Aroma Chemicals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.1 Billion |

| Market Size (2031) | USD 6.38 Billion |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aroma Chemicals Market Analysis by Mordor Intelligence

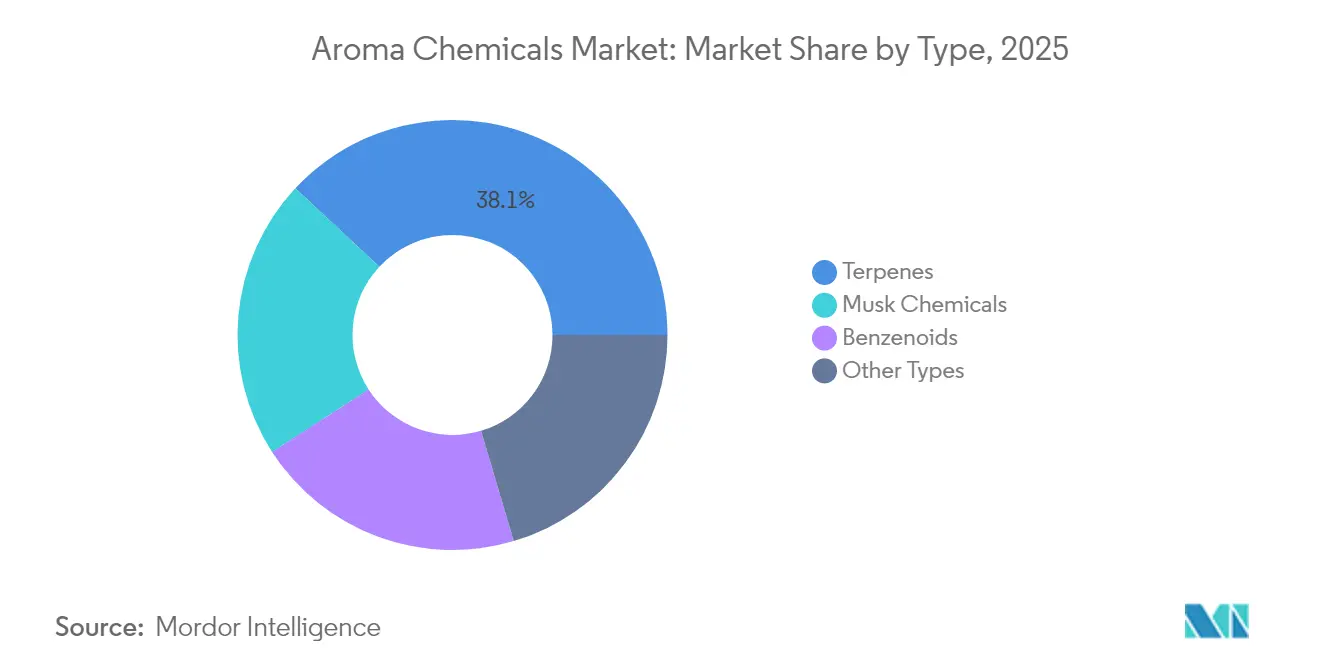

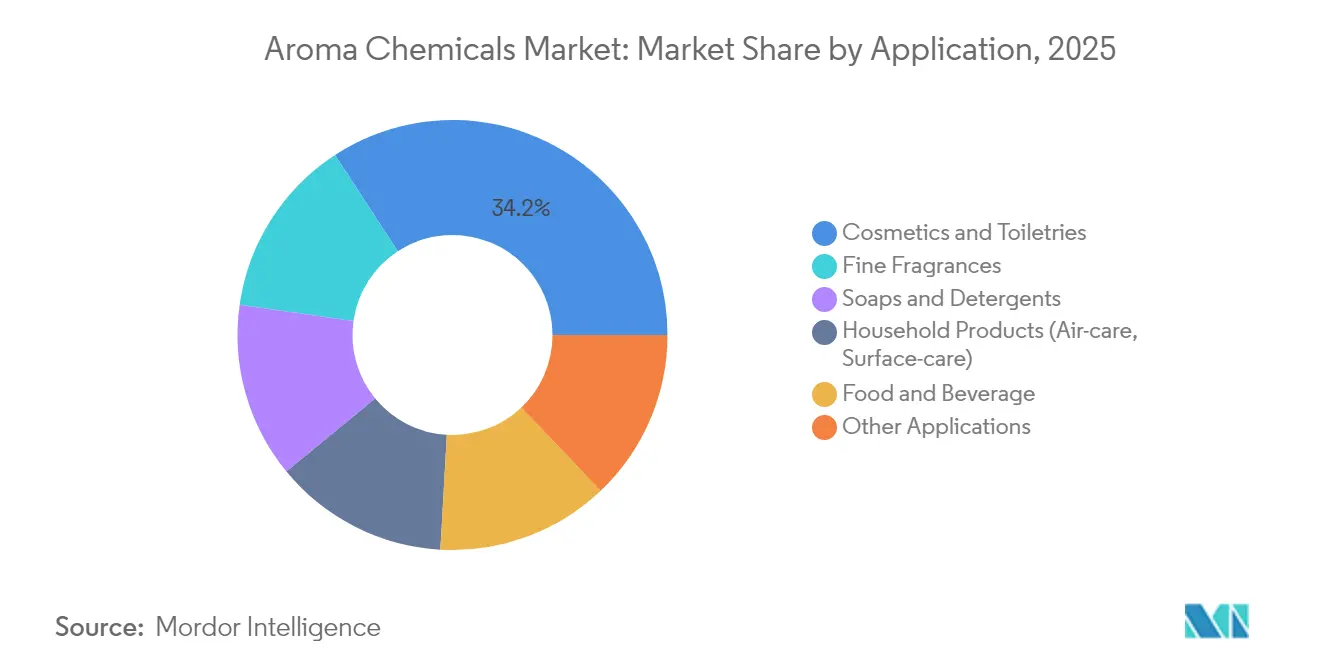

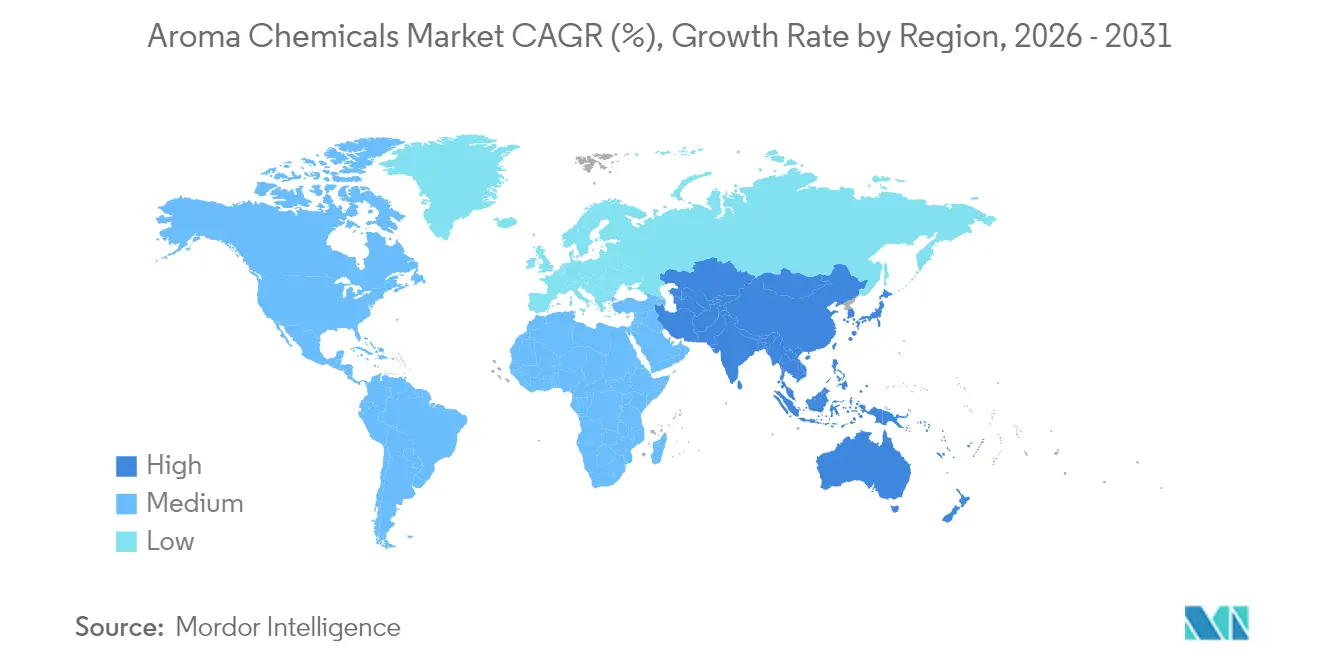

The Aroma Chemicals Market size was valued at USD 4.88 billion in 2025 and estimated to grow from USD 5.1 billion in 2026 to reach USD 6.38 billion by 2031, at a CAGR of 4.58% during the forecast period (2026-2031). Tightening safety regulations and the rapid commercialization of fermentation-based production methods are reshaping cost structures while answering the consumer push for sustainable, nature-identical ingredients. Terpenes keep their lead because microbial platforms can now deliver limonene, santalene, and related molecules at a competitive scale, anchoring 38.40% of 2024 revenue. Musk chemicals, buoyed by fourth-generation alicyclic variants, post the fastest trajectory at 5.05% CAGR as perfumers seek high-performance and readily biodegradable fixatives. On the demand side, cosmetics and toiletries absorb 34.56% of global volumes, while fine fragrances grow the quickest at 5.23% CAGR owing to premiumization and niche-brand proliferation. Asia Pacific captures the largest regional slice at 38.95% and advances at 5.76% CAGR, helped by China’s double-digit fragrance uptake and India’s specialty-chemicals investments.

Key Report Takeaways

- By product type, terpenes led with 38.05% aroma chemicals market share in 2025; musk chemicals are set to expand at a 4.98% CAGR to 2031.

- By application, cosmetics and toiletries held 34.20% revenue share in 2025, whereas fine fragrances are projected to register a 5.14% CAGR through 2031.

- By geography, Asia Pacific commanded 38.60% of the aroma chemicals market size in 2025 and is forecast to grow at 5.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aroma Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from fine-fragrance formulators | +1.20% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid growth of natural & “clean-label” personal-care brands | +1.80% | Global, led by North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Expansion of multifunctional home-care product lines | +0.90% | Global, with strongest growth in APAC & Latin America | Medium term (2-4 years) |

| Biotechnological production lowering unit costs | +1.10% | Global, with early adoption in North America & Europe | Long term (≥ 4 years) |

| Growing adoption of aroma chemicals in functional foods & beverages | +0.70% | Global, with fastest growth in APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Fine-Fragrance Formulators

Premium fragrance houses are raising performance specifications, prompting a shift from commodity notes to complex molecules that deliver long-lasting sillage and distinctive olfactory signatures. Compounds such as Helvetolide and Romandolide underpin this evolution by combining strong blooming properties with improved biodegradability. As luxury brands widen bespoke collections, formulators require differentiated musks and specialty aldehydes, amplifying order volumes per launch. Suppliers able to co-create accords through rapid prototyping hold a competitive edge, further stimulating the aroma chemicals market.

Rapid Growth of Natural & Clean-Label Personal-Care Brands

Seventy percent of Swedish consumers actively look for ecolabels when purchasing cosmetics, signaling a broader appetite for transparency. Brands respond by reformulating toward fermentation-derived terpenes and bio-vanillin, reducing reliance on petro-based inputs. L’Oréal’s pledge to secure 95% sustainable ingredients by 2030 epitomizes corporate commitments that are cascading throughout supplier networks. The result is brisk procurement of certified-natural aroma molecules, bolstering long-term demand.

Expansion of Multifunctional Home-Care Product Lines

Household-care brands are fusing cleaning efficacy with curated sensory profiles. Encapsulation technologies that protect volatile notes until activation allow detergents to release freshness during use, lifting customer satisfaction and brand loyalty. Givaudan raised its encapsulation capacity in Mexico by 40%, underscoring the scale of investments tied to this growth lane[1]“Givaudan Increases Encapsulation Capacity,” Givaudan, givaudan.com. Because stability requirements are stringent, innovation favors suppliers with deep formulation know-how, sustaining value creation within the aroma chemicals market.

Biotechnological Production Lowering Unit Costs

Fed-batch fermentation in engineered Saccharomyces cerevisiae now yields limonene and other terpenes at titers that rival plant extraction, slashing raw-material risk and shrinking carbon footprints[2]Sijie Chen et al., “Microbial Production of Terpenoids,” International Journal of Molecular Sciences, mdpi.com . Genomatica’s commercial deployment of bio-based 1,4-butanediol confirms the scalable economics of precision fermentation in adjacent chemical value chains. Early adopters can internalize these cost savings, reinforcing price discipline and margin stability over the forecast window.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petrochemical feedstock prices | -0.80% | Global, with highest impact in regions dependent on naphtha feedstock | Short term (≤ 2 years) |

| Tightened allergen-labeling rules in Europe and North America | -1.10% | Europe & North America, with spillover effects globally | Medium term (2-4 years) |

| Supply-chain risk for natural precursors | -0.60% | Global, with concentration in regions dependent on natural ingredients | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Petrochemical Feedstock Prices

Rapid swings in naphtha and natural-gas liquids prices compress margins for producers dependent on petro baselines. Firms lacking dual-feedstock flexibility face squeezed spreads and unplanned downtime, heightening short-term cost variability. Scale operators cushion volatility through strategic hedging and balanced cracker configurations, yet sustained turbulence nudges buyers toward bio-based alternatives, marginally trimming the aroma chemicals market CAGR.

Tightened Allergen-Labeling Rules in Europe & North America

The European Union’s Regulation 2023/1545 compels the declaration of 81 allergens at trace thresholds, forcing widespread reformulation and new stability testing. The International Fragrance Association’s 51st Amendment adds 48 fresh restrictions and modifies 11 others, intensifying compliance workloads[3]International Fragrance Association, “IFRA Standards 51st Amendment,” ifrafragrance.org . Concurrent alignment under the US MOCRA regime points to global standardization, which increases documentation costs and narrows viable ingredient palettes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Terpenes Extend Leadership Through Biotech Scaling

Terpenes accounted for a 38.05% aroma chemicals market share in 2025, translating into the single largest contributor to revenue. Producers capitalize on fermentation routes that convert sugars into limonene, santalene, and related frameworks, cutting extraction losses and stabilizing supply. The aroma chemicals market size for terpenes is projected to widen steadily alongside cost declines and the broad applicability of these backbones across fine fragrance, cosmetics, and household care. Musk chemicals remain the fastest-growing cohort, advancing at 4.98% CAGR through 2031 as alicyclic innovations deliver low-bioaccumulation profiles desirable under new safety regimes. Benzenoids and specialty aldehydes maintain relevance for their structural roles in sophisticated accords, even though their growth tempo is less pronounced.

Second-tier types such as specialty ketones cater to niche effects like metallic freshness or marine nuances. Their premium positioning protects average selling prices, helping suppliers diversify margin mix. The technological race is concentrated on route efficiency: enzymatic cascades coupled with solvent-free isolation lower energy draws and reinforce environmental credentials. Such advances ensure terpenes retain primacy, while leaving white-space pockets for agile producers willing to scale novel molecules.

By Application: Cosmetics Dominate While Fine Fragrance Accelerates

Cosmetics and toiletries absorbed 34.20% of global volumes in 2025, supported by resilient demand for skin-care, hair-care, and color-cosmetic items that rely on pleasant olfactory cues for brand distinction. Fine fragrance achieved the briskest expansion at 5.14% CAGR to 2031, benefitting from artisanal perfumery, direct-to-consumer launches, and travel-retail rebounds. This segment’s appetite for high-impact musks and captive molecules locks in higher margins, underpinning supplier profitability. In soaps and detergents, innovation hinges on encapsulation and malodor counteraction, providing incremental yet stable growth.

Household products now integrate mood-enhancing scents with antibacterial performance, a trend that keeps average dosage levels per unit high and supports volume throughput. Functional foods and beverages burnish consumer acceptance of protein-rich recipes, using aroma chemicals to refine texture perception and scent congruence. Collectively, these demand centers reinforce a balanced outlook, cushioning the aroma chemicals market against cyclicality in any single downstream sector.

Geography Analysis

Asia Pacific’s 38.60% revenue grip in 2025 positions the region as both the largest consumer and the primary production hub for the aroma chemicals market. Rising disposable incomes in China, Indonesia, and Vietnam nurture fragrance adoption that remains well below Western saturation, leaving sizeable headroom. Governments support bio-manufacturing parks, lowering entry barriers for fermentation-driven start-ups. These forces underpin the forecast 5.68% regional CAGR to 2031.

North America leverages advantaged ethane feedstock and deep R&D ecosystems. Producers concentrate on high-purity specialties and controlled-release systems, serving premium segments that demand tight specification control. Regulatory clarity under MOCRA drives proactive portfolio audits, ensuring steady but measured expansion. Europe continues to exert regulatory leadership, with stringent allergen thresholds shaping global formulation norms. Premium luxury brand clusters in France and Italy secure demand for captive aroma ingredients, offsetting relative market maturity.

Latin America benefits from urbanization and premiumization trends in Brazil and Mexico, though currency fluctuations occasionally temper import appetite. The Middle East & Africa see gradual uptake, with the Gulf Cooperation Council advancing fragrance-focused retail and local contract manufacturing. Although these two regions contribute a relatively small share of global sales, investors focus on them for long-term diversification, recognizing the growing middle class and retail channels linked to tourism. Overall, regional dynamics sustain growth breadth, moderating exposure to single-market shocks.

Mordor Intelligence provides coverage of the aroma chemicals market across other key regional markets, including North America, Europe, and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Value Chain Analysis

The aroma chemicals value chain starts with diversified feedstocks: petrochemical intermediates for many benzenoids and specialty molecules, paper-industry by-products such as crude sulphate turpentine (CST) as a circular input stream for terpene derivatives, and increasingly bio-based routes where sugars and other renewable substrates feed fermentation for nature-identical molecules. Upstream variability, particularly for natural precursors, continues to shape procurement strategy. Compliance requirements such as the International Fragrance Association (IFRA) Standards and the IFRA Code of Practice also influence purity specifications, restricted-use profiles, and documentation for both manufacturing and downstream formulation.

Conversion spans multi-step synthesis, separation, and quality assurance. Scale and vertical integration are used to stabilize supply and consistency. Capacity additions reflect this integration trend: in April 2026, BASF commissioned world-scale menthol and linalool production in Ludwigshafen, Germany, alongside a new citral plant in Zhanjiang, China, widening supply footprints across Europe and Asia. Distribution typically follows direct supply to multinational fragrance and flavor houses, alongside regional distributors and specialized warehouses in hubs such as Mumbai, India, where global producers reach local formulators in personal care, home care, and food and beverage.

Competitive Landscape

The aroma chemicals market showcases moderately consolidated concentration. The top five firms - BASF SE, Givaudan, Symrise, dsm-firmenich, and IFF - maintain their dominance through extensive captive libraries, well-established customer co-development frameworks, and vertically integrated supply chains spanning both petrochemical and bio-based routes. Nonetheless, regulatory churn and sustainability mandates raise operating expenses, giving nimble mid-sized players an opening to carve share through focused innovation and regional agility.

Technology is the frontline of differentiation. Givaudan’s Carto AI and Symrise’s Philyra 2.0 harness machine learning to compress development cycles and tailor accords with precision. Biotech investments accelerate: dsm-firmenich’s upcoming Parma facility will elevate capacity in concentrated powder flavors and reaction blends by 2027, reflecting strategic bets on natural-label solutions. M&A activity remains selective, targeting fermentation specialists and natural-extract processors that cement raw-material resilience.

Pricing power faces headwinds from ongoing investigations into suspected cartel behavior, particularly within Europe. Customers diversify sourcing to mitigate concentration risk, spotlighting regional challengers such as Hindustan Mint & Agro Products and others. These firms exploit cost-effective Indian manufacturing ecosystems to supply terpene derivatives at competitive rates. In the coming five years, companies capable of combining sustainable feedstocks with digital formulation expertise while effectively navigating global compliance landscapes will dominate the competitive landscape.

Aroma Chemicals Industry Leaders

BASF SE

Givaudan SA

Symrise AG

Firmenich International SA

International Flavors & Fragrances (IFF)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven reformulation and sustainability commitments are creating room for differentiated molecules that address allergen concerns and improve environmental profiles, while keeping performance requirements in view. BASF's June 2026 launch of Micadelva, positioned as a non-allergenic citrus alternative to orange terpenes, is a concrete example of product development aligned with Safe-by-Design thinking, and it supports substitution in applications where allergen labeling and restricted-use constraints narrow the usable ingredient palette.

Supply localization and fermentation-linked pathways are also widening opportunities for new capacity and partnerships in fast-growth manufacturing corridors. BASF's April 2026 capacity starts for menthol and linalool in Ludwigshafen and citral in Zhanjiang illustrate continued investment in high-volume aroma intermediates, while Privi Speciality Chemicals reaffirmed expansion to 54,000 MTPA by June 30, 2026, supporting additional sourcing options for global buyers. On the technology front, Lallemand Bio-Ingredients introduced Hevani (March 2026), a yeast-fermented vanillin at 98% purity, reinforcing demand for fermentation-derived aroma molecules that fit clean-label narratives and reduce dependence on crop-linked supply risk.

Recent Industry Developments

- June 2026: BASF launched Micadelva, a non-allergenic citrus alternative to orange terpenes under its Safe-by-Design concept. The product targets formulators managing allergen labeling and restricted-use pressures while maintaining citrus performance, expanding substitution options in fragrance and flavor formulations.

- April 2025: BASF Aroma Ingredients introduced L-Menthol FCC with a reduced Product Carbon Footprint claim compared with conventional equivalents. The initiative reinforced the shift toward quantified sustainability attributes in aroma portfolios, influencing procurement decisions among personal care and home care customers.

- March 2024: dsm-firmenich inaugurated two production facilities in Castets, France, for perfumery ingredients, including a unit for pine-based ingredients and a plant for the biodegradable musk Habanolide. The commissioning strengthened European supply of performance musks and bio-based ingredient streams, supporting reformulation needs tied to evolving safety and biodegradability requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the aroma chemicals market is defined as the value of aroma ingredients sold as chemical compounds that are used to deliver smell or taste in finished products, across key consumer and industrial applications, and measured in revenue terms.

Scope exclusions: This sizing does not include finished fragrances, essential oils sold as-is, or downstream consumer goods that contain aroma ingredients.

Segmentation Overview

- By Type

- Terpenes

- Benzenoids

- Musk Chemicals

- Other Types

- By Application

- Soaps and Detergents

- Cosmetics and Toiletries

- Fine Fragrances

- Household Products (Air-care, Surface-care)

- Food and Beverage

- Other Applications

- By Geography

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- Turkey

- South Africa

- Rest of Middle East and Africa

- Asia Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial market map and to set realistic bounds on demand, supply, and trade flows for aroma ingredients. We reviewed public sources such as UN Comtrade trade statistics, USITC and Eurostat trade releases, the US EPA chemical information pages, and publications from bodies such as IFRA and FEMA to understand usage rules and how application pull typically shows up in end-use buying.

Along with these, we used company annual reports, investor presentations, and reputable press coverage to validate capacity additions, product-mix shifts, and pricing direction. Where needed, paid subscriptions that support company financials and intelligence, patent landscapes, and shipment-level trade screening were used to cross-check totals and fill gaps around smaller privately held suppliers. The sources listed above are illustrative only, and many other public documents were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with manufacturers, distributors, and downstream users that buy aroma ingredients for soaps, personal care, home care, fine fragrance, and flavor applications. Inputs were used to confirm which chemistries are actually sold into each end use, the typical pricing structure by purity and grade, and how demand shifts with consumer preferences and regulation across major regions. Assumptions were revisited when responses indicated a mismatch between intended use and actual ingredient purchasing patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 46% |

| Mid tier: 43% | Functional/Unit leaders: 29% | EMEA: 35% |

| Smaller Players: 21% | Managers: 59% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool reconstruction where regional consumption of fragrance and flavor end uses is translated into aroma ingredient demand using usage factors, product mix shares, and observed import-export signals, and then it is adjusted for local production and net trade. Only after the demand picture is built, selective bottom-up checks are run using supplier revenue splits, sampled price bands, and volume proxies to see if the total stays within a realistic range.

Key inputs used in the model include application-level consumption trends in soaps and detergents, cosmetics and toiletries output, fine fragrance launches, and food and beverage flavor demand, followed by trade movements for key aroma intermediates, and price movement indicators for feedstocks that influence benzenoids and terpene chains. Additional checks were added using regulatory restrictions that shift permissible molecules, and substitution patterns between natural, synthetic, and natural-identical options when price gaps widen.

Forecasting was done using scenario analysis supported by simple time-series smoothing for stable applications, and then the outlook was stress-tested with interview feedback on capacity expansion timing, expected pricing changes, and adoption of new compliant molecules. When some bottom-up company data was missing, gaps were handled by applying peer-based revenue intensity ranges by region and chemistry group, which were then rechecked against trade and demand signals.

Data Validation & Update Cycle

Validation is done through repeated triangulation across demand signals, supply indicators, and pricing direction so the model does not rely on a single data series. Outliers are flagged when growth rates diverge from end-use production trends, when trade balances shift without a matching capacity event, or when implied pricing moves outside the ranges confirmed in primary discussions.

Before sign-off, the work is reviewed in steps, starting with assumption checks, followed by year-by-year variance review, and then a final pass that confirms that totals reconcile across regions and applications. The report is refreshed annually, and interim updates are triggered when major regulatory actions, feedstock shocks, or large capacity changes materially alter market direction. Prior to delivery, we run a fresh review of key indicators so clients receive the most current view possible.

Mordor Intelligence's Aroma Chemicals Market Size Measured Against Other Published Estimates

Published market sizes for aroma chemicals often do not match because the scope lines are drawn differently and the underlying inputs are not always built from the same demand pool. Differences also come from the base year used, how prices are converted into USD, and whether estimates are refreshed after feedstock swings and regulation-led formulation changes.

Finished fragrances and essential oils sold as final blends sit outside Mordor Intelligence's scope, which is why some broader estimates that bundle these adjacent categories can show a higher starting value. Other gaps usually come from using aggressive price-growth assumptions for high-value musks, mixing natural and synthetic volumes without grade-level price logic, or applying a single CAGR to all applications even when soaps and detergents behave very differently from fine fragrances.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.10 B (2026) | |

| Global Consultancy A | USD 6.51 B (2026) | Often reflects a broader definition that can fold in finished fragrance blends and a wider ingredient basket, and it may also apply higher ASP progression assumptions over the same year. |

| Industry Publisher B | USD 6.10 B (2024) | Uses an earlier base year and can mix natural, synthetic, and natural-identical values with different coverage rules, which makes back-casting to 2026 sensitive to currency timing and price inflation assumptions. |

The comparison shows that most of the spread is explained by what is counted as an aroma ingredient versus a finished blend, and by how pricing is carried forward year to year. By keeping the model tied to application demand signals, trade checks, and grade-linked pricing logic, the final number stays traceable to clear steps that can be repeated and reviewed.

Key Questions Answered in the Report

What is the current size of the aroma chemicals market?

The aroma chemicals market size stands at USD 5.1 billion in 2026, with expectations of reaching USD 6.38 billion by 2031.

Which product type holds the largest share?

Terpenes lead with 38.05% of global revenue because fermentation processes now deliver cost-effective and sustainable supply.

Which application is growing the fastest?

Fine fragrance is expanding at a 5.14% CAGR as consumers trade up to premium and niche scent portfolios.

Why is Asia Pacific the largest regional market?

Asia Pacific combines large-scale manufacturing, rising middle-class consumption, and supportive bio-manufacturing policies, resulting in a 38.60% share and a 5.68% CAGR outlook.

How are regulations influencing market dynamics?

EU allergen labeling, IFRA’s new ingredient limits, and looming US MOCRA rules compel extensive reformulation and favor suppliers with advanced R&D and transparent supply chains.

What technological change is most disruptive?

Biotechnological production that converts sugars into terpenes and musks is lowering unit costs and shrinking environmental footprints, reshaping competitive positions across the value chain.

Page last updated on: