Indium Tin Oxide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.92 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indium Tin Oxide Market Analysis by Mordor Intelligence

The Indium Tin Oxide Market size was valued at USD 1.84 billion in 2025 and estimated to grow from USD 1.92 billion in 2026 to reach USD 2.36 billion by 2031, at a CAGR of 4.23% during the forecast period (2026-2031). Display makers are scaling eighth-generation OLED fabs that require uniform, high-conductivity transparent electrodes, while thin-film photovoltaics and smart-glass projects are opening new end-use avenues. Automotive digital cockpits and battery thermal sensors are emerging, high-margin niches. On the supply side, indium export controls and recycling progress are redefining procurement strategies and pushing producers toward closed-loop recovery systems.

Key Report Takeaways

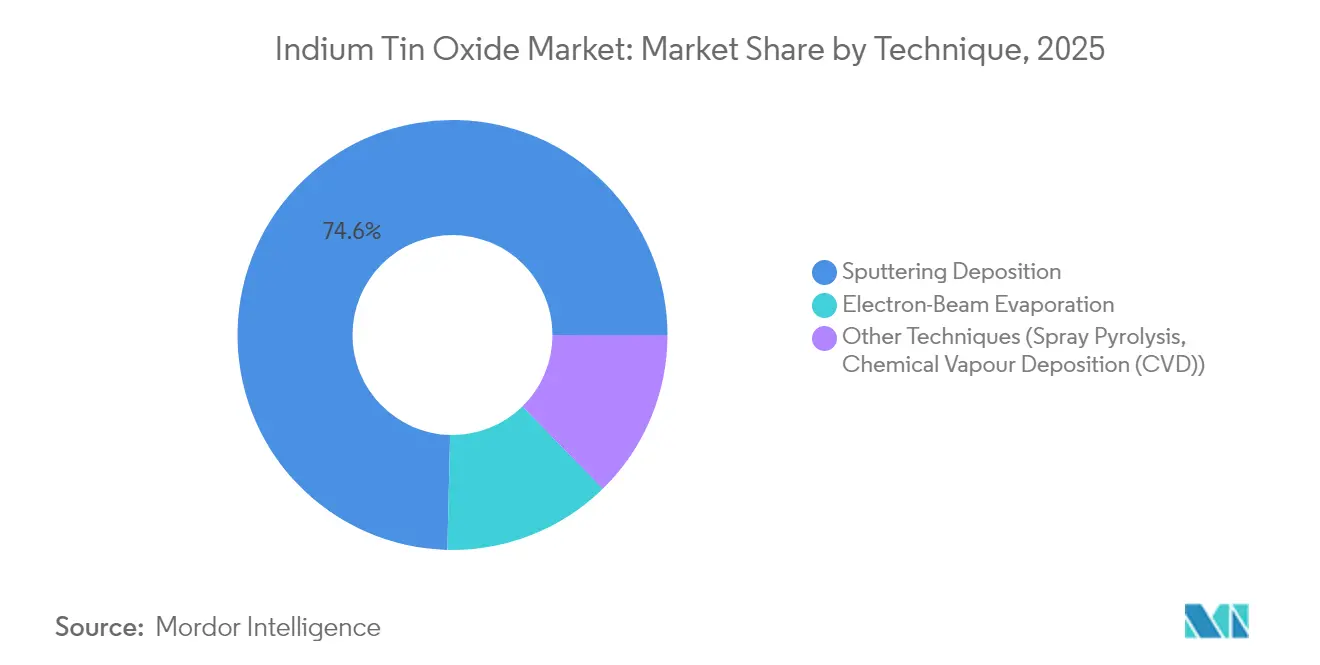

- By technique, sputtering deposition led with 74.62% of the indium tin oxide market share in 2025; spray pyrolysis and other approaches are projected to post a 5.12% CAGR through 2031.

- By application, optoelectronics commanded 47.12% revenue in 2025, while photovoltaic cells are forecast to grow at a 5.02% CAGR to 2031.

- By end-user industry, consumer electronics held 50.74% of the indium tin oxide market in 2025, and automotive applications are expected to advance at a 5.06% CAGR through 2031.

- By geography, Asia-Pacific contributed 55.68% of 2025 global revenue and is set for a 4.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Indium Tin Oxide Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand due to panel capacity additions | +1.2% | Asia-Pacific core, spill-over to global supply chains | Medium term (2-4 years) |

| Rising solar PV installations needing transparent electrodes | +0.9% | Global, with concentration in China, India, and EU markets | Long term (≥ 4 years) |

| Growth of smart-glass and touch-interface devices | +0.8% | North America & EU leading, Asia-Pacific manufacturing | Medium term (2-4 years) |

| EV battery tabs adopting ultra-thin ITO coatings for heat sensing | +0.6% | Global EV markets, early adoption in China and Europe | Long term (≥ 4 years) |

| Increase in demand from wearable and flexible electronics | +0.5% | Global consumer markets, manufacturing in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from New Panel Capacity

OLED fabs under construction across China, Korea, and Japan are lifting long-term offtake agreements for indium tin oxide targets. BOE Technology and TCL CSOT have announced eighth-generation lines designed for large substrates, driving specifications that favor high-uniformity sputtered films. Flexible smartphone displays are projected to exceed half of shipments by late-2024, and micro-OLED spending is accelerating for near-to-eye devices. Equipment providers report backlog growth, reinforcing multi-year visibility for ITO coating demand. Although inkjet-printed electrodes are improving, incumbent sputtering economics remain competitive for mainstream production[1]BOE Technology Group Co., “Announcement of Chengdu 8.6G OLED Fab Investment,” boe.com.

Rising Solar PV Installations Needing Transparent Electrodes

Global photovoltaic additions topped 230 GW in 2024, and government auctions point to larger 2025 build-outs. Thin-film CIGS developers rely on indium tin oxide layers to balance transparency and sheet resistance, especially in tandem and perovskite-on-silicon designs. Module oversupply is pushing prices down, yet lower capex per watt is spurring adoption in distributed generation. Research groups have achieved 52% indium recovery from end-of-life CIGS modules via electrolytic methods, a step toward offsetting primary supply concentration. Over the long term, higher-efficiency perovskites will require durable, low-defect transparent conductors, supporting baseline ITO volumes.

Growth of Smart-Glass and Touch-Interface Devices

Electrochromic window retrofits in commercial real estate are scaling as building owners target 30-40% HVAC savings. These systems employ ITO-coated edges to distribute voltage uniformly across large glazing panes. Automotive sunroofs and privacy glass adopt similar structures, expanding the indium tin oxide market across mobility platforms. In consumer electronics, projected-capacitive touch screens have been the standard for more than a decade, and total sensor area is rising as foldable devices add secondary panels. Even with silver-nanowire pilots, mass producers continue to specify ITO for its stable supply chain and established reliability testing protocols.

EV Battery Tabs Using Ultra-Thin ITO Coatings

Pack designers place temperature-sensing ITO films on battery tabs to detect hotspots quickly, improving safety and extending life. LG Display’s 40-inch automotive cockpit integrates local-dimming technology that lowers heat buildup, highlighting cross-overs between display and thermal management know-how. Printed sensor suppliers forecast a USD 960 million addressable market by 2034 for transparent heaters applied to LiDAR domes and windshield areas. Although carbon-based heaters show promise, the crystalline nature of sputtered indium tin oxide delivers the low haze and high power density required for automotive homologation.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High indium price volatility and supply risk | -0.7% | Global, with particular impact on cost-sensitive applications | Short term (≤ 2 years) |

| Availability of low-cost substitutes | -0.5% | Global, accelerated adoption in flexible electronics markets | Medium term (2-4 years) |

| Increasing recycling mandates lowering virgin target demand | -0.3% | EU and North America leading, gradual global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Indium Price Volatility and Supply Risk

Indium prices rose nearly 13% in early-2025 after China introduced export licensing on several indium compounds. Because 75-80% of primary indium is recovered as a zinc by-product, mines cannot quickly boost output when spot demand spikes, leaving refiners dependent on inventories. The United States started a Section 232 study to determine whether imports of refined indium threaten national security, signaling possible tariffs or stockpiling measures. Smelters in Korea and Canada are examining residue leaching to lift recoveries, while brand-owners negotiate long-term contracts to lock in allocation. These strategies cap, but do not eliminate, cost unpredictability for indium tin oxide industry participants[2]U.S. Department of Commerce, “Notice of Section 232 Investigation on Critical Mineral Imports,” commerce.gov .

Commercialization of Low-Cost Substitutes

Silver and copper nanowire films now match ITO sheet resistance at sub-60 Ω/□ with over 90% transmittance, and roll-to-roll coating lines have surpassed 100 m/min, reducing unit costs. Hybrid stacks combining nanowires with carbon nanotubes further lower material spend and enhance crease tolerance. Molybdenum-doped indium oxide shows double the conductivity of classical ITO using less indium, appealing to display fabs aiming to conserve critical metals. Polymer conductors such as PBDF synthesized in ambient air reach 1.0 × 10^4 S/cm, but long-term UV stability remains under evaluation. Broad commercialization of these options could divert demand away from traditional indium tin oxide market applications in flexible form-factors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technique: Sputtering Keeps the Lead While Alternatives Scale

Sputtering dominated the indium tin oxide market in 2025 with a 74.62% revenue share, underpinned by process maturity and superior film homogeneity. Rotary cathode upgrades cut arcing events, enhancing target utilization and lowering cost per square meter. Some producers deploy bilayer sputtering—an oxygen-lean seed film for conductivity topped by an oxygen-rich cap for optical clarity—to balance performance and throughput. Other techniques, including spray pyrolysis and chemical vapor deposition, together are projected to clock a 5.12% CAGR to 2031 as flexible substrates demand lower-temperature processing. These routes appeal to start-ups manufacturing foldable displays where substrate heat budgets cannot exceed 200 °C.

Electron-beam evaporation keeps a foothold in niche optics requiring ultra-high vacuum purity. JX Advanced Metals’ Mesa, Arizona plant expansion illustrates OEM efforts to localize sputtering target supply chains amid geopolitical pressures. Research on in-situ plasma cleaning of polymer webs may further bridge efficiency gaps between sputtering and atmospheric spray methods, suggesting a gradual, not abrupt, diversification of deposition choices.

By Application: Optoelectronics Holds Share as Photovoltaics Accelerate

Optoelectronics retained 47.12% of 2025 revenue thanks to continuous smartphone, TV, and notebook production. The indium tin oxide market size for optoelectronics is forecast to expand at a steady 3.78% compound rate, supported by the shift to larger, higher-refresh OLED panels. In contrast, photovoltaic cells are positioned for a faster 5.02% CAGR as tandem architectures push transparent electrode quality requirements. Developers of perovskite-silicon stacks specify <15 Ω/□ sheet resistance alongside 92% visible transmittance, thresholds that established ITO sputtering lines already meet.

Wearables and augmented-reality optics form a smaller but fast-growing tranche, demanding durable coatings that can flex thousands of cycles. Battery inhibitor films and EMI shielding in high-frequency IC packaging represent emerging slivers where thin, low-stress ITO layers outperform thicker metallic meshes. Across segments, incremental substitution by conductive polymers is forecast to remain below 5% of revenue through 2031, keeping indium tin oxide market share intact in mainstream uses.

By End-User Industry: Automotive Demand Builds Momentum

Consumer electronics generated 50.74% of overall 2025 consumption. Despite lengthening smartphone replacement cycles, average display area per device is increasing, stabilizing unit ITO usage. Automotive displays, instrument clusters, and head-up projections are now rolling off OEM lines at higher diagonals, propelling a 5.06% CAGR in the segment. The indium tin oxide market size for automotive screens could exceed USD 345.6 million by 2031 if current integration roadmaps hold.

Buildings adopt electrochromic façades to meet tightening energy codes, and several EU retrofit subsidies reimburse smart-glass costs. Renewable-energy developers use ITO in advanced thin-film modules and concentrator optics. Aerospace remains a specialized buyer, valuing radiation-hard coatings for cockpit avionics even at premium pricing. Across industries, sustainability initiatives encourage take-back of coated glass and photovoltaics, reinforcing closed-loop supply ambitions.

Geography Analysis

Asia-Pacific’s 55.68% revenue stake is anchored in its vertically integrated display and solar ecosystems. China alone is projected to control 76% of global OLED capacity by 2025, and producers such as BOE operate fabrication parks that co-locate glass melting, target bonding, and recycling units. Korea lags in volume but leads in process innovation, while Japan supplies high-purity sputtering targets and mask sets. Regional growth of 4.82% CAGR is forecast despite China’s 2025 export licensing, as domestic recycling and Southeast Asian back-end assembly mitigate outward flow risks.

North America is balancing demand growth with critical-mineral security programs. New sputtering-target factories in Arizona and planned indium recycling hubs in Ontario aim to shorten supply lines for semiconductor and automotive customers. The U.S. Inflation Reduction Act’s EV incentives indirectly lift ITO usage via domestic car-maker display upgrades. Europe’s Critical Raw Materials Act targets 10% domestic sourcing of strategic metals by 2030, spurring feasibility studies for secondary indium extraction from zinc smelter residues in Belgium and Bulgaria. Smart-glass mandates in revised Energy Performance of Buildings Directive will further raise regional consumption.

Smaller yet promising markets in South America and the Middle East leverage abundant solar resources. Brazil’s distributed solar auctions stipulate local content requirements that favor regional ITO coating partners, while Saudi Arabia’s NEOM project specifies electrochromic façades across key zones. Limited local target manufacturing still necessitates Asia-Pacific imports, but joint ventures with Japanese and Korean producers are under negotiation to add sputtering capacity near end-users.

Competitive Landscape

The indium tin oxide market remains moderately fragmented. The five largest suppliers control roughly 62% of target shipments, a level that confers pricing discipline yet leaves room for niche entrants. Leading companies integrate back to refining, ensuring raw-metal availability and offering customers stable contracts indexed to zinc smelter output. Continuous R&D funding focuses on longer-life rotary targets, oxygen-tailored bilayer stacks, and low-temperature deposition chemistries.

Alternative-material challengers raise competitive pressure in flexible electronics but have yet to secure equal long-term reliability data for large-area applications. Strategic cooperation between display makers and material startups accelerates pilot deployments; for instance, automotive OEMs are testing hybrid nanowire-ITO laminates to reduce reflection in curved dashboards. Environmental, social, and governance criteria influence procurement: recyclability certifications and carbon-intensity disclosures are becoming standard in supplier qualification. Geopolitical uncertainty around indium exports is pushing Western firms to dual-source targets from Korea and Canada while exploring secondary recovery from spent photovoltaic glass.

Innovation pipelines include nanoscale indium dispersions for antistatic coatings and selective-area chemical vapor deposition enabling patterned electrodes without photoresist waste. Companies that can provide turnkey sputtering lines, in-house recycling, and co-engineered electrode stack designs are best positioned to capture future growth, especially in automotive and building-integrated photovoltaics.

Indium Tin Oxide Industry Leaders

Indium Corporation

Umicore

MITSUI MINING & SMELTING Co.,LTD.

Nitto Denko Corporation.

ENAM Optoelectronic Material

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: 3M joined the US-JOINT Consortium, a collaboration of 12 semiconductor suppliers committed to advancing semiconductor technology, with a particular emphasis on packaging and back-end processing. The consortium plans to inaugurate its new R&D facility in Silicon Valley in 2025. This R&D effort is expected to drive the growth of the indium tin oxide market.

- February 2025: China's Ministry of Commerce and General Administration of Customs implemented export controls on indium-related materials, including indium tin oxide, requiring exporters to obtain permission from the competent commercial departments. This regulatory change significantly impacts global supply chains and reflects China's strategic control over critical materials essential for electronics and coating applications.

Global Indium Tin Oxide Market Report Scope

The Indium Tin Oxide Market report include:

| Sputtering Deposition |

| Electron-Beam Evaporation |

| Other Techniques (Spray Pyrolysis, Chemical Vapour Deposition (CVD)) |

| Optoelectronics |

| Photovoltaic Cells |

| Battery Inhibitors |

| Other Applications (Wearables and Flexible Electronics, etc.) |

| Consumer Electronics |

| Renewable Energy |

| Automotive and Transportation |

| Building and Construction |

| Aerospace and Defence |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Technique | Sputtering Deposition | |

| Electron-Beam Evaporation | ||

| Other Techniques (Spray Pyrolysis, Chemical Vapour Deposition (CVD)) | ||

| By Application | Optoelectronics | |

| Photovoltaic Cells | ||

| Battery Inhibitors | ||

| Other Applications (Wearables and Flexible Electronics, etc.) | ||

| By End-User Industry | Consumer Electronics | |

| Renewable Energy | ||

| Automotive and Transportation | ||

| Building and Construction | ||

| Aerospace and Defence | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Indium Tin Oxide Market size?

The indium tin oxide market size is valued at USD 1.92 billion in 2026.

How fast is the indium tin oxide market expected to grow?

It is projected to record a 4.23% CAGR between 2026 and 2031, reaching USD 2.36 billion.

Which end-use sector drives the highest ITO consumption today?

Consumer electronics holds the leading 50.74% share, anchored by smartphones, TVs, and tablets.

Why is Asia-Pacific so dominant in the ITO supply chain?

The region combines most of the world’s OLED panel capacity, solar module output, and sputtering-target manufacturing infrastructure.

Page last updated on: