Gallium Arsenide GaAs Wafer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

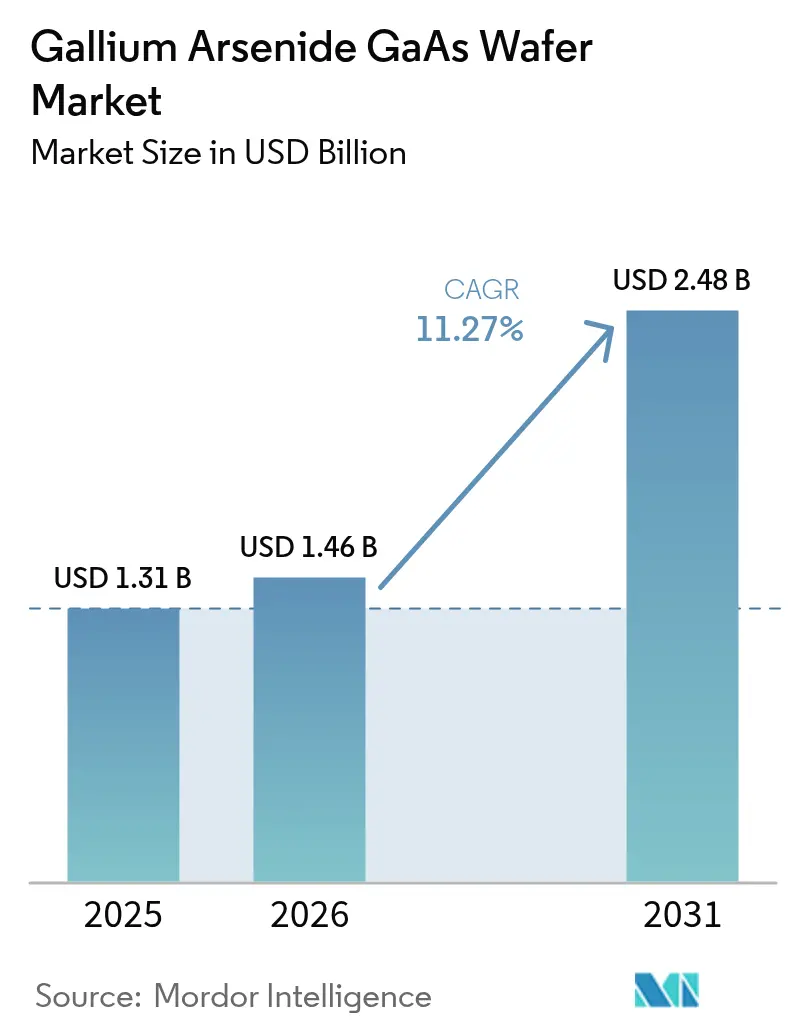

| Market Size (2026) | USD 1.46 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 11.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gallium Arsenide GaAs Wafer Market Analysis by Mordor Intelligence

Gallium arsenide wafer market size in 2026 is estimated at USD 1.46 billion, growing from 2025 value of USD 1.31 billion with 2031 projections showing USD 2.48 billion, growing at 11.27% CAGR over 2026-2031. Robust demand for high-frequency radio modules, optoelectronic emitters, and defense-grade radar devices keeps Gallium arsenide substrates firmly positioned where silicon performance plateaus. Large telecom operators are refreshing network hardware to 5G standards, compelling front-end module suppliers to specify GaAs power amplifiers that outperform CMOS at millimeter-wave bands.[1]Qorvo, “Fiscal 2025 Third Quarter Results,” qorvo.com In parallel, data-center operators adopt VCSEL arrays on GaAs to move 400G and 800G traffic with lower latency, while micro-LED innovators count on GaAs epi uniformity to scale augmented-reality headsets. Investment patterns confirm that Asia-Pacific fabs leverage vertical integration and cost advantages to supply global customers, even as North America rings-fences critical military demand for radiation-hardened wafers. Breakthrough concepts such as remote epitaxy promise to recycle substrates, hinting at future shifts in GaAs consumption economics without dampening near-term demand.

Key Report Takeaways

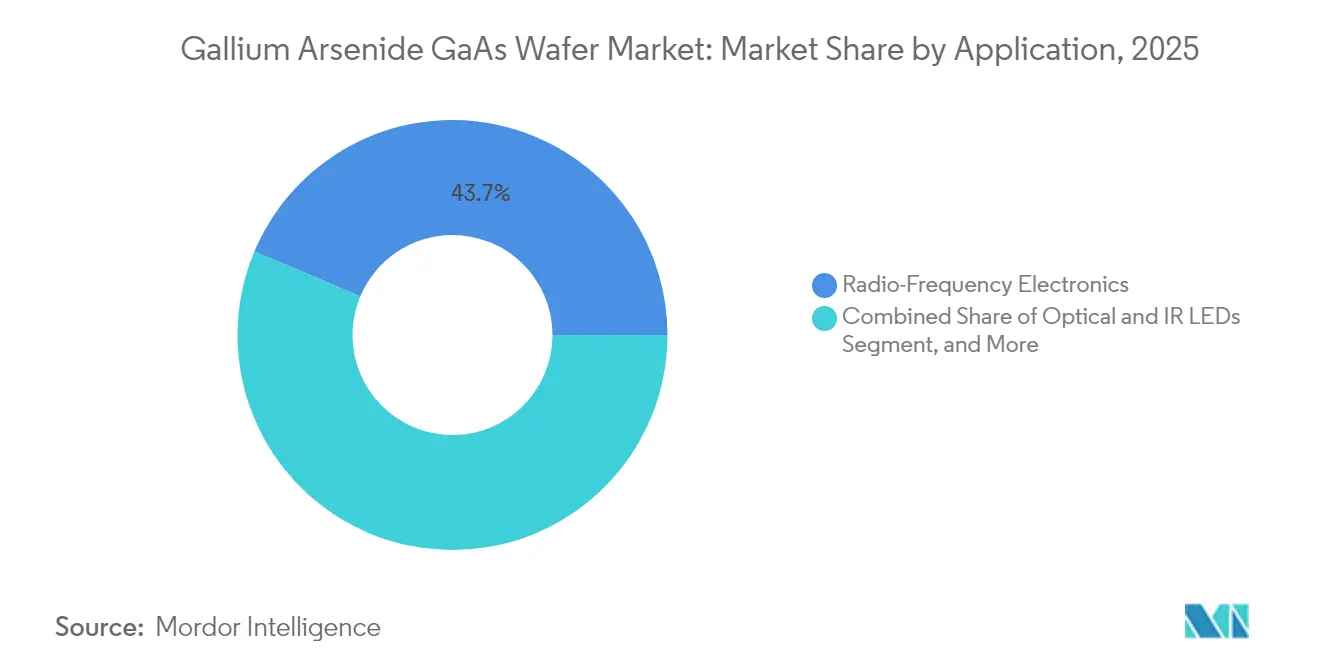

- By application, RF electronics led with 43.65% of the Gallium arsenide wafer market share in 2025; photonic and imaging devices are advancing at a 13.25% CAGR through 2031.

- By wafer diameter, 4-inch substrates accounted for 35.85% of the Gallium arsenide wafer market size in 2025, while 6-inch formats are expanding at a 12.85% CAGR to 2031.

- By growth technology, VGF captured 38.75% of the Gallium arsenide wafer market share in 2025; MBE is set to grow at a 13.1% CAGR over the forecast horizon.

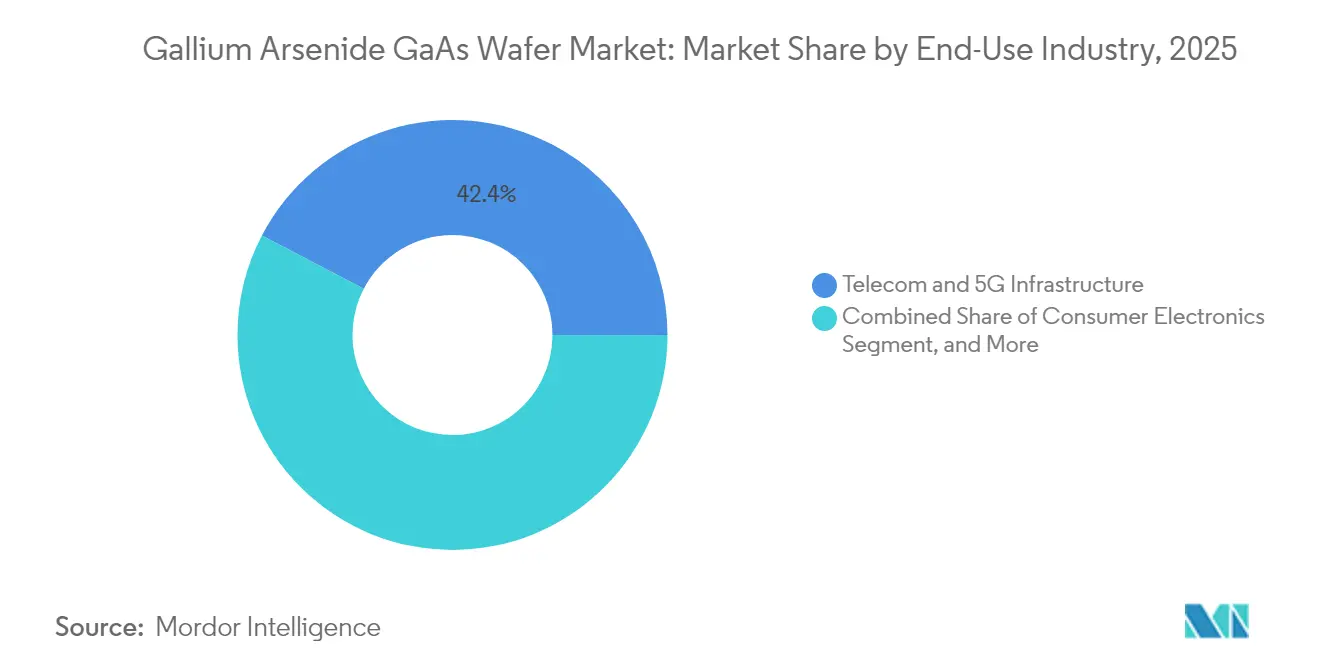

- By end-use industry, telecom and 5G infrastructure commanded 42.35% of the Gallium arsenide wafer market share in 2025, whereas automotive applications recorded the highest projected CAGR at 12.05% through 2031.

- By conductivity type, semi-insulating GaAs retained 53.15% share of the Gallium arsenide wafer market size in 2025, and semi-conducting substrates are forecast to accelerate at 11.95% CAGR to 2031.

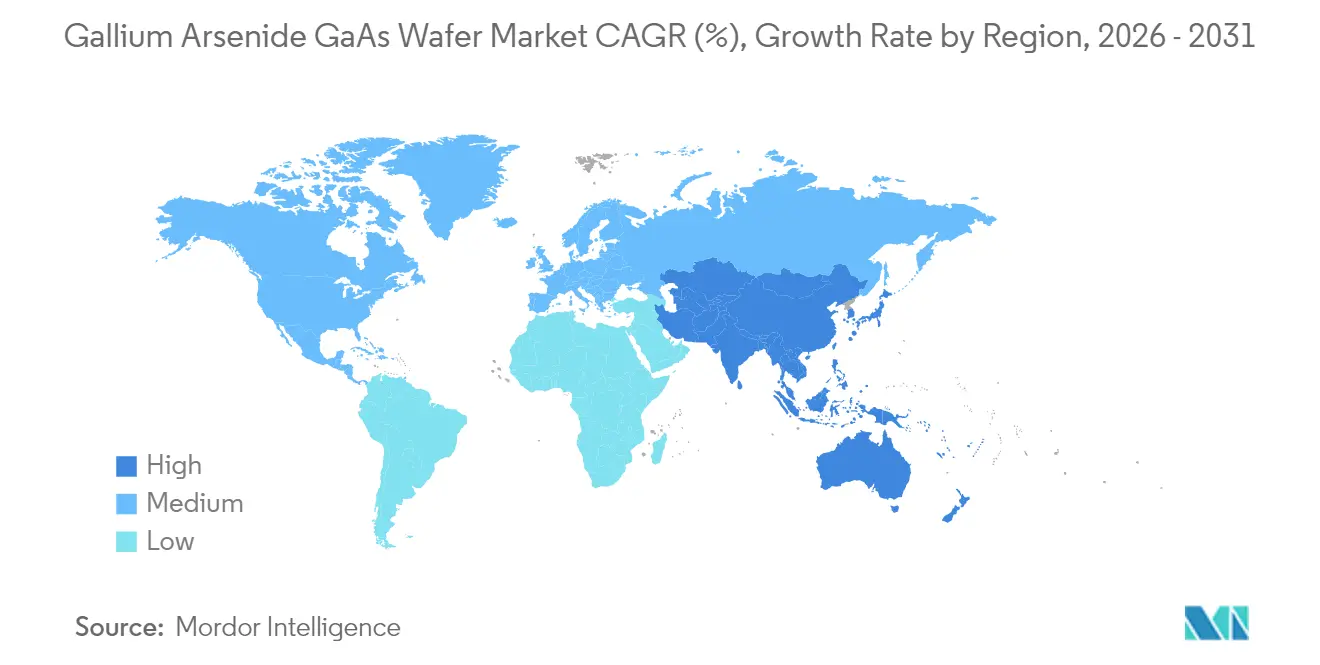

- By geography, Asia-Pacific dominated with 60.10% of the Gallium arsenide wafer market share in 2025 and remains the fastest-growing region at 11.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gallium Arsenide GaAs Wafer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G infrastructure roll-out fuels GaAs RF demand | +2.8% | Global with APAC core | Medium term (2-4 years) |

| Optoelectronic device boom (VCSELs, lasers) | +2.1% | Global, Asia-Pacific hubs | Medium term (2-4 years) |

| Aerospace and defense uptake for high-freq radar | +1.6% | North America and Europe | Long term (≥ 4 years) |

| Asian epitaxy capacity boosts supply and lowers ASP | +1.4% | Asia-Pacific | Short term (≤ 2 years) |

| Micro-LED adoption in AR/VR wearables | +1.8% | Global early adoption | Long term (≥ 4 years) |

| Remote-epitaxy substrate reuse cuts wafer cost | +1.7% | Advanced manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Infrastructure Roll-out Fuels GaAs RF Demand

Telecom operators are deploying dense 5G macro- and small-cell sites that require power amplifiers sustaining linear output well above 28 GHz, where silicon LDMOS falters. Gallium arsenide wafers deliver electron mobility around 8,500 cm²/V·s, enabling efficient front-end modules that preserve signal integrity in massive-MIMO arrays for urban coverage. Network vendors lock multiyear supply contracts with vertically integrated GaAs houses, converting 4G hardware refresh cycles into predictable demand through 2027.

Optoelectronic Device Boom (VCSELs, Lasers)

Hyperscale data centers move to 400G and 800G optics that rely on GaAs-based VCSEL arrays for lower latency and power draw. Smartphone makers embed 3D-sensing VCSELs in biometric modules, while automotive OEMs adopt GaAs lasers for LiDAR. Epitaxial regrowth advances improve thermal dissipation, extending device lifetimes and sustaining premium wafer ASPs.

Aerospace and Defense Uptake for High-Frequency Radar

Active electronically scanned arrays in fighter jets and naval radar require thousands of radiation-hard GaAs MMICs that maintain gain over extreme temperatures. Long government procurement cycles secure high-purity semi-insulating substrates, anchoring a steady revenue stream for specialized U.S. and European foundries.[2]IEEE, “GaAs MMIC Reliability and Space Qualification Guide,” ieee.org

Asian Epitaxy Capacity Boosts Supply and Lowers ASP

Taiwanese, South Korean, and mainland Chinese fabs added multi-reactor lines that drive wafer throughput and shorten lead times. Cost advantages from clustering epi, polishing, and metrology under one roof translate into lower average selling prices, widening accessibility for consumer applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost vs Si and SiC | -1.9% | Global | Short term (≤ 2 years) |

| Gallium supply concentration and export controls | -2.3% | Global, non-Chinese fabs | Medium term (2-4 years) |

| GaN and SiC competition in RF / power | -1.4% | Global | Medium term (2-4 years) |

| Environmental and safety compliance | -0.8% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Cost vs Si and SiC

GaAs crystal pulling needs pressurized arsenic atmospheres and toxic-gas handling that raise CapEx and Opex above silicon. Smaller 4-inch and 6-inch formats cannot match the die-per-wafer economics of 300 mm silicon, limiting GaAs uptake in price-sensitive consumer gadgets.[3]Stanford Advanced Materials, “Essential Electronic Materials: Part 4 – Gallium Compounds,” samaterials.com

Gallium Supply Concentration and Export Controls

China refines most of the world’s gallium, and new export licensing rules increase material lead times for foreign fabs. Alternative sources exist but require fresh hydrometallurgical capacity, elongating risk-mitigation timelines and pressuring inventories.[4]U.S. Department of Energy, “Low-Cost, High-Efficiency III-V Photovoltaics Enabled by Remote Epitaxy,” energy.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: RF Electronics Anchors Demand While Photonics Accelerates

RF electronics held 43.65% revenue in 2025 as power amplifiers and switches remain core to 5G infrastructure upgrades. This portion of the Gallium arsenide wafer market size is forecast to climb steadily alongside small-cell densification plans. Photonic and imaging devices, propelled by VCSEL interconnects and AR/VR optics, are set to outpace all other uses at 13.25% CAGR, thereby reshaping future volumes of the Gallium arsenide wafer market.

Cross-segment pull-through emerges as handset makers integrate VCSEL-based face ID modules, boosting both photonics and RF volume on common 6-inch epi lines. Solar cells on GaAs remain a niche for spacecraft, yet new heterointegration concepts could push multi-junction designs into terrestrial concentrator arrays.

By Wafer Diameter: Transition Toward 6-Inch Formats Gains Momentum

Four-inch substrates still command 35.85% revenue thanks to mature tooling, but capacity announcements reveal that 6-inch lines will absorb most incremental demand at 12.85% CAGR. The shift improves die counts per run and spreads fixed costs, nudging the overall Gallium arsenide wafer market toward lower ASPs.

Equipment vendors tackle thermal-gradient control and arsenic vapor management to scale beyond 6 inches. Early 8-inch pilot runs show promise yet require further defect reduction before commercial deployment.

By Growth Technology: VGF Dominance Meets MBE Precision

VGF yielded 38.75% of revenue in 2025 by balancing throughput with low dislocation density. However, MBE shipments are rising 13.1% annually as quantum dot emitters and telecom lasers need atomic-scale layer control. Hybrid flows combining VGF bulk growth with MBE epi caps are emerging to optimize both cost and performance.

MOCVD enjoys a share in LED and micro-LED backplanes by offering faster growth rates, while LEC remains indispensable for semi-insulating material used in defense radar.

By End-Use Industry: Telecom Leads, Automotive Surges

Telecom infrastructure consumed 42.35% of wafer output in 2025, reflecting relentless 5G roll-outs. Automotive volumes are poised to lift at a 12.05% CAGR as radar and LiDAR modules migrate from silicon to compound semiconductors for longer range and higher resolution.

Consumer electronics sustains steady mid-single-digit growth on handset RF upgrades, whereas aerospace and defense secure a premium niche that values substrate purity over price.

By Conductivity Type: Semi-Insulating Holds Majority, Doped Wafers Gain Ground

Semi-insulating material preserved a 53.15% share in 2025, indispensable for high-isolation RF devices. Doped n-type and p-type wafers are growing 11.95% annually, driven by photonic emitters where controlled carrier densities dictate emission efficiency.

Advanced fabrication now patterns selective regions of contrasting conductivity on one wafer, allowing co-integration of RF and photonic functions and opening fresh design latitude.

Geography Analysis

Asia-Pacific held 60.10% of the Gallium arsenide wafer market in 2025 thanks to clustered epitaxial lines, a deep subcontract base, and state-backed 5G build-outs. Government incentives help mainland China expand compound-semiconductor fabs, while Taiwan and South Korea provide foundry and equipment synergies that reinforce supply diversity.

North America ranks second, anchored by aerospace and defense demand requiring secure on-shore production. Recent CHIPS Act incentives finance new crystal-growth reactors and cleanrooms dedicated to semi-insulating material for radar and satellite programs, cementing long-term domestic supply.

Europe retains strength in automotive and industrial automation. Tier-1 suppliers source GaAs power devices to support ADAS radar and factory sensing, while stringent environmental directives spur circular-economy research on wafer reclamation. Coordinated EU funding backs pilot lines for 150 mm compound-semiconductor substrates, seeking to narrow the capacity gap with Asia.

Regulatory Landscape

Gallium arsenide (GaAs) wafer supply chains operate under tightening trade and security controls that affect both raw gallium availability and downstream compound-semiconductor shipments. China, through MOFCOM, has used export licensing and time-bound policy adjustments for dual-use materials, including a one-year suspension window tied to gallium-related controls that runs through 27 November 2026, keeping lead times and compliance documentation central to procurement planning for non-Chinese fabs.

In the United States, the Department of Commerce, Bureau of Industry and Security (BIS) continues to update advanced-computing and semiconductor-related control frameworks that shape equipment and technology transfers relevant to compound semiconductor manufacturing. In April 2026, BIS extended the timeline for companies to submit Approved IC Designer applications until 31 December 2026, reinforcing the importance of end-use screening and license strategy for suppliers serving defense-grade radar and electronic-warfare programs that rely on semi-insulating GaAs substrates.

Value Chain Analysis

The GaAs wafer value chain starts with upstream gallium sourcing (largely as a byproduct of aluminum refining) and arsenic supply, followed by crystal growth (LEC, VGF, HB), wafering (slicing, lapping, polishing), and metrology. Wafers then move into epitaxy (MBE and MOCVD) to produce epi-wafers for RF power amplifiers, switches, VCSELs/laser diodes, and other photonic devices. Device fabrication at IDMs and foundries, packaging, and module integration then feed telecom infrastructure, data-center optics, automotive sensors, and defense systems.

A key structural feature is upstream concentration, with the substrate market consolidated around a limited set of producers such as Sumitomo Electric Industries, Freiberger Compound Materials, and AXT (through Beijing Tongmei). As a result, the chain is sensitive to policy-driven raw-material and export disruptions. During 2026, sustained increases in gallium input costs and supply constraints flowed through to higher GaAs substrate and epi-wafer pricing, leading foundries and epi houses to renegotiate customer pricing and prioritize capacity for higher-value segments such as optical interconnects and satellite communications. Taiwan-based epitaxy suppliers also implemented price increases for GaAs and InP epi-wafers as cost pressure persisted.

Competitive Landscape

The Gallium arsenide wafer market features moderate concentration, with vertically integrated players spanning crystal growth, epi, and device fabrication to secure quality and margins. Leading suppliers deploy proprietary VGF and MBE recipes that cut dislocation counts, enabling foundry customers to lift RF yields above 90% per run. Long-term supply agreements with telecom and defense primes create entry barriers for newcomers.

Strategic moves include large-diameter capacity additions in Asia-Pacific, evident in a USD 345 million expansion that will push annual output beyond 1.5 million 6-inch wafers. Simultaneously, U.S. incumbents acquire metrology startups to characterize sub-ppm arsenic vacancies, sharpening device performance for space payloads.

Emerging disruptors focus on remote-epitaxy IP, offering wafer-reuse cycles that could slash substrate cost of ownership by 60%. While not yet commercial, such technology has garnered joint-development agreements with photonics integrators seeking thinner, transferable GaAs membranes.

Gallium Arsenide GaAs Wafer Industry Leaders

AXT Inc.

Freiberger Compound Materials GmbH

Sumitomo Electric Industries, Ltd.

Xiamen Powerway Advanced Material Co., Ltd.

Applied Materials, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace area is capacity and supply assurance for photonics-driven demand, particularly where GaAs substrates and epi-wafer specifications are optimized for high-speed optical interconnects and satellite communications. In 2026, Win Semiconductors highlighted demand growth for 1.6T optical communication module components tied to AI data centers and LEO satellite markets, supporting stronger pull-through for GaAs-based lasers and VCSEL-related supply chains beyond the traditional smartphone RF cycle.

Another opportunity is value capture through material efficiency and circularity, since export controls and input-cost volatility raise the total cost of ownership for GaAs substrates. In 2026, manufacturers raised prices for GaAs and InP products in response to sustained raw gallium cost increases and supply constraints, pushing customers to favor suppliers that can secure feedstock, offer longer-term allocation, or introduce recycling and recovery pathways. Industrial actions such as Freiberger Compound Materials commissioning a gallium recovery facility in Freiberg, Germany, provide a tangible pathway for localized raw-material supplementation that aligns with European supply-chain resilience goals and reduces exposure to single-region refining dependencies.

Recent Industry Developments

- June 2026: AXT, Inc. reported that its subsidiary Beijing Tongmei Xtal Technology entered a long-term supply agreement with Nanjing Casela Technologies Corporation, Ltd. to reserve production capacity and supply indium phosphide (InP) wafer substrates during 2027. The agreement formalizes forward capacity allocation in III-V substrates, reinforcing tighter customer-supplier planning amid constrained raw-material availability and volatile substrate pricing.

- January 2025: MACOM committed USD 345 million to expand compound-semiconductor capacity in Asia-Pacific, targeting 5G and defense sectors. This investment strengthened regional supply for GaAs-related device and substrate ecosystems and intensified competitive pressure on incumbents to scale 6-inch output and shorten lead times.

- December 2024: Coherent sold its U.K. GaAs fab to the Ministry of Defence for USD 25.2 million, supporting continuity of domestic supply for military programs. The transaction underscored the strategic role of onshore compound-semiconductor capabilities for defense procurement and the premium placed on secure, qualified wafer supply chains.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from supplying gallium arsenide (GaAs) wafers that are used as the starting substrate for making GaAs-based electronic and photonic devices, across the geographies covered in the report.

Scope exclusions: Excludes finished GaAs devices and modules (such as RF front end components and LEDs) and also excludes non-GaAs compound semiconductor substrates.

Segmentation Overview

- By Application

- Radio-Frequency Electronics

- Optical and IR LEDs

- Photovoltaic / Solar Cells

- Photonic and Imaging Devices

- Other Applications

- By Wafer Diameter

- 2 inch (50 mm)

- 3 inch (76 mm)

- 4 inch (100 mm)

- 6 inch (150 mm)

- 8 inch (200 mm) and Above

- By Growth Technology

- Liquid-Encapsulated Czochralski (LEC)

- Vertical Gradient Freeze (VGF)

- Horizontal Bridgman (HB)

- Molecular Beam Epitaxy (MBE)

- Metal-Organic CVD (MOCVD)

- By End-Use Industry

- Telecom and 5G Infrastructure

- Consumer Electronics

- Aerospace and Defense

- Automotive (ADAS, EV)

- Industrial and Energy

- By Conductivity Type

- Semi-insulating GaAs

- Semi-conducting GaAs (n-/p-type)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the ground rules for what a GaAs wafer is in commercial terms and to map where demand is coming from (RF electronics, LEDs, photovoltaics, and photonic devices). We used public sources such as the USGS for gallium-related supply context, the US International Trade Commission trade data for import and export signals, and the World Semiconductor Trade Statistics releases for broader semiconductor demand direction.

We also reviewed sources such as IEEE and other peer-reviewed journals for technology shifts like wafer diameter migration and yield learning, then complemented those with annual reports, investor presentations, and press releases to track capacity additions and product mix changes. For cross-checking company footprint and news flows, we used standard company financials and intelligence subscriptions, plus patent databases to validate the pace of process and epi-related filings. These desk sources are not exhaustive, and we reviewed additional public materials to support data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating wafer demand by application and understanding how pricing moves with diameter, crystal quality, and supply tightness. We interviewed a mix of wafer suppliers, downstream device manufacturers, distributors, and industry experts across APAC, EMEA, and the Americas. These inputs were used to confirm assumptions that were unclear in public sources and to pressure test the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | APAC: 45% |

| Mid tier: 51% | Functional/Unit leaders: 39% | EMEA: 37% |

| Smaller Players: 19% | Managers: 49% | Americas: 18% |

Market-Sizing & Forecasting

Market sizing started with a top-down build that reconstructs the addressable wafer demand pool by application, linking device build cycles to wafer consumption patterns, and then converting that into value using typical GaAs wafer ASP bands. After the demand pool was formed, we checked it using selective bottom-up approximations, including sampling supplier revenue disclosures, channel discussions on mix by diameter, and volume-to-value sanity checks.

In parallel, we tracked practical model drivers to keep results grounded, including GaAs wafer diameter mix shifts, observed capacity expansion and utilization commentary, and the RF and photonic device production outlooks that determine how much GaAs content is pulled through each cycle. We also used pricing movements tied to yield and crystal quality. Where direct volume signals were not available for a niche end use, we used proxy ratios based on similar applications, then validated those proxies with expert feedback.

For forecasting, we used scenario analysis supported by simple regression-style relationships between application demand indicators and wafer consumption, and then aligned the forward view with what interviewees described as the most likely supply and pricing trajectory. The goal was to keep the steps repeatable with data that can be refreshed annually.

Data Validation & Update Cycle

Outputs were triangulated across multiple checks, including consistency between application demand direction and implied wafer value growth, and variance checks against capacity and utilization signals discussed by market participants. When results looked off, assumptions were reopened, and follow-up questions were sent back to selected respondents to confirm whether the change was real or the result of a definition mismatch.

Before sign-off, the model and calculations go through multi-step analyst review so that unit conversions, currency handling, and segment allocations remain consistent. The report is refreshed on an annual cycle, and interim updates are triggered when material events occur, such as major capacity announcements, supply disruptions, or sharp pricing moves. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Gallium Arsenide Gaas Wafer Market Size Measured Against Other Published Estimates

Published market numbers for GaAs wafers can differ even when the end topic looks similar, because the counted item is not always the same and the time windows are often set differently. Some sources rely more heavily on company commentary, while others anchor the model on end market demand signals, which can move the total up or down.

Finished GaAs devices and RF modules sit outside Mordor Intelligence's scope here, so the value is kept at the wafer substrate level, which reduces double counting when device pricing expands faster than wafer ASPs. The spread also reflects how wafer diameter mix is treated, how price progression is assumed during capacity ramps, and whether currency conversion is done using a single-year average or a multi-year blend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.46 B (2026) | |

| Industry Publisher A | USD 0.78 B (2026) | Uses a narrower value construct that appears closer to merchant wafer revenue only, and the implied starting base is lower due to limited coverage of captive wafer use and fewer application-level demand checks. |

| Industry Publisher B | USD 1.29 B (2024) | Anchors on a different base year and broader segment splits, but does not clearly show how wafer ASP changes with diameter and quality over time, which can compress the forward value curve. |

The comparison shows that most of the difference is explained by what gets counted as wafer revenue and how captive supply is treated, followed by the year used for anchoring the math. By keeping the inputs tied to observable application demand, diameter mix, and realistic pricing movement, we produce a market view that is easy to trace and update without relying on hard-to-verify assumptions.

Key Questions Answered in the Report

How large is the Gallium arsenide wafer market in 2026?

It is valued at USD 1.46 billion, with an 11.27% CAGR projected through 2031.

Which application currently generates the most wafer demand?

RF electronics for 5G infrastructure accounts for 43.65% of 2025 revenue.

Why are 6-inch substrates gaining popularity?

They offer better die economics, driving 12.85% CAGR while equipment advances manage thermal stresses.

What region dominates GaAs wafer manufacturing?

Asia-Pacific holds 60.10% share due to dense epitaxial capacity and robust 5G investments.

How do export controls impact supply?

China¢s tight gallium control can lengthen lead times for non-Chinese fabs, adding a -2.3% drag on forecast CAGR.

Are alternative crystal growth methods emerging?

Yes, remote epitaxy enables wafer reuse and MBE adoption is rising 13.1% annually for precision heterostructures.

Page last updated on: