Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

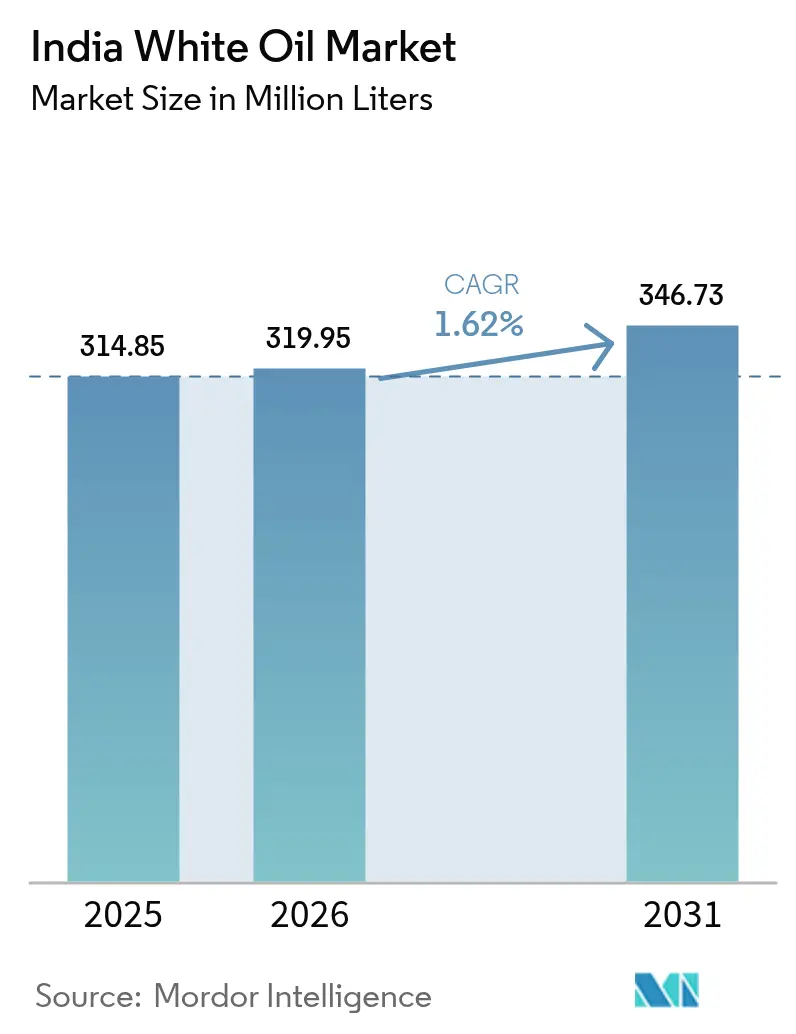

| Base Year Market Size (2025) | 314.85 Million liters |

| Market Volume (2026) | 319.95 Million liters |

| Market Volume (2031) | 346.73 Million liters |

| Growth Rate (2026 - 2031) | 1.62% CAGR |

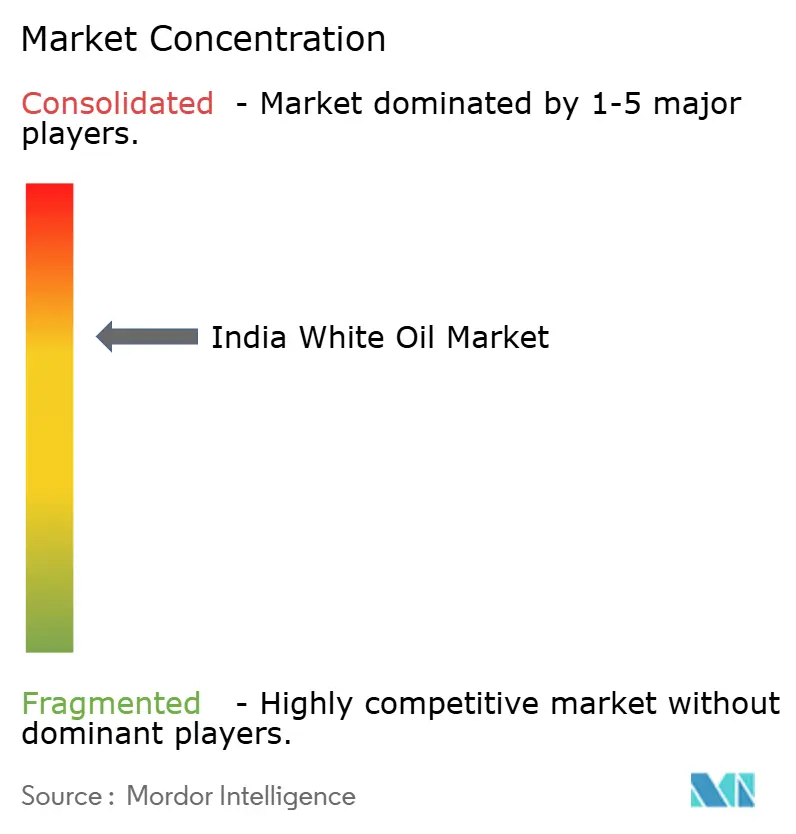

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India White Oil Market Analysis by Mordor Intelligence

India White Oil Market size in 2026 is estimated at 319.95 million liters, growing from 2025 value of 314.85 million liters with 2031 projections showing 346.73 million liters, growing at 1.62% CAGR over 2026-2031. This measured expansion reflects a shift from sheer volume growth toward higher-purity, value-added requirements that align with India’s maturing industrial base. Utilization across the country’s refining system consistently exceeds 103%, enabling producers to satisfy specialized downstream needs without relying on imports. Demand concentrates in personal-care, pharmaceutical, and polymer-processing clusters that benefit from integrated feedstock access and port infrastructure. Infrastructure upgrades—such as Indian Oil Corporation’s USD 2.1 billion capacity increase at Gujarat—strengthen domestic supply while positioning refiners to tap rising global demand for specialty oils[1]International Energy Agency, “Indian Oil Market 2024,” iea.org . Headwinds stem from base-oil price swings and growing availability of synthetic substitutes, yet established suppliers mitigate risk through vertical integration, regulatory compliance, and diverse viscosity portfolios.

Key Report Takeaways

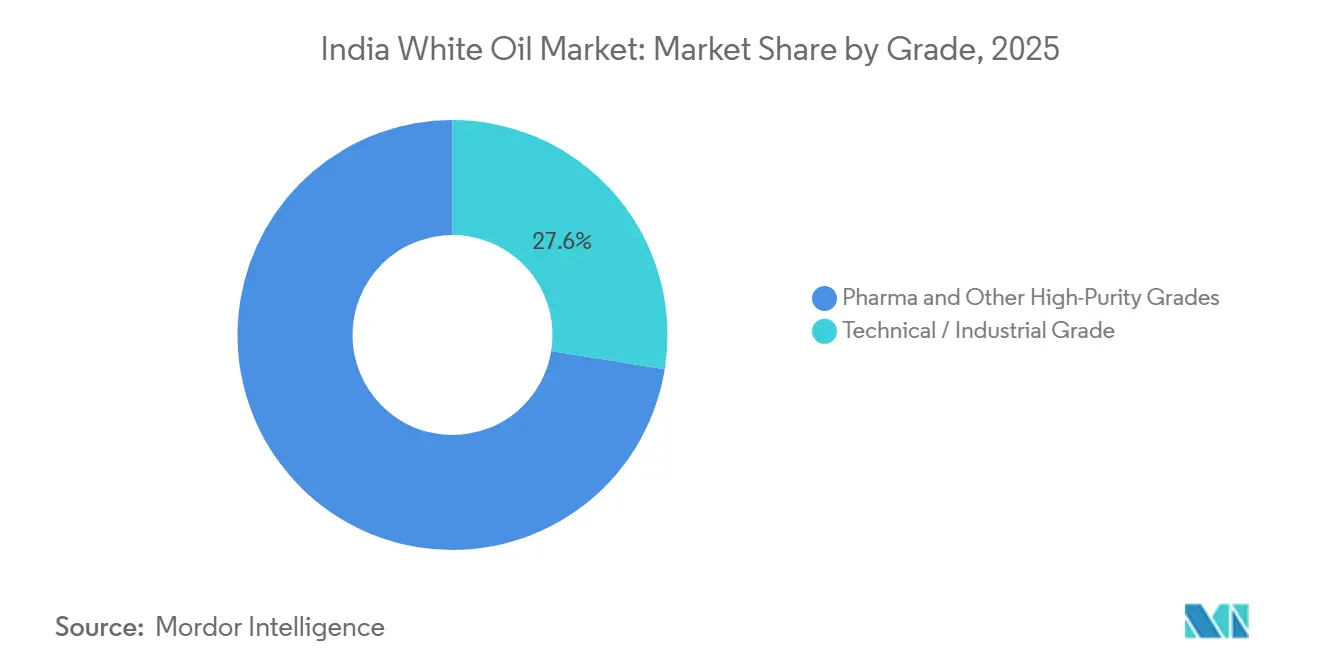

- By grade, pharma and other high-purity variants accounted for 72.45% of the India white oil market share in 2025, while the same group is forecast to grow at a 1.69% CAGR to 2031.

- By viscosity, low-viscosity products commanded 67.60% of the India white oil market size in 2025 and are advancing at a 1.63% CAGR through 2031.

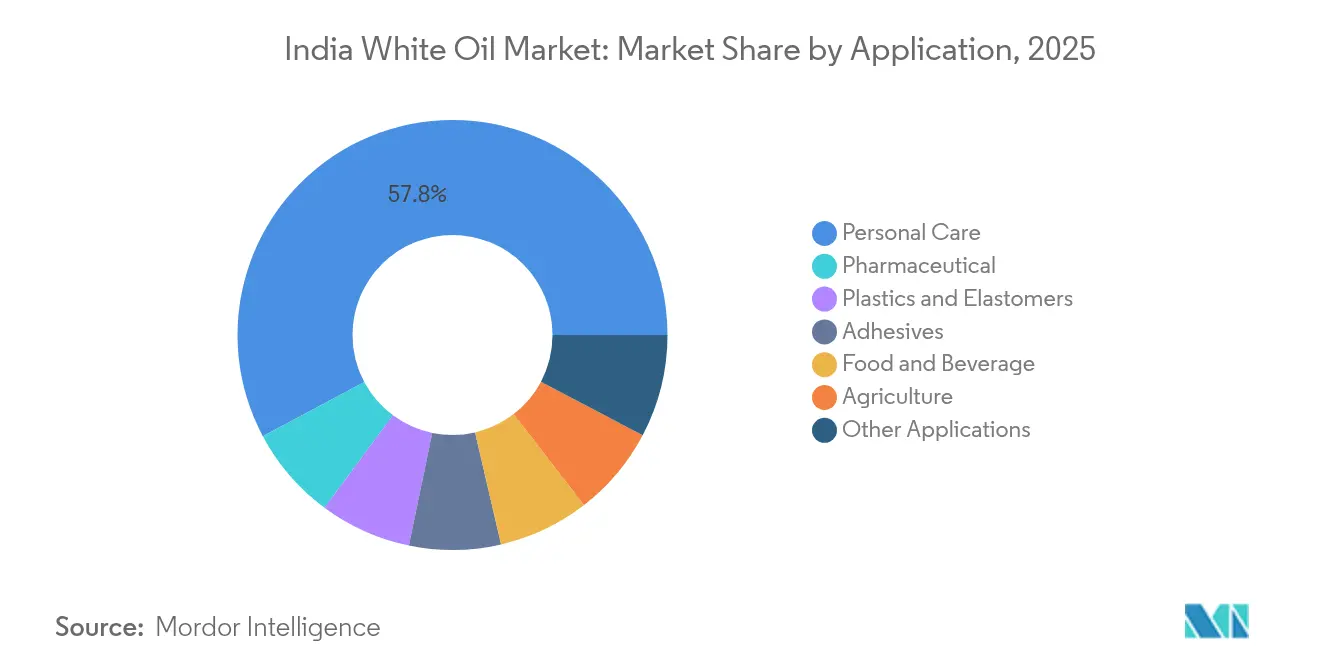

- By application, personal care led with a 57.80% share of the India white oil market in 2025; pharmaceutical uses are projected to expand at a 2.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India White Oil Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming cosmetics and personal-care manufacturing clusters | +0.6% | National, with concentration in Gujarat, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| Expanding domestic pharmaceutical formulations capacity | +0.4% | National, with hubs in Hyderabad, Ahmedabad, Mumbai | Long term (≥ 4 years) |

| Rising polymer-processing demand from plastic and elastomer plants | +0.3% | Gujarat, Maharashtra, Tamil Nadu petrochemical corridors | Medium term (2-4 years) |

| Stricter regulatory compliance driving high-purity white oil adoption | +0.2% | National, early adoption in export-oriented facilities | Short term (≤ 2 years) |

| Notable growth in the food and beverage sector | +0.2% | National, concentrated in processing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Cosmetics and Personal-Care Manufacturing Clusters

Robust growth in India’s cosmetics manufacturing hubs drives substantial uptake of high-purity white oils for emollient and carrier functions. Consumption remains well below levels in developed economies, providing a long runway for expansion. Major formulators such as Galaxy Surfactants require consistent white oil inputs to ensure product stability and texture across large-scale output lines. Integrated clusters in Gujarat, Maharashtra, and Tamil Nadu leverage feedstock proximity and consolidated logistics, lowering landed costs for processors. Brand owners targeting “clean beauty” formulations paradoxically depend on USP-grade mineral oils that deliver inertness and allergen-free properties, keeping demand resilient despite natural-ingredient marketing. These factors collectively strengthen the India white oil market as personal-care exports rise under free-trade pacts.

Expanding Domestic Pharmaceutical Formulations Capacity

India’s status as a global generics hub underpins sustained demand for USP-grade white oils in ointments, capsules, and processing equipment lubrication. Government incentives through Production Linked Incentive (PLI) schemes support Bulk Drug Parks, increasing active-pharmaceutical-ingredient self-sufficiency. U.S. FDA and EU regulatory regimes require strict batch traceability, favoring suppliers with documented quality systems. High-purity producers gain price premiums by offering certificates of analysis, stability data, and regulatory filing assistance. As production scales, consistent domestic supply reduces lead times for export consignments, reinforcing the India white oil market positioning in regulated pharma corridors.

Rising Polymer-Processing Demand from Plastic and Elastomer Plants

Technical-grade white oils remain indispensable as plasticizers, mold-release agents, and processing aids in the fast-growing polymer segment. India’s chemical economy is growing, indicating a strong feedstock pull for specialty oils. Gujarat’s integrated petrochemical complexes allow white-oil refiners to source base oils cost-effectively and supply processors within the same industrial zone, minimizing freight expenses. Consistency in viscosity and thermal stability provides manufacturability benefits over several synthetic alternatives. The high-volume, price-sensitive offtake stabilizes utilization rates for India's white oil market suppliers.

Stricter Regulatory Compliance Driving High-Purity Adoption

BIS standards, FSSAI rules, and FDA CFR 172.878 heighten purity thresholds, pushing users toward premium white oils that satisfy multiple certifications simultaneously[2]U.S. Food & Drug Administration, “CFR 172.878 – White Mineral Oil,” fda.gov . Export-oriented manufacturers require dual documentation—think USFDA plus Japanese Pharmaceutical Excipients—to avoid shipment rejections, and they lean on suppliers capable of managing audit demands. Compliance differentiates products beyond viscosity alone, enabling higher margins per liter. Smaller, non-certified producers face entry barriers, consolidating volume with established refiners and strengthening the India white oil market’s formal segment.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of functional substitutes (silicone, synthetic ester oils) | -0.3% | National, concentrated in high-performance applications | Long term (≥ 4 years) |

| Base-oil price volatility linked to crude swings | -0.2% | National, affecting all market segments | Short term (≤ 2 years) |

| Domestic ultra-low-sulfur refining scale-up delays | -0.1% | Gujarat, Maharashtra refining centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Functional Substitutes

Silicone fluids and synthetic esters capture applications demanding high thermal stability, low volatility, or biodegradable profiles, thereby capping mineral-oil penetration in premium segments. Aerospace, electronics cooling, and high-temperature food-processing lines increasingly specify synthetics whose lifecycle cost offsets their higher unit price. Manufacturers weighing formulation shifts must validate compatibility, redesign supply chains, and absorb material costs—factors that slow but do not halt substitution. Consequently, mineral grades maintain dominance in cost-sensitive and legacy formulations, moderating but not eliminating the India white oil market growth trajectory.

Base-Oil Price Volatility Linked to Crude Swings

Feedstock costs rise and fall with Brent crude, compressing processing margins for refiners unable to pass hikes downstream. India sources crude from the Middle East Gulf and Russia, making price curves susceptible to geopolitical disruptions. Smaller processors without hedging instruments or vertical integration feel margin squeezes first, occasionally leading to temporary production curtailments. End-users with strict cost ceilings shift purchases to spot volumes or delay orders, dampening near-term white-oil sales. Nonetheless, long-term supply contracts and rising in-country base-oil capacity provide stabilizing offsets within the India white oil market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: High-Purity Variants Capture Premium Pricing

Pharma and other high-purity grades held 72.45% India white oil market share in 2025 and are slated to expand at a 1.69% CAGR through 2031. Rising audits from foreign regulators and domestic authorities elevate purity expectations, prompting formulators to pay premiums for oils supplied with extensive documentation. USP, EP, and cosmetic-grade certifications enable access to lucrative export channels, boosting profitability despite modest volume growth. The India white oil market size realized from high-purity sales thus outperforms technical-grade revenues per liter.

Technical/industrial grades remain critical for polymer processing, lubricant blending, and general-purpose manufacturing, where cost sensitivity outweighs performance differentials. Integrated refiners capable of switching between grades without extensive downtime maximize plant utilization, blending base stocks to meet shifting demand patterns. Grade flexibility and in-house testing underpin customer confidence in batch consistency and strengthen long-term supply agreements.

By Viscosity: Low-Viscosity Oils Dominate for Processing Efficiency

Low-viscosity products captured 67.60% of the 2025 India white oil market size and are forecast to grow at a 1.63% CAGR through 2031. Their pumpability, blending ease, and filtration compatibility reduce production bottlenecks in automated plants, making them the default choice for cosmetics, pharmaceuticals, and plasticizers. Medium-viscosity grades service niche requirements—such as thicker skin-protection creams—while high-viscosity fractions address heavy-duty lubricity or moisture-barrier needs.

Key suppliers maintain broad viscosity slates, enabling formulators to fine-tune texture, spreadability, and processing parameters without switching vendors. Refiners with hydrotreating flexibility adjust cut points to optimize yields in response to market signals, preserving margin in the India white oil market even under feedstock volatility. Custom viscosity offerings, delivered with application engineering support, enhance stickiness of customer relationships and act as a barrier against low-price entrants.

By Application: Value-Added Uses Outpace Commodity Demand

Personal-care formulations accounted for 57.80% of the India white oil market in 2025, reflecting large-scale cosmetics manufacturing and rising consumer spending on skin and hair products. Although lower in volume, pharmaceutical applications represent the fastest growth at a 2.02% CAGR as drug makers scale excipient and topical formulations for domestic therapy and export markets. Over the forecast, pharmaceuticals capture share from technical-grade uses, increasing the India white oil market size tied to regulated sectors. Plastics, elastomers, adhesives, agriculture, and food-contact segments deliver stable baseline demand where technical-grade oils satisfy processing needs at lower cost, keeping utilization rates healthy for high-volume refiners.

Technical end-uses in plastics benefit from consistent viscosity, lubricity, and heat-transfer properties that mineral oils provide at competitive prices relative to synthetics. Food-and-beverage processors adhere to FSSAI and FDA purity mandates, favoring USP-grade white oils for incidental food contact, reinforcing demand for compliant suppliers. Niche uses in textiles, leather, and specialty coatings smooth cyclical swings in major segments. Market leaders such as Savita Oil Technologies leverage multi-grade portfolios and robust certification suites to serve all application groups, defending share in the India white oil market against both domestic and imported offerings.

Geography Analysis

Western India anchors production and consumption, with Gujarat hosting the Jamnagar refinery complex alongside Dahej’s integrated petrochemical zone, resulting in a concentrated supply of base and specialty oils. Majority of India’s dye and intermediates capacity resides in the state, creating dense downstream demand for technical- and high-purity white oils. Maharashtra ranks next, where Mumbai-Pune’s pharmaceutical, personal-care, and automotive clusters absorb significant low-viscosity grades. Tamil Nadu contributes through Chennai-Manali’s chemical corridor that serves both domestic users and export-oriented manufacturers.

Southern hubs benefit from seaport access that eases the import of select base oils and the export of finished formulations. Karnataka’s biotechnology and pharma nexus around Bangalore focuses on injectable and topical dosage forms, relying on USP-grade oils with tight batch-to-batch consistency, thereby augmenting the India white oil market demand for premium grades. Andhra Pradesh’s emerging chemical zones attract investment under state industrial policies, bringing incremental consumption into eastern coastal belts.

Northern regions participate primarily through agriculture and food-processing lines that use white oils in crop-protection emulsions and packaging machinery lubrication. Logistics challenges stemming from distance to western refineries encourage bulk shipments via rail and pipeline corridors, which recent infrastructure upgrades have eased. Meanwhile, export-oriented suppliers leverage India-GCC and ASEAN free-trade agreements, shipping white oil blends from western ports to over 75 countries, underscoring the geographic spread of the India white oil market.

Competitive Landscape

The India white oil industry is consolidated. Market players differentiate via breadth of viscosity ranges, certification coverage, and technical-service capabilities rather than price alone. Recent investments emphasize hydrotreating upgrades and in-line process analytics to guarantee color stability, odor neutrality, and ultra-low aromatic content essential for pharmaceutical and personal-care uses. Competition from synthetic substitutes triggers research and development collaboration between refiners and polymer labs to extend the operating windows of refined mineral oils. Firms co-develop blend packages combining white oils with antioxidants to enhance oxidative stability, defending mineral-oil positions in mid-temperature ranges. Long-term contracts with pharma majors and cosmetics global brands provide stable offtake and strengthen bargaining power when negotiating base-oil procurement, stabilizing the India white oil market despite volatile feedstock fundamentals.

India White Oil Industry Leaders

Gandhar Oil Refinery (India) Ltd

Savita Oil Technologies Ltd

Apar Industries

Indian Oil Corporation Ltd (IOCL)

ExxonMobil Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Daewoo, in partnership with Mangali Industries Ltd (MIL), is establishing India as a strategic hub for lubricant manufacturing and exports, targeting a 20% export share by FY 2028. The company has invested INR 30 crore in a lubricant plant in Maharashtra (40,000 MT capacity, expanding to 60,000 MT), with plans to invest INR 200 crore over the next three years. The company also plans to expand to establish a 10,000 kilo tons facility in Kandla, Gujarat, where it will produce white oil.

- July 2024: Texol Lubritech FZC, a foreign subsidiary of Gandhar Oil Refinery (India) Ltd, has secured a major contract from Abu Dhabi National Oil Company (ADNOC Distribution) to supply 30 million litres annually of lubricants for 2024, 2025, and 2026. This development strengthens the company’s position in the white oil and lubricant export market.

India White Oil Market Report Scope

White oils are mineral oils used to soften rubber and polymer products. They are used as a blending base for Pharmaceutical and Cosmetic Products. The India White Oil market is segmented by application, grade, and viscosity. By application, the market is segmented into plastics and elastomers, adhesives, personal care, agriculture, food and beverage, pharmaceutical, and other applications. By grade, the market is segmented into technical/industrial grade and pharmaceutical and other grades. By viscosity, the market is segmented into low, medium, and high. The report also covers the size and forecasts for the Indian White Oil market. For each segment, the market sizing and forecasts have been done based on volume (Kilo liter).

By Grade

| Technical / Industrial Grade |

| Pharma and Other High-Purity Grades |

By Viscosity

| Low |

| Medium |

| High |

By Application

| Plastics and Elastomers |

| Adhesives |

| Personal Care |

| Agriculture |

| Food and Beverage |

| Pharmaceutical |

| Other Applications |

| By Grade | Technical / Industrial Grade |

| Pharma and Other High-Purity Grades | |

| By Viscosity | Low |

| Medium | |

| High | |

| By Application | Plastics and Elastomers |

| Adhesives | |

| Personal Care | |

| Agriculture | |

| Food and Beverage | |

| Pharmaceutical | |

| Other Applications |

Key Questions Answered in the Report

How large is the India white oil market in 2026?

Volume reaches 319.95 million liters, reflecting its current scale across personal-care, pharmaceutical, and polymer segments.

What drives demand growth through 2031?

Shifts toward high-purity grades for cosmetics and pharma, plus expanding polymer-processing clusters, push volume to 346.73 million liters at a 1.62% CAGR.

Which application segment grows fastest?

Pharmaceutical formulations expand at 2.02% CAGR as India scales exports and domestic healthcare access.

Why do low-viscosity grades dominate?

Their pumpability and blending ease suit automated plants, giving them 67.60% market share in 2025 and a 1.63% CAGR outlook.

What risks could restrain growth?

Base-oil price volatility and substitution by silicone or synthetic esters present the largest headwinds.

Which regions consume the most white oil?

Gujarat and Maharashtra lead due to integrated refining, petrochemical, and personal-care manufacturing hubs.

Page last updated on: