India Oleochemicals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.36 Billion |

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 1.71 Billion |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Oleochemicals Market Analysis by Mordor Intelligence

The India Oleochemicals Market size was valued at USD 1.36 billion in 2025 and is estimated to grow from USD 1.41 billion in 2026 to reach USD 1.71 billion by 2031, at a CAGR of 3.89% during the forecast period (2026-2031). The India oleochemicals market sits at the intersection of energy policy and specialty-chemical demand, where the E20 ethanol-blending mandate tightens the supply of fatty acid methyl esters for soap makers even as castor oil dominance secures a feedstock advantage unmatched elsewhere. A parallel premiumization wave in personal care increases mid-cut fatty alcohol use, while integrated vegetable-oil refiners lower logistics costs and improve traceability. The India oleochemicals market now balances scarce palm-based inputs against rising soybean and castor alternatives, rewarding vertically integrated players and disadvantaging commodity formulators exposed to palm price spikes. Strong foreign-direct-investment inflows into specialty chemicals further raise the floor of domestic capacity additions, supporting steady expansion of the India oleochemicals market through 2031.

Key Report Takeaways

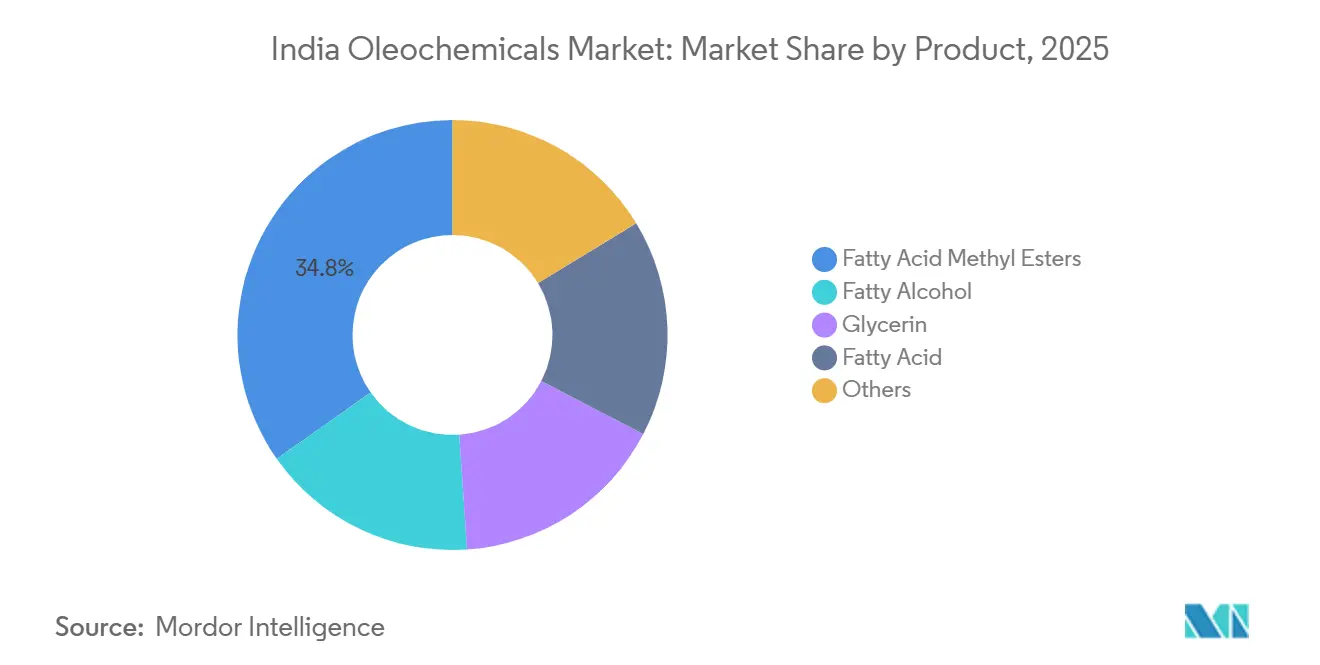

- By product, fatty acid methyl esters led with 34.76% of India oleochemicals market share in 2025, while fatty alcohols are forecast to grow at a 4.66% CAGR through 2031.

- By application, soap and detergents captured 38.92% share of India oleochemicals market size in 2025; pharmaceuticals and personal care are advancing at a 4.82% CAGR to 2031.

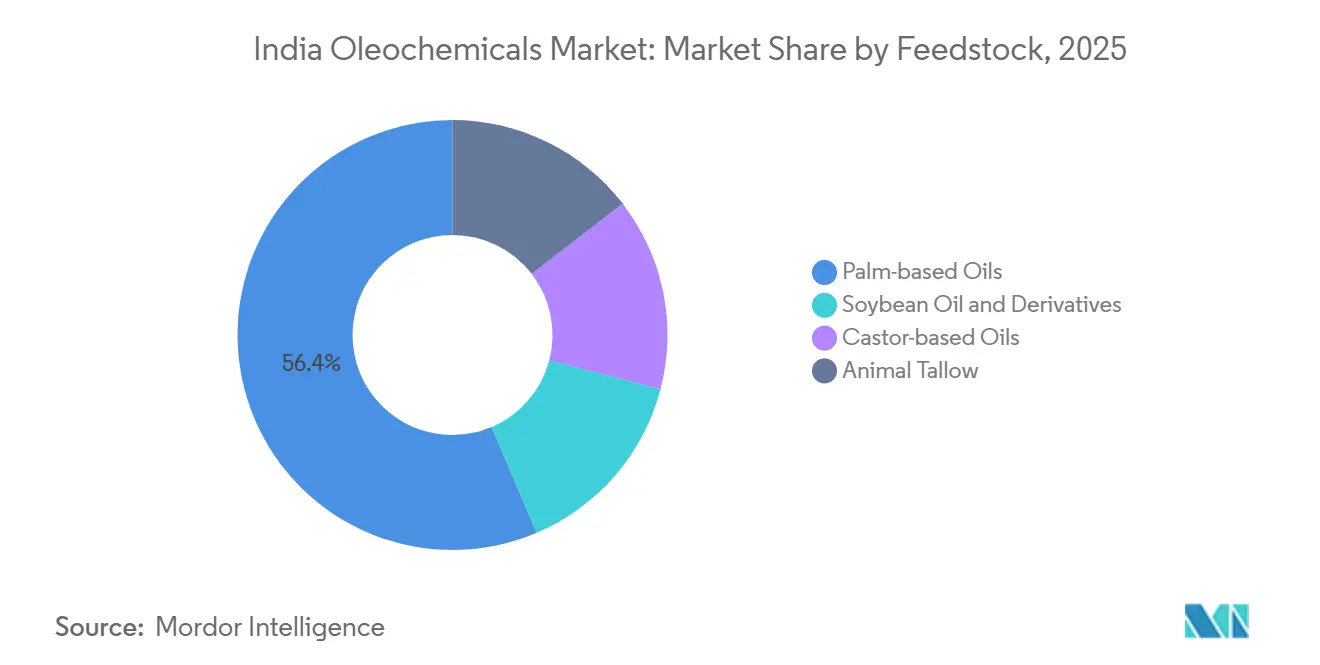

- By feedstock, palm-based oils controlled 56.41% of the India oleochemicals market share in 2025, yet castor-based oils are projected to expand at a 4.73% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Oleochemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Personal-care demand surge | +0.8% | National, urban metro clusters | Medium term (2-4 years) |

| Biodiesel and renewable-chemicals mandates | +1.2% | National, anchored by E20 rollout | Short term (≤ 2 years) |

| Expanding packaged-food processing | +0.6% | National, led by Gujarat, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| Integrated domestic vegetable-oil refining | +0.5% | Gujarat and Maharashtra refining hubs | Long term (≥ 4 years) |

| China-plus-one sourcing shift into India | +0.4% | Export-oriented SEZs in Gujarat and Maharashtra | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Personal-Care Demand Surge

The personal-care upswing channels new volumes into C12-C14 fatty alcohols as formulators replace sulfates to meet clean-label claims. The Bureau of Indian Standards updated IS 4707 in 2025, capping heavy metals and tightening pH ranges, which forces smaller brands to qualify RSPO-compliant inputs[1]Bureau of Indian Standards, “IS 4707:2025 Revision,” bis.gov.in. Croda India’s Dahej facility, opened in March 2026, supplies EXCiPACT-certified esters that sell at 15-20% premiums, signaling sustained appetite for high-grade inputs. Rising disposable income in tier-2 and tier-3 cities lifts per-capita consumption, while international brands leverage India’s cost base to export certified oleochemicals. The India oleochemicals market, therefore, expands not only in volume but in value as compliant grades displace commodity inputs, reinforcing a medium-term CAGR lift of 0.8% points.

Biodiesel and Renewable-Chemicals Mandates

April 2026 marks the operational start of E20 ethanol blending, which diverts fatty acid methyl esters away from surfactant pools into biodiesel. Universal Biofuels already runs an 80-million-gallon-per-year plant at Kakinada and has booked USD 103 million in 2024 deliveries to oil marketing companies, with higher volumes scheduled for 2025-2026[2]Aemetis, “Universal Biofuels Awarded Supply Contracts,” aemetis.com. Each 1% point rise in biodiesel use removes roughly 50,000-60,000 tons of methyl esters, prompting price spreads that encourage fatty alcohol substitution in detergents. The short-term squeeze adds 1.2% points to the India oleochemicals market CAGR, rewarding integrated refiners that can swing between methyl esters and fatty acids.

Expanding Packaged-Food Processing

India’s processed-food manufacturers broaden mono- and diglyceride uptake to extend shelf life, especially in bakery and frozen parathas, where travel-time spoilage remains high. Distilled monoglyceride, at greater than or equal to 90% purity, delays starch retrogradation by two to three days, a crucial gain for fragmented distribution channels. Domestic suppliers such as Spell Organics export E471-grade inputs to five continents, aided by India’s GRAS (Generally Recognized As Safe) acceptance in the U.S. and European Union (EU) approvals. As cold-chain infrastructure scales, downstream demand rises at least in line with the India oleochemicals market average, adding 0.6% points to forecast CAGR.

Integrated Domestic Vegetable-Oil Refining

Import-duty spreads of 20% on crude versus 32.5% on refined edible oils have spurred in-country crushing, giving refiners captive acid-oil streams convertible to fatty acids and tocopherols. Adani Wilmar’s INR 1,300 crore (approximately USD 156 million) Haryana complex integrates refining with oleochemical output, trimming logistics costs and enhancing traceability. Fairchem Organics converts acid-oil waste to dimer and isostearic acids, capturing triple-digit dollar premiums versus commodity fatty acids. The India oleochemicals market thus gains resilience from domestic feedstock loops, worth 0.5% points of long-term CAGR lift.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Palm-oil price volatility | -0.3% | Nationwide, palm-dependent formulators | Short term (≤ 2 years) |

| Cost-competitive petrochemical substitutes | -0.2% | Commodity soap and detergent clusters | Medium term (2-4 years) |

| Import dependence on high-purity esters | -0.2% | Pharma-grade and cosmetic supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Palm-Oil Price Volatility

Palm-based oils held 56.41% feedstock share in 2025, yet imports fell to a 7.1 million-ton, 15-year low as Malaysia and Indonesia diverted supply to domestic biodiesel. Soap and detergent makers reliant on palm derivatives saw EBITDA margins compress 200-300 basis points (bps) during 2025-2026 spikes. Substituting soybean oil provides some hedge, but Argentine export policies and South American weather add fresh volatility. The net drag slices 0.3% points from the India oleochemicals market CAGR.

Cost-Competitive Petrochemical Substitutes

When crude oil trades below USD 70/barrel, linear alkylbenzene sulfonates and synthetic fatty alcohols undercut bio-based inputs by more than 15%. Mass-market detergent brands, therefore, toggle between bio and petro routes, bottlenecking fatty-alcohol momentum. This flexibility trims 0.2% points from the CAGR of the India oleochemicals market, particularly in medium-sized timeframes when feedstock spreads widen.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Fatty Alcohols Outpace Methyl Esters on Sulfate-Free Shift

Fatty acid methyl esters commanded 34.76% share of India oleochemicals market size in 2025, yet fatty alcohol value will rise faster at a 4.66% CAGR during the forecast period (2026-2031) as detergent makers increase mid-cut loading by 10%. Godrej’s INR 750 crore (approximately USD 90 million) expansion doubles fatty alcohol output and quadruples specialty capacity, targeting sulfate-free shampoos priced at 15-20% premiums. VVF’s Taloja plant, Asia’s largest, strengthens India oleochemicals market share in exports across 90 countries.

Commodity glycerin faces oversupply as Chinese cargoes land at USD 620-680/ton, so Godrej pivots to USP-grade units where price spreads remain strong. Specialty fatty acids such as dimer and isostearic, processed by Fairchem from acid-oil waste, earn 50-100% premiums and insulate margins from palm volatility.

By Application: Pharma and Personal Care Accelerate on Compliance Tightening

Soap and detergents delivered 38.92% India oleochemicals market share in 2025, yet pharma and personal care grow at 4.82% CAGR through 2031, powered by IS 4707:2025 heavy-metal and pH limits that favor certified inputs. Croda’s Dahej unit, with zero-liquid-discharge, sells EXCiPACT-certified esters at a 15-20% markup, showing how higher standards unlock premium pricing. The food and beverages segment leverages E471 emulsifiers to extend bakery shelf life, supported by exports from Spell Organics to five continents. Polymers remain small but fast, as Balrampur Chini Mills’ future PLA plant dovetails with slip-agent growth at Fine Organic Industries.

By Feedstock: Castor Derivatives Gain as Palm Imports Tighten

Palm-based Oils dominated feedstock share at 56.41% in 2025, yet India's palm-oil imports fell to 7.1 million tons in marketing year 2025-26, a 15-year low, as Malaysian and Indonesian prices climbed and domestic biodiesel mandates diverted palm stocks, forcing processors to substitute soybean oil. Soybean Oil and Derivatives, the second-largest feedstock, benefit from India's rising domestic soybean imports sourced from West African producers (Togo, Niger, Benin) under zero-duty Least Developed Countries schemes.

Castor-based Oils will expand at 4.73% CAGR through 2031, the fastest among feedstocks, leveraging India's unique position as the source of over 90% of the global castor oil supply. Gujarat produced 13.65 lakh tons in 2025-26, representing 80% of India's total cultivation, with national production reaching 17.6 lakh tons (up 11% year-on-year). Animal Tallow, the smallest feedstock segment, faces cultural and regulatory constraints in India yet remains relevant for industrial fatty acids and soap production in export-oriented facilities.

Geography Analysis

India's oleochemical production concentrates in Gujarat and Maharashtra, where integrated vegetable-oil refineries, port infrastructure (Kandla, Nhava Sheva, Mumbai), and chemical-manufacturing clusters create feedstock-to-market proximity that reduces logistics costs by 8-12% versus inland locations. Gujarat's dominance in castor cultivation anchors a castor-derivatives ecosystem that supplies sebacic acid, ricinoleic acid, and hydrogenated castor oil to global buyers in China, the Netherlands, the USA, France, and Japan. Maharashtra hosts Godrej Industries' Valia facility (GreenCo Gold-rated), Fine Organic Industries' seven plants (Ambernath, Badlapur, Dombivli, Patalganga), and VVF's Taloja fatty alcohol complex, creating a specialty-chemicals corridor that serves domestic FMCG brands and exports to over 90 countries.

Andhra Pradesh emerged as a biodiesel hub, with Universal Biofuels operating an 80-million-gallon-per-year plant in Kakinada that secured USD 103 million in deliveries to oil marketing companies in 2024 and plans to exceed 200 million gallons per year through expansions into dairy biogas, ethanol, and sustainable aviation fuel. Tamil Nadu and Karnataka host smaller oleochemical producers serving regional soap, detergent, and food-processing clusters, yet lack the feedstock integration and port access that confer cost advantages to Gujarat and Maharashtra.

Competitive Landscape

The India oleochemicals market is moderately fragmented. Multinationals like KLK Oleo and AAK eye India for China-plus-one demand, raising competitive heat and pressuring commodity segment margins. Sustainable process technologies, biocatalysis, continuous flow, and renewable energy differentiate winners as buyers embed ESG audits in sourcing.

India Oleochemicals Industry Leaders

Godrej Industries Group

VVF ltd.

AWL Agri Business

3F Industries LTD.

Fairchem Organics Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Croda International Plc launched a manufacturing facility in Dahej, India, targeting Asian markets. Key features of the facility include Zero Liquid Discharge systems, RSPO-certified oleochemicals, and adherence to Extended Producer Responsibility plastic recycling standards.

- August 2025: BN Holdings Ltd. announced its debut in the specialty and oleochemical sector, unveiling plans for a manufacturing facility close to Kandla port in Gujarat, India.

India Oleochemicals Market Report Scope

Oleochemicals are chemical compounds derived from renewable plant oils (palm, soybean) or animal fats, serving as sustainable, biodegradable alternatives to petroleum-based chemicals.

The India oleochemicals market is segmented by product, application, and feedstock. By product, the market is segmented into fatty acid methyl esters, fatty alcohol, glycerin, fatty acid, and others. By application, the market is segmented into pharmaceuticals and personal care, soap and detergents, food and beverages, polymers, and others. By feedstock, the market is segmented into palm-based oils, soybean oil and derivatives, castor-based oils, and animal tallow. The market sizes and forecasts are provided in terms of value (USD).

| Fatty Acid Methyl Esters |

| Fatty Alcohol |

| Glycerin |

| Fatty Acid |

| Others |

| Pharmaceuticals and Personal Care |

| Soap and Detergents |

| Food and Beverages |

| Polymers |

| Others |

| Palm-based Oils |

| Soybean Oil and Derivatives |

| Castor-based Oils |

| Animal Tallow |

| By Product | Fatty Acid Methyl Esters |

| Fatty Alcohol | |

| Glycerin | |

| Fatty Acid | |

| Others | |

| By Application | Pharmaceuticals and Personal Care |

| Soap and Detergents | |

| Food and Beverages | |

| Polymers | |

| Others | |

| By Feedstock | Palm-based Oils |

| Soybean Oil and Derivatives | |

| Castor-based Oils | |

| Animal Tallow |

Key Questions Answered in the Report

What is the projected value of India’s oleochemicals sector by 2031?

India oleochemicals market is forecast to reach USD 1.71 billion by 2031, expanding at a 3.89% CAGR from 2026.

How will the E20 ethanol-blending mandate affect domestic oleochemical supply?

Beginning April 2026, it diverts fatty acid methyl esters to biodiesel, tightening supply for soap and detergent makers and raising input prices.

Which product category is expected to grow the fastest through 2031?

Fatty alcohols are set to rise at a 4.66% CAGR during the forecast period (2026-2031), helped by higher use in sulfate-free personal-care formulations.

Why are castor-based derivatives gaining momentum?

India controls over 90% of global castor oil output, giving local producers a stable, cost-advantaged feedstock that supports a 4.73% CAGR (2026-2031) for castor derivatives.

Page last updated on: