Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

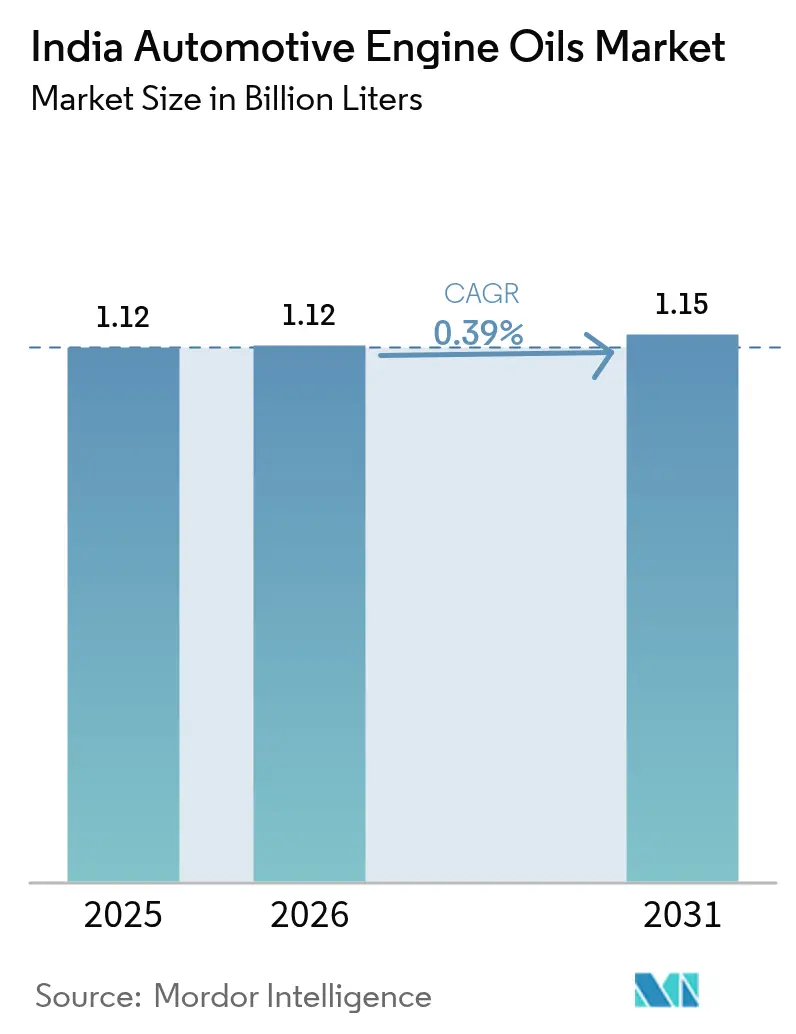

| Base Year Market Size (2025) | 1.12 Billion Liters |

| Market Volume (2026) | 1.12 Billion Liters |

| Market Volume (2031) | 1.15 Billion Liters |

| Growth Rate (2026 - 2031) | 0.39% CAGR |

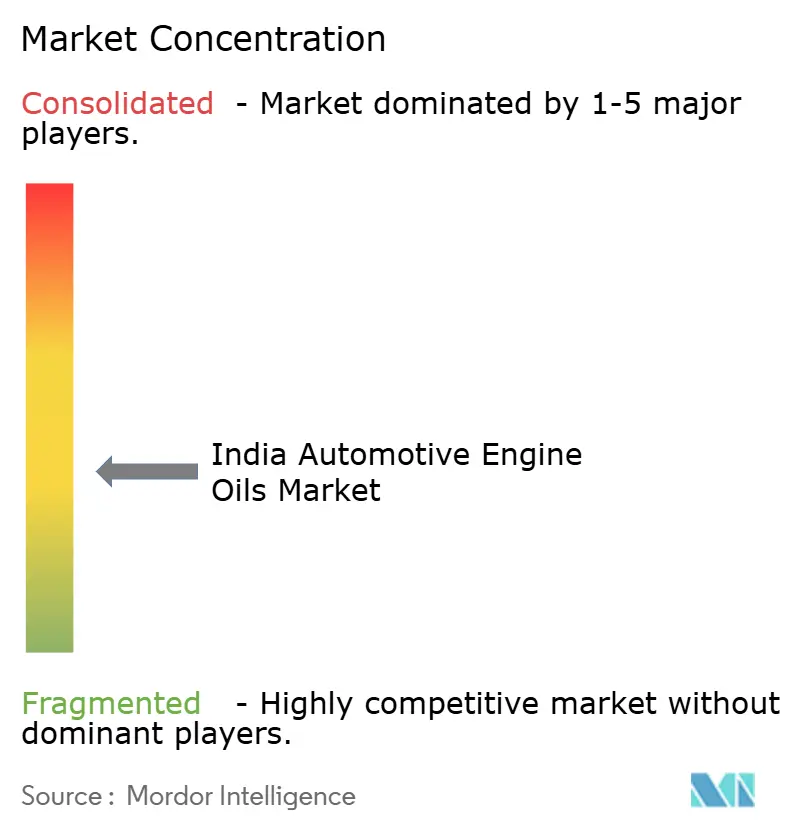

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automotive Engine Oils Market Analysis by Mordor Intelligence

The India Automotive Engine Oils Market size was valued at 1.12 Billion Liters in 2025 and estimated to grow from 1.12 Billion Liters in 2026 to reach 1.15 Billion Liters by 2031, at a CAGR of 0.39% during the forecast period (2026-2031). Demand is shifting toward low-viscosity synthetic blends as BS-VI Stage-2 regulations tighten, CNG fleets expand, and e-commerce delivery cycles accelerate maintenance needs. Manufacturers are balancing premiumization and price sensitivity by widening their synthetic portfolios while preserving mineral-oil offerings for older vehicles. Rising two-wheeler ownership sustains per-capita lubricant demand even as extended-drain formulations curb change frequency. Competitive intensity centers on distribution reach and OEM tie-ups, with refiners guarding volume positions and multinationals targeting high-margin niches. The India automotive engine oil market remains fundamentally volume-driven, so every liter saved through electrification or telematics directly pressures revenue.

Key Report Takeaways

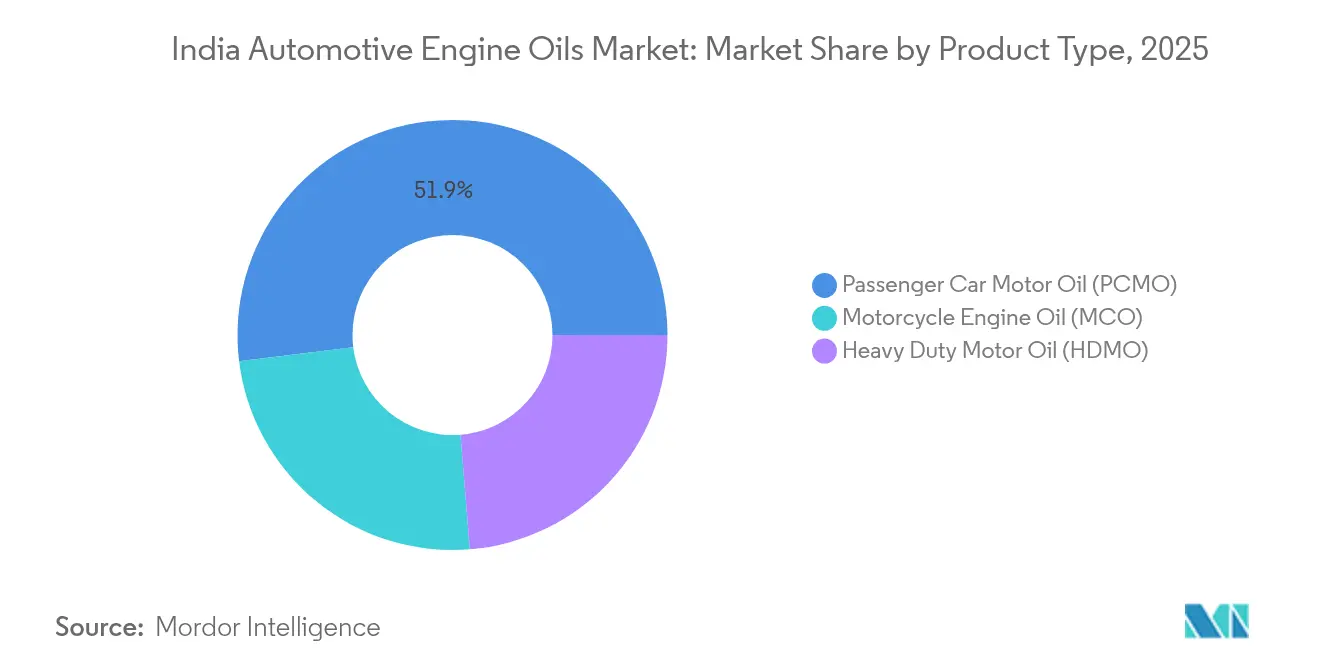

- By product type, passenger Car Motor Oil held 51.94% of the India automotive engine oil market share in 2025, while motorcycle engine oil posted the fastest growth at a 0.53% CAGR through 2031, outpacing all other product categories.

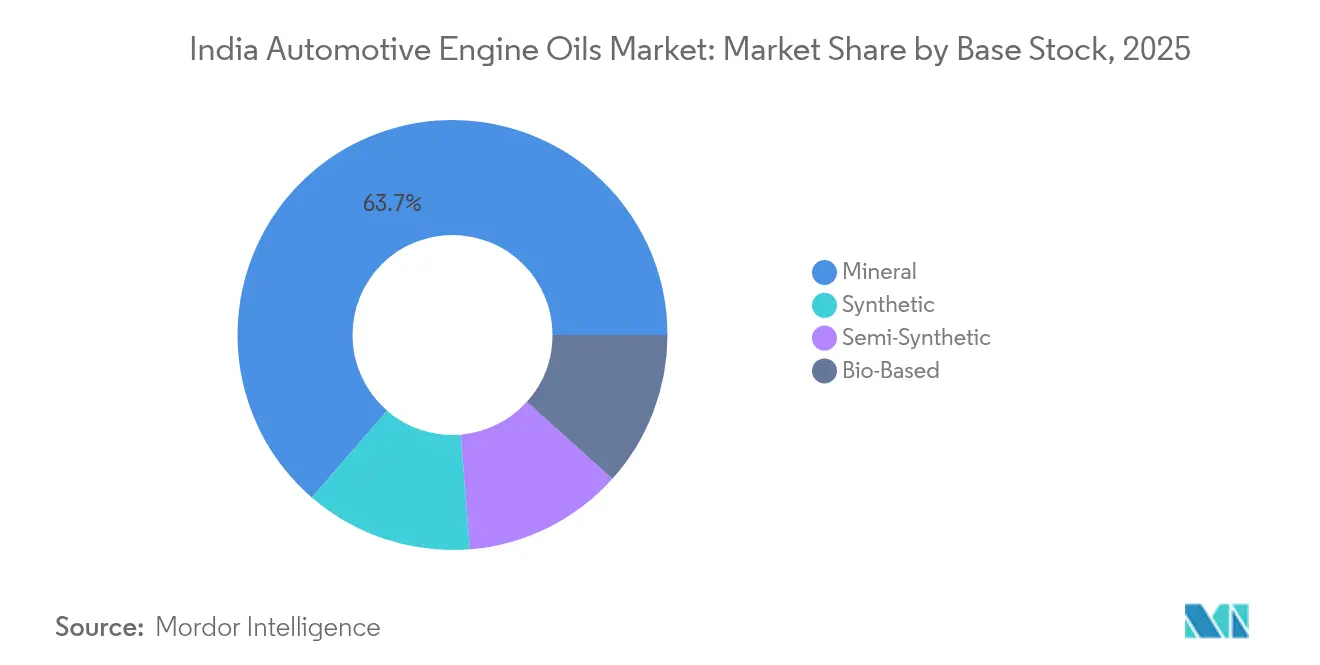

- By base stock, mineral base stocks captured 63.65% of the India automotive engine oil market size in 2025, yet synthetic oils recorded the highest 0.67% CAGR during the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising passenger-vehicle and two-wheeler parc expansion | +0.15% | Tier-2 and tier-3 cities nationwide | Medium term (2-4 years) |

| Rapid CNG-vehicle growth and higher-temperature lube demand | +0.08% | Delhi NCR, Punjab, Gujarat | Short term (≤ 2 years) |

| BS-VI Stage-2 norms driving shift to premium low-viscosity oils | +0.12% | Nationwide | Short term (≤ 2 years) |

| E-commerce last-mile fleets shortening drain-interval cycles | +0.05% | Metro and tier-1 cities | Medium term (2-4 years) |

| Scrappage-policy led spike in factory-fill demand (2026-28) | +0.10% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

BS-VI Stage-2 Norms Driving Shift to Premium Low-Viscosity Oils

The April 2023 onset of Real Driving Emissions testing forced OEMs to adopt low-SAPS oils that protect after-treatment systems under real-world conditions[1]TVS Motor Team, “BS6 Phase 2, RDE and OBD 2 Compliance Explained,” TVS Motor Company, tvsmotor.com . Synthetic and semi-synthetic grades now dominate factory-fill bids as mineral formulations struggle with tighter oxidation limits and deposit control. Fleet operators accept the 30–50% price premium because extended drains lower downtime and cut maintenance spend. Refiners have upgraded additive packages, positioning low-viscosity 5W-30 and 0W-20 grades for modern petrol and diesel platforms. Central Pollution Control Board audits reinforce compliance, making this regulatory push an irreversible driver of premiumization across the India automotive engine oil market.

Rapid CNG-Vehicle Growth and Higher-Temperature Lube Demand

India’s CNG fleet expansion in buses, taxis, and light-duty trucks raises lubricant operating temperatures, accelerating polymer shear and nitration. Premium CNG-specific oils priced 15–20% above diesel equivalents deliver the higher thermal stability and valve-seat protection these engines require. The north-centric refueling network sparks regional demand clusters where distributors prioritize CNG variants. Government targets that elevate CNG to 15% of all transport fuel by 2030 underpin steady volume growth, cushioning suppliers from BEV cannibalization in urban freight.

E-commerce Last-Mile Fleets Shortening Drain-Interval Cycles

Stop-start duty cycles in parcel and food delivery increase fuel dilution, soot loading, and oxidation, forcing oil changes 20–30% sooner than highway operations. Quick-lubrication chains and mobile service vans capture this higher-frequency maintenance business, pushing overall liter sales upward even when individual drains shrink in volume. While telematics-based condition monitoring is rolling out, most fleets still follow time-based schedules, creating a near-term volume tailwind within the India automotive engine oil market.

Scrappage-Policy Led Spike in Factory-Fill Demand (2026-28)

The national vehicle scrappage initiative retires aged commercial and private units, catalyzing new-vehicle production and factory-fill lubricant demand. OEMs negotiate multi-year supply contracts that secure volume and margin stability for lubricant partners. Peak replacement in 2026–2028 could lift annual factory-fill demand by up to 10%, helping offset long-term volume erosion from electrification and extended drains.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV and e-2W penetration eroding engine-oil volume | -0.18% | Metro cities and southern states | Long term (≥ 4 years) |

| Extended-drain synthetic oils cutting per-vehicle consumption | -0.12% | Highway corridors, national fleets | Medium term (2-4 years) |

| Telematics-based condition monitoring reducing oil changes | -0.08% | Organized logistics operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV and e-2W Penetration Eroding Engine-Oil Volume

FAME-II incentives and cheaper lithium-ion packs accelerate electric two-wheeler adoption, displacing motorcycles that currently anchor growth in the India automotive engine oil market[2]Professionals UK, “Electric Trends Shaping India Truck Market 2031 Outlook,” professionalsuk.co.uk. Each e-scooter eliminates 800–900 milliliters of annual oil demand, and adoption is clustering in Bengaluru, Chennai, and Pune before cascading into smaller cities. Heavy-duty electrification is slower, yet every BEV truck removes up to 40 liters per drain, magnifying the long-term drag on volume.

Extended-Drain Synthetic Oils Cutting Per-Vehicle Consumption

Carriers running 40,000–60,000-kilometer drains with API CK-4 synthetics halve yearly oil use, even after paying two to three times more per liter. Warranty-backed approvals from Tata Motors and Ashok Leyland validate this switch, and national express fleets are standardizing on premium grades to shrink maintenance windows. Extended drains thus present the most immediate volume-loss risk outside electrification, especially in long-haul corridors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Passenger Car Motor Oil Dominance Amid MCO Momentum

Passenger Car Motor Oil posted the largest 2025 share at 51.94% of the India automotive engine oil market share, thanks to an expanding passenger-vehicle parc and slower EV uptake in midsize cars. Multigrade 5W-30 and 5W-40 synthetics now anchor OEM factory fills, while 15W-40 mineral grades linger in older compact cars across non-metro regions. Motorcycle Engine Oil, benefiting from India’s 25-million-unit annual two-wheeler production, delivered the fastest 0.53% CAGR through 2031. OEM-driven viscosity shifts toward 10W-30 and 10W-40 synthetics improve cold-start protection and clutch performance, supporting premiumization. Heavy Duty Motor Oil maintains volume stability by servicing long-haul diesel and emerging CNG trucks. Despite synthetic penetration, older mineral 20W-40 monogrades remain relevant among price-sensitive owner-drivers.

OEMs and refill brands are refining additive chemistries to secure API SP and JASO MA2 credentials, positioning for tighter emission and fuel-economy norms. Product portfolios therefore straddle premium synthetics for modern vehicles and affordable mineral lines for legacy fleets, allowing suppliers to protect share across income segments.

By Base Stock: Mineral Leadership Challenged by Synthetic Innovation

Mineral oils retained 63.65% of 2025 volume due to cost advantages and compatibility with legacy engines, yet their hold is weakening as regulatory and economic factors push fleets toward synthetics. Synthetic grades, bolstered by BS-VI Stage-2 and extended-drain economics, recorded the highest 0.67% CAGR. Semi-synthetics carve out a mid-tier value proposition, blending hydro-cracked bases with premium additives to offer 25–30% longer drains at modest price uplifts.

Imports from Singapore and South Korea supplement domestic synthetic production, but rising Group III refinery projects in India aim to localize supply. Suppliers therefore invest in flexible blending lines that can swing between Group I, II, and III stock, ensuring cost competitiveness across customer tiers.

Geography Analysis

India’s northern corridor, encompassing Delhi NCR, Punjab, and Haryana, accounted for the highest regional lubricant demand in 2025 of the India automotive engine oil market, thanks to dense CNG adoption and a large commercial fleet base. The western region, led by Maharashtra and Gujarat, is underpinned by industrial clusters and strong passenger-vehicle penetration.

The India automotive engine oil market size for the northern region is sustained by construction and freight activity, offset by efficiency gains. Western and southern regions will show more pronounced shifts toward synthetic and extended-drain regimes. Eastern and northeastern states, though smaller in absolute volume, present above-average growth potential because rising vehicle density coincides with refinery infrastructure improvements that lower distribution costs. Urban centers anchor premium product sales. Rural districts remain mineral-oil strongholds, supporting supply chains of state-owned refiners that leverage fuel-station networks. Cross-border trade with Nepal and Bangladesh also channels surplus mineral stock from eastern India, extending the geographic influence of domestic blenders.

Competitive Landscape

India’s automotive engine oil arena remains moderately fragmented. Channel partnerships reshape distribution footprints. Gulf Oil’s 2024 tie-up with Nayara Energy unlocked 6,500 retail outlets, raising its rural penetration and reinforcing mid-tier brand credentials. Technology is the new battleground. ExxonMobil pilots IoT sensor kits that alert fleets to oil degradation, aligning lubricant supply with predictive maintenance contracts. Domestic challenger Veedol launched EstoBioLides-based synthetics in 2025 to carve out a sustainability niche. Start-ups offer direct-to-consumer packs via online marketplaces, but logistics costs and return-policy risks constrain their scale. Overall, pricing discipline remains intact in premium segments, while intense competition keeps mineral-oil margins thin, especially in the rural aftermarket.

India Automotive Engine Oils Industry Leaders

Bharat Petroleum Corporation Limited

BP plc

Gulf Oil International

Hindustan Petroleum Corporation Limited

Indian Oil Corporation Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Veedol Corporation introduced “SwiftPower” and “SynthGlide” fully synthetic oils featuring EstoBioLides Technology, starting with domestic sales and planning exports.

- August 2025: TotalEnergies launched an updated Quartz engine-oil line in India that meets API SQ and ILSAC GF-7 standards for improved fuel economy and timing-chain wear protection.

India Automotive Engine Oils Market Report Scope

By Resin Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Resin Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

How large is the India automotive engine oil market in 2026?

It stands at 1.12 billion liters in 2026 and is projected to reach 1.15 billion liters by 2031 at a 0.39% CAGR.

Which product segment uses the most engine oil in India today?

Passenger Car Motor Oil leads with 51.94% market share in 2025.

Why are synthetic oils gaining ground so quickly?

BS-VI Stage-2 regulations, extended-drain economics, and OEM warranties push fleets to adopt low-viscosity synthetic blends.

How will electric two-wheelers affect lubricant demand?

Each electric scooter removes up to 900 milliliters of annual engine-oil consumption, making e-2W adoption a key volume headwind.

What role does the scrappage policy play in the lubricant outlook?

Between 2026 and 2028, accelerated vehicle replacement is expected to lift factory-fill lubricant demand by up to 10%.

Which companies dominate premium synthetic sales?

Shell, ExxonMobil, and BP leverage advanced additive technology and OEM tie-ups to capture the high-margin synthetic segment.

Page last updated on: