Indium Gallium Zinc Oxide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

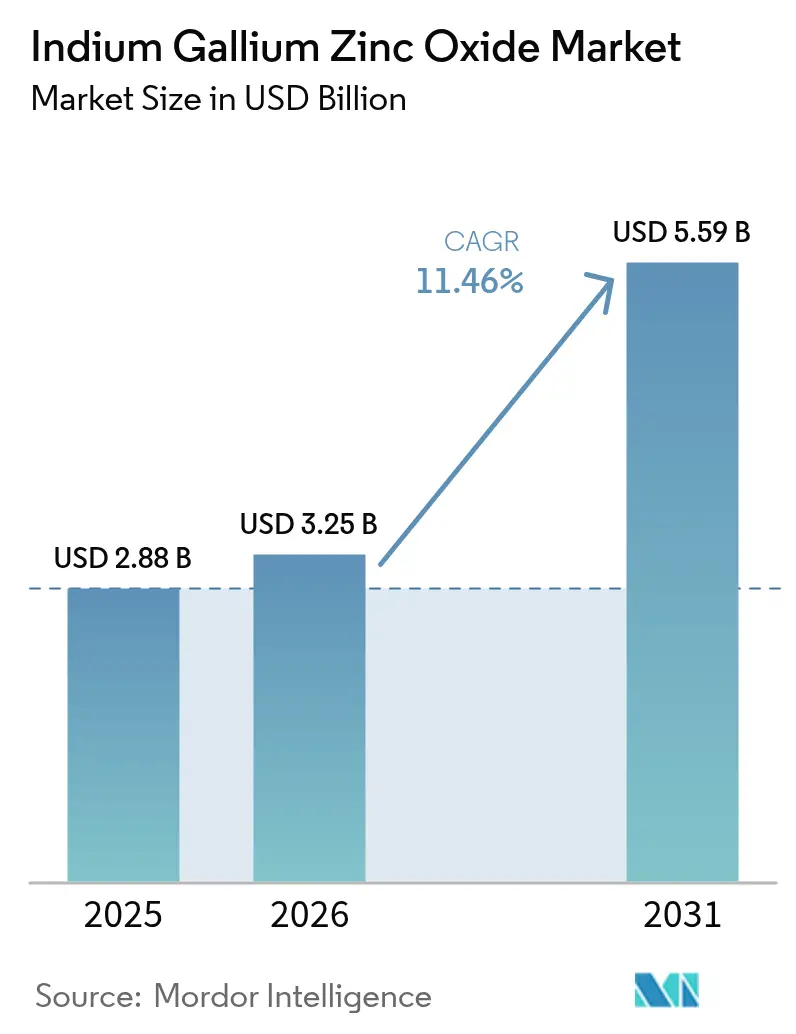

| Market Size (2026) | USD 3.25 Billion |

| Market Size (2031) | USD 5.59 Billion |

| Growth Rate (2026 - 2031) | 11.46% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indium Gallium Zinc Oxide Market Analysis by Mordor Intelligence

The Indium gallium zinc oxide market size is projected to expand from USD 3.25 billion in 2026 to USD 5.59 billion by 2031, registering an 11.46% CAGR between 2026 and 2031. Robust demand for high-resolution OLED televisions, foldable smartphones, and mixed-reality headsets is driving oxide-semiconductor adoption, while government incentives in Asia-Pacific accelerate fabrication capacity. Panel makers are reallocating capital from conventional a-Si and LTPS backplanes toward oxide thin-film transistors that combine higher electron mobility with ultralow leakage, enabling variable refresh rates down to 1 Hz that cut display power draw during static content. Cost headwinds tied to indium price volatility are partly offset by yield improvements as sputtering-system suppliers introduce multi-cathode configurations that raise IGZO target utilization above 80%. Competitive dynamics remain fluid: Korean incumbents seek margin security in premium OLED IT panels, Chinese entrants leverage subsidy-supported scale, and Japanese firms pivot toward automotive and medical niches.

Key Report Takeaways

- By geography, Asia-Pacific led with 52.41% of the Indium gallium zinc oxide market share in 2025 and is forecast to grow at a 12.59% CAGR through 2031.

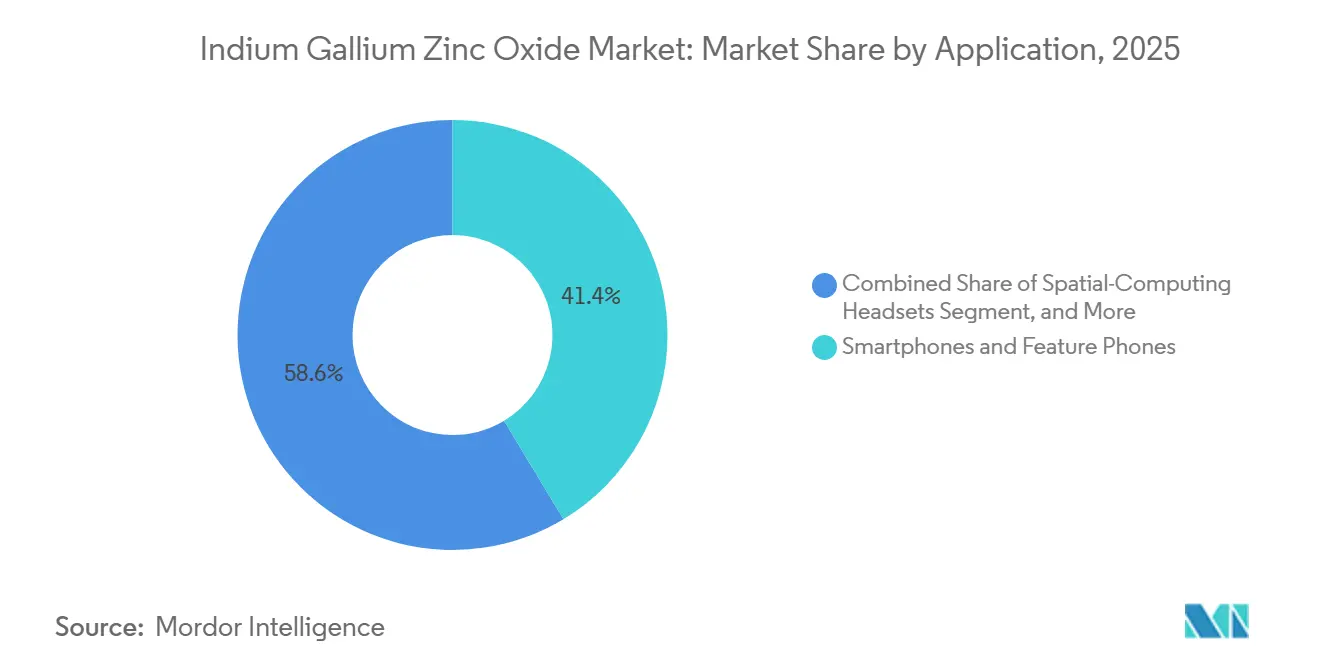

- By application, smartphones and feature phones held 41.37% of the Indium gallium zinc oxide market share in 2025, while spatial-computing headsets are advancing at a 12.55% CAGR to 2031.

- By end-use industry, consumer electronics accounted for 56.29% share of the Indium gallium zinc oxide market size in 2025; aerospace and defense is projected to record a 12.31% CAGR during 2026-2031.

- By display technology, OLED commanded 61.81% share of the Indium gallium zinc oxide market size in 2025; MicroLED and MiniLED segments are set to expand at a 12.49% CAGR to 2031.

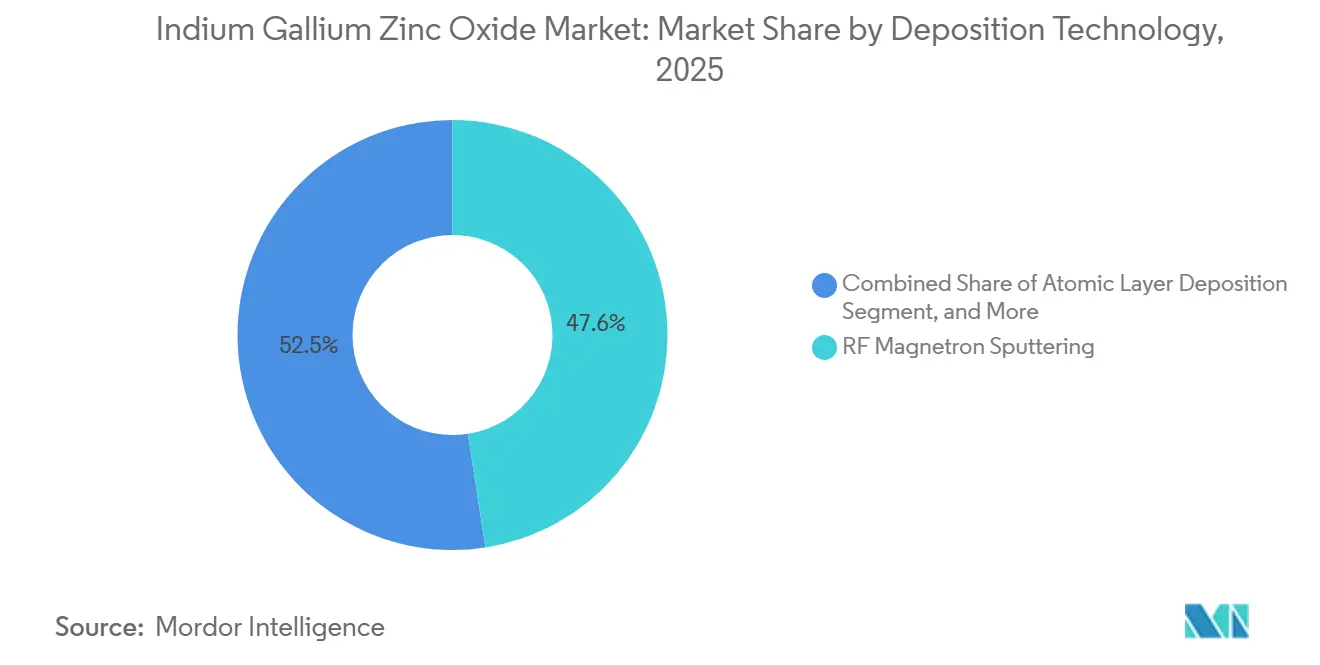

- By deposition technology, RF magnetron sputtering captured 47.55% of the Indium gallium zinc oxide market share in 2025, whereas atomic layer deposition is expected to climb at a 12.67% CAGR through 2031.

- By conductivity phase, amorphous IGZO dominated with 72.58% share of the Indium gallium zinc oxide market size in 2025; single-crystal IGZO is forecast to log a 12.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Indium Gallium Zinc Oxide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in High-Resolution OLED and 8K TV Demand | +3.20% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Requirement for Energy-Efficient Portable Devices | +2.80% | Global, particularly Asia-Pacific and Europe | Short term (≤ 2 years) |

| Rapid Adoption in Foldable and Flexible Displays | +2.50% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| IGZO Backplanes Enabling Ultra-Low-Power Wearables | +1.60% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Integration of IGZO in Spatial-Computing Headsets | +1.30% | North America and Europe, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Sub-Threshold Switching for Neuromorphic In-Memory AI | +0.80% | Global, concentrated in advanced semiconductor regions (US, Taiwan, South Korea) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge In High-Resolution OLED And 8K TV Demand

Premium television makers are migrating to oxide backplanes to maintain current uniformity across 8K panels, where 33 million pixels amplify leakage-induced grayscale errors. Samsung Display shipped 4.9 million OLED TV panels in H1 2025 and captured 74% quarterly share after switching its QD-OLED line from LTPS to oxide TFT.[1]Samsung Electronics, “Q4 2025 Earnings Report,” samsung.com LG Display committed USD 925 million to enlarge its E6 OLED fab, citing oxide-LTPO hybrids that extend panel life past 100,000 hours and cut power use by 30%. Chinese players BOE and China Star added 8.6-generation oxide capacity totaling RMB 63 billion to pursue laptop and tablet substrates.[2]BOE Technology Group, “Annual Report 2023,” boe.com Energy-efficiency rules under IEC 62087 encourage adoption of IGZO by rewarding standby draw below 0.5 W in the European Union and United States.

Requirement For Energy-Efficient Portable Devices

Tablets and 2-in-1 PCs require displays that last a full workday on a single charge, and IGZO’s picoampere-scale off-current enables 1 Hz refresh for static screens. Samsung’s UT One IT OLED prototype demonstrated this capability in September 2025, validating roadmap targets for commercial laptops in 2027.[3]Samsung Display, “OLED IT Summit Presentation,” samsungdisplay.com Apple’s planned OLED iPad Pro refresh depends on oxide substrate supply, prompting both Korean majors to boost 8.6-gen capacity. Industrial handhelds in logistics operate 16-hour shifts, and IGZO panels reduce battery swaps that disrupt workflows. Research published in IEEE Electron Device Letters (Dec 2025) showed self-aligned imprint lithography cutting process steps 40%, lowering static power further.[4]IEEE Electron Device Letters, “Self-Aligned Imprint Lithography for a-IGZO TFTs,” ieeexplore.ieee.org

Rapid Adoption in Foldable and Flexible Displays

Foldables endure >200,000 bend cycles, and the amorphous IGZO matrix, free of grain boundaries, resists crack propagation better than poly-Si. Samsung Display validated 500,000 folds at 1.5 mm radius in July 2025, crediting oxide TFT stability. BOE’s mass-produced high-mobility oxide AMOLEDs raised flexible panel shipments 50% year over year. Sharp unveiled a 12.3-inch flexible IGZO OLED for automotive dashboards rated from −40 °C to +85 °C. Chip-on-encapsulation reduces module stack height by 0.3 mm, helping foldable smartphones meet slimness goals for 2027 launches.

IGZO Backplanes Enabling Ultra-Low-Power Wearables

Smartwatches demand below-5 mW always-on displays. IGZO’s 10-50 cm² V⁻¹ s⁻¹ mobility allows smaller TFT geometries that improve aperture ratio and luminance at lower current. Wearable AMOLED volumes remain modest, yet CAGR tops 12.55% as vendors shift from monochrome to full colour. IMEC fabricated 2T0C DRAM on 300 mm wafers with 4.5-hour retention, foreshadowing monolithic display-memory stacks for health-monitoring bands. ISO 14971 fault-tolerance rules in medical wearables favour IGZO uniformity over organic TFT alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from LTPS and LTPO Silicon Backplanes | -2.10% | Global, particularly in premium smartphone segment | Short term (≤ 2 years) |

| Supply-Chain Volatility and Indium Price Fluctuation | -1.80% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Low Recycling Rates of Spent IGZO Sputter Targets | -0.60% | Global, concentrated in Asia-Pacific manufacturing hubs | Long term (≥ 4 years) |

| Threshold Voltage Drift in Humid Environments | -0.40% | Tropical and subtropical regions (Southeast Asia, South America) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition From LTPS And LTPO Silicon Backplanes

LTPS mobility exceeds 100 cm² V⁻¹ s⁻¹, enabling faster pixel switching in high-refresh smartphones. Apple and Samsung adopted LTPO hybrids in 2021, integrating LTPS switching with IGZO drive to obtain 1-120 Hz variable refresh without battery penalties. The added 20%-30% cost premium is acceptable in USD 800-plus handsets, limiting pure IGZO uptake. Research targeting single-crystal IGZO mobilities near 80 cm² V⁻¹ s⁻¹ is promising but unscaled.

Supply-Chain Volatility and Indium Price Fluctuation

China supplied 70% of the 1,080-t global indium output in 2024 and imposed a 25% export tariff that pushed spot prices from USD 244 kg⁻¹ in 2023 to USD 340 kg⁻¹ in 2024. The United States remains fully import-reliant, drawing 29% from South Korea, 18% from Japan, and 14% from Canada. Spikes to USD 420 kg⁻¹ compressed panel margins and spurred R&D into indium-free zinc-tin oxide substitutes that still trail IGZO electrical performance. South Korea’s K-Chips Act, effective February 2025, raised tax credits for local sputtering-target plants to 20% to cushion volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Spatial-Computing Headsets Outpace Smartphones

Spatial-computing headsets represented a minor slice in 2025 yet are projected for double-digit expansion as Meta and Apple ramp mixed-reality volumes. The Indium gallium zinc oxide market size tied to headsets is set to expand at a 12.55% CAGR, benefiting from IGZO’s ability to drive micro-OLED pixels below 10 µm at 90 Hz without thermal throttling. Smartphone demand remains foundational, retaining 41.37% 2025 share, especially for mid-tier models where oxide TFTs undercut LTPS costs while providing 10-20 cm² V⁻¹ s⁻¹ mobility. Tablets adopt variable-refresh oxide OLED to extend battery endurance during e-reading sessions, and Samsung’s UT One IT panel validates near-zero hertz hold mode. Automotive dashboards, industrial HMIs, and diagnostic monitors capitalize on IGZO’s wide temperature stability and grayscale fidelity, opening design wins in electric vehicles and radiology suites.

The Indium gallium zinc oxide market share held by wearables is small today, yet integration of IGZO memory-in-display promises compact sensor arrays that support multiday medical monitoring. Televisions and large-format panels sustain growth as 8K adoption broadens and Gen-10 oxide lines deliver higher yields than LTPS at identical substrate sizes. Industrial AR glasses, driven by logistics picking and field maintenance, push oxide to pixel densities unseen in conventional monitors, consolidating IGZO’s foothold across divergent form factors.

By End-Use Industry: Aerospace Emerges as Growth Frontier

Consumer electronics dominate revenue at 56.29% as smartphones, tablets, and TVs proliferate, but the aerospace and defense corridor grows at 12.31% CAGR on cockpit upgrades to ultrabright, radiation-tolerant IGZO OLED. Commercial airlines adopt ruggedized 4K flight-deck monitors that withstand −40 °C to +85 °C excursions, and defense programs select IGZO for helmet-mounted sights immune to cosmic radiation single-event upsets. Automotive follows, deploying curved infotainment clusters that pair oxide TFTs with MiniLED backlights for 1,000-nit daylight readability, while the healthcare vertical taps IGZO LCD for calibrated grayscale in mammography. Industrial robotics benefits from 24/7 duty cycles, leaning on IGZO’s elevated mean-time-between-failure versus a-Si.

Defense prime contractors increasingly stipulate oxide-backplane panels in procurement, insulating the Indium gallium zinc oxide market from consumer cyclicality. Civil-aviation regulators certify oxide displays under DO-178C for software and DO-254 for hardware, lifting compliance hurdles for alternatives. Conversely, consumer devices remain price-elastic; sustained indium cost spikes could restrain adoption, though value-chain integration offsets part of the risk.

By Display Technology: MicroLED Bets on Oxide Backplanes

OLED captured a 61.81% hold in 2025 as oxide TFTs facilitated low-temperature processing compatible with organic emitters. MicroLED targets >2,000-nit peak luminance and intrinsic longevity but needs pixel pitches under 5 µm, a window where IGZO’s amorphous nature avoids LTPS grain-boundary shorts. The Indium gallium zinc oxide market size within MicroLED applications is pegged for a 12.49% CAGR as consumer TV brands and automakers pilot prototypes for 2028 launches.

LCD persists in value segments, with oxide TFT-LCD lowering glass-warp defects on Gen-10+ lines. E-paper leverages IGZO’s sub-picoamp leakage for month-long shelf-label lifetimes in grocery chains. Hybrid QD-OLED gaming monitors such as Samsung’s 34-inch 360 Hz model show oxide’s capacity to sustain millisecond gray-to-gray response.

By Deposition Technology: Atomic Layer Precision Gains Traction

RF magnetron sputtering remains the workhorse due to throughput exceeding 100 Gen-8 substrates per hour, giving it 47.55% 2025 share. However, atomic layer deposition growth is forecast at 12.67% CAGR as sub-10 nm film precision becomes essential for single-crystal and neuromorphic stacks. Applied Materials’ Spectral ALD platform supports monolithic 3D schemes that layer logic, memory, and display on a single substrate.

Pulsed-DC sputtering offers higher film density for automotive reliability, while solution-inkjet printing finds use in flexible IoT tags where roll-to-roll economies matter. ULVAC’s 1,300-unit SMD installed base anchors retrofit demand for multi-cathode IGZO targets.

By Conductivity Phase: Single-Crystal Mobility Race

Amorphous IGZO accounts for 72.58% due to low-temperature deposition compatibility with plastic substrates. Polycrystalline IGZO serves middle-ground needs for higher drive current at moderate cost, popular in industrial kiosks.

Academic breakthroughs in epitaxial single-crystal IGZO on sapphire and glass hit 70 cm² V⁻¹ s⁻¹ mobility. The Indium gallium zinc oxide market share of single-crystal variants may still be minor in 2031, yet 12.61% CAGR illustrates momentum from neuromorphic compute and RF front-end filters seeking >60 GHz operation. Yield scalability to Gen-6+ glass remains the gating factor before mass adoption.

Geography Analysis

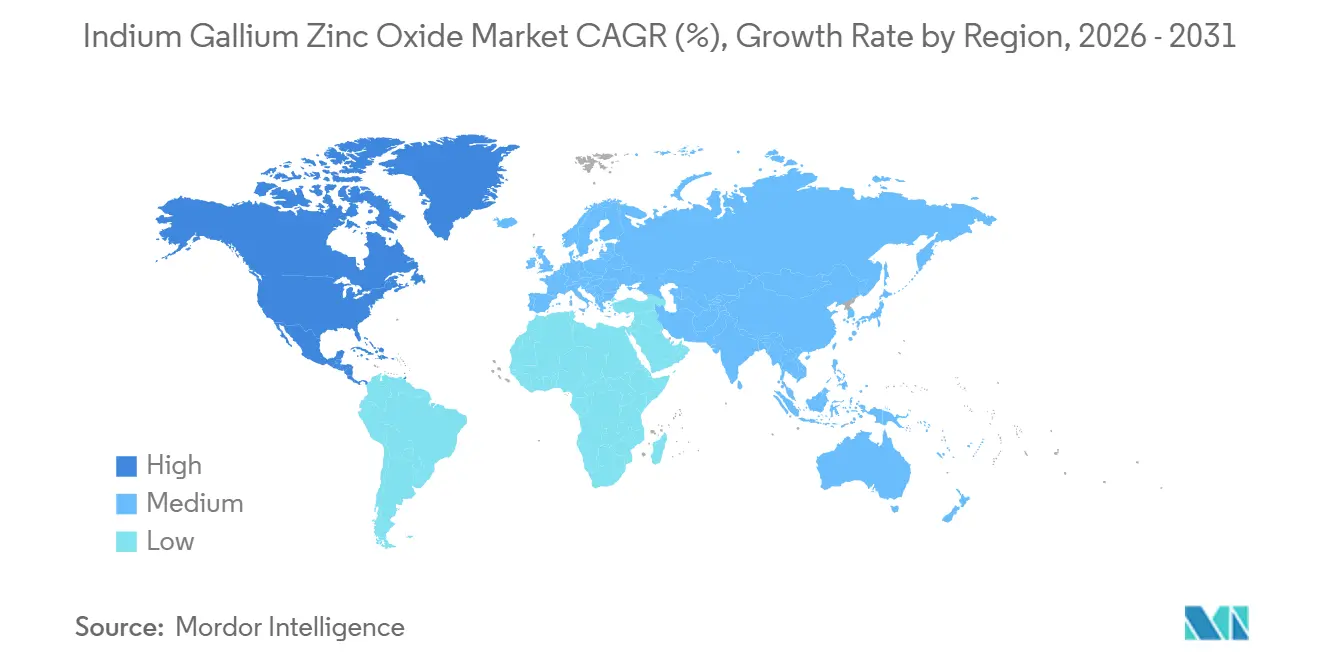

Asia-Pacific anchors both capacity and innovation. China, South Korea, and Japan together held 52.41% of 2025 revenue, and regional CAGR is estimated at 12.59% through 2031 as BOE, CSOT, Samsung Display, and LG Display commission multiple 8.6-gen oxide OLED fabs. The Indium gallium zinc oxide market size in China benefits from municipal subsidies that cut capex per substrate by 20%. South Korea’s 2025 tax-credit jump to 20% under the K-Chips Act incentivizes domestic sputtering-target and ALD precursor plants. Japan focuses on niche medical and automotive panels, though Sharp’s Kameyama K2 LCD closure in August 2026 underscores cost-pressured exits.

North America lacks large-area panel fabs but commands early-adopter demand for spatial-computing and micro-OLED, driven by Apple and Meta roadmaps. Research hubs in California, Austin, and New York foster neuromorphic IGZO circuits, creating future downstream pull. Europe’s strength lies in premium automotive clusters in Germany and Sweden, where Tier-1 suppliers specify oxide TFT for curved HUD modules that meet UNECE R125 glare limits. The Middle East and Africa, as well as South America, remain subscale; regional assembly incentives could unlock latent demand, yet infrastructure gaps and import tariffs keep oxide panels price-disadvantaged relative to legacy LCD.

Competitive Landscape

Market concentration is moderate: the top five vendors account for roughly 65% of oxide-capacity shipments, granting them bargaining leverage on sputtering targets and ALD tools. Samsung Display committed USD 3.1 billion to an 8.6-gen IT OLED fab targeting 2026 volume, aiming to secure laptop and tablet share where oxide delivers 1 Hz idle refresh.

LG Display’s USD 925 million E6 expansion seeks higher-margin LTPO 3.0 panels for premium TVs and monitors. BOE and CSOT receive municipal funds covering up to 30% capex, allowing aggressive pricing that squeezes Japanese peers; Sharp consequently shutters commodity LCD lines and shifts to automotive orders.

Visionox is constructing a USD 7.6 billion maskless vapor-phase OLED line, touting 30% lower photomask costs and faster design iteration for oxide backplanes. Equipment makers ULVAC and Applied Materials concentrate on ALD and high-density sputter tools, scrubbing particle counts below 0.14 cm⁻² to meet MicroLED yield demands. Patent filings rise for monolithic 3D integration that stacks IGZO logic and memory under emissive layers; IMEC’s 2T0C DRAM prototype exemplifies ecosystem readiness. Heightened Chinese capacity could trigger consolidation among mid-tier Taiwanese and Japanese suppliers, who may pivot toward specialized medical and avionics markets to sustain utilization.

Indium Gallium Zinc Oxide Industry Leaders

Sharp Corporation

LG Display Co., Ltd.

Samsung Display Co., Ltd.

AU Optronics Corp.

BOE Technology Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Japan Display Inc. raised JPY 95.6 billion to fund high-value displays and sensors, selling patents and a factory as part of restructuring.

- May 2025: Indium Corporation and Rio Tinto reported progress in gallium extraction aimed at diversifying oxide TFT supply chains.

- March 2025: Tata Electronics signed an MoU with Himax and PSMC to bolster India’s display and ultralow-power AI sensing ecosystem.

- June 2024: LG Display began mass production of 13-inch tandem OLED laptop panels delivering 40% lower power and triple brightness.

Global Indium Gallium Zinc Oxide Market Report Scope

The Indium Gallium Zinc Oxide Market Report is Segmented by Application (Smartphones and Feature Phones, Tablets and 2-in-1 PCs, Wearable Devices, Televisions and Large-Format Displays, Automotive Displays, Industrial and Medical Displays), End-Use Industry (Consumer Electronics, Automotive and Transportation, Healthcare, Industrial and Manufacturing, Aerospace and Defense, Others), Display Technology (LCD, OLED, MicroLED and MiniLED, E-Paper and Other Emerging), Deposition Technology (RF Magnetron Sputtering, Pulsed-DC Magnetron Sputtering, Atomic Layer Deposition, Solution and Inkjet Printing, Other Techniques), Conductivity Phase (Amorphous IGZO, Polycrystalline IGZO, Single-Crystal IGZO), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Smartphones and Feature Phones |

| Tablets and 2-in-1 PCs |

| Wearable Devices |

| Televisions and Large-Format Displays |

| Automotive Displays |

| Industrial and Medical Displays |

| Consumer Electronics |

| Automotive and Transportation |

| Healthcare |

| Industrial and Manufacturing |

| Aerospace and Defense |

| Others End-Use Industry |

| LCD |

| OLED |

| MicroLED and MiniLED |

| E-Paper and Other Emerging |

| RF Magnetron Sputtering |

| Pulsed-DC Magnetron Sputtering |

| Atomic Layer Deposition |

| Solution / Ink-Jet Printing |

| Other Deposition Technology |

| Amorphous IGZO |

| Polycrystalline IGZO |

| Single-Crystal IGZO |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Application | Smartphones and Feature Phones | |

| Tablets and 2-in-1 PCs | ||

| Wearable Devices | ||

| Televisions and Large-Format Displays | ||

| Automotive Displays | ||

| Industrial and Medical Displays | ||

| By End-Use Industry | Consumer Electronics | |

| Automotive and Transportation | ||

| Healthcare | ||

| Industrial and Manufacturing | ||

| Aerospace and Defense | ||

| Others End-Use Industry | ||

| By Display Technology | LCD | |

| OLED | ||

| MicroLED and MiniLED | ||

| E-Paper and Other Emerging | ||

| By Deposition Technology | RF Magnetron Sputtering | |

| Pulsed-DC Magnetron Sputtering | ||

| Atomic Layer Deposition | ||

| Solution / Ink-Jet Printing | ||

| Other Deposition Technology | ||

| By Conductivity Phase | Amorphous IGZO | |

| Polycrystalline IGZO | ||

| Single-Crystal IGZO | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for the Indium gallium zinc oxide market between 2026 and 2031?

The market is projected to grow at an 11.46% CAGR during 2026-2031.

Which region holds the largest share of IGZO panel production?

Asia-Pacific led with 52.41% share in 2025, reflecting concentrated capacity in China, South Korea, and Japan.

Why are oxide TFTs preferred for foldable smartphones?

IGZO's amorphous matrix lacks grain boundaries, maintaining electrical stability through more than 500,000 bend cycles validated by Samsung Display.

How do indium price fluctuations impact panel makers?

A 42% price surge to USD 340 kg⁻¹ in 2024 raised material costs by up to 8% of panel BOM, pressuring margins until tax credits and recycling initiatives offset exposure.

Which deposition technology is gaining momentum beyond 2026?

Atomic layer deposition is growing at a 12.67% CAGR as advanced nodes demand sub-10 nm IGZO film control for single-crystal and neuromorphic devices.

What advantage does IGZO provide in mixed-reality headsets?

IGZO backplanes drive micro-OLED pixels at More than 3,000 ppi and 90 Hz with ultralow power, reducing motion-to-photon latency critical for spatial computing.

Page last updated on: