Power Semiconductor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 59.98 Billion |

| Market Size (2031) | USD 78.25 Billion |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

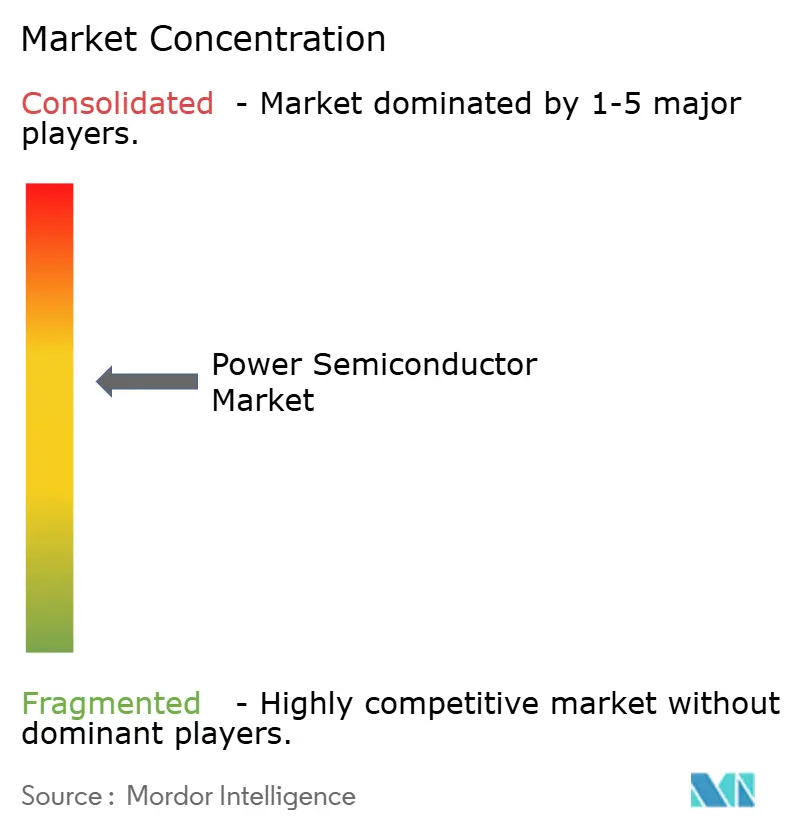

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Power Semiconductor Market Analysis by Mordor Intelligence

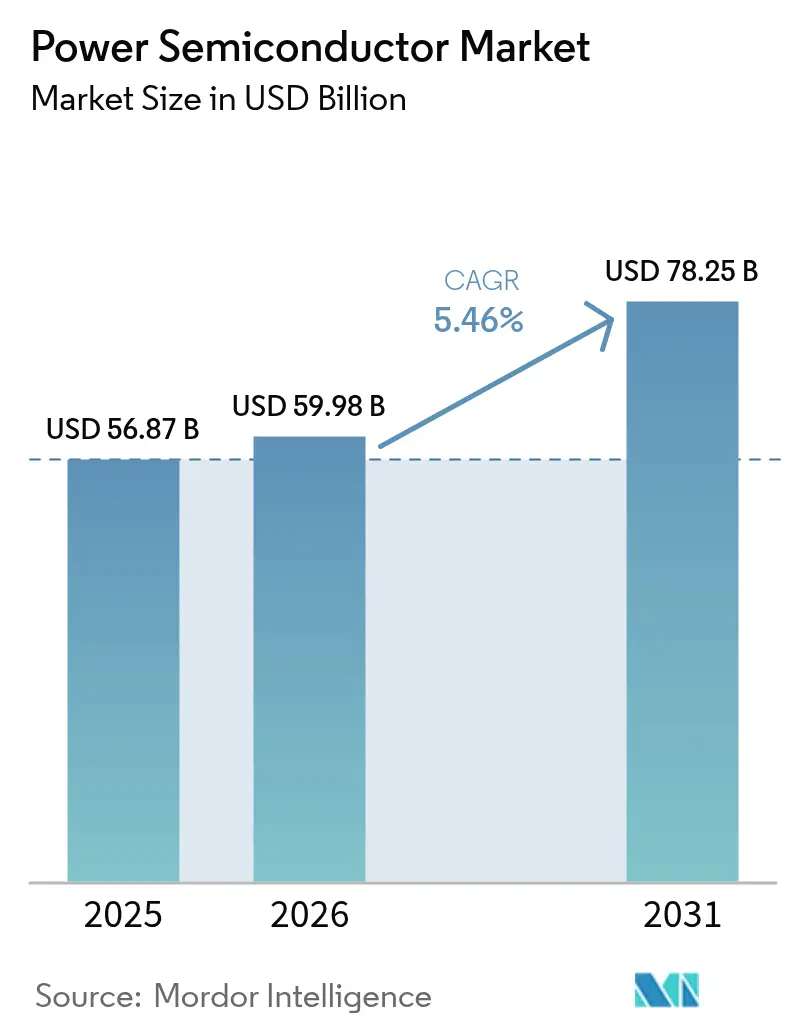

The power semiconductor market size was valued at USD 56.87 billion in 2025 and estimated to grow from USD 59.98 billion in 2026 to reach USD 78.25 billion by 2031, at a CAGR of 5.46% during the forecast period (2026-2031). Strong demand for efficient power conversion across electric vehicles, renewable energy systems, and data-intensive electronics keeps the power semiconductor market resilient even as cyclical slowdowns emerge elsewhere. Wide-bandgap (WBG) materials-chiefly silicon carbide (SiC) and gallium nitride (GaN)-command premium pricing because they outperform silicon in high-voltage and high-frequency conditions. Automotive electrification anchors volume, yet rapid growth stems from solar-plus-storage installations, 5G infrastructure rollouts, and factory automation upgrades. Regional supply-chain policies such as the U.S. CHIPS Act and the European Chips Act intensify domestic fabrication investments, while the Asia Pacific leverages its end-to-end manufacturing scale to maintain leadership.

Key Report Takeaways

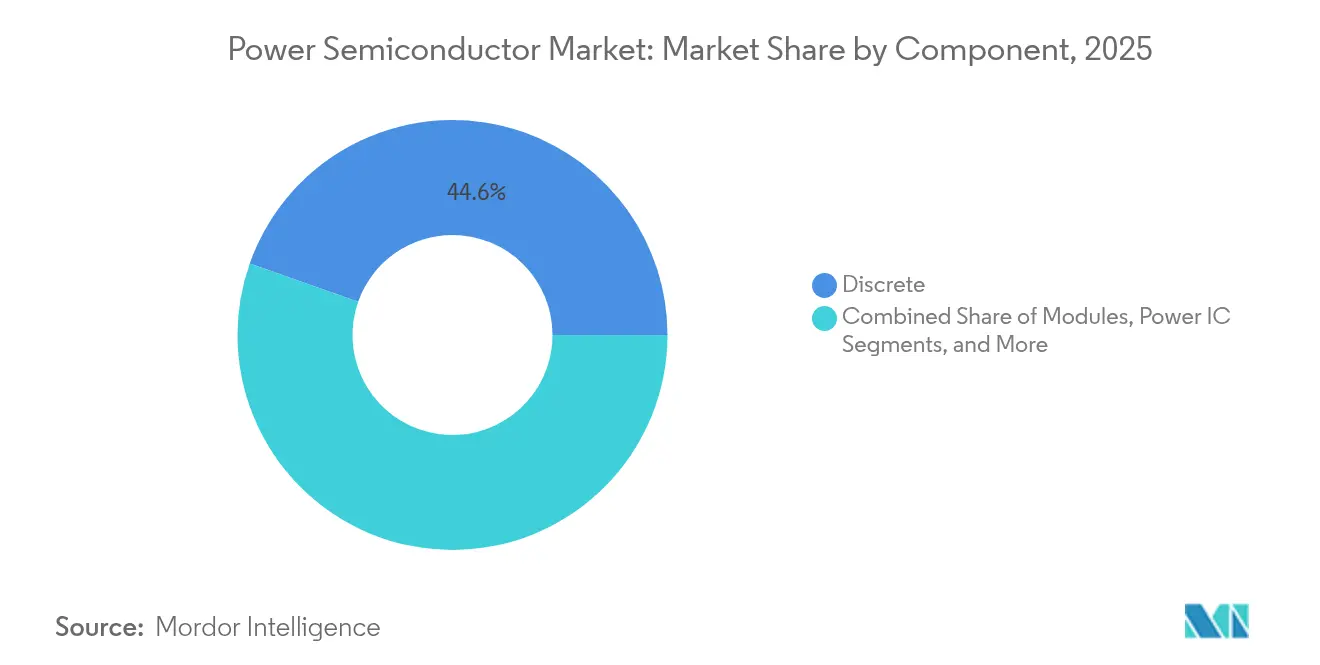

- By component, discrete devices held 44.60% of the power semiconductor market share in 2025, while power ICs are forecast to post a 6.02% CAGR through 2031.

- By material, silicon commanded 77.55% share of the power semiconductor market size in 2025, whereas GaN is projected to expand at a 9.03% CAGR to 2031.

- By end-user, automotive retained 31.02% of the power semiconductor market share in 2025, and the energy and power segment is set to register a 7.21% CAGR through 2031.

- By geography, the Asia Pacific accounted for 51.35% revenue share in 2025 and is advancing at a 6.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Power Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for EVs and charging infrastructure | +1.8% | Global, with APAC and Europe leading adoption | Medium term (2-4 years) |

| Proliferation of 5G base-stations | +0.9% | Global, with North America and APAC core markets | Short term (≤ 2 years) |

| Renewables-led power conversion growth | +1.2% | Global, with Europe and North America policy-driven | Long term (≥ 4 years) |

| Industrial automation and motor-drive upgrades | +0.8% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| HAPS and all-electric aircraft powertrains | + 0.3% | North America and Europe aerospace hubs | Long term (≥ 4 years) |

| Fast-charging 2-/3-wheeler EV architectures in Asia | +0.6% | APAC, primarily India and Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for EVs and Charging Infrastructure

Electric vehicles increasingly rely on SiC MOSFETs that raise drivetrain efficiency and shorten charging times.[1]Source: Infineon Technologies AG, "Solutions for Photovoltaic Energy Systems," Infineon.com Automakers shifting to 800 V systems specify SiC to trim inverter losses, evidenced by FORVIAs, such as onsemi’s agreement with Volkswagen, secure vertically integrated chip-to-module deliveries, mitigating allocation risks.[2]Source: Infineon Technologies AG, “FORVIA HELLA Selects Infineon’s New CoolSiC Automotive MOSFET 1200 V,” infineon.com Parallel DC fast-charger roll-outs require 8 kW to 1 MW power blocks, effectively doubling SiC demand from vehicle content alone. Automotive-grade yields stay challenging, so IDMs add captive substrate capacity to stabilize cost curves and safeguard margins.

Proliferation of 5G Base-Stations

GaN high-electron-mobility transistors deliver higher gain and efficiency than LDMOS at sub-6 GHz and mmWave frequencies. Small-cell densification pushes GaN shipments to quadruple by decade-end as operators combat escalating energy bills. NXP couples Si LDMOS with GaN die in multichip massive-MIMO modules that integrate antenna arrays and simplify thermal design. Power semiconductor suppliers add sintered die-attach materials to cope with hot-spot temperatures above 225 °C. The telecom sector’s focus on total-cost-of-ownership converts incremental efficiency gains into reduced opex, cementing GaN adoption in next-phase rollouts.

Renewables-Led Power Conversion Growth

Utility-scale solar and wind projects specify WBG devices to surpass 99% inverter efficiency thresholds. SMA Solar’s 2,000 V inverter platform integrates ROHM 2 kV SiC MOSFETs within Semikron Danfoss modules to maximize energy yield under partial-load conditions [3]Source: ROHM Semiconductor, “Semikron Danfoss Module with ROHM 2 kV SiC MOSFETs,” rohm.com. Grid-interactive storage adds bidirectional converters that favor high-frequency SiC topologies to shrink magnetics. Multilevel architectures lower filtering costs and enable compact skid designs for brownfield retrofits. Policymakers mandating low-harmonic injection provide additional pull for advanced power stages over legacy IGBT stacks.

Industrial Automation and Motor-Drive Upgrades

Smart factories adopt SiC-based drives that cut switching losses and shrink heat-sink volume by up to 70% [4]Source: Microchip Technology, “Silicon Carbide Powers the Next Generation of Industrial Motor Drives,” microchip.com . Higher switching frequencies simplify passive filtering and improve power factor, aligning with sustainability certification targets. Centralized 1,000 V DC-bus architectures distribute power at lower copper weight, boosting energy efficiency. While initial device premiums persist, falling 200 mm wafer costs narrow the differential and accelerate payback periods. Fabs prioritizing AI and automotive may squeeze industrial allocations, so OEMs diversify sourcing through qualified second-source agreements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silicon wafer supply tightness cycles | -0.7% | Global, with particular impact on Asia Pacific | Short term (≤ 2 years) |

| High cost / design complexity of WBG devices | -0.9% | Global, with cost sensitivity in emerging markets | Medium term (2-4 years) |

| Thermal limits in high-density EV inverters | -0.4% | Global, concentrated in automotive applications | Medium term (2-4 years) |

| Export controls on GaN epitaxy tools | -0.5% | China and allied countries affected differently | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Silicon Wafer Supply Tightness Cycles

Total wafer demand now eclipses qualified capacity, and inventory drawdown at memory suppliers distorts short-term purchasing behavior [5]Source: SEMI, “2025 Silicon Wafer Market: At the Threshold Between Cyclical Limits and Structural Change,” semi.org. Geopolitical friction inflates fab-construction costs, while water-usage limits restrict greenfield sites in drought-prone zones. Chinese entrants pursue price competition that compresses margins across the chain. Although front-end equipment bookings hint at recovery, end-market weakness in PCs and smartphones tempers volume pick-up, exposing structural rather than cyclical imbalances.

High Cost / Design Complexity of WBG Devices

SiC substrates incur higher defect densities, raising die-sorting losses and final part pricing. GaN lateral devices require bespoke gate-drive and layout practices unfamiliar to many OEM engineers. Design-for-manufacture guidelines evolve rapidly, increasing validation overheads. As 200 mm SiC ramps and GaN on silicon epitaxy mature, cost curves bend downward, yet sticker-shock persists among cost-sensitive consumer and motor-control segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Integration Upside for Power ICs

Power integrated circuits contributed significantly to the power semiconductor market size in 2025 and will climb at a 6.02% CAGR through 2031. Automotive battery-management units require multi-rail regulators and functional-safety diagnostics delivered in a compact PMIC footprint. Infineon’s ISO 26262-compliant OPTIREG TLF35585 underpins safety-related electronic control units, illustrating the trend toward single-chip power management . Discrete devices remain indispensable for high-current paths, preserving 44.60% revenue share; nevertheless, the discrete share edges lower as designers favor cost-optimized module or IC solutions in space-constrained subsystems.

Supplier roadmaps bundle GaN or SiC dies within intelligent power modules that integrate gate drive, sensing, and protection, shortening time-to-market for inverter and charger assemblies. Module consolidation benefits mid-volume industrial and residential energy customers who lack in-house packaging expertise. Conversely, consumer-electronics ODMs still procure discrete MOSFETs for adapter designs to exploit board-level flexibility and price advantages. The coexistence of discrete, module, and IC formats enriches the power semiconductor market, enabling tailored performance-cost trade-offs.

By Material: GaN Scales While Silicon Retains Core Volume

Silicon fueled 77.55% of revenue in 2025, anchoring the power semiconductor market share despite physical limits. Continuous superjunction MOSFET advances and mature supply networks keep silicon relevant for 650 V and below. GaN, though smaller today, records the fastest rise at a 9.03% CAGR, winning sockets in mobile fast chargers, 5G base stations, and residential solar micro-inverters. Infineon forecasts a decisive adoption inflection by 2025 as reference designs standardize gate-drive and EMI mitigation.

SiC owns high-power traction and grid sectors, where its 1,200 V and 1,700 V ratings exceed GaN's economic reach. The transition to 200 mm SiC wafers compresses cost per ampere, narrowing the gap versus superjunction silicon. Material diversification lowers concentrated supply risk and unlocks design optionality. Over the forecast horizon, designers will assign silicon to cost-driven mass-market applications, SiC to high-power transport and renewables, and GaN to high-frequency, lower-power uses, creating a balanced multi-material ecosystem.

By End-User Industry: Energy and Power Outpaces Automotive Growth

Automotive captured 31.02% of 2025 revenue thanks to battery-electric traction inverters, on-board chargers, and DC-DC converters. Yet the energy and power vertical leads expansion at a 7.21% CAGR through 2031 as utilities deploy SiC-based string and central inverters exceeding 1,500 V. Grid-storage rollouts add multi-megawatt bidirectional converters that further swell device demand. Industrial automation follows close behind, leveraging SiC drives for high-efficiency process lines and robot actuators. Consumer electronics remains the largest unit-count outlet but faces stiff ASP pressure, restricting WBG penetration to flagship notebooks and premium adapters. Healthcare, aerospace, and defense form niche high-reliability slices where performance premiums offset volume constraints, preserving high gross-margin opportunities.

Geography Analysis

Asia Pacific accounted for 51.35% of the power semiconductor market share in 2025 and sustained a 6.74% CAGR through 2031. China spearheads SiC and GaN capacity ramps, aided by state subsidies and vertically integrated supply chains. India fast-tracks an INR 7,600 crore OSAT campus targeting 15 million units per day, signaling intent to onshore assembly. Taiwan and South Korea guard leadership in advanced packaging and memory, respectively, while Japan fortifies upstream materials command.

North America benefits from USD 50 billion in CHIPS Act incentives that unlock brownfield conversions and greenfield fabs by Wolfspeed, Bosch, and overseas entrants. Automotive, defense, and data-center clusters concentrate demand, boosting local content requirements. SEMI projects regional fab-equipment outlays doubling to USD 24.7 billion by 2027, underscoring long-term scale-up .

Europe leverages its automotive and renewable energy policy alignment to catalyze SiC and GaN uptake. Germany’s EUR 5 billion Dresden fab approval exemplifies public-private alignment to elevate self-sufficiency. France and Italy offer additional grant packages to preserve leading-edge module and substrate know-how. Emerging markets across the Middle East, Africa, and Latin America stay value-conscious, adopting mature silicon platforms while gradually trialing WBG for utility-scale solar and railway electrification.

Regulatory Landscape

Industrial policy and trade controls are increasingly shaping power semiconductor supply chains, with wide-bandgap devices exposed to the sharpest sourcing and equipment constraints. In the United States, semiconductor-related trade actions intensified in January 2026 with Proclamation 11002 under Section 232 (as published in the Federal Register) and a White House two-phase tariff plan focused on certain advanced chips. This combination increases compliance burden for cross-border sourcing and increases the value of locally qualified production for OEMs serving automotive and energy programs.

In Europe, semiconductor competitiveness and supply resilience continue to be reinforced through the EU Chips Act framework and its 2026 review cycle (COM/2026/504/FIN and the accompanying SWD/2026/0504). The same framework also ties to product reliability and market access requirements that are relevant for automotive-grade power devices. Regulatory discussions around export controls and technology access also remain a factor for GaN and SiC toolchains, influencing equipment availability and qualification timelines across regions.

Value Chain Analysis

The value chain spans raw materials and wafer inputs (silicon wafers; SiC boules/substrates; GaN epitaxy), device fabrication (IDMs and foundries), and backend assembly, testing, and advanced packaging into discrete devices, modules, and power ICs sold through direct OEM/Tier-1 programs and distribution. Wide-bandgap flows add critical steps, including substrate growth and epitaxial deposition, and they tend to be more packaging-intensive than silicon. As a result, module assembly (sintered attach, high-temperature interconnects, and automotive-grade qualification) is often a throughput constraint relative to front-end capacity.

Investment and localization programs are also changing where capacity sits across the chain. In July 2026, Infineon opened its Smart Power Fab in Dresden as a EUR 5 billion project aimed at doubling capacity at the site. Bosch reached an agreement for up to USD 225 million in CHIPS Act funding tied to a USD 2 billion SiC investment in Roseville, California. In June 2026, Hitachi Energy expanded work at its Lenzburg, Switzerland power semiconductor site under its broader investment program, reflecting how grid and industrial power conversion depend on steady device supply. These moves support dual-sourcing strategies and shorter logistics paths, but they also raise the emphasis on qualification, traceability, and local ecosystem readiness for materials, tooling, and high-yield power module packaging.

Competitive Landscape

Market concentration is moderate yet edging upward. Five suppliers—STMicroelectronics, onsemi, Infineon, Wolfspeed, and ROHM—controlled more than 70% of SiC device revenue in 2024 [8]Source: Evertiq, “Five Companies Control the SiC Power Market,” evertiq.com. Vertical integration from substrate to module mitigates supply disruptions and yields cost leverage. Platform-oriented portfolios replace single-socket offerings, allowing reuse across traction, solar, and industrial drives and lowering non-recurring engineering expense.

Capacity race dynamics dominate strategy. Wolfspeed secured USD 750 million in CHIPS Act grants plus matching private capital to expand Mohawk Valley 200 mm SiC capacity [9]Source: Wolfspeed, “Wolfspeed Announces $750 M Funding Under U.S. CHIPS Act,” wolfspeed.com . onsemi acquired Qorvo’s SiC JFET assets and selected the Czech Republic for end-to-end SiC production, ensuring European supply resilience. Infineon opened a 200 mm SiC mega-fab in Malaysia, powered entirely by renewable electricity, positioning for cost leadership at scale.

Patent portfolios and equipment access emerge as competitive moats amid tightened export-control regimes. Companies increase joint-development agreements to secure tool roadmaps compliant with evolving regulations. White-space applications—such as humanoid robots requiring high-precision motor drives—attract R&D allocations, extending growth optionality beyond core markets.

Power Semiconductor Industry Leaders

-

Infineon Technologies AG

-

Texas Instruments Inc.

-

STMicroelectronics NV

-

NXP Semiconductors NV

-

Qorvo Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Data-center power delivery is emerging as a distinct opportunity alongside EV, renewables, and industrial demand, pulling more SiC and GaN content into high-efficiency AC/DC and DC/DC stages at very high rack power. Concrete industry actions support this direction, including the May 2025 Infineon and NVIDIA agreement to co-develop an 800 V direct-current power delivery architecture targeting rack power above 1 MW. That focus increases demand for high-voltage, high-efficiency switching devices and advanced packaging able to manage thermal density.

Manufacturing and supply-chain regionalization also creates whitespace for companies that can supply qualified, automotive-grade and grid-grade WBG devices with stable lead times, including 200 mm SiC transitions and scalable module platforms. In 2026, new and expanding capacity commitments highlight this pathway. Infineon opened the Smart Power Fab in Dresden (EUR 5 billion, capacity doubling at the site), and Bosch advanced its U.S. SiC manufacturing build-out in Roseville with CHIPS-linked funding and sample production activities. At the same time, OEMs and Tier-1s seeking resilience are increasing long-term wafer and module agreements and qualifying alternative package footprints, which creates room for suppliers with vertically integrated substrate-to-module capabilities and for specialized OSATs able to deliver high-yield power module assembly at automotive reliability levels.

Recent Industry Developments

- July 2026: Infineon officially opened its Smart Power Fab in Dresden, Germany, described as a EUR 5 billion investment designed to double manufacturing capacity at the site. The added front-end scale strengthens supply for automotive and industrial power devices and supports the industry shift toward localized, high-volume production in Europe.

- June 2025: Texas Instruments announced a plan to invest more than USD 60 billion across seven U.S. semiconductor fabs in Texas and Utah to expand production of foundational semiconductors. The multi-fab expansion program supports longer-term availability for power management and related analog components used across automotive, industrial, and infrastructure systems.

- May 2024: STMicroelectronics announced a EUR 5 billion program for a fully integrated silicon carbide campus in Catania, Italy, supported by EUR 2 billion from the Italian government under the EU Chips Act framework. The campus approach advances vertical integration for SiC, improving control over critical materials and device supply for EV traction, charging, and renewable energy inverters.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues generated from power semiconductors used to convert, control, and manage electrical power in end equipment, across discrete devices, modules, and power IC formats, and sold into global end-use demand.

Scope exclusions: This sizing excludes downstream power electronic systems (such as inverters and chargers) and counts only the semiconductor devices and integrated power ICs themselves.

Segmentation Overview

-

By Component

-

Discrete

- Rectifier

- Bipolar

- MOSFET

- IGBT

- Other Discrete Components (Thyristor, HEMT, etc.)

-

Modules

- Thyristor Module

- IGBT Module

- MOSFET Module

- Intelligent Power Module (IPM)

-

Power IC

- PMIC (Multichannel)

- Switching Regulators (AC/DC, DC/DC, Iso/Non-iso)

- Linear Regulators

- Battery Management IC

- Other Power ICs

-

Discrete

-

By Material

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Others

-

By End-user Industry

- Automotive

- Consumer Electronics and Appliances

- ICT (IT and Telecom)

- Industrial and Manufacturing

- Energy and Power (Renewables, Grid)

- Aerospace and Defense

- Healthcare Equipment

- Others (Rail, Marine)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- France

- United Kingdom

- Italy

- Rest of Europe

-

Asia Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

-

Africa

- South Africa

- Egypt

- Rest of Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on where power semiconductor demand comes from and how it moves with end markets. We rely on public sources such as International Energy Agency releases for EV and energy transition indicators, US International Trade Commission trade statistics for category level import export signals, World Bank macro series for industrial output and electricity access proxies, and US Patent and Trademark Office publications to track technology direction (SiC and GaN activity).

To ground the commercial side, annual reports, 10-K style filings, investor presentations, and earnings call transcripts are read for device revenue cues, capacity commentary, and mix shifts across automotive, industrial, and energy applications. Reputed press, industry association pages, and standards and regulatory references are used to sanity-check adoption timing and regional rollouts. For company financials, news and financials, and patent intelligence, we also use a paid subscription database when it helps speed up collection and cross-checking. This list is not exhaustive, and many other sources were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test assumptions that are hard to observe from public data, like realistic ASP movement by device type, supply tightness timing, and what portion of EV, industrial motor drives, and renewable installations converts into power device demand. We speak with executives, product and application leaders, and commercial managers across device makers, module suppliers, distribution channels, and OEM and integrator side buyers. Views are balanced across APAC, EMEA, and the Americas so regional demand cycles do not get overfit.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 20% | APAC: 47% |

| Mid tier: 46% | Functional/Unit leaders: 35% | EMEA: 33% |

| Smaller Players: 21% | Managers: 45% | Americas: 20% |

Market-Sizing & Forecasting

Sizing begins with a top-down build that reconstructs the demand pool from end-market activity and device intensity, then it is checked against selective bottom-up approximations so totals stay realistic. In practice, we map automotive electrification build rates, industrial motor drive and automation activity, renewable additions, and consumer appliance volumes into device demand, before applying mix assumptions for discrete, modules, and power ICs.

A few inputs that typically matter are EV production and hybrid penetration, renewable capacity additions, industrial production and capex cycle signals, average device content per platform (for example, traction inverter versus onboard charger needs), and the pace of wide bandgap adoption (SiC and GaN) versus silicon. Where the market is moving quickly, assumptions are separated by region to reflect different ramp patterns, and currency conversion is kept consistent to the chosen year.

Forecasts are produced using scenario analysis supported by regression-style checks on the most stable drivers. The short-term outlook is adjusted using what experts share about lead times, utilization, and end customer order behavior. When bottom-up checks have gaps, such as limited visibility into smaller suppliers, we fill them using distribution channel structure, import export directionality, and conservative share bands, then revalidate them in follow-up calls.

Data Validation & Update Cycle

Validation is done through repeated cross-checks between the model and independent signals, so an output that looks large or small is questioned before it is accepted. We compare implied device demand with end-market volumes, regional growth signals, and major technology shifts, and then we run variance checks when a segment moves faster than its drivers.

Before sign-off, the work goes through multi-step analyst review. Any large deltas trigger a revisit of key assumptions and, when needed, re-contact with sources to confirm what changed. The report is refreshed annually, and interim updates are made when material events occur, such as policy shifts that change EV demand, major capacity changes, or pricing resets. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Power Semiconductor Market Size Compared With Other Published Estimates

Published market sizes for power semiconductors do not always line up, even when the topic name looks the same. Differences usually come from what is counted as a power semiconductor, which end markets are weighted more heavily, and which year is used as the anchor for currency and pricing.

Key gaps often show up in whether power ICs are fully included alongside discretes and modules, how wide bandgap adoption is timed in the forecast, and whether pricing is assumed to fall steadily or to remain firm during tight supply cycles. Base year choices also matter because fast-moving automotive and renewable demand can shift the size quickly from one year to the next.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 56.87 B (2025) | |

| Global Consultancy A | USD 54.94 B (2025) | The estimate appears to anchor on a different base-year setup and may apply slower ASP progression and a more conservative wide bandgap ramp, which can pull down the 2025 total even with similar segment labels. |

| Industry Publisher B | USD 59.06 B (2025) | The higher value can come from broader inclusion around adjacent power electronics content or from using a stronger near-term demand stance for automotive and industrial, with less adjustment for mix and pricing normalization by device category. |

By tracking end-market build indicators and refreshing pricing and mix assumptions mid-cycle, Mordor Intelligence keeps the 2025 power semiconductor total tied to discrete, module, and power IC revenues, which explains why the table shows a narrower spread than longer-horizon forecasts.

Key Questions Answered in the Report

How large is the power semiconductor market in 2026 and where is it headed?

The power semiconductor market size is USD 59.98 billion in 2026 and is projected to reach USD 78.25 billion by 2031, reflecting a 5.46% CAGR.

Which sector will add the most incremental revenue over the next five years?

Energy & power applications, led by solar-plus-storage deployments, are expected to log a 7.21% CAGR through 2031, outpacing all other end-user segments.

Why are SiC and GaN gaining momentum over silicon?

SiC and GaN switch faster, handle higher voltages, and dissipate less heat, enabling lighter inverters, faster chargers, and higher-frequency telecom equipment.

Which region dominates power semiconductor production today?

Asia Pacific holds 51.35% of 2025 revenue and maintains the most complete supply chain from substrate to assembly.

How will the CHIPS Act influence North American capacity?

Federal incentives totaling more than USD 50 billion underpin new fabs by Wolfspeed, Bosch, and others, with regional equipment outlays forecast to double by 2027.

Page last updated on: