Europe Titanium Dioxide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

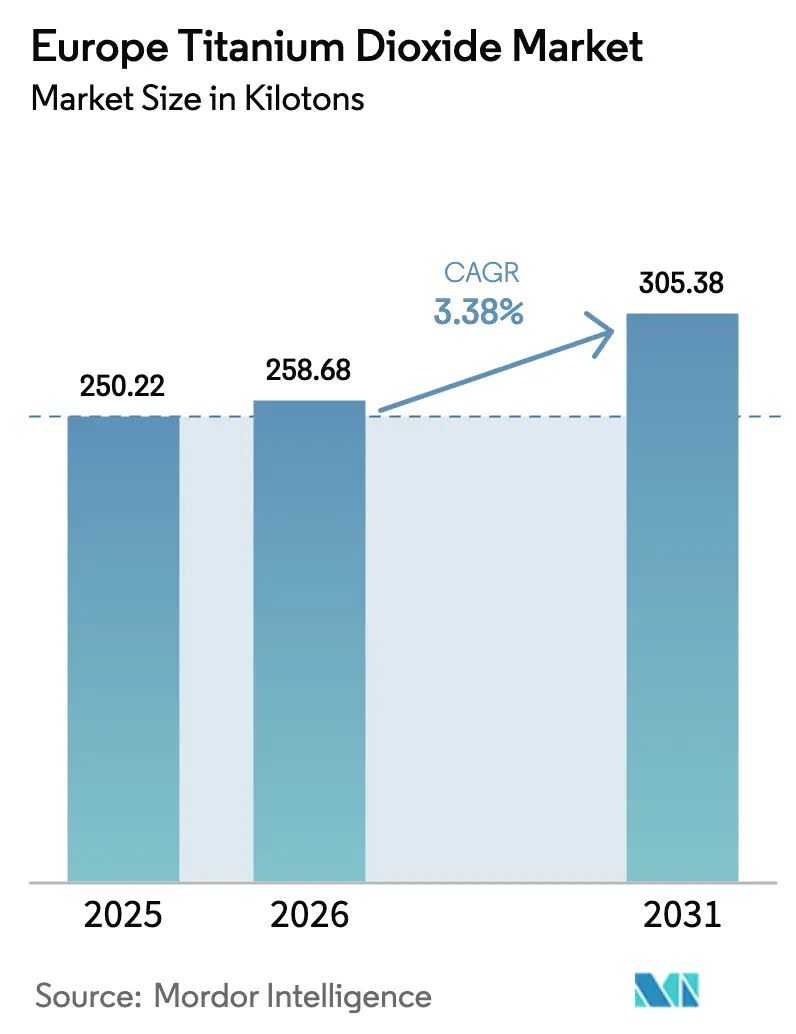

| Base Year Market Size (2025) | 250.22 kilotons |

| Market Volume (2026) | 258.68 kilotons |

| Market Volume (2031) | 305.38 kilotons |

| Growth Rate (2026 - 2031) | 3.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Titanium Dioxide Market Analysis by Mordor Intelligence

The Europe Titanium Dioxide Market size was valued at 250.22 kilotons in 2025 and estimated to grow from 258.68 kilotons in 2026 to reach 305.38 kilotons by 2031, at a CAGR of 3.38% during the forecast period (2026-2031). Capacity rationalization now overlaps with stringent environmental mandates, shifting demand toward chloride-route, high-purity grades that satisfy Nordic Swan and ISO 50001 requirements. Venator’s closure of 130,000 tonnes of sulfate lines and Tronox’s 90,000-tonne Botlek shutdown illustrate how Western producers cede share to premium chloride units even after the January 2025 anti-dumping duties on Chinese imports. Nano and ultrafine TiO₂ grades are expanding at 5.18% annually as self-cleaning façade coatings and medical-device coatings grow under the EU Renovation Wave and EMA rulings, adding a specialty tailwind that partly offsets contraction in commodity volumes.

Key Report Takeaways

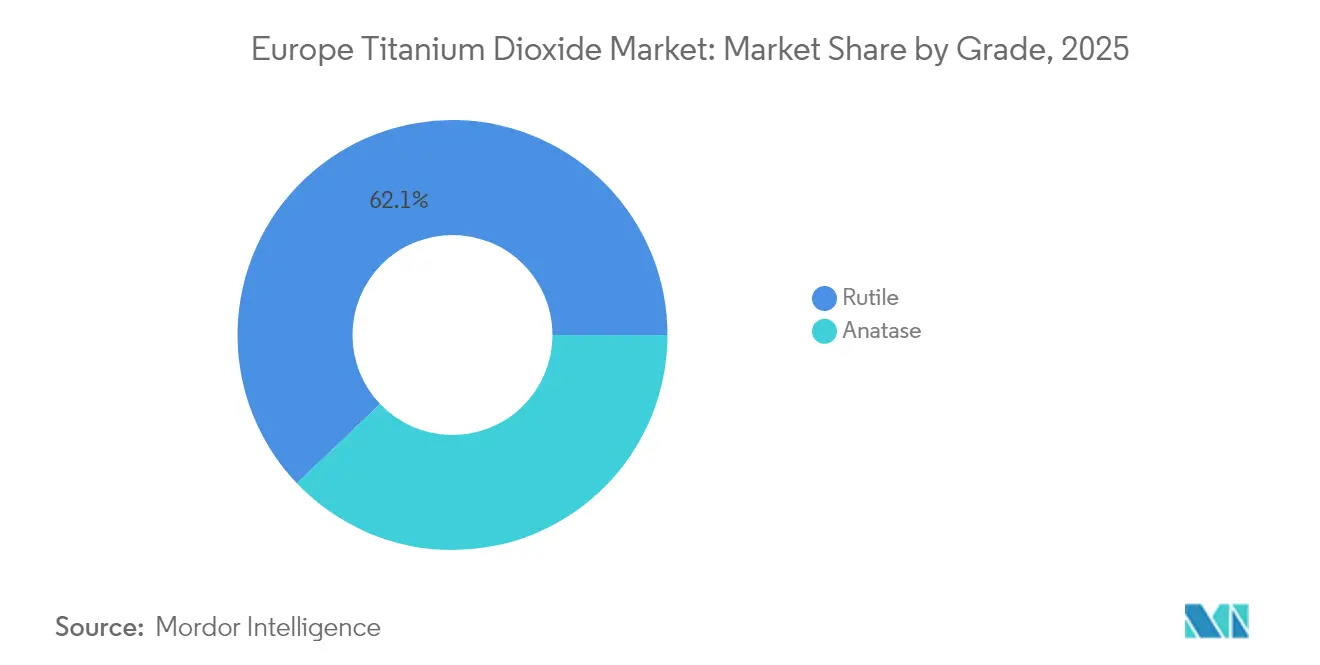

- By grade, rutile held 62.12% of the Europe titanium dioxide market share in 2025, while nano and ultrafine grades are advancing at a 4.96% CAGR through 2031.

- By production process, the chloride route commanded 57.86% of the Europe titanium dioxide market size in 2025, and its output is projected to grow at a 4.12% CAGR to 2031.

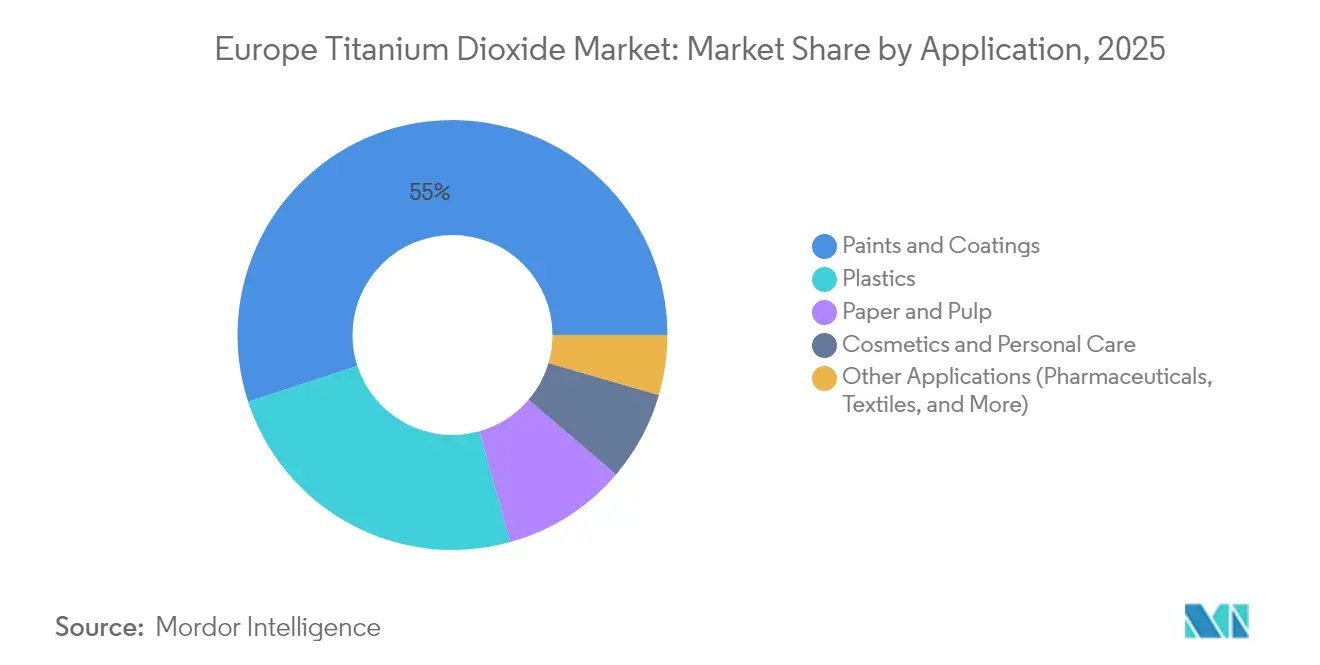

- By application, paints and coatings accounted for 55.02% of the Europe titanium dioxide market size in 2025; cosmetics and personal care are growing the fastest at a 5.12% CAGR.

- By geography, Germany led with 18.96% of the Europe titanium dioxide market share in 2025, whereas the Nordics represent the quickest riser at a 4.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on titanium dioxide market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Titanium Dioxide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-driven demand for high-performance paints and coatings | +0.9% | Germany, France, Nordics, Spain, Italy | Medium term (2-4 years) |

| Lightweight durable plastics boosting TiO₂ loadings | +0.6% | Germany, France, Italy | Medium term (2-4 years) |

| Shift to chloride-process premium grades for sustainability | +0.7% | Nordics, Germany | Long term (≥ 4 years) |

| EU Renovation Wave spurring photocatalytic facades | +0.5% | Germany, France, Nordics, Spain | Medium term (2-4 years) |

| Ultrafine rutile in medical-device and drug-delivery coatings | +0.3% | Germany, France, United Kingdom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction-Driven Demand for High-Performance Paints and Coatings

Architectural coatings retain a roughly 56% share of Europe’s paints segment, making TiO₂ indispensable for opacity and weather resistance[1]Fédération Française des Industries des Peintures, “Coatings Cost Index 2025,” fipec.org. The EU Renovation Wave, aimed at a 40% cut in building emissions by 2030, channels subsidies toward high-hiding‐power façade coatings that lower life-cycle paint use. France’s electricity costs, while down 40% year-over-year to EUR 58/MWh in 2024, are still 80% above 2019 levels, nudging formulators to favor durable TiO₂-rich recipes rather than cheaper extenders. German green-building incentives prioritize photocatalytic coatings that decompose NOx, a niche requiring TiO₂ loads of more than 3% to comply with ISO 50001. Finnish producer Teknos has requested an 18-month phase-in of anti-dumping duties, warning that sudden cost spikes on Chinese TiO₂ would slow waterborne repaint projects.

Lightweight Durable Plastics Boosting TiO₂ Loadings

The automotive shift to glass-fiber-reinforced polyolefins and the proliferation of thin, high-opacity packaging films are increasing TiO₂ concentrations in masterbatches. Volkswagen and Stellantis specify 2%–4% TiO₂ in interior trims to meet color-fastness targets in electric vehicles manufactured in Germany and France. Recycled polymer lines, accounting for 89 kilo tonnes of 2024 output, also rely on TiO₂ to blend post-consumer feedstocks into a uniform white base. EU single-use plastic rules are driving the use of thinner films, which require higher pigment loadings to maintain shelf appeal. Chloride-route pigment, which generates at most 329 kg of waste per tonne, increasingly displaces sulfate grades in REACH-compliant automotive supply chains.

Shift to Chloride-Process Premium Grades for Sustainability Compliance

The Europe titanium dioxide market is tilting toward chloride units because they consume 20% less energy and skirt sulfate acid-waste disposal. Nordic Swan limits sulfate emissions to 7 kg SOx/tonne, a threshold most legacy plants breach, prompting Tronox and Venator to close 220,000 tonnes of sulfate capacity since 2024. Chemours’ decision to pair TiO₂ with an on-site 340,000-tonne chlorine plant illustrates how vertical integration is becoming mandatory for cost control. Chinese chloride output decreased to 13.91% of its 2024 total, highlighting technical hurdles that provide European producers with a premium-price window. Germany’s VdMi forum is meanwhile uniting producers around a chloride-advocacy platform to shore up competitiveness.

EU Renovation Wave Spurring Photocatalytic Self-Cleaning Facades

Anatase TiO₂ coatings cut NOx by up to 60% under UV, according to 2024 TU Wien trials, fitting the Renovation Wave’s air-quality goals. Europe’s photocatalytic coatings market now totals USD 659 million, with titanium dioxide (TiO₂) comprising 70% of the active ingredients. Municipal tenders in Germany, France, and the Nordics typically accept a 15%–25% cost premium, as maintenance savings offset the higher purchase prices. Coatings containing more than 3% TiO₂ must demonstrate ISO 50001 energy management compliance, driving demand for chloride rutile that meets stricter waste caps[2]Nordic Ecolabelling, “Criteria for Indoor Paints and Varnishes (2024),” nordic-ecolabel.org. VTT’s EUR 1.3 million CELLIGHT program, which studies cellulose-based alternatives, underscores how regulators continue to push incumbents for additional environmental proof points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity perception and tightening REACH/CLP rules | -0.5% | Germany, France, Nordics | Short term (≤ 2 years) |

| Volatile prices for ilmenite, rutile, and energy | -0.4% | Germany, France, Italy | Short term (≤ 2 years) |

| Chlorine availability pressure on chloride units | -0.2% | Germany, Netherlands, UK | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Toxicity Perception and Tightening REACH/CLP Classification

ECHA’s 2021 inhalation-hazard label on TiO₂ now forces any powder product exceeding 1% content to carry a cancer warning, denting consumer confidence in wall paints and cosmetics. Germany’s 2022 ban on food-grade E171 amplified public concern, encouraging brands like AURO to unveil TiO₂-free paints despite lower opacity. Lavera and other cosmetics players followed by launching TiO₂-free foundations in 2024, even though SCCS confirmed skin safety the same year. Occupational safety mandates in France and Germany now require respirators in powder units, which increases compliance costs and nudges coatings producers toward liquid dispersions. Green-building labels further reward partial TiO₂ substitution with calcium carbonate, cutting embodied carbon 15%–20% at the expense of visual brightness.

Volatile Prices for Ilmenite, Rutile and Energy

Norway’s 360,000-tonne ilmenite output serves under 5% of European pigment needs, while Ukraine’s conflict-hit mines delivered just 120,000 tonnes of ilmenite and 10,000 tonnes of rutile in 2024, tightening feedstock supply. Natural-gas prices of EUR 36/MWh in France—triple the 2019 baseline—inflate sulfate-route costs, which are already 20% more energy-intensive than those of the chloride route. Fipec notes that 2024–2025 TiO₂ pigment invoice levels remain 30%–40% above pre-COVID averages, leaving paint makers to choose between margin erosion and end-market price hikes. Russian titanium worth USD 244 million continued to flow to the EU in 2023, exposing Germany, France, and the United Kingdom to supply-chain criticism despite sanctions rhetoric. Titanor’s Kokkola project may yield 1.6 million tonnes of ore annually but awaits EUR 85–110 million in financing and stringent tailings approval, meaning reliance on imports will persist through the forecast.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Nano Innovations Challenge Rutile Dominance

Rutile controlled 62.12% of the Europe titanium dioxide market in 2025 thanks to superior opacity and weather fastness required in exterior paints and plastics. Nano and ultrafine pigments are projected to grow at a 4.96% CAGR, driven by self-cleaning coatings and pharmaceutical demand, which supports premium prices that cushion revenue despite their smaller tonnage base. Chloride-route rutile is priced 10%–15% higher than sulfate rivals due to its tighter particle distribution and lower impurity levels, attributes that are highly valued by automotive OEMs for achieving high-gloss finishes. The Europe titanium dioxide market size for rutile applications is forecast to expand steadily even as substitution pressure nudges commodity interior grades toward calcium carbonate extenders.

Anatase retains relevance in photocatalytic façades because its surface energy accelerates NOx oxidation, a function validated by TU Wien’s 2024 tests, which showed 40%–60% pollution removal. Yet economic headwinds stifle new sulfate-anatase investment after Venator mothballed its Duisburg and Scarlino units. VTT’s cellulose-based CELLIGHT concept illustrates a long-term threat across all grades but faces functional gaps in opacity, UV shielding, and chemical inertness that TiO₂ uniquely provides. Thus, rutile should hold core share while nano segments erode margin dilution by capturing specialty demand under stricter EU ecolabels.

By Production Process: Chloride Routes Gain Amid Sulfate Retreat

Chloride operations supplied 57.86% of the Europe titanium dioxide market in 2025 and are expanding 4.12% yearly, outpacing sulfate’s sub-3% advance as waste-acid fees soar and energy costs linger above pre-2019 benchmarks. Europe titanium dioxide market size for chloride grades will widen as producers retrofit ISO 50001 and secure captive chlorine streams, illustrated by Chemours partnering PCC for an integrated chlor-alkali line.

Sulfate capacity rationalization has removed over 220,000 tonnes since 2024, leaving a smaller, higher-utilization base that still struggles under Nordic Swan’s 7 kg SOx ceiling. Chinese competition remains acute, yet anti-dumping margins of EUR 0.25–0.74/kg provide modest breathing space for Europe’s premium chloride segments. Feedstock flexibility once favored sulfate, but geopolitical disruptions to Ukrainian ilmenite and rising disposal levies erode that edge, making further shutdowns likely near term.

By Application: Cosmetics Surge as Paints Plateau

Paints and coatings consumed 55.02% of Europe titanium dioxide market size in 2025, but growth hovers in low single digits because extenders like calcium carbonate nibble at loading rates. In contrast, cosmetics and personal care are growing at a rate of 5.12% per year, buoyed by the SCCS clearance of nano-TiO₂ and a consumer shift to mineral sunscreens following the 2022 E171 food-grade ban. Europe titanium dioxide market share gains in cosmetics cushion overall revenue and improve mix toward higher-margin ultrafine grades.

Plastics account for roughly a quarter of the volume, supported by automotive lightweighting and flexible packaging. TotalEnergies’ 9,111 kilo-tonne petrochemical platform embeds TiO₂ in both virgin and recycled resins, sustaining dependable offtake. Pharmaceuticals remain a niche yet secure pillar, following the EMA's maintenance of TiO₂ authorization in October 2025. Paper coatings are declining as digital media expands, yet specialty papers in luxury packaging partially offset the contraction, leaving overall demand divergent across end-use sectors.

Geography Analysis

Germany’s 18.96% share underscores its twin status as Europe’s largest TiO₂ producer and consumer, anchored by 339,000 tonnes of chloride capacity serving automotive and construction clusters. VdMi’s 2024 summit crystallized German leadership in chloride advocacy, while AURO’s TiO₂-free paint launch demonstrates how localized consumer green sentiment is influencing pigment demand.

France hosts Europe’s second-largest coatings base, but elevated power tariffs and Fipec-reported 30%–40% pigment cost inflation squeeze margins, inducing producers to favor higher-coverage TiO₂ grades over extender dilution. Tronox’s shift in focus away from its Thann unit to battery materials further tightens French supply. The United Kingdom’s 315,000-tonne chloride capacity provides high-purity pigment to local aerospace and healthcare sectors, yet faces cost pressure after Venator’s asset disposals. The Nordics lead growth at 4.58% annually as green-building codes, photocatalytic coatings, and cellulose substitution projects gain state backing. Norway’s ilmenite mines and Finland’s prospective Kokkola project aim to cut import dependency, though environmental permitting delays linger. Italy and Spain round out Southern Europe demand via packaging and textiles, while ongoing Russian exports highlight geopolitical complexity when sanctions clash with supply security.

Mordor Intelligence provides coverage of the titanium dioxide market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

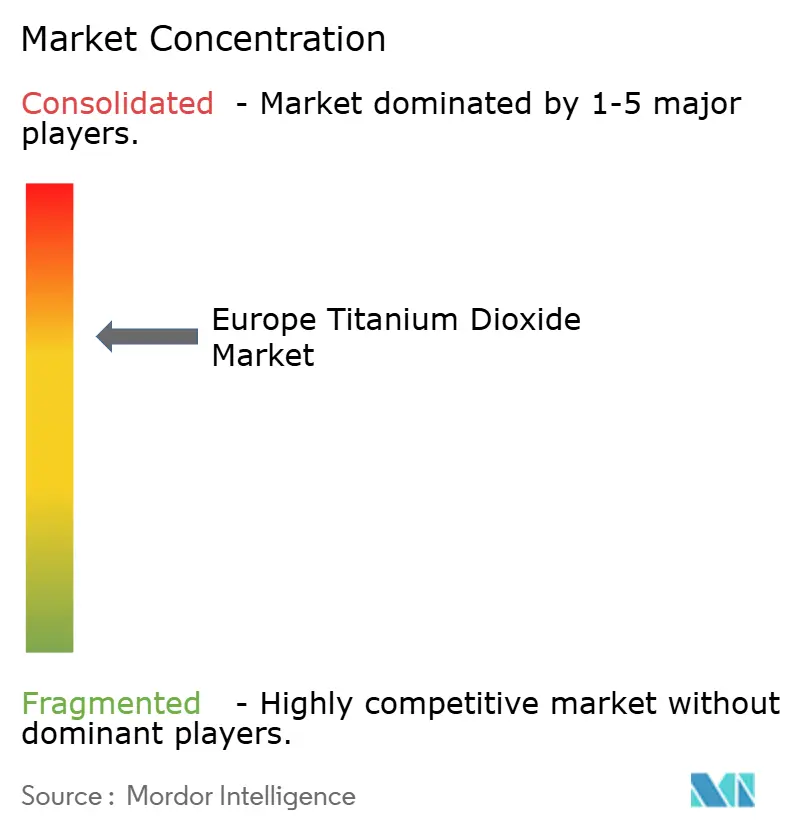

The Europe Titanium Dioxide market is moderately consolidated, with Kronos, Tronox, and Venator spearheading 2023’s anti-dumping petition that yielded January 2025 tariffs on Chinese imports. Capacity rationalization is the prime lever: Tronox eliminated 90,000 tonnes at Botlek in 2025, and Venator shuttered 130,000 tonnes at Duisburg and Scarlino in 2024 before divesting its LPC unit to Kronos for USD 185 million. Smaller players such as Cinkarna Celje, Grupa Azoty, and Precheza carve regional niches through ISO 50001 compliance, particularly in the Nordics, where ecolabel criteria strictly favor low-carbon pigments. Chinese producers maintain price pressure globally, but technical limits in chloride scaling and EU duties afford European suppliers a premium corridor in high-purity grades.

Europe Titanium Dioxide Industry Leaders

The Chemours Company

Venator Materials PLC

Kronos Worldwide, Inc.

Tronox Holdings plc

LB Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: LB Group, the world’s largest supplier of titanium dioxide, announced to acquire of the British factory belonging to Venator Materials UK. The acquisition will enable the LB Group to enhance its titanium dioxide production processes and product offerings.

- September 2025: Following a June 2025 ruling by the Court of Justice of the European Union that revoked the carcinogenic classification of titanium dioxide, the European Chemicals Agency (ECHA) has officially removed the substance from its C&L Inventory.

Europe Titanium Dioxide Market Report Scope

Titanium dioxide is an inorganic compound with the chemical formula TiO2. It is a naturally occurring mineral that is extracted from the earth, processed and purified, and used in a wide range of industrial & consumer product applications. It finds application in industrial and consumer products, such as paints and coatings, adhesives, plastics, paper, rubber, printing inks, coated fabrics, and textiles.

The European titanium dioxide market is segmented by grade, application, and geography. By grade, the market is segmented into rutile and anatase. By application, the market is segmented into paints and coatings, plastics, pulp and paper, cosmetics, and other applications (pharmaceuticals, textiles, food colorants, etc.) The report also covers the market size and forecasts for the titanium dioxide market in 6 countries across the region.

For each segment, the market sizing and forecasts have been done based on volume (tons).

| Rutile |

| Anatase |

| Sulfate |

| Chloride |

| Paints and Coatings |

| Plastics |

| Paper and Pulp |

| Cosmetics and Personal Care |

| Other Applications (Pharmaceuticals, Textiles, Food Colorants, etc.) |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Nordics Countries |

| Russia |

| Rest of Europe |

| By Grade | Rutile |

| Anatase | |

| By Production Process | Sulfate |

| Chloride | |

| By Application | Paints and Coatings |

| Plastics | |

| Paper and Pulp | |

| Cosmetics and Personal Care | |

| Other Applications (Pharmaceuticals, Textiles, Food Colorants, etc.) | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics Countries | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe titanium dioxide market today?

The market stood at 258.68 kilo tons in 2026 and is on track to reach 305.38 kilo tons by 2031.

What CAGR is expected for European TiO₂ demand through 2031?

Demand is projected to expand at a 3.38% CAGR between 2026 and 2031, led by chloride-route specialty grades.

Which application is growing fastest for TiO₂ in Europe?

Cosmetics and personal care are set to rise 5.12% annually, benefiting from nano-pigment uptake in sunscreens.

Why are chloride-route pigments gaining share?

Lower energy use, reduced acid waste, and compliance with Nordic Swan and ISO 50001 standards favor chloride processes.

How will anti-dumping duties affect supply?

Duties of EUR 0.25–0.74/kg on Chinese imports give European producers margin relief but could lift costs for downstream coatings if local capacity remains tight.

Page last updated on: