, sound, voice, and video, enabling direct business-to-business communication. Additionally, marketers leverage these telecommunication platforms to enhance a company's industry visibility and pinpoint networking prospects, further fueling the demand for B2B telecommunications.

The report covers Indonesian B2B telecom companies, and the market is segmented by connectivity type (mobile connectivity, fixed connectivity [covers DSL, FTTP/B, cable modem, FWA]) and size of enterprises (small and medium-sized enterprises [SMEs], large enterprises).

The report offers market sizes and forecasts in value (USD) for all the above segments.

| Mobile Connectivity (5G and 4G/LTE) |

| Fixed Connectivity (Fiber-to-the-Premise/Building (FTTP/B), Cable Modem, xDSL, Fixed Wireless Access (FWA)) |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| Voice Services |

| Data and Internet Services |

| Managed and Cloud Services (IaaS/PaaS/SaaS) |

| IoT / Machine-to-Machine (M2M) Connectivity |

| Unified Communications and Collaboration |

| Manufacturing |

| Banking, Financial Services and Insurance (BFSI) |

| Retail and E-commerce |

| Healthcare |

| Government and Public Sector |

| Energy and Utilities |

| Transportation and Logistics |

| By Connectivity Type | Mobile Connectivity (5G and 4G/LTE) |

| Fixed Connectivity (Fiber-to-the-Premise/Building (FTTP/B), Cable Modem, xDSL, Fixed Wireless Access (FWA)) | |

| By Enterprise Size | Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises | |

| By Service Category | Voice Services |

| Data and Internet Services | |

| Managed and Cloud Services (IaaS/PaaS/SaaS) | |

| IoT / Machine-to-Machine (M2M) Connectivity | |

| Unified Communications and Collaboration | |

| By Industry Vertical | Manufacturing |

| Banking, Financial Services and Insurance (BFSI) | |

| Retail and E-commerce | |

| Healthcare | |

| Government and Public Sector | |

| Energy and Utilities | |

| Transportation and Logistics |

Key Questions Answered in the Report

How large is the Indonesia B2B Telecom market in 2026?

The Indonesia B2B Telecom market size stands at USD 1.91 billion in 2026 and is set to reach USD 2.05 billion by 2031.

Which segment grows fastest between 2026 and 2031?

Fixed connectivity posts the quickest advance at a 6.05% CAGR, driven by fiber-to-the-premises rollouts and enterprise latency demands.

What is driving enterprise adoption of SD-WAN in Indonesia?

Firms seek centralized control, reduced MPLS costs, and direct cloud access while complying with data-sovereignty rules, all of which SD-WAN enables.

Why are SMEs important for telecom revenue growth?

Government subsidies and affordable cloud bundles help SMEs digitize sales and operations, giving the segment a 5.65% CAGR through 2031.

How will the XL Axiata-Smartfren merger affect competition?

The combined carrier will command roughly 25% revenue share and wider spectrum holdings, prompting rivals to differentiate through edge cloud and managed security offerings.

Page last updated on: