India Pet Veterinary Diets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

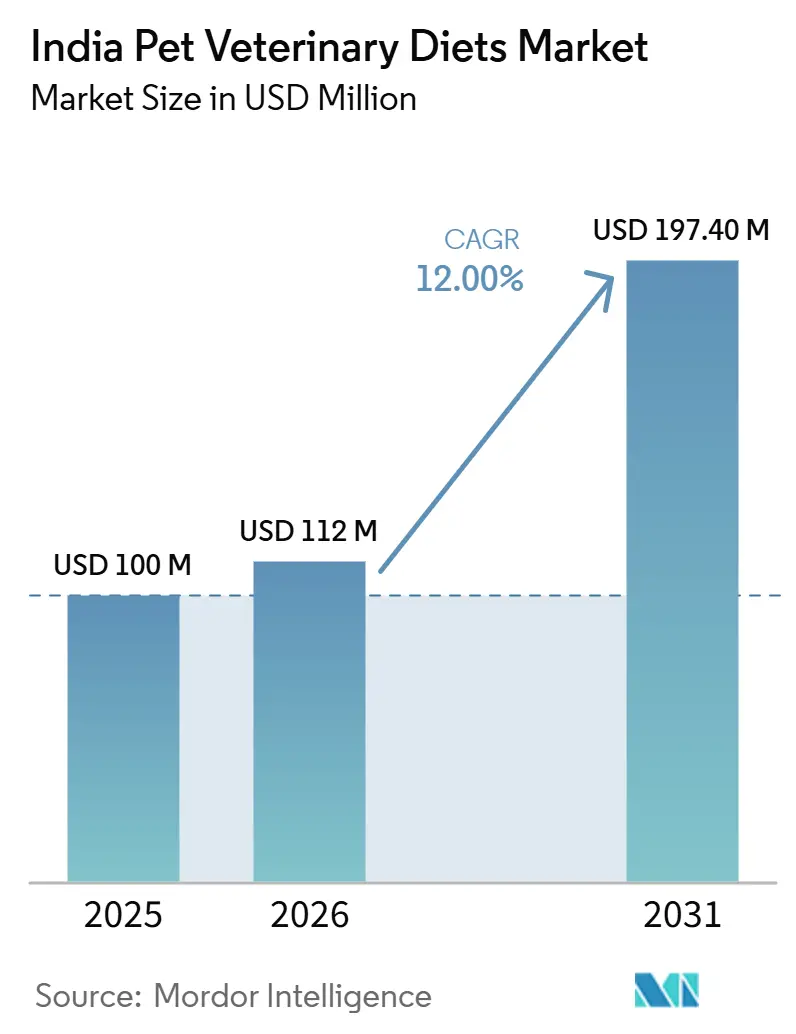

| Base Year Market Size (2025) | USD 100 Million |

| Market Size (2026) | USD 112 Million |

| Market Size (2031) | USD 197.40 Million |

| Growth Rate (2026 - 2031) | 12.00% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Pet Veterinary Diets Market Analysis by Mordor Intelligence

The India pet veterinary diets market size was valued at USD 100.00 million in 2025 and is estimated to grow from USD 112.00 million in 2026 to reach USD 197.40 million by 2031, at a CAGR of 12.0% during the forecast period. The India pet veterinary diets market is transitioning from a niche prescription segment to an integral component of pet healthcare. Urban households are increasingly addressing chronic pet conditions with greater seriousness, leading to higher acceptance of recurring expenditures on therapeutic nutrition. Improved access through online platforms, telehealth consultations, and an expanding veterinary presence in Tier-2 cities is reducing reliance on metro-based clinics for product recommendations and refills. Additionally, the low penetration of formulated pet food in India presents a significant opportunity for companies to convert pets from home-cooked meals to condition-specific diets by building veterinary trust and providing continuous education. Competitive dynamics are intensifying as multinational companies such as Nestle S.A. (Purina) and Mars Incorporated strengthen veterinary partnerships and domestic players focus on enhancing product accessibility, mass distribution, and affordability, thereby increasing competition within the market[1]Source: Nestlé Purina, “India’s Pet Care Market, Innovation, Growth, and the Long Road Ahead,” Unleashed by Purina, unleashedbypurina.com. The next phase of growth in the India pet veterinary diets market is anticipated to benefit companies that can integrate clinical credibility, digital refill convenience, and expanded reach beyond major metros while addressing the needs of price-sensitive households.

Key Report Takeaways

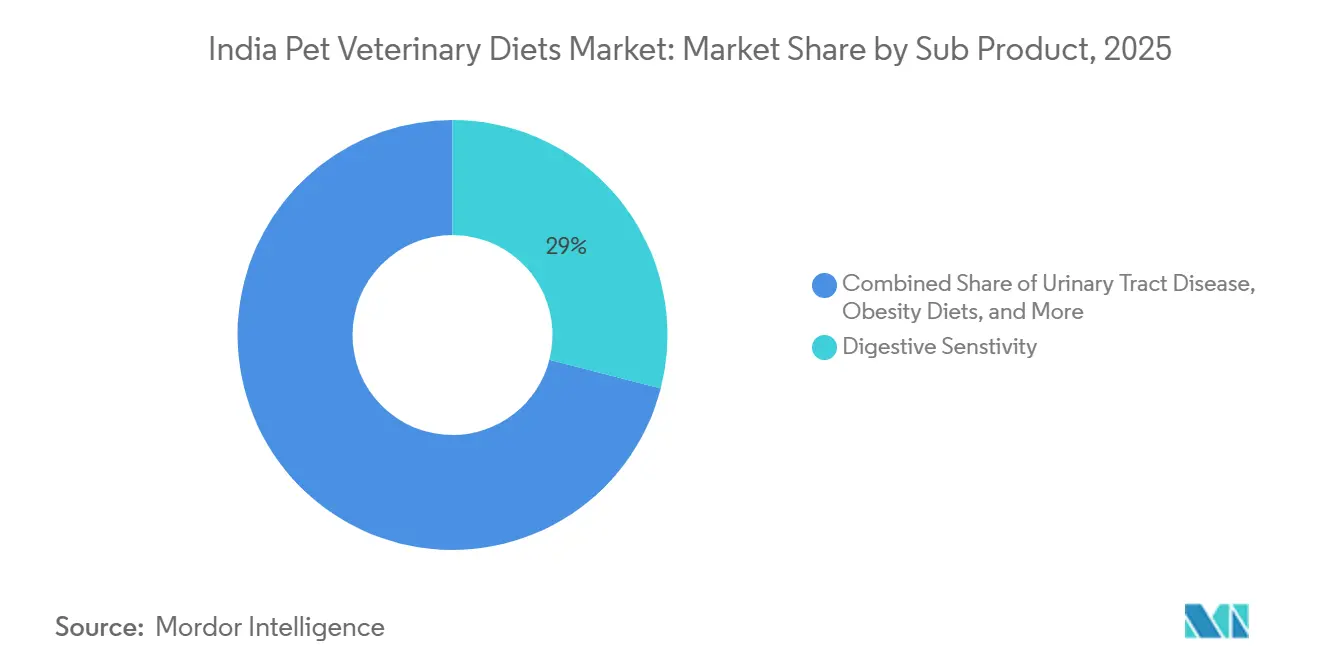

- By sub product, digestive sensitivity held 29.0% of the India pet veterinary diets market share in 2025, while oral care diets are forecast to expand at a 16.0% CAGR through 2031.

- By pets, dogs accounted for 65.0% share of the India pet veterinary diets market size in 2025, while cats recorded the highest projected CAGR at 14.0% through 2031.

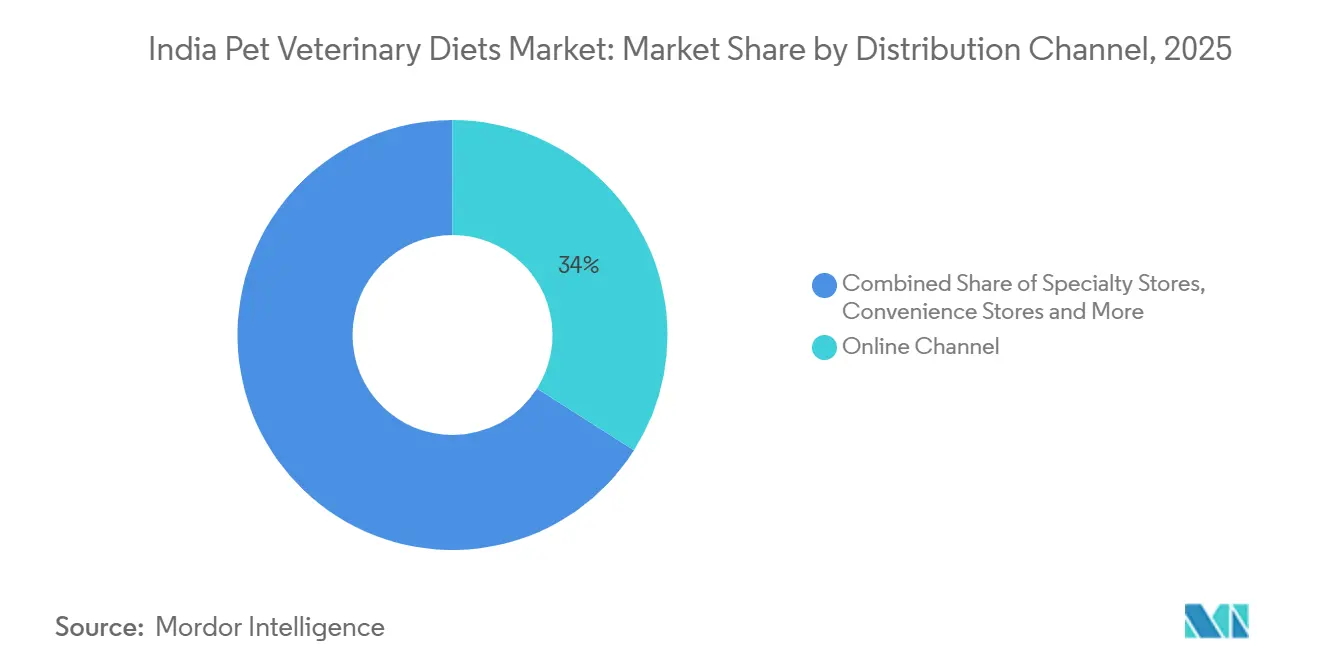

- By distribution channel, the online channel held 34.0% share of the India pet veterinary diets market in 2025 and is projected to grow fastest at a 15.0% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Pet Veterinary Diets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diagnosis Rates for Chronic Pet Conditions | +2.5% | India-wide, strongest in Mumbai, Delhi, Bengaluru, and Hyderabad | Medium term (2-4 years) |

| Veterinary Telehealth Improves Prescription Diet Access | +1.8% | India-wide, especially Tier-2 and Tier-3 cities | Short term (≤ 2 years) |

| Rapid Premiumization Among Urban Pet Parents | +2.2% | Metro cities and leading Tier-2 consumer hubs | Medium term (2-4 years) |

| E-Commerce Expands Reach Beyond Major Metros | +1.5% | India-wide, with stronger momentum in Tier-2 and Tier-3 cities | Short term (≤ 2 years) |

| AI-Assisted Nutritional Personalization Gains Early Traction | +0.8% | Metro cities first, then Tier-2 cities | Long term (≥ 4 years) |

| Tier-2 Clinic Expansion Broadens Therapeutic Diet Adoption | +1.2% | National, with early gains in Pune, Jaipur, Chandigarh, Kochi, and Coimbatore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Diagnosis Rates for Chronic Pet Conditions

The India pet veterinary diets market is experiencing growth driven by the increasing prevalence of chronic diseases in companion animals. Conditions such as renal disease, canine diabetes, urinary tract disorders, and digestive issues are being reported more frequently, particularly in urban areas where sedentary lifestyles and calorie-dense feeding habits are common. A prospective study published in the Indian Journal of Animal Research found that in 2025, nephritis and renal failure accounted for 35.88% of renal disorders in dogs in the South Saurashtra region of Gujarat. Similarly, clinical data from Guru Angad Dev Veterinary and Animal Sciences University indicated 6 to 7 cases of renal failure daily and over 200 dialysis sessions during the reported period. Once diagnosed, diet therapy for these conditions often extends for months or even years, creating a recurring demand for therapeutic diets. This recurring demand shifts therapeutic diets from occasional use to a routine component of medical care, particularly for the management of renal, diabetes, and urinary health. As diagnostic capabilities improve and veterinary case management becomes more structured, the India pet veterinary diets market is increasingly driven by clinical necessity rather than general premium food preferences.

Veterinary Telehealth Improves Prescription Diet Access

Telehealth is addressing a significant access barrier in the India pet veterinary diets market by reducing the time between symptom onset and clinical advice. Traditionally reliant on in-person consultations, the market's reach was limited in areas outside major cities, where specialist veterinary services were less accessible. According to IBEF (India Brand Equity Foundation), India’s pet telemedicine segment experienced a 40% growth in demand in previous years, supported by smartphone penetration surpassing 900 million users by late 2024[2]Source: India Brand Equity Foundation, “Decoding the Rise of the Pet Care Industry in India, A New Consumer Growth Story,” India Brand Equity Foundation, ibef.org. This increased connectivity facilitates faster digital interactions between pet owners and veterinarians. Remote consultations can seamlessly transition into diet recommendations and online orders, minimizing delays. This efficiency is particularly beneficial for conditions such as digestive sensitivity, obesity, renal issues, and urinary disorders, where timely intervention is crucial. Additionally, telehealth expands access for pet owners in Tier-2 and Tier-3 cities, who may have limited availability of therapeutic products through local clinics. As digital consultations gain wider acceptance in pet care, the India pet veterinary diets market is anticipated to reach a broader audience, including those previously outside the organized treatment network.

Rapid Premiumization Among Urban Pet Parents

Urban premiumization is increasing spending capacity for therapeutic nutrition, providing the India pet veterinary diets market with greater opportunities for growth. According to the IBEF, India’s urban pet care market surpassed INR 30,434 crore (USD 3.6 billion) in 2024, highlighting the expanding spending pool for higher-value pet products. This trend is particularly evident among younger urban pet owners, who increasingly view pets as family members and are more inclined toward preventive and corrective healthcare. This shift is significant, as veterinary diets are priced higher than standard packaged pet food and require a clear preference for health-focused feeding over cost-saving alternatives. Additionally, grain-free pet food sales on Swiggy Instamart grew by 152% year-on-year in 2025, and pet care orders from Tier-2 cities outpaced those from metro areas, indicating that premium demand is not confined to major urban centers. As spending on pet nutrition increases, prescription products become more affordable within household budgets when recommended by veterinarians. This trend supports a broader and more sustainable growth trajectory for the India pet veterinary diets market.

E-Commerce Expands Reach Beyond Major Metros

E-commerce has emerged as a significant distribution channel for the India pet veterinary diets market, enhancing both accessibility and refill continuity. In 2025, Online platforms saw higher pet food sales in India, indicating that digital purchasing behavior is well established in the pet care market. Therapeutic diets align well with this channel, as pet owners often seek detailed product information, consistent access, and verified brand storefronts before making clinical purchases. Additionally, online channels reduce reliance on local shelf availability, which is particularly important in cities with limited specialty pet retail options. For instance, Drools’ online-exclusive renal support subscription kit for senior dogs demonstrates how digital platforms can effectively bundle food, supplements, and treats, which physical retail often cannot match. Furthermore, quick commerce enhances convenience, reducing barriers to repeat purchases for chronic conditions. As online penetration increases, the India pet veterinary diets market is expanding its national reach without relying on uniform physical retail growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price Sensitivity Outside Major Cities | -2.5% | Semi-urban and rural India, with sharper pressure in Tier-3 cities | Long term (≥ 4 years) |

| Low Packaged Food Penetration Versus Home-Cooked Feeding | -2.0% | National, strongest outside metro areas | Long term (≥ 4 years) |

| Limited Prescription Compliance After Initial Diagnosis | -1.5% | India-wide | Medium term (2-4 years) |

| Gray-Market and Informal Online Sales Erode Brand Control | -0.8% | India-wide, concentrated in unregulated marketplace listings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity Outside Major Cities

Price sensitivity remains a significant restraint on the India pet veterinary diets market, particularly outside major urban areas. The pricing range for leading therapeutic products is INR 800 (USD 9.4) to INR 1,400 (USD 16.5) per kilogram, representing a substantial recurring expense for many households. In smaller cities and semi-urban markets, pet care often competes with other essential household priorities, making long-term therapeutic feeding challenging to sustain. The issue extends beyond the initial purchase to the ongoing need for consistent spending over several months or longer. While pet owners may adopt a therapeutic diet following a diagnosis, they often discontinue it once symptoms improve or when the recurring monthly cost becomes more apparent. The planned 2024 launch of Bowler’s Nutrimax by Allana aims to address this challenge by providing a more affordable premium option positioned between generic and veterinary-grade nutrition. However, unless improvements are made in price segmentation, pack sizes, and compliance support, this restraint will continue to hinder the expansion of the India pet veterinary diets market beyond affluent urban consumers.

Low Packaged Food Penetration Versus Home-Cooked Feeding

Low penetration of packaged food continues to limit the growth of the India pet veterinary diets market, as it reduces the number of households familiar with commercial pet nutrition. According to Mars Incorporated, 90% of Indian pet owners in 2025 still rely on home-cooked food as their pets' primary diet, highlighting the deeply ingrained nature of this practice. The dual challenge for veterinary diet brands is persuading pet owners to transition away from home-cooked meals and justifying the higher cost of therapeutic formulas. Many households perceive home-prepared food as fresher, more natural, and more trustworthy compared to packaged alternatives. This perception diminishes the urgency to adopt clinical diets, even when veterinarians recommend them. Consequently, education through veterinarians becomes more critical than mass marketing efforts, as trust remains the primary barrier. Until packaged feeding gains wider acceptance, the India pet veterinary diets market will continue to operate with a smaller active buyer base than the overall pet population might suggest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Digestive Health Leads as Oral Care Grows

Digestive Sensitivity accounted for 29% of the India pet veterinary diets market share in 2025, making it the largest sub-product category. This dominance is attributed to the high prevalence of gastrointestinal issues in pets, often caused by mixed feeding patterns that combine processed food with home-cooked meals. The segment also benefits from the visibility of symptoms, which prompt pet owners to seek veterinary care more quickly. Renal and Diabetes diets represent the next significant segment of therapeutic demand, driven by the increasing diagnosis of chronic diseases in urban pet populations. Additionally, Urinary Tract Disease, Obesity Diets, Derma Diets, and other Veterinary Diets contribute to the market's depth, enabling brands to address a broader range of clinical conditions.

The market is shifting towards more specialized sub-product offerings rather than broad, generic solutions. Hill’s expanded its Prescription Diet range in early 2024 with the introduction of the z/d Low Fat Hydrolyzed Soy Canine formula and the c/d Multicare Low Fat formulation, signaling a focus on multi-condition therapeutic solutions. Oral Care Diets have emerged as the fastest-growing segment, projected to grow at a 16% CAGR through 2031. This growth is supported by increased awareness of dental diseases and a lower price point compared to some renal and diabetes diets. In response to this demand, Virbac reformulated its HPM Small and Toy range in 2024, emphasizing clinically supported oral health benefits. Within the India pet veterinary diets market, competition among sub-products has shifted focus. The emphasis is now less on whether a condition can be addressed and more on which brand can ensure treatment accessibility through veterinary clinics and verified retail channels.

By Pets: Canine Dominance Persists as Feline Demand Rises

Dogs accounted for 65% of the India pet veterinary diets market size in 2025, maintaining their position as the largest pet segment. This dominance reflects the broader pet-ownership base in the country, where dogs significantly outnumber cats. Canine demand spans a wide range of clinical needs, including digestive sensitivity, renal disease, diabetes, urinary issues, and obesity. Large and medium breeds are particularly significant because they are more susceptible to metabolic and feeding-related conditions in urban environments. The availability of diverse SKU ranges across leading canine therapeutic brands supports dogs as the primary revenue driver for the India pet veterinary diets market.

Cats are the fastest-growing pet segment, projected to expand at a 14% CAGR through 2031, surpassing the overall market growth rate. This growth is driven by increasing feline adoption among younger, apartment-based households in cities such as Bengaluru, Mumbai, and Delhi. Royal Canin India’s launch of Fussy Cat demonstrates that manufacturers are adapting products to cater to selective feline appetite behaviors, rather than treating cats as a minor extension of dog nutrition. As cat ownership matures, conditions such as feline urinary disease and renal disease are anticipated to drive more structured therapeutic demand. Other pets, including rabbits and birds, represent a small share of the category due to the limited availability of therapeutic diet options for these animals. While the India pet veterinary diets market remains predominantly dog-led, the growing demand for feline-specific products is emerging as a significant secondary growth driver.

By Distribution Channel: Online Channel Commands the Distribution Network

The Online Channel held 34% share of the India pet veterinary diets market size in 2025 and is also projected to post the fastest expansion at a 15% CAGR through 2031. This lead is supported by the nature of therapeutic diet buying, which usually involves product comparison, repeat access, detailed information, and refill convenience. E-commerce also works well because many pet owners outside the largest cities do not yet have dependable access to a full range of veterinary nutrition in local stores. The draft links this trend to India’s broader e-commerce growth and to online platforms' ability to handle research-led and subscription-oriented purchases more effectively than convenience retail. Purina’s move to list Pro Plan Veterinary Diets on Amazon in 2024 shows the kind of channel strategy shaping broader access to therapeutic diets.

Specialty Stores remain the second major channel because they provide a stronger trust environment for first-time buyers who are still moving away from home-cooked food. Heads Up For Tails, reaching more than 100 stores across 20 Indian cities by October 2024, shows that organized premium pet retail is still scaling alongside digital growth rather than being displaced by it. These stores allow in-person guidance and curated assortment, which can matter when owners are choosing a therapeutic product for the first time. Supermarkets and Hypermarkets remain secondary because prescription-grade diets rely more on explanation and professional endorsement than on impulse visibility. Convenience Stores and Other Channels still cater mainly to mainstream pet food rather than to specialized clinical nutrition. For the India pet veterinary diets market, the most effective route remains a dual-channel model where online handles scale and refill continuity while specialty retail supports trust and onboarding.

Geography Analysis

Metro cities in India remained the primary value centers for the pet veterinary diets market in 2025 and are estimated to continue driving category demand in 2026. Cities such as Mumbai, Delhi, Bengaluru, Hyderabad, Chennai, and Kolkata benefit from a higher density of veterinary services, greater comfort with digital commerce, and better access to organized specialty pet retail compared to other regions. These cities also exhibit stronger awareness of chronic disease management and a higher willingness to invest in therapeutic nutrition when recommended by veterinarians. The concentration of formal pet care infrastructure in these areas provides certified brands with a competitive edge over informal sellers and supports better treatment continuity.

Tier-2 cities are becoming the next significant growth segment for the India pet veterinary diets market. Cities such as Pune, Kochi, Jaipur, Chandigarh, Coimbatore, and Lucknow are witnessing rising pet ownership, increased middle-class spending, and improved access to veterinary clinics and online retail platforms. The expansion of veterinary infrastructure in these cities, driven by both independent clinics and organized players, is enabling therapeutic diet recommendations for buyers who previously had limited access. Domestic companies are well-positioned to capitalize on these opportunities, as local distribution networks and price familiarity play a crucial role in these markets.

Southern India is emerging as a key regional focus within the India pet veterinary diets market. Godrej Pet Care launched Godrej Ninja in Tamil Nadu in April 2025, identifying the state as home to 2 to 3 million pet-parent households, underscoring the region's commercial potential. Southern India combines urban density, established veterinary institutions, and early adoption of premium pet food formats, making it a promising market. In contrast, Eastern and Central India remain underpenetrated relative to their population size, presenting long-term opportunities for expansion as distribution networks and veterinary access improve. Overall, while metro cities continue to drive value, Tier-2 and regional cities are becoming the primary volume growth engines, shaping the market trajectory through 2031.

Competitive Landscape

The India pet veterinary diets market is moderately concentrated, with the top five players being Mars, Incorporated, Nestlé S.A. (Purina), Colgate-Palmolive Company (Hills Pet Nutrition Inc.), General Mills (Blue Buffalo), and Virbac. Mars, Incorporated, benefits from the extensive reach and clinical positioning of Royal Canin, while Colgate-Palmolive supports Hills Pet Nutrition Inc. through clinical evidence and veterinary credibility. Nestlé S.A. (Purina) strengthens its position through veterinarian engagement and in-clinic sampling. Additionally, its May 2025 minority stake in Drools Pet Food Pvt Ltd. enhances its access to local manufacturing and distribution capabilities. This market structure indicates that scale remains an advantage in the India pet veterinary diets market, but opportunities still exist for emerging local competitors.

Recent strategic moves highlight that competition in this category extends beyond product awareness. For instance, Godrej Pet Care’s April 2025 launch of Godrej Ninja in Tamil Nadu, supported by an INR 500 crore (USD 58.8 million) investment over five years, marked the entry of a major Indian consumer products company into a segment traditionally dominated by specialist and multinational players. Meanwhile, Royal Canin previewed Veterinary Fresh Nutrition, and Hills Pet Nutrition Inc. introduced new therapeutic formulations in 2024[3]Source: Hills Pet Nutrition, “Hill’s to Unveil Prescription Diet Innovations,” Hills Pet Nutrition Press Release, hillspet.com. These developments demonstrate that established leaders are defending their premium positions through continuous innovation.

The primary growth opportunities in the India pet veterinary diets market lie in Tier-2 city expansion, digital subscription services, and improved post-diagnosis compliance. Specialist brands like Virbac and Farmina are leveraging focused veterinary channel strategies rather than broad consumer marketing to maintain relevance. Companies that integrate clinical trust, local availability, and refill continuity are likely to outperform those relying solely on premium brand recognition. While the market remains accessible for domestic brands to gain market share, the competitive landscape is becoming more challenging as treatment continuity and clinical relevance gain importance over mere visibility.

India Pet Veterinary Diets Industry Leaders

Mars Incorporated

Nestlé S.A. (Purina)

Colgate-Palmolive Company (Hills Pet Nutrition Inc.)

General Mills (Blue Buffalo)

Virbac

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nestlé S.A. (Purina) acquired a minority stake in Drools Pet Food Pvt. Ltd. for an undisclosed sum, valuing Drools Pet Food Pvt. Ltd. at over USD 1 billion and making it India's first pet food unicorn. The deal positions Nestlé S.A. (Purina) to benefit from Drools' 40,000-plus outlet distribution network while Drools retains operational independence, helping both companies reach pet veterinary diet purchasers.

- April 2025: Godrej Pet Care launched "Godrej Ninja" in Tamil Nadu. The scientifically formulated range targets gut health and immunity and was developed at the Nadir Godrej Center for animal research and development. The company has committed INR 500 crore (USD 58.8 million) to pet care investment over the next 5 years

- January 2024: Hill's Pet Nutrition Inc. announced new prescription diet innovations at VMX 2024, including the z/d Low Fat Hydrolyzed Soy Canine formula featuring ActivBiome+ technology and the c/d Multicare Low Fat Canine formula for dual fat-sensitivity and urinary management.

India Pet Veterinary Diets Market Report Scope

Pet veterinary diets (also known as therapeutic or prescription diets) are specialized, scientifically formulated pet foods designed to treat, prevent, or manage specific medical conditions.

The India Pet Veterinary Diets Market Report is segmented by sub product (Diabetes, Renal, Urinary Tract Disease, Digestive Sensitivity, Oral Care Diets, Derma Diets, Obesity Diets, and Others), by pets (Cats, Dogs, and Other Pets), by distribution channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and others). The market forecasts are provided in terms of value in USD and volume in metric tons.

| Diabetes |

| Digestive Sensitivity |

| Oral Care Diets |

| Renal |

| Urinary Tract Disease |

| Obesity Diets |

| Derma Diets |

| Other Veterinary Diets |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Diabetes |

| Digestive Sensitivity | |

| Oral Care Diets | |

| Renal | |

| Urinary Tract Disease | |

| Obesity Diets | |

| Derma Diets | |

| Other Veterinary Diets | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the estimated value of India pet veterinary diets by 2031?

The market is forecast to reach USD 197.4 million by 2031, up from USD 112 million in 2026 at a 12.0% CAGR.

Which sub product leads therapeutic pet nutrition demand in India?

Digestive Sensitivity led in 2025 with 29% share, reflecting the strong incidence of gastrointestinal issues and the need for structured feeding support.

Which pet type is growing fastest in veterinary diets?

Cats are projected to grow at a 14% CAGR through 2031, driven by rising urban feline adoption and stronger product targeting by global brands.

Why is online retail important for this category?

The Online Channel held 34% share in 2025 and is projected to grow at 15% CAGR because it supports product research, verified access, and repeat refill behavior.

What is the biggest barrier to wider adoption outside major cities?

Price sensitivity remains the largest barrier because leading therapeutic diets cost INR 800 (USD 9.4) to INR 1,400 (USD 16.5) per kilogram and require ongoing spending.

Page last updated on: