South Korea Discrete Semiconductors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

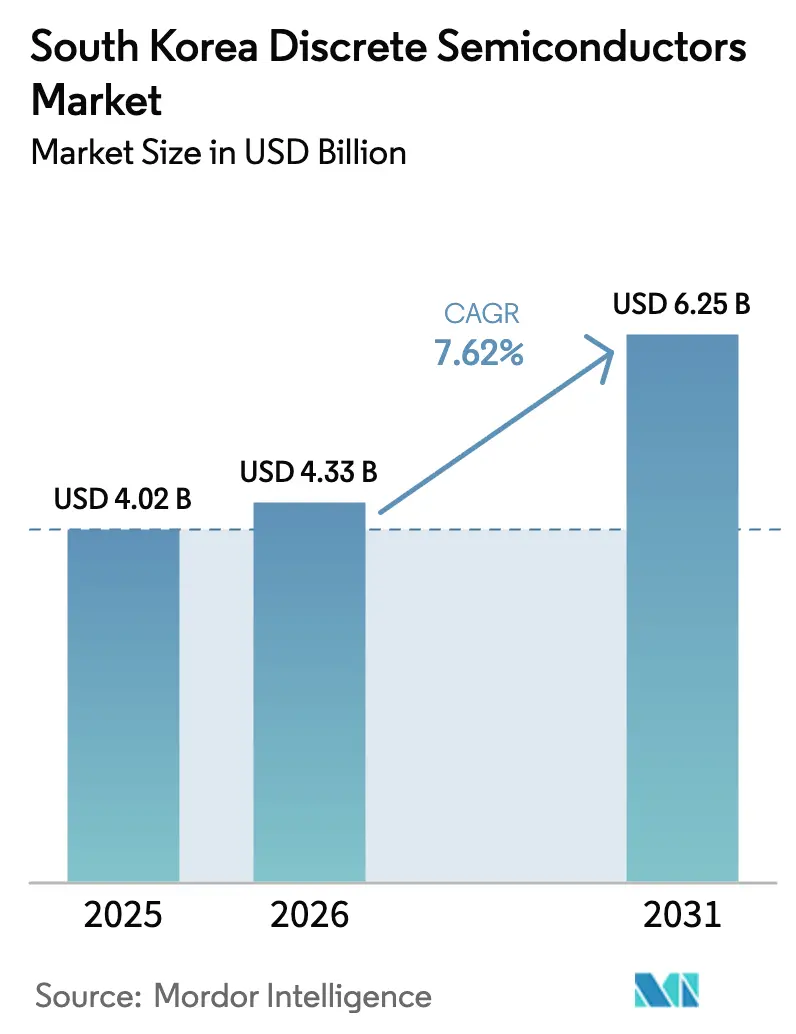

| Base Year Market Size (2025) | USD 4.02 Billion |

| Market Size (2026) | USD 4.33 Billion |

| Market Size (2031) | USD 6.25 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

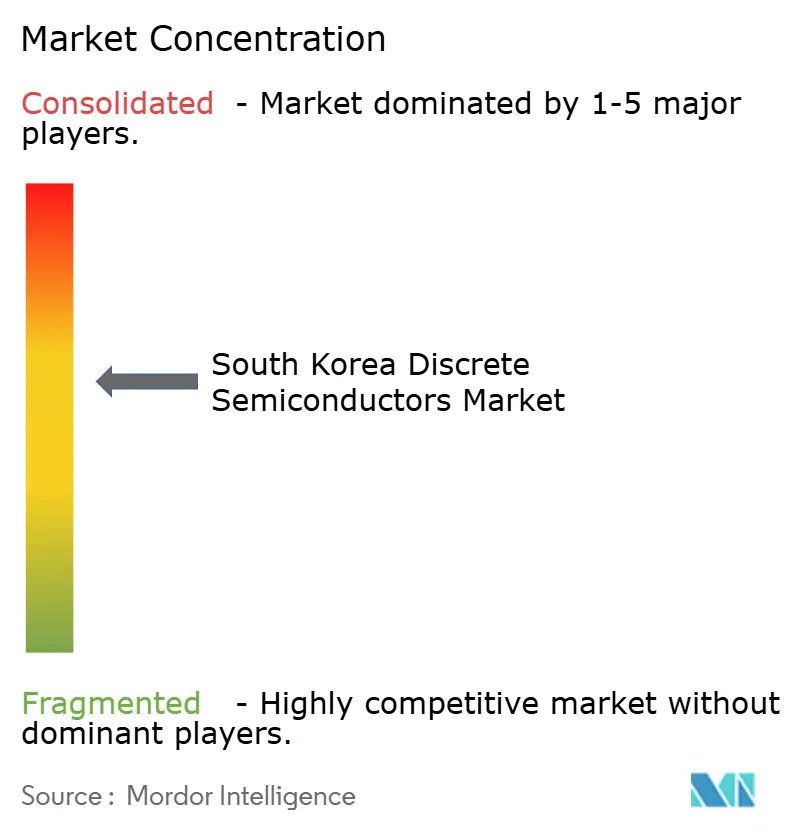

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Discrete Semiconductors Market Analysis by Mordor Intelligence

South Korea discrete semiconductors market size in 2026 is estimated at USD 4.33 billion, growing from 2025 value of USD 4.02 billion with 2031 projections showing USD 6.25 billion, growing at 7.62% CAGR over 2026-2031. This expansion is linked to the electrification of vehicles, the densification of 5G networks, and the scaling-up of domestic fabs under the K-Semiconductor Belt programme. Power transistors held a commanding 65.5% share in 2024, reflecting their pivotal role in energy conversion across automotive and industrial systems. Silicon remained the dominant material, but Silicon Carbide (SiC) posted a 19.2% CAGR on the strength of fast-charging infrastructure that demands wide-bandgap efficiency. Domestic champions such as Samsung Electronics and SK Hynix deepened vertical integration, while global suppliers—including Infineon and STMicroelectronics—leveraged specialised SiC and GaN portfolios to win automotive design slots. Capital subsidies, higher tax credits, and an established electronics ecosystem continue to attract fresh investment, even as IC-level integration and skilled-labour shortages temper long-term upside.

Key Report Takeaways

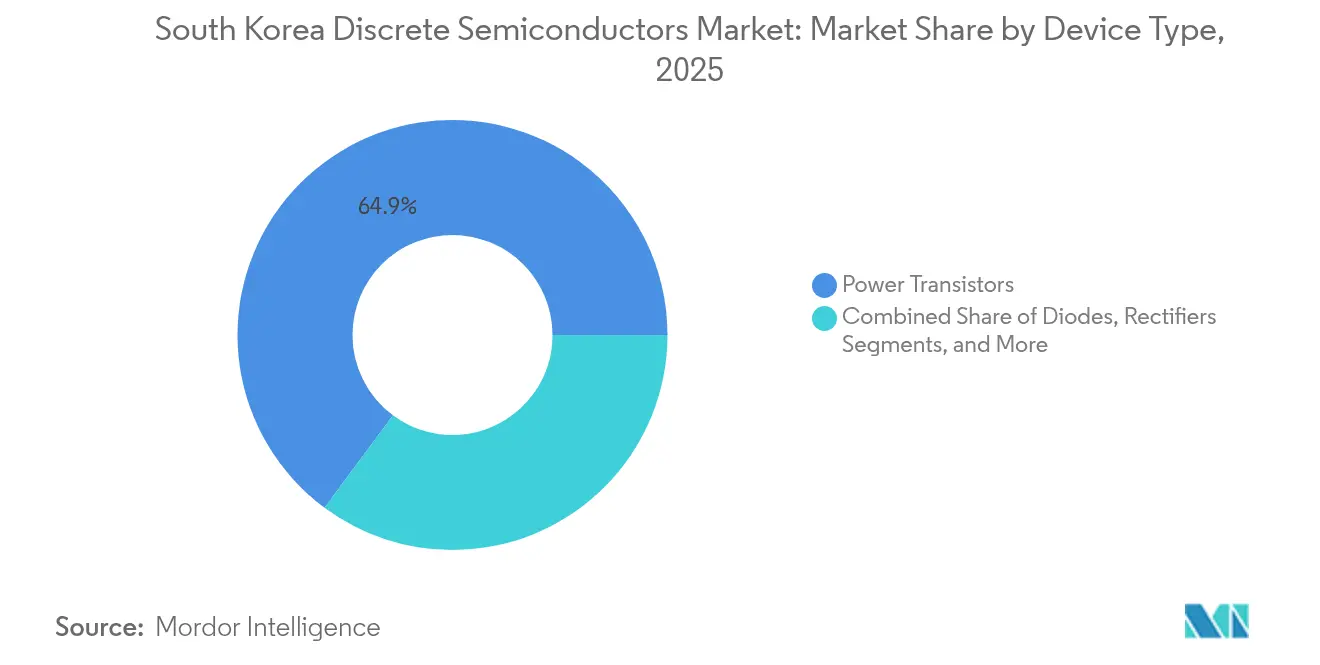

- By device type, power transistors led with 64.85% of South Korea discrete semiconductors market share in 2025; SiC devices within this class are advancing at 18.7% CAGR through 2031.

- By semiconductor material, silicon accounted for 87.95% of South Korea discrete semiconductors market size in 2025, yet SiC is forecast to expand at 18.7% CAGR to 2031.

- By voltage class, high-voltage (>600 V) discrete represented 17.55% of South Korea discrete semiconductors market size in 2025 and are growing at 11.6% CAGR to 2031.

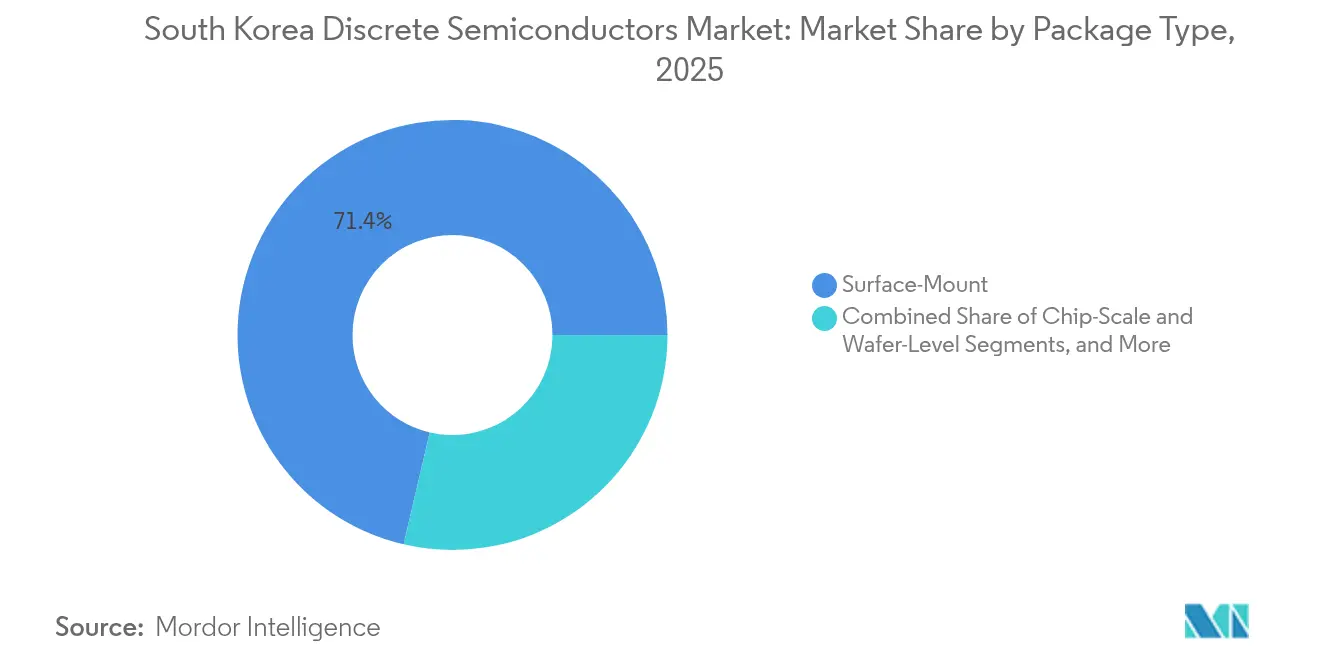

- By package type, surface-mount formats captured 71.35% revenue share in 2025, while chip-scale packages are slated to post a 15.2% CAGR by 2031.

- By end-user vertical, consumer electronics commanded 40.25% of South Korea discrete semiconductors market share in 2025; automotive is the fastest-growing sector at 15.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Competitive positioning in South korea includes both locally based firms and those operating across multiple regions. The market landscape in the global discrete semiconductor industry research shows how these players are arranged internationally.

South Korea Discrete Semiconductors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Govt-backed K-Semiconductor Belt capex subsidies accelerating domestic fab build-out | +2.1% | National – focus on Gyeonggi Province | Medium term (2-4 years) |

| Rapid EV-charging roll-out driving SiC/GaN power devices | +1.8% | Urban centres, highway corridors | Short term (≤ 2 years) |

| Memory and display equipment pull for high-spec discrete | +1.3% | Semiconductor manufacturing hubs | Medium term (2-4 years) |

| 5G base-station densification by SKT/KT/LGU+ | +1.0% | Urban centres are expanding nationwide | Short term (≤ 2 years) |

| OEM China-plus-one strategies channel imports through Korean OSATs | +0.7% | Export zones nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-Backed K-Semiconductor Belt Capex Subsidies

The government’s K-Semiconductor Belt earmarked about USD 23 billion in 2025 for new fabs and materials plants, spurring over KRW 510 trillion (USD 0.37 trillion) in pledged private investments. Samsung confirmed an additional Pyeongtaek line, while SK Hynix advanced a Yongin cluster that will bring high-volume discrete capacity online by 2027. Tax credits rose to 20% for conglomerates and 30% for SMEs in February 2025, closing capital gaps that once discouraged wide-bandgap manufacturing. These incentives lower entry costs for SiC and GaN process lines, shorten time-to-market for local suppliers and intensify competition among equipment vendors.[1]Chosun Ilbo, “Seoul Expands Semiconductor Support to $23 B,” Chosun.com

Rapid EV-Charging Roll-Out Driving SiC/GaN Power Devices

South Korean cities added hundreds of ultra-fast chargers in 2024–2025 as Hyundai’s 800 V EV architecture gained traction. SiC MOSFETs inside the chargers cut switching losses by up to 80%, enabling 350 kW stations with 30% smaller footprints compared with silicon IGBTs. Fleet operators in Seoul reported 20% energy-efficiency gains after retrofitting to SiC power modules. Vehicle OEMs mirrored the trend: next-generation on-board chargers now integrate GaN devices to shrink weight and improve thermal margins, driving incremental demand for discrete power semiconductors.

Memory and Display Equipment Supply-Chain Pull for High-Spec Discrete

Samsung’s conversion of its P2 factory to advanced DRAM, slated for 100,000 wafers per month by early 2026, plus SK Hynix’s NAND investment, required high-voltage discrete for plasma etchers, implant tools, and test handlers. Equipment suppliers turned to SiC transistors that delivered 15% energy savings and tighter process stability, meeting strict uptime targets. Display fabs followed suit, specifying discrete with higher avalanche ratings and improved heat dissipation to maximise OLED yield. These upstream requirements ripple through the South Korea discrete semiconductors market, sustaining premium ASPs for rugged power devices.

5G Base-Station Densification by SKT/KT/LGU+

The trio of mobile operators invested roughly KRW 4 trillion (USD 2.9 billion) in new 5G cells between 2024 and June 2025, part of a plan to add another KRW 5 trillion (USD 3.6 billion) by 2026. Each base station relies on GaN RF transistors that boost amplifier efficiency by 40%, trimming cooling loads and permitting compact radio designs. SK Telecom’s private 5G deployments inside semiconductor plants further increased discrete demand for high-reliability RF switches and protection devices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IC-level integration replacing stand-alone components | -1.2% | Global, affecting Korean makers | Long term (≥ 4 years) |

| Import dependency on raw wafers exposes FX volatility | -0.8% | Nationwide manufacturing hubs | Medium term (2-4 years) |

| High SiC/GaN capex thresholds restrict SME entry | -0.5% | Emerging players nationwide | Medium term (2-4 years) |

| Skilled talent shortage in power device design | -0.6% | R&D centres nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

IC-Level Integration Replacing Stand-Alone Components

Smartphone OEMs eliminated multiple discrete power regulators by adopting integrated PMICs, freeing 30% board area and cutting energy use 15%. Similar consolidation emerged in wearables and IoT sensors. Given that consumer electronics represented 40.9% of 2024 demand, such system-on-chip strategies curb unit volumes of small-signal discrete. Automotive zonal-architecture roadmaps point in the same direction, where gate-driver and sensing functions are moving into mixed-signal ASICs, placing structural pressure on long-run growth.

Import-Dependency on Raw Wafers Exposes FX Volatility

Korean discrete producers source SiC boules primarily from the United States, Japan, and Europe. The won’s slide to KRW 1,438 per USD in late 2024 lifted material costs by up to 12% for mid-tier firms, eroding margins on export contracts denominated in USD. While Samsung and SK Hynix hedge currency exposure, smaller vendors lack comparable tools, amplifying cash-flow risk. Domestic crystal-growth initiatives remain at pilot scale, so exchange-rate sensitivity will persist through 2027.[2]IT조선, “South Korea’s Industry Worries as Exchange Rate Rises,” it.chosun.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Power Transistors Anchor Growth

Power transistors generated 64.85% of 2025 revenue, placing them at the centre of the South Korea discrete semiconductors market. The class is projected to clock a 8.95% CAGR from 2026 to 2031 as EV inverters shift to 800 V architectures and industrial drives demand higher efficiency. Within this segment, MOSFETs command the largest slice, and the South Korea discrete semiconductors market size for SiC MOSFETs is on track to widen markedly alongside charger rollouts. Hyundai’s IONIQ 5 platform alone employs over 50 power transistors per vehicle, underscoring the depth of automotive pull.

Competition intensified as Infineon increased its automotive foothold to 14% globally, supplying Korean OEMs with second-generation trench-stop IGBTs that meet stringent junction-temperature requirements. Diodes and rectifiers accounted for roughly 20.35% of revenue, servicing auxiliary power rails in consumer devices and servers. Small-signal transistors took 10.05% share, where volume growth is tempered by PMIC integration. Thyristors, at 4.75%, remained vital to grid-side power controllers, a modest yet stable niche that benefits from KEPCO’s distribution-upgrade projects.

By Semiconductor Material: SiC Accelerates, Silicon Retains Scale

Silicon held an 87.95% share in 2025, reflecting its low cost and entrenched supply chain. Yet SiC ascended on steep demand for high-voltage robustness, growing 18.7% CAGR through 2031. The South Korea discrete semiconductors market size for SiC devices is expected to eclipse USD 1 billion by the end of the decade as Onsemi invests KRW 1.4 trillion (USD 1 billion) in a Bucheon fab and research centre devoted to EV-grade SiC. A leading industrial-motor maker testified to a 25% loss reduction after swapping to SiC modules.

GaN, though smaller, gained visibility in telecom and mobile fast-chargers where switching frequencies above 1 MHz cut coil volume. Other compound semiconductors—GaAs and SiGe—totalled under 3% share, yet remained indispensable in microwave links and lidar amplifiers. Despite wide-bandgap advances, silicon continues to underpin bulk commodity discrete devices thanks to mature 200 mm fabs that deliver low-cost diodes and small-signal devices.

By Voltage Class: High-Voltage Tier Leads CAGR

Low-voltage (<40 V) components formed 51.85% of 2025 shipments, mirroring their ubiquity in phones and IoT nodes. Medium-voltage (40-600 V) parts accounted for 30.60%, serving white goods and factory-automation drives. The high-voltage (>600 V) tier, with 17.55% share, is projected to grow fastest at 11.6% CAGR to 2031, powered by EV inverters, renewable-energy converters, and grid-modernisation projects. The South Korea discrete semiconductors market size for high-voltage SiC diodes is advancing as KEPCO’s smart-grid rollout specifies SiC for lower switching losses, delivering 35% energy savings in pilot substations.

OEM migrations to 800 V battery packs multiply device count and volt-ampere ratings, compelling suppliers to refine gate-drive ruggedness and short-circuit withstand times. Medium-voltage devices, meanwhile, benefit from the electrification of HVAC compressors and industrial robots, although their CAGR remains single-digit.

By Package Type: Surface-Mount Dominance Faces Chip-Scale Disruption

Surface-mount packages, including SOT and DFN, captured 71.35% share in 2025 thanks to PCB automation and compact form factors. Chip-scale and wafer-level packages, are scaling briskly at 15.2% CAGR to 2031. A Korean smartphone flagship replaced all power discrete components with chip-scale versions, trimming board area by 40% and raising thermal headroom. Automotive suppliers mirrored this shift, co-designing chip-scale IGBT modules that deliver 50% higher power density for traction inverters.

Back-side metallisation, copper clip bonding, and sintered die-attach are emerging as key differentiators. As SiC junction temperatures climb above 175 °C, package innovation becomes decisive in thermal bottleneck mitigation, an area where Korean OSATs are investing in vacuum reflow and advanced underfill.

By End-User Vertical: Automotive Surges While Consumer Electronics Holds Lead

Consumer electronics and appliances accounted for 40.25% of South Korea discrete semiconductors market share in 2025, reflecting the country’s dominance in smartphones, TVs and premium home appliances. These high-volume devices rely on low-voltage MOSFETs, ESD protection diodes and rectifiers that are produced in mature 200 mm fabs clustered around Seoul. The segment’s expansion pace is moderating as system-on-chip integration trims the bill of materials for small-signal discretes, yet replacement cycles and premium display upgrades keep unit demand stable.

Automotive applications are advancing at a 15.4% CAGR through 2031 on the back of accelerating electrification. Hyundai’s 800 V EV platforms integrate more than 300 discrete power devices per vehicle—including SiC MOSFET traction inverters and GaN on-board chargers—to maximise efficiency and driving range. Each shift to higher battery voltage elevates discrete content by close to 30%, creating a multiplier effect on demand for high-voltage, high-current packages. Telecommunications infrastructure absorbed about 14.60% of revenue, driven by GaN RF transistors used in 5 G base stations that operators SK T, KT and LG Uplus continue to densify. Industrial automation and robotics held near-9.70% share, while renewable-energy power converters and grid-scale storage systems combined for 5.05%, supported by national carbon-neutrality targets.

Geography Analysis

Gyeonggi Province dominated the national capacity in 2025. Massive campuses in Pyeongtaek, Hwaseong, and Icheon house wafer fabs that churn out both silicic diodes and emerging SiC lines. The K-Semiconductor Belt funnels infrastructure funding into this corridor, facilitating supplier clusters for gases, photomasks, and CMP slurries. Such agglomeration shortens logistics loops but concentrates seismic and water-supply risk.

The Seoul-Incheon axis contributed significant share of market value next to Gyeonggi Province, anchored by design hubs, R&D labs, and advanced-packaging houses. Onsemi operates a solution-engineering centre in Bundang, supporting camera and analogue customers, while multiple OSATs in Incheon package power modules destined for export. Proximity to consumer-electronics OEMs accelerates design cycles, an advantage for high-turnover handset discrete. Busan-Ulsan in the southeast produced nomial of discrete, leveraging automotive and heavy-industry linkages. Local university-industry programmes focus on power-device reliability for harsh maritime environments. The remaining 5.00% was distributed among emerging towns such as Daejeon, which benefits from KAIST’s talent pipeline.

Mordor Intelligence tracks the discrete semiconductor market across other major regions such as Europe, with additional country-level coverage spanning Taiwan, Japan, United States, and China, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The market shows moderate concentration, balancing scale efficiencies with room for niche specialists. Samsung Electronics anchors the domestic tier by fabricating silicon power transistors in the same complexes that build its TVs and appliances, ensuring captive demand and cost leverage. SK Hynix has broadened beyond memory into high-voltage discretes for data-centre power rails and targets a further USD 3.87 billion capacity build-out by 2027.

Among global entrants, Infineon held 17.7% of South Korea’s automotive semiconductor revenue in 2024, supplying EDT3 trench-stop IGBTs that deliver 20% lower conduction losses in EV inverters.[4]Infineon Technologies, “Infineon Introduces New Generation of IGBT Chips for Automotive,” infineon.com STMicroelectronics strengthened its foothold with a 2024 launch of automotive-grade MOSFETs that feature enhanced thermal resistance tailored to Korean OEM specifications. ON Semiconductor expanded a Bucheon SiC line to serve local traction-inverter contracts, capitalising on its KRW 1.4 trillion (USD 1 billion) investment commitment.

Specialised Korean players fill technology gaps: RFHIC commands GaN RF devices for 5 G macro cells, while BOS Semiconductors focuses on automotive body-domain chips. ROHM staked JPY 510 billion (USD 3.5 billion) through FY 2027 to lift global SiC output, signalling possible joint ventures with Korean module makers. Competitive differentiators now centre on wide-bandgap wafer quality, chip-scale packaging and certified reliability data that meet AEC-Q101 and telecom-grade standards. Firms combine R&D alliances with equipment makers and EV OEMs to co-optimise device physics and module topology, ensuring a steady pipeline of application-specific products.

South Korea Discrete Semiconductors Industry Leaders

-

Vishay Intertechnology Inc.

-

STMicroelectronics NV

-

Infineon Technologies AG

-

On Semiconductor Corporation

-

Rohm Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Samsung Electronics committed USD 17 billion to triple wide-bandgap power-device output by 2028, targeting SiC MOSFETs for automotive traction inverters.

- April 2025: SK Hynix earmarked USD 3.87 billion for a new high-voltage discrete campus, adding 2,000 jobs and reinforcing Korean supply resilience.

- March 2025: The Ministry of Trade, Industry and Energy raised total semiconductor support to USD 23 billion, allocating sizeable grants to discrete-device pilot lines.

- February 2025: Parliament lifted chip-industry tax credits to 20% for large enterprises and 30% for SMEs under the K-Chips Act.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korean discrete semiconductor market as the value of all newly-manufactured single-function devices, diodes, small-signal and power transistors (MOSFET, IGBT, bipolar), rectifiers and thyristors, built on silicon, SiC or GaN and shipped in any finished package for domestic sale or export. These parts handle switching, amplification or protection functions and are counted at first commercial sale price within South Korea's borders by either local fabs or importers.

Scope exclusion: Integrated circuits, image sensors, compound-laser diodes used purely for optical communication, and unpackaged bare die assembled only inside multi-chip modules are excluded.

Segmentation Overview

-

By Device Type

- Diodes

- Rectifiers

- Small-Signal Transistors

-

Power Transistors

- MOSFET

- IGBT

- Bipolar

- Thyristors

- Other Device Types

-

By Semiconductor Material

- Silicon (Si)

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Others (GaAs, SiGe)

-

By Voltage Class

- Low (< 40 V)

- Medium (40-600 V)

- High (> 600 V)

-

By Package Type

- Surface-Mount (SMD/SOT/DFN)

- Through-Hole (TO-, DO-)

- Chip-Scale and Wafer-Level

-

By End-User Vertical

- Automotive

- Consumer Electronics and Appliances

- Communication Infrastructure

- Industrial Automation and Robotics

- Energy and Power (Renewables, ESS)

- Aerospace and Defense

- Other Verticals (Healthcare, Lighting)

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured mail surveys with fab operations heads, EV inverter designers, distribution channel managers, and procurement leads across Seoul, Gyeonggi, and Chungcheong allowed us to stress-test unit yields, average selling prices, and import substitution rates that secondary data could not pin down with certainty. Feedback loops helped us reconcile automotive pull-through assumptions and SiC wafer adoption curves.

Desk Research

We began with production, trade and pricing lines from open sources such as Korea Customs Service HS-level exports, KSIA quarterly device output, WSTS unit shipments, Bank of Korea producer-price time series, and UN Comtrade import volumes. Company 10-Ks, investor decks and press releases supplemented cost and capacity data, while Dow Jones Factiva and D&B Hoovers supplied vetted financials for privately-held local fabs. Patent-trend pulls from Questel clarified material shifts toward SiC and GaN. The sources listed illustrate the breadth consulted; many additional datasets were reviewed before modeling.

Market-Sizing & Forecasting

A top-down construct converts production plus net-imports into domestic availability, which is then split by end-use using appliance, smartphone, EV and 5G base-station output statistics; selective bottom-up roll-ups of sampled ASP × volume from six leading distributors validate totals before final adjustment. Key variables include: EV assembly volumes, 5G macro cell deployments, smartphone shipments, SiC wafer starts, and KRW-USD parity. Multivariate regression blended with exponential smoothing projects each driver, with scenario bounds informed by primary research consensus. Data gaps, particularly in captive automotive modules, were bridged with penetration-rate proxies and re-validated with follow-up calls.

Data Validation & Update Cycle

Our analysts triangulate every model pass against WSTS Korea totals, KSIA board-level checks and quarterly earnings of the top eight suppliers. Variances beyond three percentage points trigger a re-forecast and senior analyst review. Reports refresh annually, and any material fab expansion or tariff shift prompts an interim update before client delivery.

South Korea Discrete Semiconductors Baseline Numbers You Can Rely On

Published estimates often diverge because publishers choose different device mixes, import treatment rules, and forecast cadences.

Key gap drivers here stem from narrower product scopes, reliance on listed-company revenue only, or missing gray-market imports; Mordor Intelligence factors in all commercial flows, corroborates assumptions through firsthand interviews, and refreshes the base year each June, which competitors seldom match.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.02 bn (2025) | Mordor Intelligence | - |

| USD 1.63 bn (2025) | Regional Consultancy A | excludes offshore-made devices sold via Korean EMS firms and lacks primary validation |

| USD 0.60 bn (2024) | Segment-Focused Firm B | tracks MOSFETs only and scales Korea from global ratios without country trade data |

In sum, the 2025 baseline generated through Mordor's blended top-down/bottom-up model, live local interviews and annual refresh cadence delivers a balanced, transparent figure that decision-makers can trace back to clearly stated variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the South Korea discrete semiconductors market?

The market stood at USD 4.33 billion in 2026 and is forecast to reach USD 6.25 billion by 2031.

Which device type leads revenue in South Korea?

Power transistors are the largest category, accounting for 64.85% of 2025 sales owing to their critical role in EV and industrial power stages.

How fast are Silicon Carbide devices growing?

SiC discrete devices are expanding at 18.7% CAGR through 2031, outpacing all other material segments as fast-charging and 800 V EV systems proliferate.

What government incentives support domestic semiconductor fabs?

The K-Semiconductor Belt and K-Chips Act provide capital subsidies and tax credits of up to 20% for conglomerates and 30% for SMEs, catalysing new wide-bandgap fabs.

Which end-user sector is the fastest growing?

Automotive applications are growing at 15.4% CAGR, driven by rising semiconductor content in electric vehicles and onboard chargers.

How concentrated is market competition?

The top five players command roughly 59.20% of revenue, indicating moderate concentration with space for specialised Korean challengers.

Page last updated on: