Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 121.07 Billion |

| Market Size (2026) | USD 125.98 Billion |

| Market Size (2031) | USD 148.06 Billion |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Telecom MNO Market Analysis by Mordor Intelligence

The Japan telecom MNO market size is projected to be USD 125.98 billion in 2026 and reach USD 148.06 billion by 2031, growing at a CAGR of 3.28% from 2026 to 2031. Subscriber penetration already exceeds 150%, so topline growth depends on 5G-stand-alone monetization, fixed-mobile convergence bundles, and enterprise Internet of Things (IoT) use cases. Operators are racing to densify 3.7 GHz and 4.5 GHz macro-cells while off-loading peak traffic to home Wi-Fi and fiber backhaul, a strategy that holds average revenue per user (ARPU) flat despite continuing price competition. New revenue streams arise from network application programming interfaces (APIs) that let enterprises invoke assured quality on demand, location verification, and device-identity services. At the same time, satellite-cellular hybrids improve coverage in Japan’s rugged terrain, and all-photonics backbone upgrades shrink energy cost per bit, cushioning profitability against surging data traffic.

Key Report Takeaways

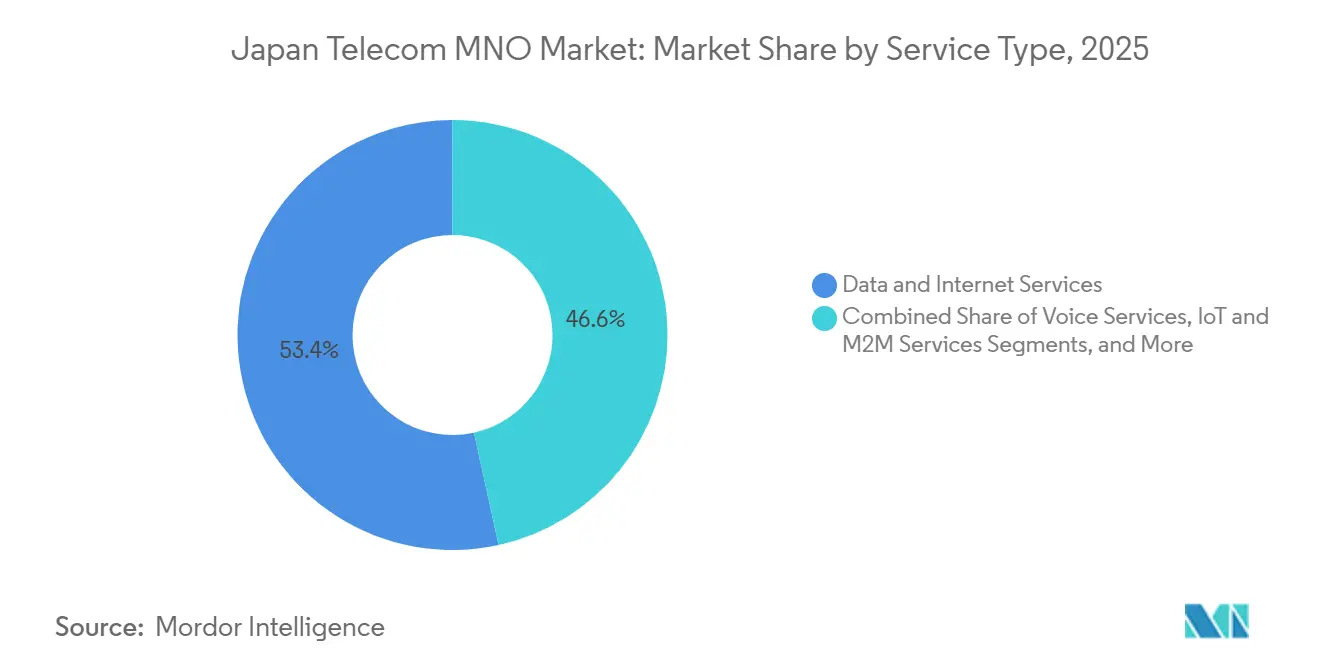

- By service type, Data and Internet Services held 53.43% of the Japan telecom MNO market share in 2025, while IoT and M2M Services is set to expand at a 3.44% CAGR to 2031.

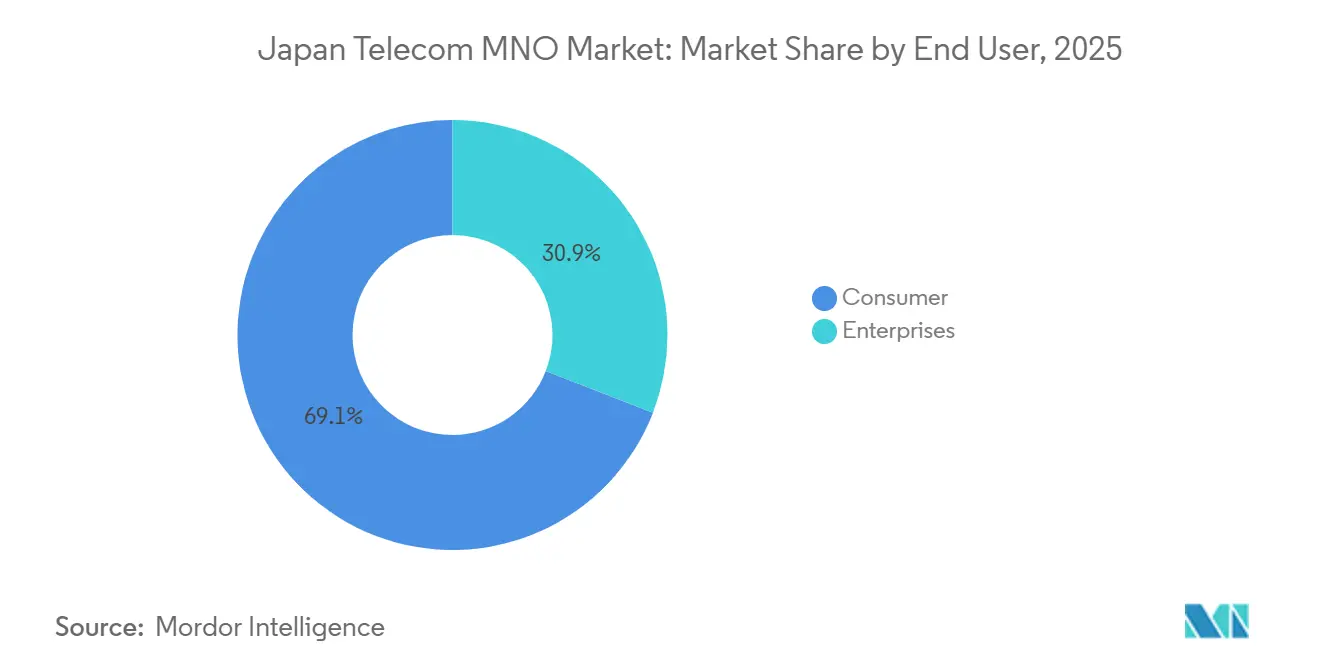

- By end-user, Consumer subscribers captured 69.12% revenue in 2025; the Enterprises segment is advancing at a 3.59% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G Standalone Expansion and Private Network Monetization | +0.9% | Tokyo, Osaka, Nagoya industrial corridors | Medium term (2-4 years) |

| Explosion of Ultra-HD Video and XR Data Traffic | +0.7% | Urban centers nationwide | Short term (≤ 2 years) |

| Digital Garden City Nation Strategy Catalyzing Regional IoT Uptake | +0.5% | Regional smart-city zones | Long term (≥ 4 years) |

| Fixed-Mobile Convergence Driving Premium Bundled ARPU | +0.4% | Fiber-dense metropolitan areas | Medium term (2-4 years) |

| Satellite-Cellular Hybrid Connectivity Licenses Opening Rural Markets | +0.3% | Remote islands and mountains | Long term (≥ 4 years) |

| Monetization of Network APIs via GSMA Open Gateway Framework | +0.2% | Major business districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Standalone Expansion and Private Network Monetization

NTT Docomo activated 6.6 Gbps downlink service in early 2025 by aggregating sub-6 GHz and millimeter-wave bands, showcasing real-time 8K video and machine-vision control. Enterprises are licensing n79 spectrum slices for robotics, semiconductor tooling, and smart logistics, supported by the Ministry of Internal Affairs and Communications (MIC) registration regime that obliges carriers to appoint certified chief telecommunication engineers, a structure that protects incumbents’ margins. SoftBank’s latency-optimization trial with Ericsson in late 2024 achieved sub-5 ms round-trip delay, bolstering standalone cores as revenue generators for deterministic industrial traffic. MIC’s 2025 Beyond 5G white paper projects enterprise private networks to absorb 15% of total mobile infrastructure outlays by 2030.[1]Ministry of Internal Affairs and Communications, “Statistics on Telecommunications Services,” soumu.go.jp

Explosion of Ultra-HD Video and XR Data Traffic

Fixed-line traffic jumped 15.3% year-over-year in May 2025, while 5G handset growth lifted mobile usage in parallel. MIC forecasts immersive content to push volumes ten-fold by 2030, forcing operators to densify small cells and deploy edge computers. NTT Docomo’s fiscal-2025 interim report logged double-digit data growth, with premium unlimited tiers shielding ARPU. Ericsson’s mid-2025 Mobility Report cites artificial-intelligence spectrum allocation as key to handling asymmetric uplinks from live XR streams.[2]Ericsson, “Mobility Report North East Asia 2025,” ericsson.com Bundling streaming or metaverse access into tiered plans lets carriers upsell without proportional cost, provided content-delivery caches sit close to users.

Digital Garden City Nation Strategy Catalyzing Regional IoT Uptake

MIC’s Digital Garden City Nation blueprint pledges 99% 5G coverage by fiscal 2030 and 99.9% fiber-to-the-home by fiscal 2027, undergirding rural telemedicine, smart agriculture, and municipal sensor grids. KDDI’s ConnectIN added 45.5 million IoT lines by March 2024, many in regional prefectures facing labor shortages.[3]KDDI Corporation, “ConnectIN IoT Platform Update,” kddi.com NTT Docomo’s business SIGN IoT, launched December 2025, blends LoRaWAN and satellite backhaul for forestry and agriculture. Mizuho Bank projects machine-to-machine revenue to exceed JPY 530 billion by 2030 (USD 3.9 billion).[4]Mizuho Bank, “IoT Market Outlook 2030,” mizuhobank.co.jp Cabinet Office smart-city pilots co-fund local sensors, lowering risk for operators and accelerating the Japan telecom MNO market transition toward B2B IoT streams.

Fixed-Mobile Convergence Driving Premium Bundled ARPU

NTT’s Innovative Optical and Wireless Network (IOWN) 2.0 in 2025 fused fiber backbone and mobile radios, enabling unified gigabit fiber and 5G billing. NTT Docomo’s docomo MAX combines unlimited 5G, 10 Gbps fiber, and streaming for household ARPU above JPY 10,000 (USD 67.9).[5]NTT Communications, “TypeD Private 5G Service,” ntt.com KDDI’s Vision 2030 cross-sells banking, electricity, and entertainment, raising lifetime value. Shared backhaul lowers capex intensity and streamlines care systems, offsetting stagnant subscriber growth. Submission of bundle terms to MIC ensures transparency, a process that smaller challengers find resource-heavy, cementing incumbents’ moat.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Price Competition Among MNOs Compressing Margins | -0.8% | National, Most Acute in Phnom Penh and Other Urban Centers | Short Term (≤ 2 Years) |

| High Rural Deployment Costs Versus Low Income Base | -0.6% | Remote Provinces (Ratanakiri, Mondulkiri, Preah Vihear, Stung Treng) | Medium Term (2–4 Years) |

| Limited Fiber Backhaul Causing Capacity Bottlenecks | -0.4% | Semi-Urban and Deep Rural Districts | Short Term (≤ 2 Years) |

| Regulatory Uncertainty on Active Sharing Delaying 5G Small Cells | -0.3% | Dense Urban Zones That Need Indoor Micro-Sites | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Aging and Declining Population Limiting Subscriber Growth

Japan’s population fell below 123 million in 2025 with a median age above 49, trimming organic handset uptake. Cellular lines stood at 193 million, leaving scant headroom outside IoT. Rakuten Mobile’s 8.5 million users in early 2025 faced churn as price hunters rotated to promotions. Operators tailor elder-care voice assistants, yet these generate modest data income. MIC’s Mobile Software Competition Act, effective 2025, enhances portability, boosting price sensitivity and eroding loyalty.

Continued Government Pressure on Tariffs Depressing ARPU

Successive administrations compelled roughly 40% retail-price cuts between 2018-2020, and MIC annual reviews sustain downward tension. Rakuten’s JPY 1,980 (USD 12.7) 20 GB plan in May 2025 rekindled price wars. Incumbents answered with discount sub-brands ahamo, povo, and LINEMO, cannibalizing premium tiers. App-store fee mandates limit content-bundle upsell, so carriers pivot to enterprise slices and API revenue insulated from consumer price caps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Dominance With IoT Upside

Data and Internet Services accounted for over half of 2025 revenue, supported by 92.367 million 5G subscriptions and double-digit fixed broadband traffic growth. The Japan telecom MNO market size tied to IoT and M2M Services is forecast to expand fastest at a 3.44% CAGR thanks to fleet telematics, industrial robotics, and rural smart-city sensors, a trajectory underscored by KDDI ConnectIN’s 45.5 million lines and NTT Docomo’s business SIGN IoT rollout. Voice and SMS continue to shrink as over-the-top applications dominate, while pay-TV bundles cushion ARPU through premium content licensing.

Operators are now packaging network APIs into developer marketplaces, an initiative aligned with the GSMA Open Gateway framework demonstrated by KDDI at Mobile World Congress 2025. The Japan telecom MNO market size for these APIs remains nascent, yet global projections reach USD 300 billion by 2030. Regulatory oversight of interconnection under the Telecommunications Business Law tempers innovation velocity but ensures nondiscriminatory wholesale pricing, balancing competition and stability.

By End-User: Enterprise Velocity Outpacing Consumer Scale

Consumer lines still supply 69.12% of 2025 revenue, sustained by high smartphone penetration and unlimited-data indulgence, with Opensignal clocking above-30% 5G availability in major prefectures. Yet demographic drag and regulatory price caps limit further expansion, pushing carriers toward bundled fiber-mobile offers that raise household stickiness rather than chasing new handsets.

Enterprises deliver the quickest growth at a 3.59% CAGR: private 5G slices power robotic welding, augmented-reality maintenance, and autonomous guided vehicles in factories, while AU Starlink Direct satellite-cellular hybrids secure offshore rigs and remote construction. Average enterprise ARPU runs three-to-five times higher than consumer plans because contracts bundle service-level agreements, edge computing, and cybersecurity audits mandated by the 2024 National Security Act. These characteristics position the Japan telecom MNO market as a vital digital infrastructure backbone for corporate Japan.

Geography Analysis

Japan’s dense urban corridors of Tokyo, Osaka, and Nagoya command the lion’s share of the Japan telecom MNO market size, thanks to population clustering and enterprise headquarters concentration. 5G population coverage hit 98.4% nationwide by fiscal 2024, yet metro areas still draw the most capital for mid-band refarming and millimeter-wave infill. High-rise propagation challenges in Tokyo push operators to deploy indoor small cells and distributed-antenna systems, a capex cycle that supports vendor revenue

Regional prefectures benefit from the Digital Garden City Nation grants that subsidize smart-agriculture sensors and telehealth nodes, lifting IoT line density. Rakuten Mobile focuses rural rollouts on inexpensive open-RAN gear to close its coverage gap, but MIC administrative guidance on base-station delays revealed compliance hurdles that slow progress. Remote islands and mountainous districts are the proving ground for satellite-cellular hybrids, where KDDI’s AU Starlink Direct service integrates low-Earth-orbit links with terrestrial core handoff.

Looking ahead, the first spectrum auction for 26 GHz and 40 GHz bands scheduled before March 2026 could reshape millimeter-wave holdings, inviting new niche entrants to Tokyo’s stadiums and entertainment districts. Still, strict MIC build-out obligations and security vetting under the 2024 supply-chain law mean incumbents with deep balance sheets remain favored to defend share. Thus, urban densification, regional IoT enablement, and remote-area satellite augmentation together sustain the geographically balanced advance of the Japan telecom MNO market.

Competitive Landscape

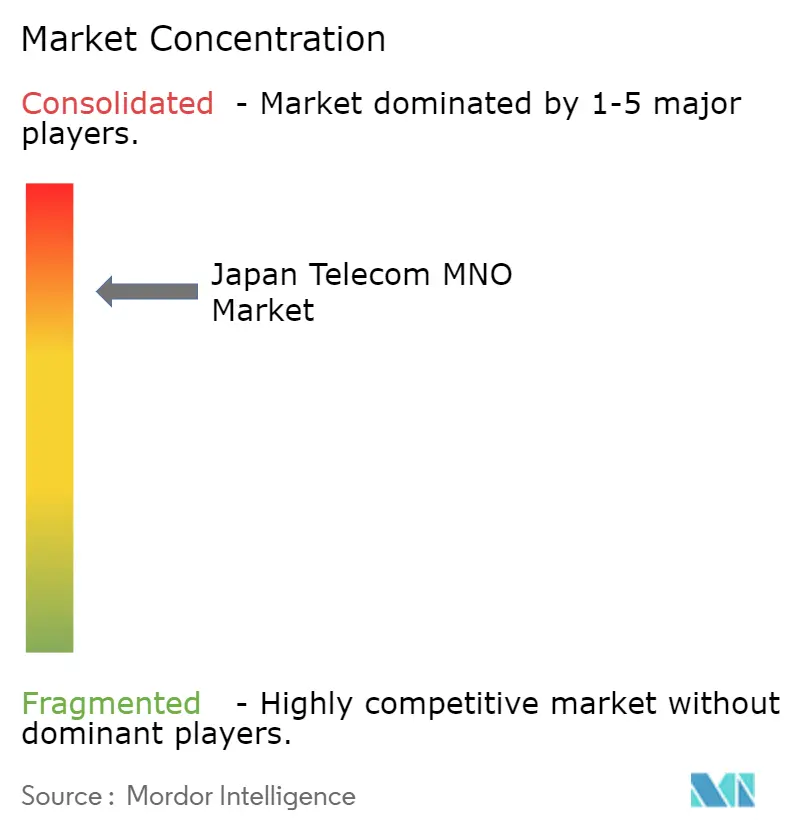

The Japan telecom MNO market concentrates heavily in three incumbents, NTT Docomo, KDDI, and SoftBank, who together hold roughly 97% subscriber share. NTT Docomo leverages parent NTT’s fiber footprint and IOWN roadmap to bundle 10 Gbps home broadband, mobile unlimited data, and over-the-top video, elevating household ARPU and deterring churn. KDDI differentiates through cross-sector convergence, folding payment apps, energy retail, and esports into its AU ecosystem. SoftBank emphasizes artificial-intelligence radio resource management via its AI-RAN initiative, trimming latency and boosting spectral efficiency.

Rakuten Mobile, the only recent entrant, attained full-year profitability in fiscal 2025 but still controls just 2.6% share. It pursues vendor-diverse open-RAN deployment with Fujitsu and Nokia while marketing the nation’s cheapest large-bucket data plan to lure switchers. Structural barriers persist: stringent MIC quality-of-service rules and National Security Act component vetting impose compliance overhead that smaller challengers struggle to absorb.

Strategic moves in 2025-2026 underscore the innovation race. NTT Docomo is trialing direct satellite-to-smartphone links to match KDDI’s Starlink reseller agreement. SoftBank and Nokia inked a Western-Japan modernization deal covering AirScale radios and AI-driven MantaRay orchestration. Tower-sharing specialist JTower is rolling out neutral-host 5G poles that reduce duplicate capex and align with government policy to accelerate densification. All players collaborate on disaster-recovery refueling drills, reflecting regulatory expectations for resilient national networks.

Japan Telecom MNO Industry Leaders

NTT Docomo, Inc.

KDDI Corporation (au)

SoftBank Corp.

Rakuten Mobile, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: NTT Docomo will launch a direct satellite-to-smartphone service in early fiscal 2026 to extend coverage in disaster zones.

- February 2026: Rakuten Mobile posted its first full-year mobile profit for fiscal 2025, citing 8.5 million subscribers and disciplined network spending.

- February 2026: NTT Docomo trimmed its fiscal-2025 profit outlook due to extra network investment and tariff pressure.

- January 2026: Eight carriers held joint fuel-supply drills in Kanagawa Prefecture to speed disaster recovery of base stations.

- December 2025: NTT Docomo introduced business SIGN IoT low-power services for agriculture and forestry.

Japan Telecom MNO Market Report Scope

The study provides an in-depth analysis of the telecommunication industry in Japan. Japan's telecom MNO market is segmented by services, which is further classified into voice services (wired, wireless), data and messaging services, and OTT and pay TV.

The Japan Telecom MNO Market Report is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, IoT and M2M Services, OTT and PayTV Services, and Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, Rest of Service Type)), End-User (Enterprises, and Consumer), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services, Roaming and International Services, Enterprise and Wholesale Services |

End-User

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services, Roaming and International Services, Enterprise and Wholesale Services | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large will the Japan telecom MNO market be by 2031?

It is forecast to reach USD 148.06 billion by 2031, reflecting a 3.28% CAGR from 2026.

Which service category is growing fastest?

IoT and M2M Services is projected to grow at a 3.44% CAGR through 2031 as enterprises deploy smart-factory and logistics solutions.

Why is ARPU under pressure in Japan?

Government tariff reductions and aggressive discount brands have driven headline mobile prices down, forcing operators to rely on bundled fiber, content, and enterprise services to defend ARPU.

What share do the top three carriers control?

NTT Docomo, KDDI, and SoftBank together hold about 97% of mobile subscribers, making the market highly concentrated.

How are operators addressing rural coverage gaps?

They deploy satellite-cellular hybrids such as KDDI's AU Starlink Direct and plan direct satellite-to-smartphone links to extend service to remote islands and mountainous areas.

What is the main regulatory hurdle for new entrants?

Strict Ministry of Internal Affairs and Communications quality-of-service rules and supply-chain security reviews raise compliance costs, benefiting incumbents with greater resources.

Page last updated on: