Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

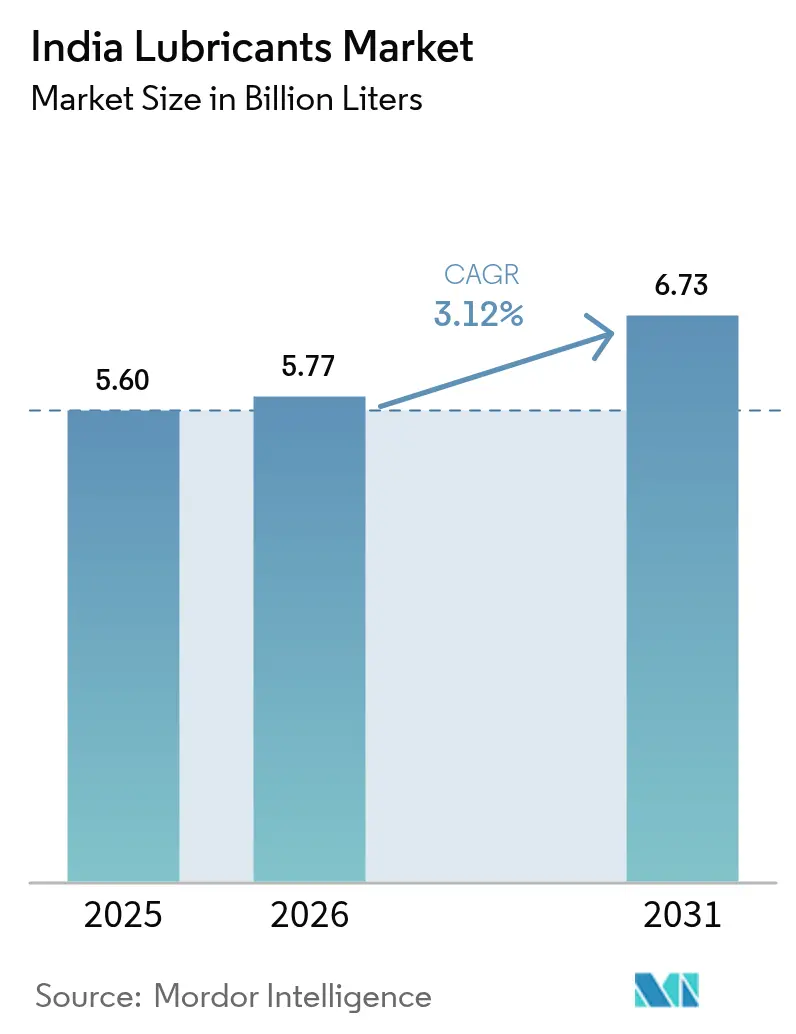

| Base Year Market Size (2025) | 5.60 Billion liters |

| Market Volume (2026) | 5.77 Billion liters |

| Market Volume (2031) | 6.73 Billion liters |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

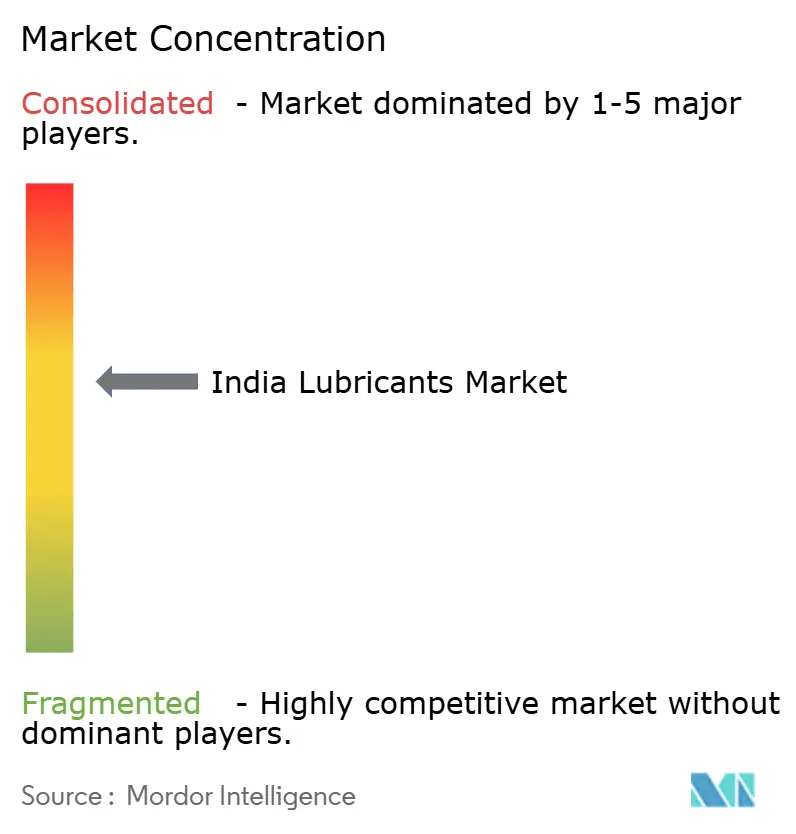

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Lubricants Market Analysis by Mordor Intelligence

The India Lubricants Market size is expected to grow from 5.60 billion liters in 2025 to 5.77 billion liters in 2026 and is forecast to reach 6.73 billion liters by 2031 at 3.12% CAGR over 2026-2031. A robust vehicle parc, expanding industrial output, and a decisive shift toward premium‐grade formulations underpin this growth. Synthetic product innovation, stricter BS-VI and CAFE regulations, and the roll-out of digital condition monitoring solutions encourage higher-value sales even as electric mobility gathers pace. Industrial automation is widening demand for precision fluids in machining, hydraulics, and gearboxes, while organized fleet operators adopt predictive maintenance, sustaining volumes despite longer drain intervals. Competitive intensity continues to rise as domestic refiners leverage retail reach and multinational brands position premium portfolios to capture the evolving end-user mix.

Key Report Takeaways

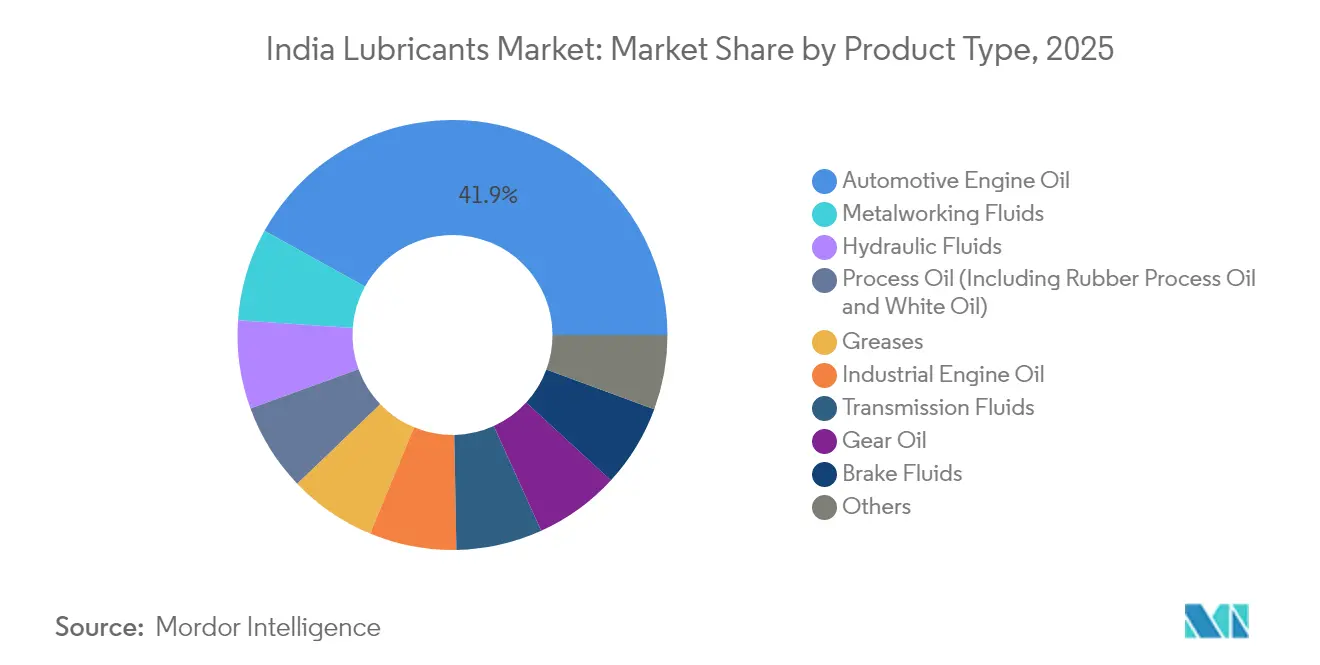

- By product type, automotive engine oil commanded 41.95% of the India lubricants market share in 2025, whereas metalworking fluids are projected to expand at a 5.29% CAGR through 2031.

- By end-user industry, automotive led with 54.15% revenue share in 2025 and is projected to post the fastest CAGR at 5.16% through 2031.

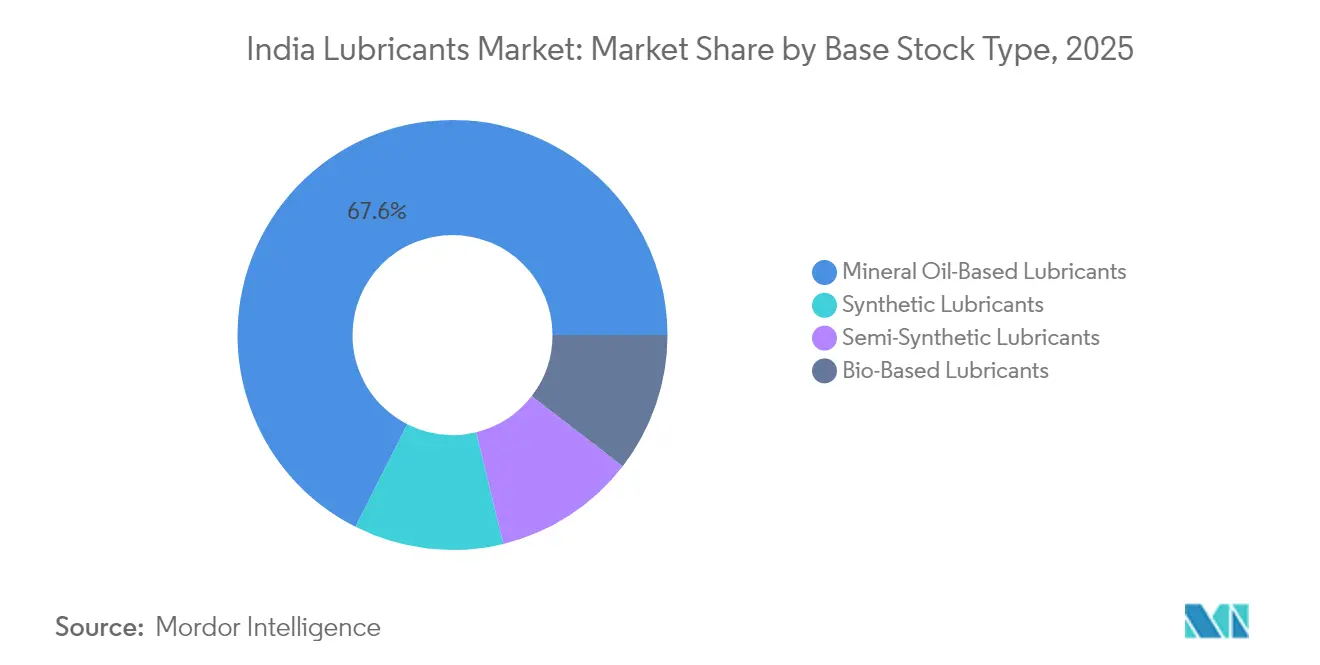

- By base stock type, mineral oil-based grades accounted for 67.55% share of the India lubricants market size in 2025, and synthetic alternatives are advancing at a 4.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Vehicle Parc and Miles-driven | +0.8% | National, concentrated in Maharashtra, Gujarat, Tamil Nadu | Medium term (2-4 years) |

| Industrial Output Growth Under "Make in India" | +0.6% | National, with manufacturing hubs in western and southern states | Long term (≥ 4 years) |

| BS-VI and CAFE Norms Pushing Premium Lubricants | +0.4% | National implementation, urban markets leading adoption | Short term (≤ 2 years) |

| Rapid CNG Fleet Expansion Needs Dedicated Engine Oils | +0.3% | Urban centers, commercial transport corridors | Medium term (2-4 years) |

| Digital Condition-monitoring Enabling Predictive Lube Changes | +0.2% | Industrial clusters, organized fleet operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Parc and Miles-driven

Passenger vehicle capacity additions in the western states are driving sustained demand for lubricants, even as electrification accelerates. Commercial fleets clock higher annual mileage due to e-commerce logistics and highway upgrades, which increases the frequency of lubricant replacement. Organized fleet operators rely on telematics to schedule oil changes that protect engines while minimizing downtime, reinforcing preference for premium synthetics. The automotive segment’s 54.72% share in 2024 illustrates this core demand anchor. Ageing two-wheeler and light-commercial fleets also bolster mineral oil volumes and maintain a broad customer base across rural markets.

Industrial Output Growth Under “Make in India”

Government manufacturing incentives continue to channel capital toward hubs for chemicals, metals, and heavy machinery in Gujarat, Maharashtra, and Tamil Nadu. Rising capacity utilization increases consumption of hydraulic fluids, gear oils, and compressor lubricants. The growth in precision machining at automotive and aerospace plants fuels a 5.51% CAGR in metalworking fluids, particularly neat cutting oils designed for broaching and carbide grinding. Investment in petrochemical complexes expands demand for turbine and compressor oils that operate under high temperatures. The preference for application-specific formulations supports the migration from commodity grades to performance-oriented synthetics, which extend drain intervals and limit unplanned shutdowns.

BS-VI and CAFE Norms Pushing Premium Lubricants

Nationwide enforcement of BS-VI tail-pipe standards and tighter fuel-efficiency targets require low-viscosity 0W-20 and 5W-30 oils with advanced additive packs. These regulations explain the 4.48% CAGR posted by synthetic lubricants despite the 68.12% dominance of mineral grades. Original equipment manufacturers recommend extended-drain synthetics to preserve catalytic converters and particulate filters, stimulating higher unit realizations for lubricant blenders. Formulators incorporate friction modifiers and anti-wear chemistry that maintain oil film stability at elevated engine temperatures common to Indian driving cycles. As compliant products command price premiums, suppliers with research and testing capability gain a competitive edge.

Rapid CNG Fleet Expansion Needs Dedicated Engine Oils

City bus fleets and intra-city delivery vehicles are switching to compressed natural gas, which burns hotter than gasoline and places greater stress on valves and piston rings. Bharat Petroleum’s MAK CNG Plus and other dedicated formulations offer enhanced thermal stability and oxidation resistance, which are essential for these engines[1]Bharat Petroleum Corporation Limited, “Partner with MAK,” bpcl.in. Fleet managers accept higher product prices because total operating cost declines when engines run cleaner and oil change intervals lengthen. This specialty demand diversifies revenue and partially cushions any future slide in traditional diesel volumes. Premiumization also fosters brand loyalty among fleet operators who value technical support and seamless performance guarantees.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Base-oil and Additive Prices | -0.5% | National, affecting all market segments | Short term (≤ 2 years) |

| Accelerating EV Adoption Curbing ICE Lubricant Demand | -0.4% | Urban centers, expanding to tier-2 cities | Medium term (2-4 years) |

| Import Dependency on Group III/IV Base Oils | -0.3% | National, particularly affecting premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Base oil and Additive Prices

Group I base oils constitute a major portion of many finished blends, so crude price swings quickly erode blender margins. India is ramping up its domestic base-oil capacity, yet premium Group III and IV stocks must still be imported, leaving formulators exposed to currency fluctuations and freight spikes[2]World Bank, “Commodity Markets Outlook April 2025,” worldbank.org. Additive packages, particularly dispersants and friction modifiers used in BS-VI compliant synthetics, also face supply chain disruptions during global events. Smaller regional blenders struggle to maintain inventory buffers and may cede market share to integrated refiners that manage feedstock volatility more effectively. Frequent price adjustments can nudge cost-sensitive users toward lower-grade products or extend drain intervals, shaving near-term volume growth for the India lubricants market.

Accelerating EV Adoption Curbing ICE Lubricant Demand

Government targets aim for 30% electric penetration in passenger cars by 2030, which could trim automotive engine oil volume. EV powertrains eliminate crankcase lubrication and often use sealed transmissions with reduced fluid demand. However, electric platforms introduce fresh needs for thermal-management fluids and specialty greases for motor bearings and battery packs. Lubricant suppliers are reallocating research budgets to these segments while expanding their industrial portfolios to balance the likely long-term decline in demand for internal combustion engine oils. During the transition, parallel growth in hybrid vehicles and a sizeable legacy fleet should keep the India lubricants market expanding, though at a moderated pace.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type – Engine Oils Anchor Volumes While Metalworking Fluids Outpace

Automotive engine oil held 41.95% of the India lubricants market share in 2025, reflecting the country’s large on-road fleet and dusty operating environment that accelerates oil degradation. Heavy traffic and high ambient temperatures shorten drain intervals, locking in repeat purchases for passenger cars, commercial trucks, and two-wheelers. Industrial engine oils support diesel generator sets, earth-moving equipment, and marine engines that power port operations, providing a stable base for high volumes. Transmission and gear oils accompany the rise in vehicle production, while greases secure bearings in heavy machinery, maintaining a balanced product mix.

Metalworking fluids are projected to grow at a 5.29% CAGR, the fastest among all categories, driven by an increase in precision machining for automotive and aerospace components. Neat cutting oils provide superior lubrication and heat dissipation in gear hobbing and broaching, while soluble oils protect tools during high-speed aluminium milling. Rubber and white process oils serve tire and food applications, with regulatory purity norms enabling premium pricing. Brake fluid requirements remain steady because even regenerative braking systems retain hydraulic circuits for emergency and parking functions. Collectively, these trends elevate specialty fluids as a strategic growth lever within the broader India lubricants market.

By End-user Industry – Automotive Dominates Though Industrial Diversification Accelerates

The automotive sector contributed 54.15% to the India lubricants market size in 2025, and it is also forecast to expand the fastest at a 5.16% CAGR through 2031. Passenger vehicle ownership is climbing in urban centers, prompting a move toward mid-tier synthetics that offer longer service life. Commercial fleets, particularly in logistics, require diesel engine oils and driveline fluids that can withstand intense duty cycles. The two-wheeler parc remains the world’s largest, where budget mineral oils still prevail, but a gradual shift toward higher specifications is visible in organized service channels.

Heavy equipment in construction, mining, and agriculture is another pivotal user, consuming hydraulic fluids that resist water contamination and extreme loads. Public infrastructure programs spur demand for excavator and crane lubricants, sustaining baseline volumes. Marine lubricants cater to India’s extensive coastline, with formulations that meet IMO mandates for low-sulfur fuel compliance. Aerospace, though a niche market, requires ultra-clean greases and turbine oils certified by the Defence Research and Development Organisation, marking an avenue for technology-led differentiation.

By Base Stock Type – Mineral Oils Retain Scale, Synthetics Capture Value

Mineral base oils still command a 67.55% share of the India lubricants market size in 2025, due to their cost advantages and wide refinery integration. Group I materials work well in legacy diesel engines and agricultural pumps, where affordability often takes precedence over performance. Semi-synthetic blends offer modest upgrades with limited polyalphaolefin content, gaining acceptance in mid-range passenger cars and taxis that seek a balance between price and protection.

Synthetics record the highest 4.41% CAGR, propelled by BS-VI emission norms and OEM factory-fill mandates. Group III and Group IV formulations provide stable viscosity across a broad temperature range, enhancing fuel economy and prolonging engine life. Bio-based stocks are embryonic but benefit from the Bureau of Indian Standards Ecomark Rule 2024, which rewards biodegradability credentials in environmentally sensitive uses. As end-users weigh total cost against uptime, synthetics are poised to expand their share of the India lubricants market.

Geography Analysis

Western India, led by Maharashtra and Gujarat, hosts clustered automotive assembly plants from Tata Motors, Maruti Suzuki, and Hyundai, making the region the single largest consumption center for engine and process oils. Port infrastructure, steel mills, and petrochemical complexes add further pull for turbine and compressor lubricants, cementing supplier focus on this corridor. Service stations here stock higher-spec 0W-20 and 5W-30 grades, mandated by factory warranties, which accelerates premium product penetration.

Tamil Nadu is emerging as a southern stronghold with integrated supply chains spanning component forging, vehicle assembly, and shipbuilding. Demand rises across engine oils, hydraulic fluids, and metalworking coolants as plants ramp up exports. Organized channel reach supports product mix diversification, including synthetics for passenger cars and factory fill for new energy vehicles.

Northern states, such as Haryana and Uttar Pradesh, contribute sizable volumes through agricultural equipment and an expanding light commercial vehicle fleet. Although brand visibility remains fragmented outside large cities, rural initiatives like BPCL’s taluka-level dealerships are widening access to genuine products. Eastern and northeastern states currently lag in consumption; however, infrastructure expansion under the Petroleum, Chemicals, and Petrochemicals Investment Regions policy is expected to boost lubricant uptake in the long term.

Competitive Landscape

State-owned refiners utilize their extensive fuel retail networks to distribute branded lubricants at over 70,000 filling stations nationwide. Downstream integration shields them from base-oil price volatility and supports aggressive pricing in mineral grades. Multinationals counter with premium synthetics, global OEM alliances, and digital service platforms that promise fleet uptime and reduced total cost of ownership. Regulation also reshapes competition. The 2024 Ecomark environmental label raises formulation barriers, favoring incumbents with research and development assets that can certify low toxicity and high biodegradability. Smaller blenders without additive science or rigorous quality labs may retreat to unorganized markets or consolidate. Overall, rivalry is set to intensify as firms jostle for share within the growing but evolving India lubricants market.

India Lubricants Industry Leaders

Indian Oil Corporation Limited

BP p.l.c.

Bharat Petroleum Corporation Limited

Hindustan Petroleum Corporation Limited

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Shell India rolled out its revamped premium motor oil, Shell Helix Ultra, tailored to align with the cutting-edge 2025 API SQ Standard. The company also introduced a striking new packaging design for its Shell Helix lubricant lineup, emphasizing a contemporary aesthetic.

- June 2025: Mahindra awarded the Aftermarket Service Fill contract to PETRONAS Lubricants (PLIPL), a PETRONAS Lubricants International (PLI) subsidiary. This move bolsters PLIPL's presence in India's automotive lubricant sector. As part of the agreement, PLIPL becomes the exclusive distributor of the Maximile brand's vehicle fluids, including engine oils, transmission oils, axle oils, and steering fluids.

India Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

What is the size of the India lubricants market in 2026?

The market is expected to stand at 5.77 billion liters in 2026 and is projected to reach 6.73 billion liters by 2031.

Which segment holds the largest share of the India lubricants market today?

Automotive engine oil remains the leading segment, accounting for a 41.95% share in 2025.

What is the forecast CAGR for automotive lubricant demand?

Automotive applications are expected to grow at a 5.16% CAGR through 2031.

Why are synthetic lubricants gaining traction?

BS-VI and CAFE regulations, longer drain intervals, and OEM recommendations are boosting demand for synthetics, which are projected to post a 4.41% CAGR.

Which region consumes the most lubricants in India?

Western India, particularly Maharashtra and Gujarat, leads in consumption due to its dense automotive and industrial clusters.

How will electric vehicles affect lubricant demand?

EVs will cut engine oil volumes over time, yet they create new needs for thermal management fluids and specialty greases that offset part of the decline.

Page last updated on: