Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

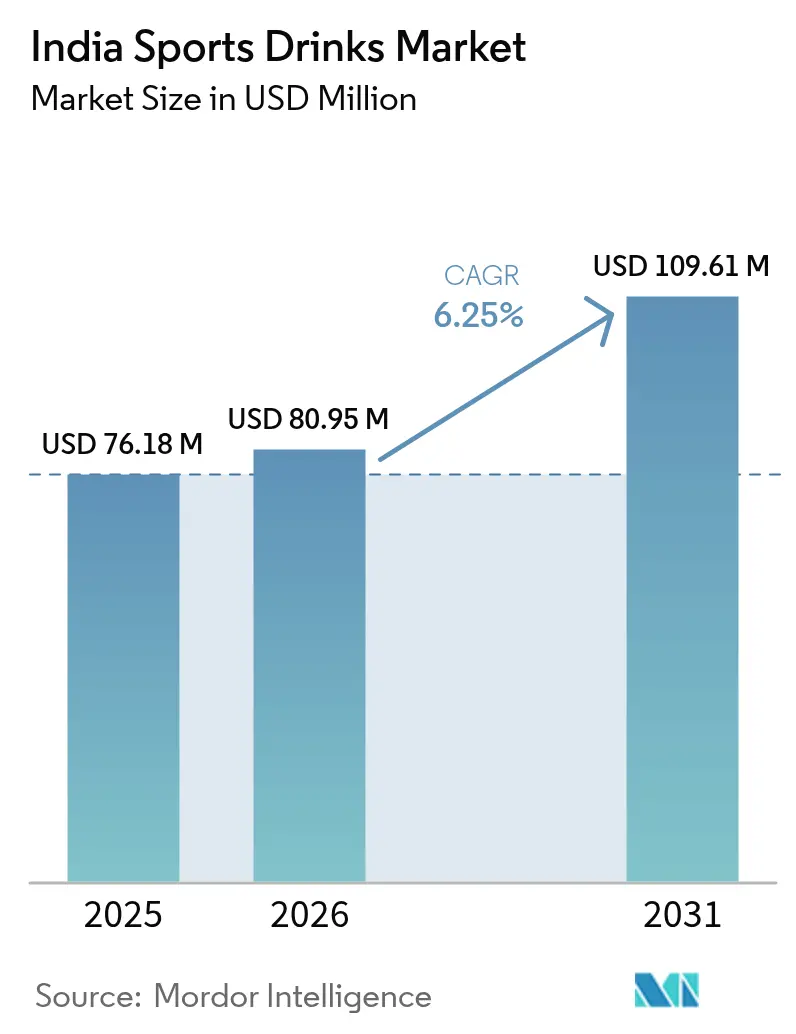

| Base Year Market Size (2025) | USD 76.18 Million |

| Market Size (2026) | USD 80.95 Million |

| Market Size (2031) | USD 109.61 Million |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

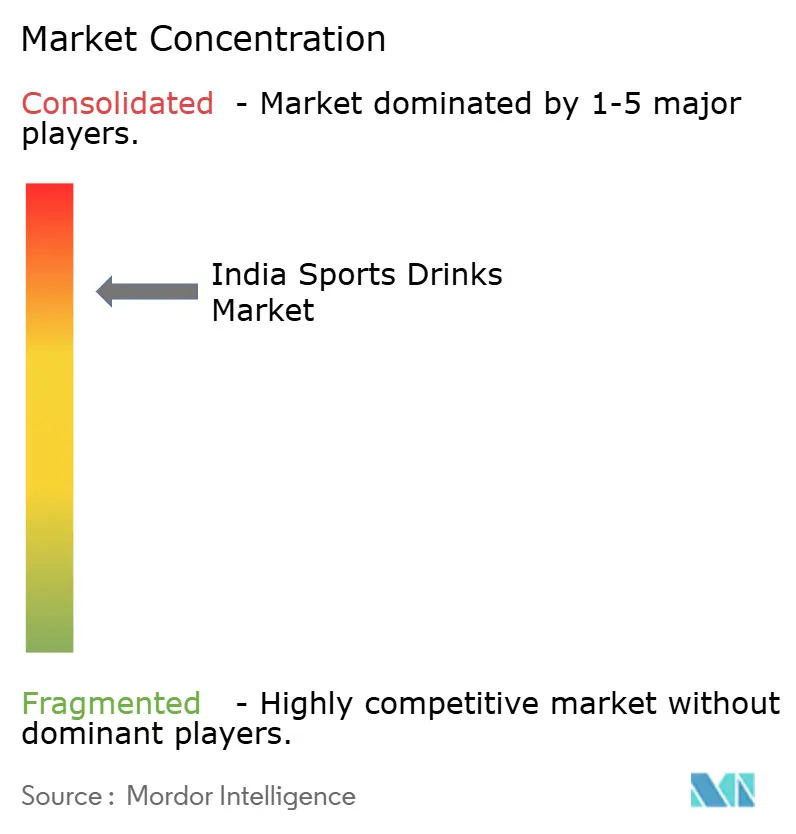

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Sports Drinks Market Analysis by Mordor Intelligence

The Indian sports drinks market size in 2026 is estimated at USD 80.95 million, growing from 2025 value of USD 76.18 million with 2031 projections showing USD 109.61 million, growing at 6.25% CAGR over 2026-2031. Growing gym memberships, expanding marathon calendars, and government funding under the Khelo India initiative are turning hydration into a mainstream daily habit, rather than an elite athletic requirement. Quick-commerce platforms that deliver chilled beverages in under 15 minutes, combined with rising demand for low-sugar formulations that dodge front-of-pack warnings, are reshaping category economics. Multinational incumbents safeguard shelf space through IPL sponsorships, while price-disruptive domestic brands court tier-2 shoppers with INR 10 single-serve packs. Cold-chain gaps continue to drive investment in aseptic packaging, and policy commitments, such as the July 2025 Khelo Bharat Niti, ensure a steady pipeline of young athletes who will normalize isotonic and hypotonic drinks from an early age.

Key Report Takeaways

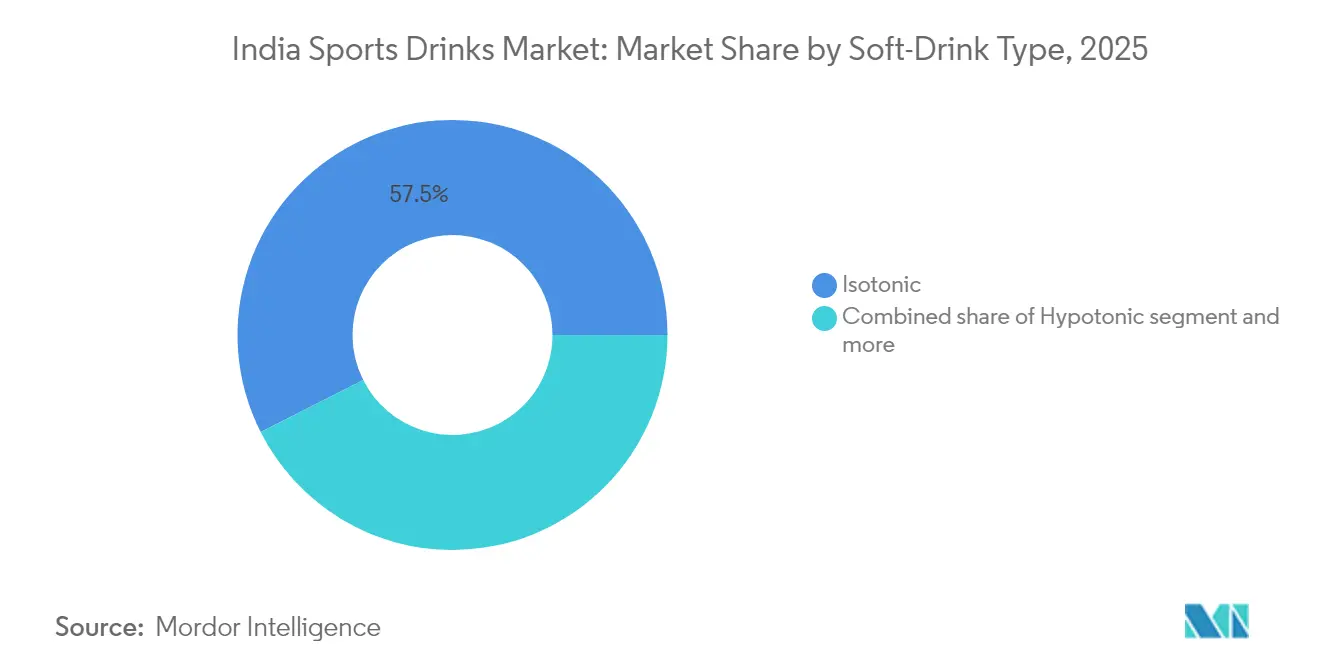

- By soft-drink type, isotonic variants led India's sports drinks market share, accounting for 57.45% in 2025. In contrast, hypotonic drinks are forecasted to grow at a 7.12% CAGR through 2031.

- By packaging, PET bottles accounted for 71.92% of the India sports drinks market size in 2025; aseptic cartons are expanding at a faster 7.6% CAGR to 2031.

- By functionality, intra-workout beverages commanded 36.72% share of the India sports drinks market in 2025, while pre-workout products are on track for the highest 8.07% CAGR to 2031.

- By distribution channel, off-trade outlets accounted for a 67.83% revenue share in 2025, growing at a 6.53% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Sports Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of organized sports leagues | +1.2% | Metros and tier-2 hubs | Medium term (2-4 years) |

| Growth of gyms and academies in smaller cities | +1.1% | Tier-2 and tier-3 locations | Medium term (2-4 years) |

| Consumer shift to low-sugar clean labels | +0.9% | Urban millennials and Gen-Z | Short term (≤ 2 years) |

| Social-media-led product discovery | +0.7% | National, strongest in 18-35 age band | Short term (≤ 2 years) |

| Endurance sports participation boom | +0.8% | Metros, with spillover to tier-2 | Medium term (2-4 years) |

| High-visibility sports sponsorships | +0.6% | National, IPL peak April-May | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Organized Sports Leagues and Grassroots Training Ecosystems

Khelo India’s 1,041 centers provide structured coaching to over 2,700 scholarship athletes, incorporating hydration guidelines into daily drills, as per the Ministry of Youth Affairs and Sports[1]Source: Ministry of Youth Affairs and Sports, “Khelo India Programme,” yas.nic.in. The July 2025 Khelo Bharat Niti scales this model nationally, targeting 2 million talent assessments that implicitly widen the addressable base for isotonic and hypotonic drinks[2]Source: Press Information Bureau, “Khelo Bharat Niti 2025 Launched,” pib.gov.in. Private brands ride the wave: Amul’s Stamina logo appeared courtside in 9 of 10 IPL teams during the 2025 season, tapping the league’s 400 million viewers. Each new center enrolls around 250 trainees, and even a 20% adoption rate yields thousands of new monthly sport-drink consumers, justifying deeper distribution beyond metros. Consequently, the India sports drinks market benefits from simultaneous public-sector infrastructure and private-sector activation.

Rising Penetration of Fitness Chains, Gyms, and Sports Academies Across Tier-2 and Tier-3 Cities

Cult.fit’s recent expansion into Mysore, Nashik, Indore, Bhubaneswar, Coimbatore, Visakhapatnam, and Surat indicates that Tier-2 consumers are increasingly adopting metro-like wellness habits. The company now operates more than 300 centers serving 2.5 million active users, and reported FY23 revenue of INR 476 crore (USD 57 million), a 34% year-on-year increase, according to its annual report. Gold’s Gym India operates 140 gyms across 75 cities and aims to expand to 200 locations by 2025, supported by a franchise model that requires an investment of INR 1–2 crore (USD 120,000-240,000) per site. These facilities serve as controlled sales environments, where members paying INR 3,000-5,000 per month (approximately USD 36–60) are regularly exposed to in-gym displays and trainer recommendations, which help drive product trial and repeat use. For brands, partnering directly with fitness chains offers a route to secure shelf space, introduce exclusive SKUs, and strengthen visibility without depending on traditional retail channels. This approach also reduces cold-chain challenges, as most gyms maintain chilled vending or storage infrastructure.

Shift Toward Low-Sugar, Clean-Label, and Natural Hydration Formulations

Indian consumers are increasingly preferring clean-label beverages and are willing to pay more for natural ingredients, a trend that is particularly strong among the country’s 101 million diabetic adults, for whom sugar content is a primary consideration in their purchasing decisions (International Diabetes Federation). Reflecting this shift, Coca-Cola launched Powerade Power Water in November 2025, a zero-sugar electrolyte drink targeted at health-focused millennials. Regulation is reinforcing these preferences. The FSSAI’s July 2024 mandate for bold front-of-pack disclosures on sugar, salt, and fat is accelerating reformulation, as products flagged with red or amber warnings risk lower acceptance[3]Source: Food Safety and Standards Authority of India, “Front-of-Pack Labelling Gazette,” fssai.gov.in. Consequently, brands are moving from sucralose and aspartame to natural sweeteners such as stevia and monk fruit. Brands with clear ingredient transparency are gaining traction. Amul’s Stamina line leverages whey protein as a natural differentiator, while coconut-water-based formulations are emerging as a niche opportunity. Coca-Cola’s planned 2025 launch of BodyArmor Lyte taps into this demand for naturally positioned hydration products in urban India.

Social Media Influence Boosting Market Growth

PepsiCo’s May 2025 partnership between Sting Energy and Battlegrounds Mobile India (BGMI) demonstrates how digital ecosystems are driving beverage trials among Gen Z. In-game QR codes on virtual bottles unlock rewards, merging entertainment with product discovery. Fitness influencers on Instagram and YouTube, often seen as authentic practitioners rather than paid endorsers, now outperform traditional celebrity advertising. A mid-tier fitness influencer (100,000-500,000 followers) can generate 5,000-10,000 direct clicks to e-commerce listings per post, according to the Social Media Marketing Association India, converting awareness into immediate sales. This environment benefits agile D2C brands like Fast&Up, which invests heavily in micro-influencer collaborations and athlete-led user-generated content showcasing hydration tablets in real training contexts. Social media effectively collapses the awareness-to-purchase funnel: consumers see an influencer's story, tap through to an e-commerce page, and complete the purchase within minutes. Brands that underinvest in digital storytelling risk losing relevance to competitors that dominate consumers’ social feeds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 40% GST plus cess on carbonated drinks | -0.9% | Nationwide, acute in tier-2/3 | Short term (≤ 2 years) |

| Anti-sugar sentiment and FSSAI labels | -0.6% | Urban metros with high diabetes rates | Medium term (2-4 years) |

| High price sensitivity outside metros | -0.7% | Tier-2 and tier-3 clusters | Medium term (2-4 years) |

| Weak refrigerated supply chains | -0.5% | Rural and semi-urban regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

40% GST Plus Cess on Carbonated and Functional Drinks

The September 2025 GST increase to 40% on carbonated and caffeinated functional beverages has directly reduced affordability in tier-2 and tier-3 markets, where annual disposable incomes average INR 1.5-2.5 lakh, roughly half that of metro consumers. A 200 ml sports drink that previously sold for INR 20 (pre-tax) now retails at around INR 28, crossing a key price threshold for budget-sensitive shoppers. Reliance’s Campa responded by introducing an INR 10 SKU, utilizing vertical integration and reduced trade margins to offset the tax impact, thereby pressuring incumbents to follow suit or risk losing market share. Brands are countering this trend by offering tighter portfolio segmentation: providing “value” SKUs with smaller packs and simplified formulations for price-conscious markets, and premium functional variants for metropolitan areas where price elasticity is lower. The new tax regime is also prompting a shift toward non-carbonated formats, as still electrolyte waters fall under an 18% GST slab, creating a clear incentive for reformulation[4]Source: Goods and Services Tax Council, “GST Rate Notifications,” gstcouncil.gov.in.

Rising Anti-Sugar Sentiment and Proposed FSSAI Front-of-Pack Labels

India’s 101 million diabetic adults actively filter beverages by sugar content, and the FSSAI’s July 2024 mandate for bold front-of-pack labeling makes sugar levels immediately visible at the point of purchase. Consumer sentiment data indicate that 58% of Indians are concerned about sugar intake, rising to 70% among urban millennials and Gen Z (International Diabetes Federation). Products triggering red or amber warnings reduce purchase intent by 30–40% (FSSAI Consumer Perception Study, 2024). Coca-Cola’s November 2025 launch of Powerade Power Water, a zero-sugar electrolyte drink, exemplifies proactive reformulation, avoiding front-of-pack warnings while maintaining functional benefits. The strategic takeaway is clear: brands must accelerate reformulation timelines, as delaying compliance risks ceding first-mover advantage. Natural sweeteners, such as stevia and monk fruit, enable zero-sugar formulations without compromising taste, although they carry a 15–20% cost premium that must be managed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Soft-Drink Type: Diversifying Formulations for Distinct Use Occasions

Isotonic drinks retained a 57.45% market share in 2025, cementing their status as the default choice for long-duration efforts. Hypotonic alternatives, however, are projected to outstrip the category at a 7.12% CAGR, mirroring the preference among recreational athletes in India for sports drinks that facilitate rapid fluid uptake. Hypertonic offerings remain niche for weight-training recovery but deliver glycogen replenishment in a single serve. Protein-enriched hybrids, led by Amul’s Stamina whey blend, fuse hydration and muscle repair, simplifying consumer post-workout routines. Electrolyte waters, such as Powerade Power Water, target sugar-averse users who want functionality without the caloric baggage. Regulatory trends favor lower-osmolality products that naturally comply with FSSAI sugar thresholds, intensifying R&D efforts around monk fruit and stevia sweeteners to maintain palatability.

Continued bifurcation forces brands to cover the entire osmolality spectrum. Competitive endurance athletes still demand carbohydrate-rich isotonic SKUs for races, whereas gym-goers finishing a 45-minute HIIT class opt for hypotonic drinks to avoid bloating. A growing micro-segment of desk-bound consumers uses electrolyte waters as healthier substitutes for carbonated colas, incrementally enlarging the India sports drinks market beyond traditional sport contexts. Smart portfolio management, anchoring on isotonic mainstays while incubating hypotonic and protein hybrids, will determine share gains over the next five years.

By Packaging: Ambient-Stable Cartons Challenge PET Dominance

PET bottles accounted for 71.92% of the value in 2025, thanks to their resealability and existing filling lines. Yet aseptic cartons are racing ahead at 7.6% CAGR, propelled by cold-chain gaps in semi-urban geographies and sustainability narratives that resonate with urban buyers. Amul’s investment in SIG technology delivers a 1-year shelf life without refrigeration, enabling sales through 1 million kirana stores that are currently unserved by chillers. Metal cans serve a premium impulse niche around energy-drink crossovers but add weight and cost for rural freight.

Plastic-waste rules require extended producer responsibility, making lightweight paper-based packs more attractive. Retailers appreciate the T-shape stacking flexibility of cartons on narrow kirana shelves. Meanwhile, quick-commerce dark stores located near apartment clusters retain PET bottles because speed trumps ambient convenience; they maintain refrigeration in-house and move product within hours. In essence, urban real-time delivery sustains PET relevance, yet the broader India sports drinks market growth in tier-2 hinges on ambient-stable innovations.

By Functionality: Pre-Workout SKUs Become the Fastest Climber

Intra-workout beverages still hold the lion’s share at 36.72%, reflecting their entrenched position on gym floors. However, pre-workout drinks are growing at an 8.07% CAGR as boutique HIIT studios and CrossFit boxes flourish in cities like Coimbatore and Visakhapatnam. Caffeine-electrolyte blends promise an immediate power boost, which resonates with Gen-Z consumers juggling work, study, and training schedules. PepsiCo leverages gamification through its partnership with Sting-BGMI to encourage gamers to transition into real-world workouts, converting virtual rewards into physical purchases.

Post-workout recovery drinks sit smaller in value but command high loyalty because muscle soreness is felt immediately. Protein-carb blends such as Amul’s Pro Drink deliver a one-stop solution, reducing cart complexity. All-day hydration SKUs, including coconut-water-enriched BodyArmorLyte, are set to launch in summer 2025, expanding total addressable consumption to non-exercise contexts such as commutes, office desks, and outdoor festivals. By blanketing all three functionality windows, before, during, and after exertion, brands can lock users into continuous usage, lifting annual per-capita volumes.

By Distribution Channel: Off-Trade Still Leads, Quick Commerce Redraws Maps

Off-trade venues accounted for 67.83% of 2025 revenues, with supermarkets and hypermarkets serving as anchor formats. Yet the true disruptor is quick commerce, growing at a significant CAGR, which flips traditional supply-chain economics. Instead of shipping pallets to distant stores, brands forward-deploy cases to micro-warehouses within 3 km of households. This favors smaller pack sizes and chilled PET, as products are typically moved within hours of arrival. Online marketplaces, such as Amazon and Flipkart, widen SKU depth and publish star ratings that influence tier-3 shoppers who lack access to big-box stores.

Cult.fit and Gold’s Gym act as living showrooms where trainers double as brand evangelists. Exclusive placement deals guarantee fridge prominence next to treadmills, cementing immediate consumption after intense sessions. Specialty nutrition stores stock higher-priced effervescent tablets and protein-hydration combinations, targeting users who are willing to pay a premium for ingredient transparency and imported flavors. Synchronizing on-trade sampling with off-trade replenishment ensures that a convenient second purchase can follow every first sip.

Geography Analysis

Southern India dominates the value, with Karnataka, Tamil Nadu, Telangana, and Andhra Pradesh collectively accounting for roughly half of the nation's electrolyte beverage sales. High ambient temperatures exceeding 35°C for much of the year accelerate perspiration, prompting more frequent rehydration. Zydus Wellness piloted the rollout of its Glucon-D Activators in Telangana and Andhra Pradesh at INR 45 per 200ml tetra pack, capitalizing on climate-driven demand. Bangalore, the region’s startup capital, hosts multiple marathons and is the headquarters for Cult.fit, amplifying consumption among a digitally savvy audience.

Western markets, led by Mumbai, Pune, and Ahmedabad, represent 25.00%-30.00% of the turnover. The Tata Mumbai Marathon’s 65,000 runners in January 2025 act as a massive sampling event, while Amul’s Gujarat base creates a stronghold for its Stamina line. Metropolitan disposable incomes permit both premium PET bottles and value cartons, allowing brands to run dual-tier SKUs without cannibalization. Northern territories, including Delhi-NCR and Haryana, account for 15.00%-20.00%. Colder winters shrink demand for four months each year, prompting companies to launch seasonal bundle promotions to smooth their revenue.

Eastern India is the white space. Lower per-capita incomes and weaker cold chains keep penetration modest, yet Bhubaneswar’s recent addition to Cult.fit’s map signals early green shoots. Reliance capitalizes on East India’s price sensitivity with its INR 10 PET shot, enticing retailers through 8% margins that beat incumbents’ 5%. Government cold-chain investments skew toward agricultural belts in Bihar and West Bengal, which will spill over to beverage logistics by 2028. Brands that position aseptic SKUs now will secure shelf equity ahead of infrastructure maturation.

Competitive Landscape

The India sports drinks market is moderately consolidated. Coca-Cola recorded INR 4,521 crore in revenue in FY23, a 45% increase, providing it with an ample advertising budget for multi-channel blitzes. PepsiCo mirrored this trajectory with double-digit volume expansion, buoyed by localized flavor labs in Gurgaon that refine their offerings to suit Indian palates. Domestic cooperative Amul leverages a supply-chain advantage through dairy integration and now produces 36,000 aseptic cartons per hour, enabling statewide coverage without the need for chillers.

Reliance’s Campa drives a textbook price-led assault, offering INR 10 shots that gift retailers 8% margins, double those from global brands. Zydus positions itself as the science-backed challenger, piloting Glucon-D Activators through medical representatives' networks to secure pharmacist recommendations. Fast&Up and MuscleBlaze thrive online, capturing share among supplement buyers already accustomed to D2C. Prime Hydration remains a premium niche, selling INR 399 bottles through select storefronts to create a sense of scarcity.

Strategic pivots center on omnichannel mastery and regulatory foresight. Multinationals hedge against sugar taxes with zero-calorie waters, while locals exploit GST asymmetries by formulating non-carbonated value SKUs. Sponsorship wars escalate: PepsiCo locks up gaming, Coca-Cola doubles down on cricket, and Amul retains dairy halo via grassroots wrestling leagues. Over the forecast horizon, sustained differentiation will stem less from ingredient novelty and more from agile logistics, dynamic pricing, and real-time consumer engagement.

India Sports Drinks Industry Leaders

Gujarat Cooperative Milk Marketing Federation Limited

PepsiCo, Inc.

The Coca-Cola Company

Red Bull GmbH

FDC Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PepsiCo India partnered with Battlegrounds Mobile India (BGMI) to integrate Sting Energy into the gaming platform, embedding in-game QR codes on virtual bottles that unlock rewards and drive trial among Gen-Z consumers.

- November 2024: Prime Hydration entered the Indian market through Globe Grocer Food Private, importing 1 million bottles initially and pricing 500-milliliter SKUs at INR 399 (approximately USD 4.73), more than double the U.S. retail prices.

- April 2024: Amul commissioned 2 SIG aseptic filling lines with a combined capacity of 36,000 cartons per hour, enabling shelf-stable distribution of its Stamina and Pro Drink brands via ambient logistics networks that reach 1 million retail outlets across India.

India Sports Drinks Market Report Scope

Electrolyte-Enhanced Water, Hypertonic, Hypotonic, Isotonic, Protein-based Sport Drinks are covered as segments by Soft Drink Type. Aseptic packages, Metal Can, PET Bottles are covered as segments by Packaging Type. Convenience Stores, Online Retail, Specialty Stores, Supermarket/Hypermarket, Others are covered as segments by Sub Distribution Channel.

By Soft-Drink Type

| Isotonic |

| Hypotonic |

| Hypertonic |

| Electrolyte-Enhanced Water |

| Protein-based Sports Drinks |

By Packaging

| PET Bottles |

| Metal Cans |

| Aseptic Packages |

| Others |

By Functionality

| Pre-Workout |

| Intra-Workout |

| Post-Workout |

| Others |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| By Soft-Drink Type | Isotonic | |

| Hypotonic | ||

| Hypertonic | ||

| Electrolyte-Enhanced Water | ||

| Protein-based Sports Drinks | ||

| By Packaging | PET Bottles | |

| Metal Cans | ||

| Aseptic Packages | ||

| Others | ||

| By Functionality | Pre-Workout | |

| Intra-Workout | ||

| Post-Workout | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms