India Aroma Chemicals Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

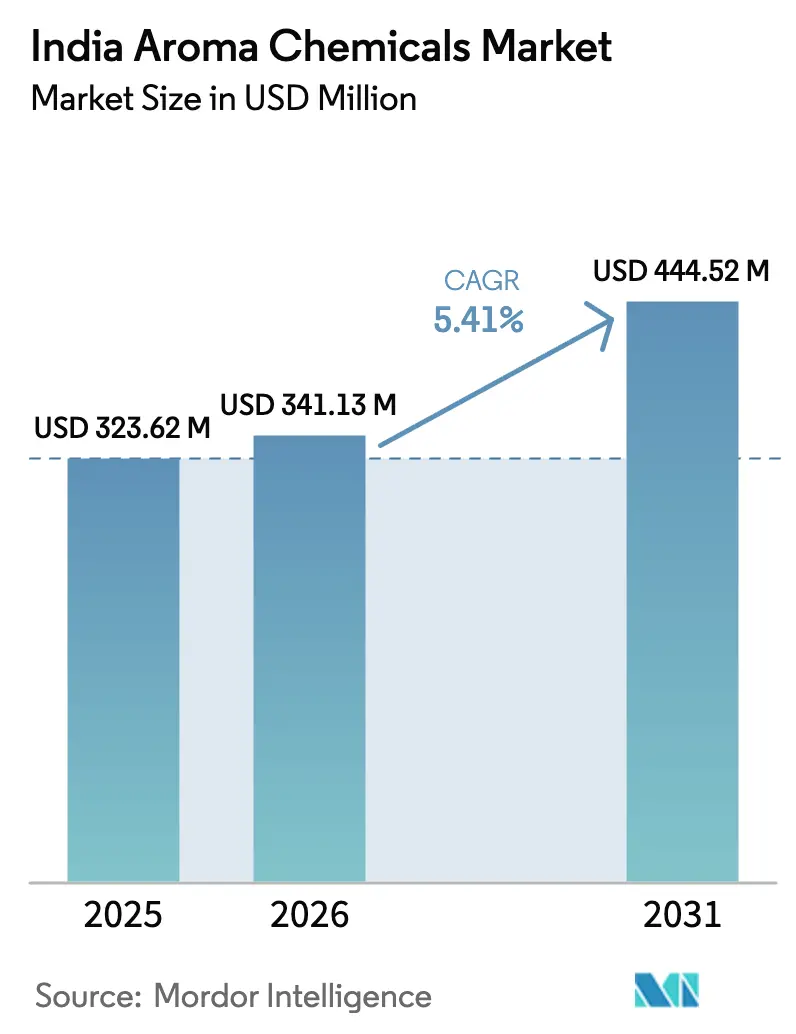

| Base Year Market Size (2025) | USD 323.62 Million |

| Market Size (2026) | USD 341.13 Million |

| Market Size (2031) | USD 444.52 Million |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

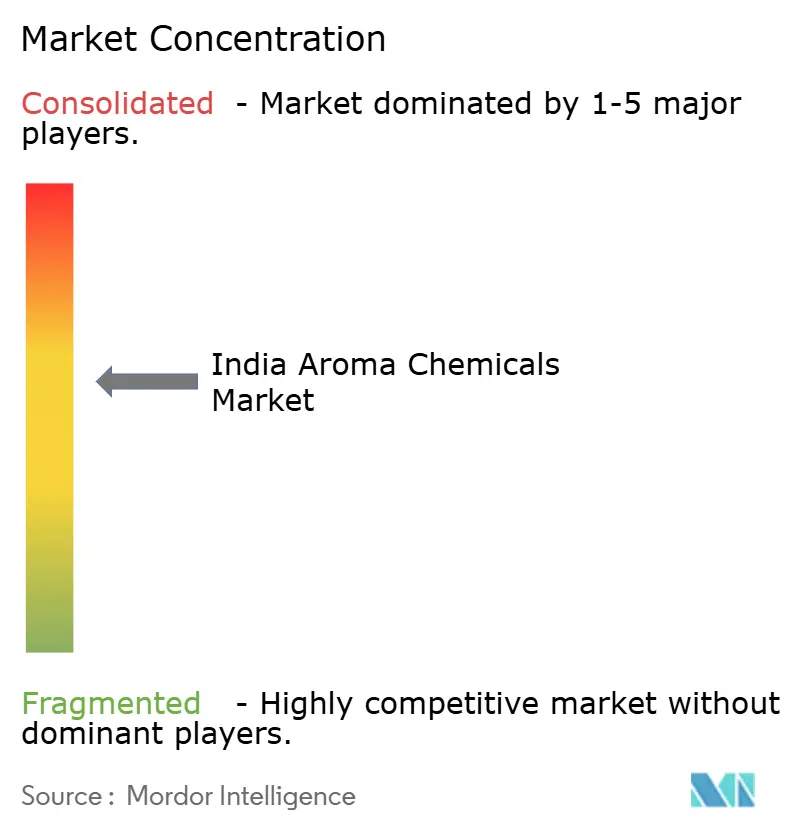

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Aroma Chemicals Market Analysis by Mordor Intelligence

The India Aroma Chemicals Market size was valued at USD 323.62 million in 2025 and estimated to grow from USD 341.13 million in 2026 to reach USD 444.52 million by 2031, at a CAGR of 5.41% during the forecast period (2026-2031). This steady trajectory reflects rising premiumization in beauty, home care, and functional food categories that lean heavily on specialized molecules. Domestic producers benefit from Gujarat’s integrated petrochemical corridors and Maharashtra’s proximity to consumer-goods formulators, allowing reliable feedstock access and quick turnaround on bespoke orders. Demand is supported further by sustained exports of “Other Organic Compounds,” coupled with Production Linked Incentive schemes that reward capacity additions and technology upgrades. At the same time, tightening waste-management rules and volatile crude prices encourage investments in biotechnology and circular feedstocks that cushion cost swings while aligning with customer sustainability agendas.

Key Report Takeaways

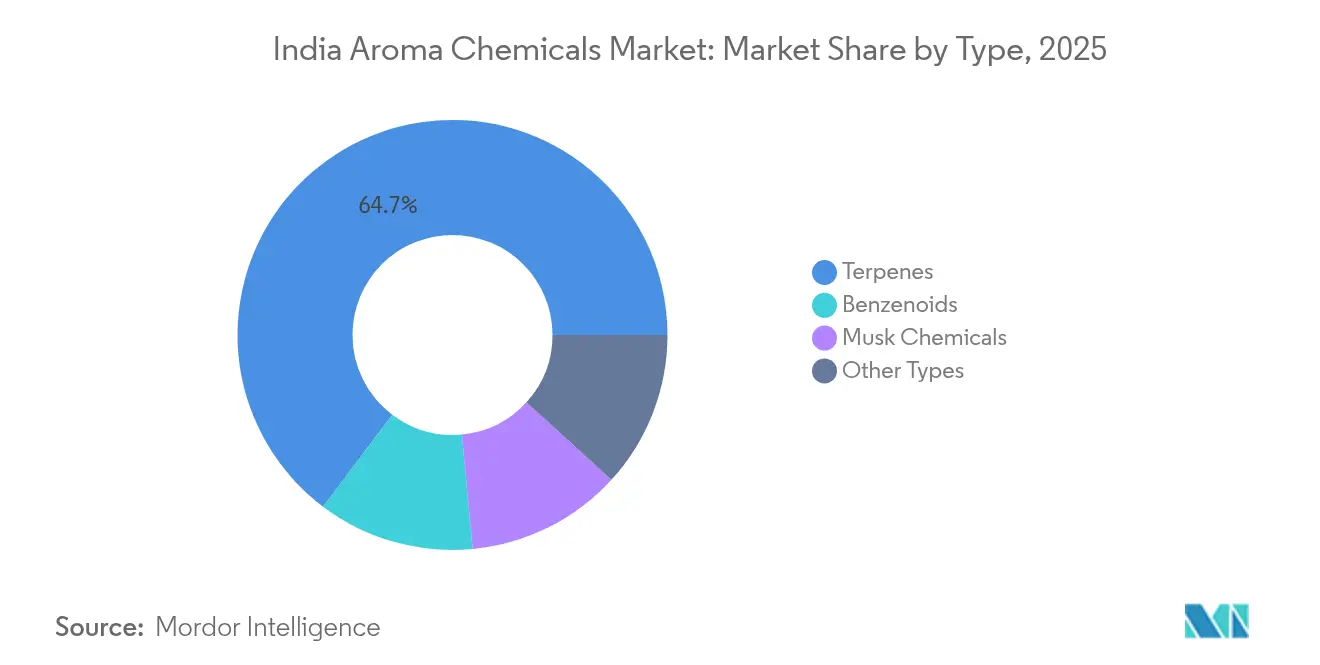

- By type, terpenes led with 64.72% revenue share of the India aroma chemicals market share in 2025; musk chemicals are projected to register the highest 5.94% CAGR through 2031.

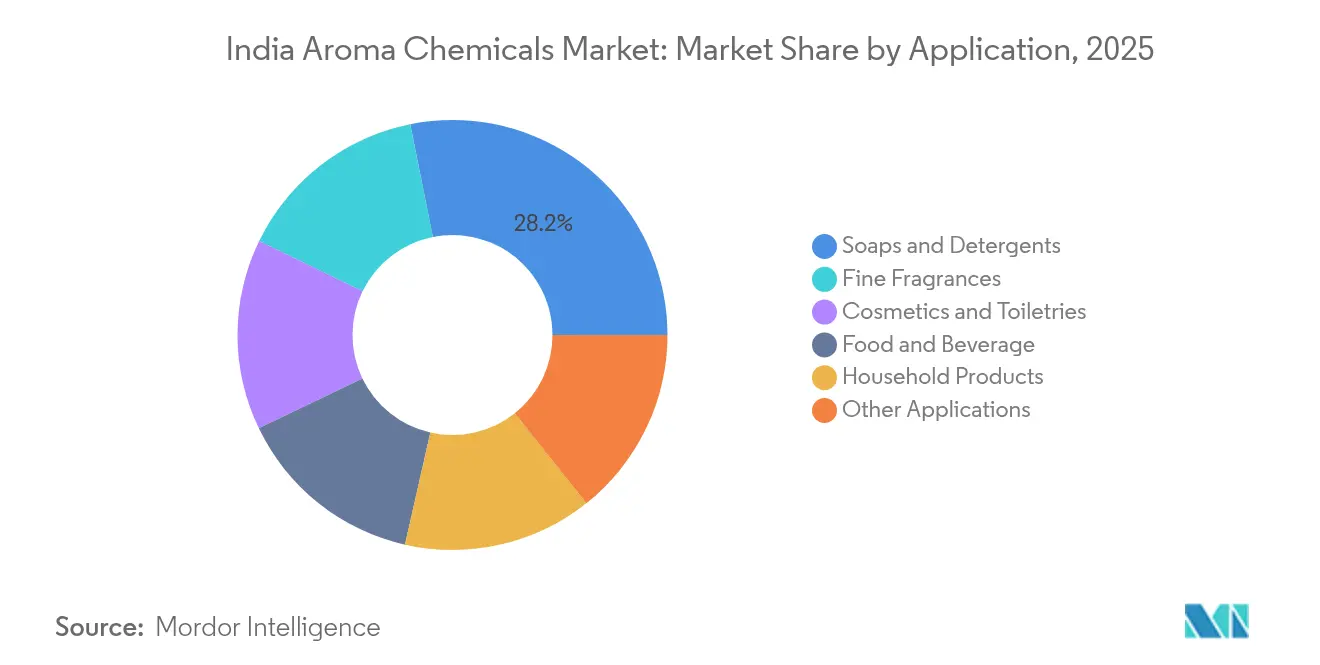

- By application, soaps and detergents accounted for 28.15% of the India aroma chemicals market size in 2025, while fine fragrances are advancing at a 5.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of India. The aroma chemicals market share in our global report expresses these relative weights.

India Aroma Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from fine-fragrance formulators | +1.8% | National, with concentration in Mumbai, Delhi, Bangalore premium markets | Medium term (2-4 years) |

| Rapid growth of natural and "clean-label" personal-care brands | +1.2% | National, with early adoption in urban centers and tier-1 cities | Medium term (2-4 years) |

| Expansion of multifunctional home-care product lines | +0.8% | National, driven by rural penetration and urban premiumization | Long term (≥ 4 years) |

| Growing adoption of aroma chemicals in functional foods and beverages | +0.6% | National, with strength in Maharashtra, Tamil Nadu food processing hubs | Long term (≥ 4 years) |

| Synthetic-biology production scaling rare aroma molecules | +0.4% | Gujarat, Maharashtra manufacturing clusters with biotech capabilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Fine-Fragrance Formulators

India’s fine-fragrance segment is growing at a 6.25% CAGR through 2030, outrunning other end uses as affluent consumers trade up to niche scents. Luxury beauty revenue is expected to reach USD 1.6 billion by 2028, signaling considerable headroom for complex aroma profiles requiring specialty terpenes, musks, and captive aldehydes. Givaudan’s South Asia arm recorded 20.9% like-for-like growth in 2024, while its Fragrance Ingredients division expanded 11.1%, underscoring sustained downstream pull for captive intermediates[1]Givaudan, “Full-Year 2024 Results,” givaudan.com. Mass players like Hindustan Unilever also emphasize fragrance-led SKU renovations, allowing domestic chemical suppliers to scale volume while moving up the value curve.

Rapid Growth of Natural and “Clean-Label” Personal-Care Brands

Clean-label momentum places biodegradable, botanically derived inputs over fossil-based synthetics in shampoos, lotions, and deodorants. Hindustan Unilever aims for 100% biodegradable ingredients by 2030, reshaping raw-material specifications and accelerating demand for terpene isolates from Indian flora. Symrise reached 95% biologically sourced raw materials in 2024, proving that large-scale natural supply chains can meet stringent quality thresholds. Indian extraction houses leverage abundant lemongrass, palmarosa, and mint feedstocks, positioning the India aroma chemicals market to capture premium volumes as global formulators search for traceable supply.

Expansion of Multifunctional Home-Care Product Lines

India’s liquid detergents, fabric conditioners, and surface cleaners rely on fragrance for scent and to signal cleaning efficacy and added benefits. Hindustan Unilever’s Home Care unit posted INR 21,900 crore revenue in FY 2024, with continued investment in premium aromatics for concentrated formats that must deliver olfactory punch at lower dosage. Quick-commerce channels now account for nearly 75% of e-grocery shipments, accelerating consumer trial of fragrance-enriched SKUs that command higher ticket sizes.

Growing Adoption in Functional Foods and Beverages

The USD 307.2 billion processed-food sector is projected to climb toward USD 470-535 billion by 2028, which widens the addressable opportunity for flavor molecules and masking agents. Food Safety and Standards Authority of India’s 2025 packaging code compels traceability, favoring established aroma-chemical suppliers with certified quality systems. Nutraceutical GST cuts to 5% starting September 2025 stimulate innovations in fortified snacks and drinks, often requiring tailored aromas to offset off-notes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petrochemical feedstock prices | -0.9% | National, with highest impact on Gujarat, Maharashtra manufacturing hubs | Short term (≤ 2 years) |

| Tightened allergen-labelling rules in Europe and North America | -0.7% | Export-oriented manufacturers, particularly Gujarat chemical clusters | Medium term (2-4 years) |

| Supply-chain risk for natural precursors | -0.6% | National, with concentration in botanical raw material sourcing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Petrochemical Feedstock Prices

Crude-linked raw materials dictate cost curves for benzenoids and aldehydes, creating margin pressure when oil spikes. Although India plans to raise petrochemical capacity from 257 MMTPA to 310 MMTPA by 2028, near-term fluctuations continue to unsettle working-capital cycles, especially for smaller processors lacking long-term contracts. Integrated players with captive naphtha crackers in Gujarat enjoy relative insulation and can leverage scale economies to sustain exports.

Tightened Allergen-Labelling Rules in Europe and North America

EU regulations now compel detailed disclosure for 80+ fragrance allergens, raising analytical testing and documentation costs. Indian exporters must update Safety Data Sheets and invest in trace-level quantification equipment or risk losing contracts from global FMCG (fast-moving consumer goods) majors. Compliance burdens may accelerate consolidation as niche producers struggle with overheads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Terpenes Dominate Through Natural Advantage

The India aroma chemicals market size for terpenes exceeded two-thirds of the overall value in 2025, reflecting dependable access to lemongrass, palmarosa, and mint crops in Uttar Pradesh, Rajasthan, and Tamil Nadu. Scale in steam distillation plus backward linkages with essential-oil exporters reduces unit costs, enabling competitive pricing in both domestic and overseas tenders. Benzenoids remain integral for volume exports, leveraging Gujarat’s refinery integration for toluene and benzene derivatives. Musk chemicals command higher margins because of consistent performance in fine fragrances, and their 5.94% CAGR signals the wallet shift toward premium olfactory compounds. Atul Ltd extends its portfolio with perfumery-grade geraniol isolated from palmarosa, illustrating synergy between natural extraction and synthetic upgrades.

Price-sensitive soap formulators still drive bulk terpene orders, yet emerging biotech routes for rare lactones could tilt value toward specialty molecules over time. ISO-driven quality norms plus Bureau of Indian Standards benchmarks reinforce India’s export credibility, sustaining market access to Europe, the United States, and Japan. Forward integration into reaction-controlled derivatives such as linalyl acetate helps hedge raw-material volatility and deepens customer stickiness.

By Application: Fine Fragrances Accelerate Amid Premiumization

Fine fragrances posted the highest 5.98% CAGR, fed by rising disposable income and retail expansion of niche perfume boutiques across metros. Although soaps and detergents hold 28.15% of the India aroma chemicals market share, the incremental revenue slope is steeper in premium spray and roll-on formats that command 3-5 times higher per-kilogram fragrance cost. Cosmetics and toiletries manufacturers boost olfactory signatures to fend off me-too products, pushing demand for captive aldehydes and proprietary accords. Food and beverage users integrate vanilla, citrus, and spice notes to elevate functional drinks and fortified snacks, widening the end-market base.

Household products, especially fabric conditioners, rely on long-lasting encapsulated scent boosters, driving adoption of polymer-bound aroma microcapsules. The India aroma chemicals market size tied to those encapsulated systems is projected to expand with quick-commerce adoption, which skews toward premium sachets and small packs that promise heightened sensory payoff.

Geography Analysis

Gujarat and Maharashtra collectively account for roughly 70% of India's Aroma Chemicals market capacity, benefiting from refinery integration, port access, and experienced talent pools. Ankleshwar, Dahej, and Vapi clusters in Gujarat offer common effluent treatment plants and shared utilities, shortening the time to market for greenfield units. The state contributes 50% of India’s overall chemical output and 33% of electronics-grade specialty chemicals, giving aroma manufacturers a robust ecosystem for feedstock and ancillary services. Maharashtra hosts Privi Speciality Chemicals near Mumbai’s shipping lanes, catering to premium global clients that demand shorter lead times and extensive technical documentation.

Southern states leverage biotechnology and agricultural diversity. Tamil Nadu houses fermenter capacity to switch between pharmaceutical APIs and aroma molecules, allowing agile production of yeast-derived terpenes. Karnataka nurtures a start-up ecosystem around synthetic biology, supported by venture capital and state incentives for clean chemistry. Northern belts such as Uttar Pradesh supply lemongrass and palmarosa oils that feed into terpene synthesis, while Odisha and Andhra Pradesh lure investment through coastal chemical parks with logistics tax breaks.

Export patterns reflect regional specialization: Gujarat plants focus on high-volume benzenoid shipments to detergent formulators in Southeast Asia and the Middle East, whereas Maharashtra units export narrow-cut musks and aldehydes to European perfumers. Emerging clusters in the east target ASEAN duty advantages under trade agreements, indicating a gradual diffusion of capacity beyond the western seaboard. Regulatory factors also influence siting decisions; Gujarat’s Petroleum, Chemicals & Petrochemicals Investment Region offers simplified environmental clearances, while stricter coastal zone norms in other states may extend project timelines.

Mordor Intelligence examines the aroma chemicals market across diverse other regional markets as well, including North America, Europe, and Asia.

Competitive Landscape

The Indian Aroma Chemicals market is consolidated. Process technology and sustainability are emerging battlegrounds. Players adopt continuous-flow reactors, solvent-recovery loops, and bio-based feedstocks to meet brand-owner decarbonization targets. Government incentives through Production Linked Incentive schemes accelerate capacity build-outs, driving roughly 12% CAGR across specialty chemicals. Export competitiveness hinges on consistent quality certifications (ISO 9001, FSSC 22000) and robust Responsible Care implementation. Firms with integrated backward linkages and in-house R&D lines can swiftly tailor molecules to shifting allergen-labeling norms, comforting global FMCG customers seeking dependable, compliant supply.

India Aroma Chemicals Industry Leaders

International Flavors & Fragrances Inc.

BASF

Symrise

dsm-firmenich

Givaudan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Givaudan started operations at its new Mahad Fragrance Ingredients facility. This marked a milestone in Givaudan's joint venture with Privi Speciality Chemicals Limited, a leading aroma chemicals producer based in India. The newly inaugurated facility will produce a wide array of value-added products, with plans to gradually intensify operations over the coming two to three years.

- April 2024: Anuvi Chemicals Limited unveiled Anurom, a new division targeting the fragrance and flavor sector. Anurom aims to produce premium ingredients for diverse applications, spanning beauty, personal care, laundry, detergents, incense, home fragrances, fine fragrances, and deodorants.

India Aroma Chemicals Market Report Scope

Aroma chemicals are highly volatile, complex aromatic compounds known for enhancing the flavor or fragrance of the formulations into which they are infused.

The Indian aroma chemicals market is segmented by type and application. The market is segmented by terpenes, benzenoids, musk chemicals, and other types (esters, ketones, etc.). The market is segmented by application into soap and detergents, cosmetics and toiletries, fine fragrances, household products, food and beverage, and other applications (textile, tobacco, candles, etc.). For each segment, market sizing and forecasts have been done based on revenue (USD).

| Terpenes |

| Benzenoids |

| Musk Chemicals |

| Other Types |

| Soaps and Detergents |

| Cosmetics and Toiletries |

| Fine Fragrances |

| Household Products |

| Food and Beverage |

| Other Applications |

| By Type | Terpenes |

| Benzenoids | |

| Musk Chemicals | |

| Other Types | |

| By Application | Soaps and Detergents |

| Cosmetics and Toiletries | |

| Fine Fragrances | |

| Household Products | |

| Food and Beverage | |

| Other Applications |

Key Questions Answered in the Report

How large is the India aroma chemicals market in 2026?

The India aroma chemicals market size is USD 341.13 million in 2026 and is on track to reach USD 444.52 million by 2031.

What is the growth rate for aroma chemicals used in Indian fine fragrances?

Fine fragrances are advancing at a 5.98% CAGR, outperforming traditional soap and detergent applications.

Which product type holds the highest share in 2025?

Terpenes dominate with 64.72% of the India aroma chemicals market share thanks to abundant botanical feedstocks.

Where are most aroma-chemical plants located in India?

Gujarat and Maharashtra host about 70% of capacity, leveraging integrated petrochemical hubs and port logistics.

How are regulatory changes overseas affecting Indian exporters?

Stricter allergen-labeling rules in the EU and North America raise testing costs, favoring manufacturers with advanced analytical capabilities.

Page last updated on: