Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

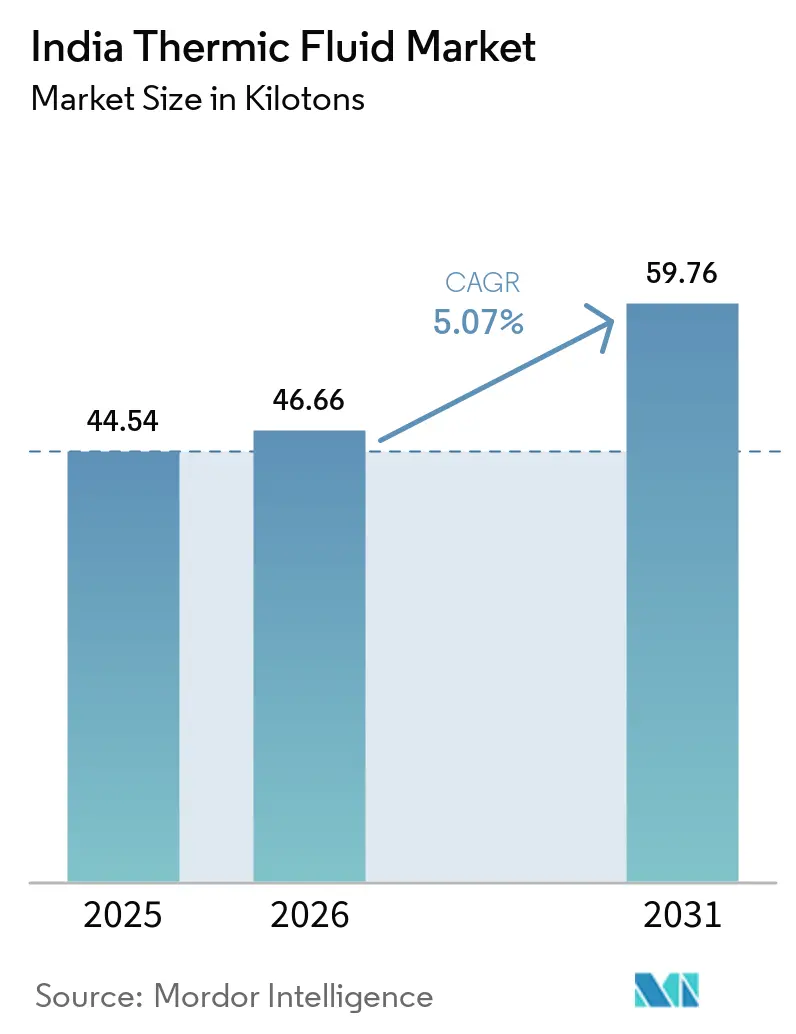

| Base Year Market Size (2025) | 44.54 kilotons |

| Market Volume (2026) | 46.66 kilotons |

| Market Volume (2031) | 59.76 kilotons |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Thermic Fluid Market Analysis by Mordor Intelligence

The India Thermic Fluid Market size is projected to expand from 44.54 kilotons in 2025 and 46.66 kilotons in 2026 to 59.76 kilotons by 2031, registering a CAGR of 5.07% between 2026 and 2031. Demand rests on three pillars: refinery and petrochemical integration that raises process-heating loads, rising deployment of concentrated solar power (CSP) plants that require high-temperature synthetic oils, and pharmaceutical investments that mandate closed-loop, contamination-free heat-transfer loops. Mineral-oil grades still lead by volume, but silicone and aromatic formulations are expanding faster because they withstand higher temperatures and longer service intervals. Western India’s chemical corridor anchors consumption, yet policy-driven growth in CSP capacity across Rajasthan, Gujarat, and Andhra Pradesh is shifting a share of future volumes toward renewables. Suppliers are differentiating through fluid life-extension additives, real-time monitoring sensors, and product portfolios that span mineral, glycol, silicone, and ester chemistries.

Key Report Takeaways

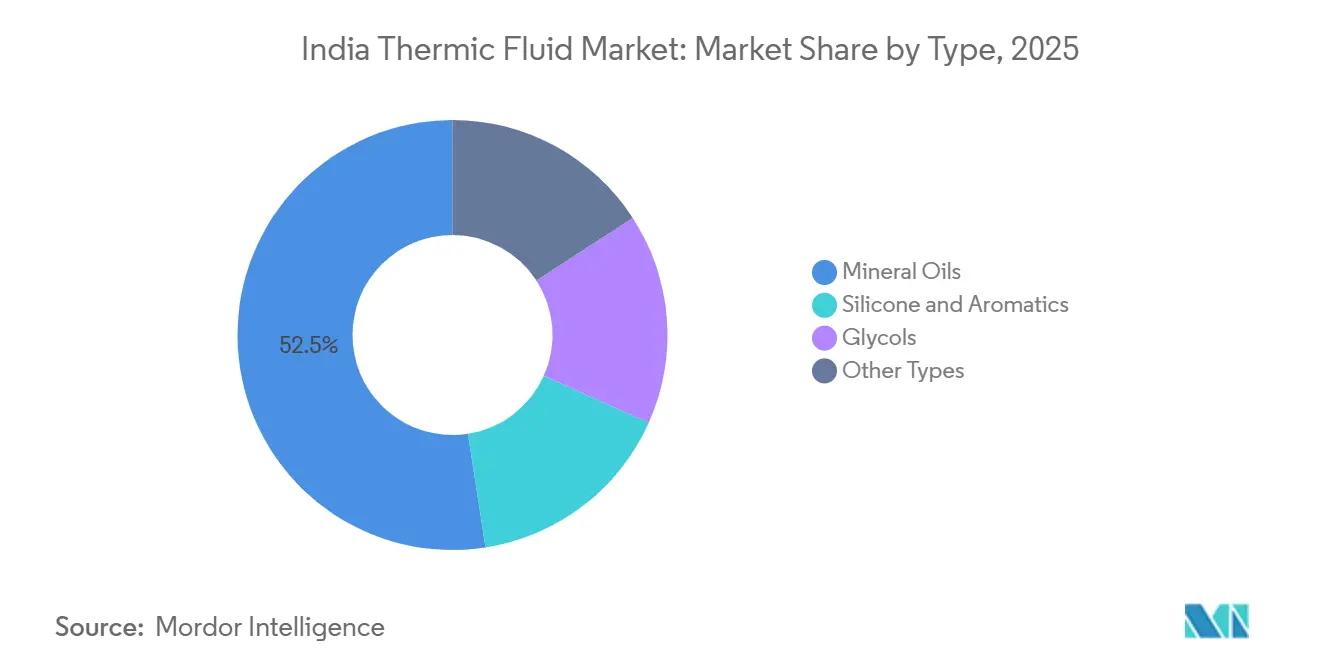

- By type, mineral oils led with 52.46% of India Thermic Fluid market share in 2025, while silicone and aromatic fluids are projected to grow at a 7.45% CAGR through 2031.

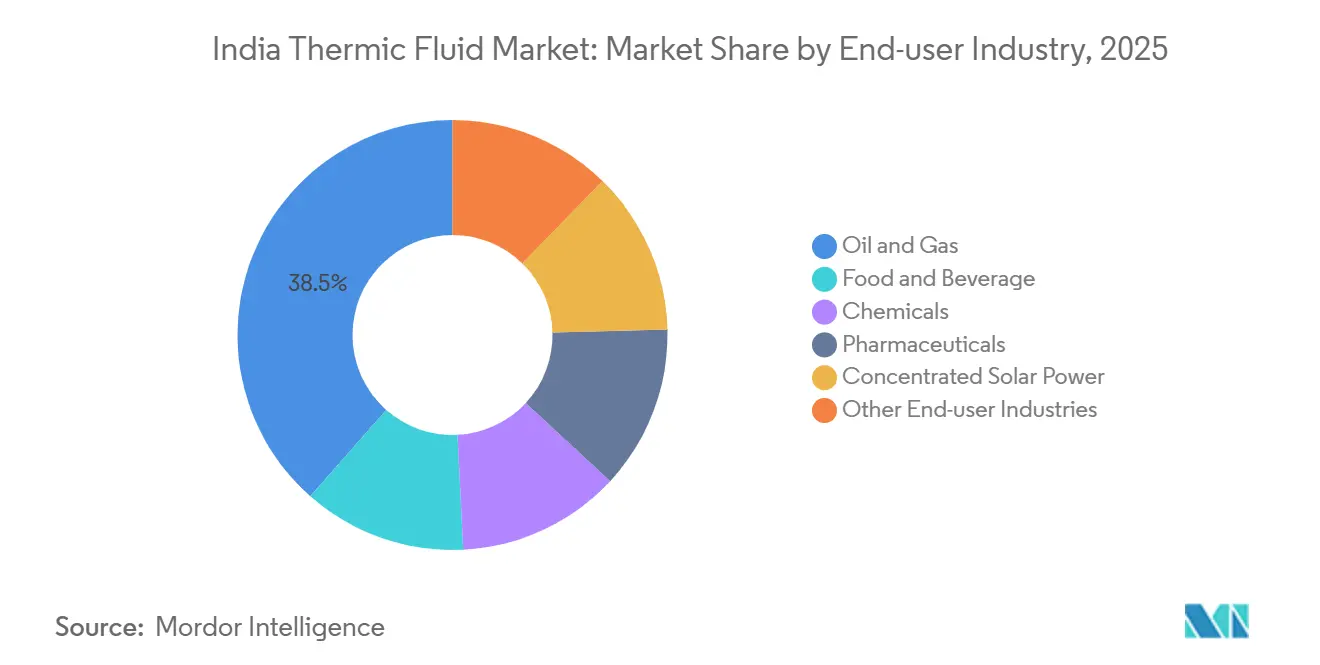

- By end-user, oil and gas accounted for 38.5% of the India Thermic Fluid market size in 2025 and Concentrated Solar Power (CSP) is advancing at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Thermic Fluid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extensive demand from oil and gas sector | +1.8% | National, with concentration in Gujarat (Jamnagar, Vadodara), Maharashtra (Mumbai refinery belt), Uttar Pradesh (Mathura), and Odisha (Paradip) | Medium term (2-4 years) |

| Increasing use in concentrated solar power (CSP) | +1.2% | Rajasthan (Nokh, Askandra), Gujarat (Kutch, Mehsana), Andhra Pradesh (coastal belt) | Long term (≥ 4 years) |

| Western-India chemical-processing capacity expansion (Greenfield + brownfield) | +1.0% | Gujarat (Dahej, Bharuch, Ankleshwar), Maharashtra (Raigad, Thane, Pune) | Medium term (2-4 years) |

| Government-funded bulk-drug parks mandating closed-loop HTF systems | +0.6% | Andhra Pradesh (Nakkapalli), Himachal Pradesh, Gujarat, with spillover to Tamil Nadu and Telangana pharma clusters | Medium term (2-4 years) |

| Government incentives for bio-based thermic fluids in MSME clusters | +0.3% | National MSME clusters, early adoption in Tamil Nadu (Coimbatore), Gujarat (Vapi, Ankleshwar), Maharashtra (Aurangabad) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extensive Demand From Oil and Gas Sector

Brownfield refinery upgrades and petrochemical additions dominate volume growth. BPCL’s INR 1.7 trillion (USD 20.3 billion) program covers new polypropylene and residue-upgradation units that operate at 350-450°C and rely on synthetic thermic fluids for stable heat transfer. Indian Oil has rolled out digital twins across seven refineries, trimming unplanned downtime by 22%, a move that elevates demand for fluids compatible with smart sensors and online diagnostics. HPCL’s Vizag complex has paired a residue-upgradation facility with on-site electrolyzers, lowering carbon intensity by 15% yet still depending on high-temperature fluid loops. A higher Nelson Complexity Index at all three state-owned refiners converts directly into additional heat-exchanger surface and therefore larger fluid inventories.

Increasing Use in Concentrated Solar Power

SECI’s forthcoming 500 MW CSP-with-storage tender stipulates that more than half of the contracted energy comes from solar-thermal generation, ensuring sizable molten-salt storage blocks[1]ET EnergyWorld, “SECI to Float 500 MW CSP Tender,” etenergyworld.com. Operational precedents, notably the 50 MW Godawari plant in Rajasthan that circulates Dowtherm A between 293°C and 390°C, validate the technical case for high-stability aromatic oils and a three- to five-year replacement cycle. Direct-normal-irradiance levels of 1,900-2,100 kWh/m² across north-western India strengthen project economics, while research at IISc Bangalore on supercritical CO₂ Brayton cycles signals future step-ups in operating temperature envelopes.

Western-India Chemical-Processing Expansion

Reliance Industries has filed for clearance of a USD 715 million Dahej package that adds ethylene-dichloride, PET-G, and cyclohexanedimethanol capacity, each requiring precise jacket temperatures and favoring closed-loop thermal-oil systems. A planned USD 10 billion crude-to-chemicals project at Jamnagar will further enlarge regional utility loads. Suppliers serving Dahej, Ankleshwar, and Raigad enjoy freight advantages that enable just-in-time replenishment and shorter inventory cycles. BASF’s February 2026 dispersion line at Mangalore for low-VOC acrylics offers an additional pull for reactor and drying-oven heating fluids.

Government-Funded Bulk-Drug Parks

The Union Scheme for Promotion of Bulk Drug Parks allocates INR 3,000 crore (USD 330 million) for common infrastructure, including mandatory closed-loop heat-transfer networks. Andhra Pradesh’s Nakkapalli park spans 2,002 acres and earmarks INR 1,438.89 crore (USD 165.47 million) for utilities, with Phase 1 completion scheduled for March 2026. API synthesis demands tight temperature control between 80°C and 180°C, steering selection toward low-toxicity propylene glycol and premium silicone fluids certified for incidental food contact. Strategic proximity to Gangavaram Port simplifies raw-material logistics and export flows, reinforcing the long-term need for specialty fluids and maintenance contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion and fire hazards of HTFs | -0.5% | National, with heightened scrutiny in high-density industrial zones (Gujarat, Maharashtra, Tamil Nadu) | Short term (≤ 2 years) |

| Volatility in base-oil and additive prices | -0.8% | National, import-dependent regions (coastal refineries, blending hubs in Mumbai, Chennai, Visakhapatnam) | Short term (≤ 2 years) |

| Substitution by high-efficiency electric heating in SMEs | -1.0% | National MSME clusters, early impact in Tamil Nadu (Coimbatore), Karnataka (Bengaluru), Maharashtra (Pune) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Base-Oil and Additive Prices

India imported 4.1 million t of base oils in 2025, but January 2026 volumes slipped to a 17-month low as Gulf suppliers reduced exports. Base oils form up to 90% of thermic-fluid cost. When Brent crude breached USD 90/bbl in mid-2025, Group I and Group II postings rose by up to 20%, squeezing blender margins and prompting selective pass-through pricing. Domestic base-oil expansions due in 2026 should temper exposure, yet structural linkage to crude persists, nudging buyers toward long-term contracts, hedging strategies, and fluid-life-extension technology.

Substitution by High-Efficiency Electric Heating in SMEs

A May 2025 roadmap released by the Global Green Growth Institute and the Confederation of Indian Industry suggests that high-temperature heat pumps, mechanical vapor recompression, and electric boilers could raise industrial electricity’s share of final energy to 25.3% by 2030[2]Global Green Growth Institute, “Industrial Heat Electrification Roadmap,” gggi.org. Implementation will need INR 20,000-30,000 crore of capital and concessional loans, but where tariffs sit below INR 6/kWh, SMEs (small and medium-sized enterprises) may favor electrification for processes under 250°C. Thermic-fluid vendors are countering by offering hybrid systems, online monitoring, and performance-based service contracts, yet an incremental share of low-temperature demand is expected to migrate to electric technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mineral Oils Anchor Volume, Silicones Capture Premium Growth

Mineral oils held 52.46% of India Thermic Fluid market share in 2025. Competitive pricing at INR 80-100/kg and ready availability from domestic refiners explain their dominance. Silicone and aromatic fluids together are forecast to expand at 7.45% CAGR, fueled by Concentrated Solar Power (CSP) adoption and pharmaceutical demand for wide operating-range heat carriers. The growth of the India Thermic Fluid market size for silicone grades reflects an increasing preference for single-fluid systems that swing from cryogenic cooling to high-temperature heating.

Glycol fluids, notably propylene glycol, compliant with FSSAI (Food Safety and Standards Authority of India) and FDA (Food and Drug Administration) norms, are carving out a share in food and drug applications. Research programs at IISc on liquid-metal and chloride-salt media remain pre-commercial, so mineral oils will continue to dominate price-sensitive sectors such as textile dyeing and asphalt batching. Over the forecast horizon, premium synthetics will steadily erode mineral-oil share where lifecycle cost, not upfront price, governs procurement.

By End-user Industry: Oil and Gas Leads, CSP Accelerates

Oil and gas accounted for 38.5% of the India Thermic Fluid market size in 2025. Integrated projects at BPCL’s Kochi and Bina complexes, along with Indian Oil’s refinery upgrades, translate into sustained orders for high-temperature synthetic oils capable of handling hydrocracking and residue-upgradation duty cycles. CSP, although smaller, is set to record the fastest 8.12% CAGR during the forecast period (2025-2031), underpinned by SECI (Solar Energy Corporation of India)’s tender pipeline and operational proof from Rajasthan’s parabolic-trough plants.

Chemicals and pharmaceuticals form a mid-tier but strategic segment. Reliance’s Dahej and Jamnagar expansions, plus bulk-drug parks with closed-loop mandates, are pushing adoption of FDA-grade glycols and low-toxicity silicones. Food and beverage processors add incremental volume as pasteurization and spray-drying lines modernize. Electric-heating substitution remains the chief headwind for low-temperature users, but sectors needing heat above 250°C will continue to depend on fluid-based technologies.

Geography Analysis

Western India dominates consumption with the largest share of 2025 volumes, propelled by the Gujarat-Maharashtra chemical belt that houses refineries, petrochemical crackers, and specialty-chemical plants. Logistics efficiency via Kandla, Nhava Sheva, and Mumbai ports lowers inbound feedstock costs and improves service intervals through local blending hubs. Southern India follows as an emerging growth pole. Andhra Pradesh’s Nakkapalli bulk-drug park and Karnataka’s precision-engineering clusters favor propylene glycol and silicone fluids meeting stringent safety norms. BASF’s Mangalore dispersion line further boosts regional process-heating demand.

Northern India’s share is anchored in Indian Oil’s Mathura and Panipat refineries and Rajasthan’s CSP installations. High direct-normal-irradiance values support future solar-thermal capacity additions, which in turn require aromatic oils with stability near 400°C. Eastern India remains nascent but could scale once Paradip’s petrochemical integration matures. Regional growth trajectories reflect infrastructure density, policy incentives, and proximity to ports; Western and Southern India are forecast to post the highest incremental volumes through 2031.

Competitive Landscape

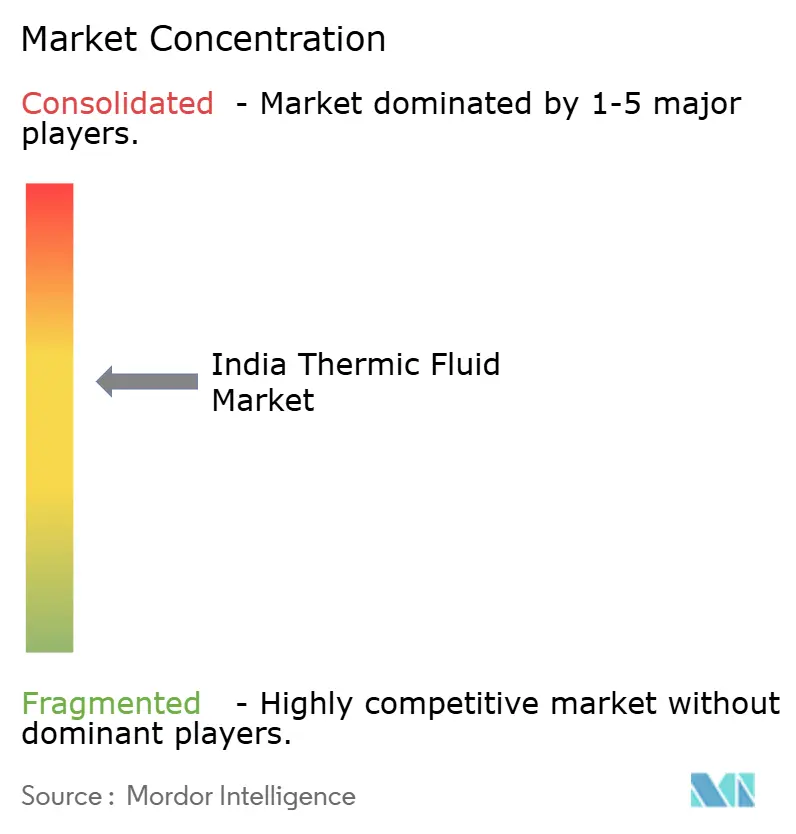

The India Thermic Fluid market is moderately concentrated. Competitive levers now center on backward integration for base oils, ISO-compliant manufacturing that aligns with PESO’s March 2025 traceability directive, and digital service bundles that embed IoT sensors for fluid-health tracking. Consolidation has been modest, yet sustained feedstock volatility and capital intensity of new blending technologies could trigger strategic alliances or acquisitions among smaller players seeking scale.

India Thermic Fluid Industry Leaders

Indian Oil Corporation Ltd

Bharat Petroleum Corporation Limited

Shell Plc

Exxon Mobil Corporation

Eastman Chemical Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Savita Oil Technologies Limited commissioned Phase 2 of its Synthetic Ester manufacturing plant located in Mahad, India. This plant produces synthetic esters catering to a range of applications, including transformer fluids, high-performance automotive and industrial lubricants, EV coolants, battery immersion cooling, and cooling fluids for data centers.

- October 2025: Bharat Petroleum Corp of India partnered with explorer Oil India to construct a refinery and petrochemical complex in southern India, with an investment of USD 11.38 billion. This project is poised to boost the production of mineral oils, providing a substantial uplift to the Indian Thermic Fluid market.

India Thermic Fluid Market Report Scope

Thermic fluids, also known as heat transfer fluids, are chemicals that can be in liquid or vapor form and used for transferring heat from one system to another. These fluids are mainly used in the reboiler, condenser, regenerator, and other heat-exchanging systems in the processing facilities of various end-user industries, including oil and gas, chemical, and pharmaceutical. Thermic fluids can be based on synthetic oils, molten salts, silicone fluids, glycols, etc.

The Indian Thermic Fluid market is segmented by type and end-user industry. By type, the market is segmented into mineral oil, silicon and aromatics, glycols, and other types. By end-user industry, the market is segmented into food and beverage, chemicals, pharmaceuticals, oil and gas, concentrated solar power, and other end-user industries. The market sizing and forecasts are based on volume (tons) for each segment.

By Type

| Mineral Oils |

| Silicone and Aromatics |

| Glycols |

| Other Types |

By End-user Industry

| Food and Beverage |

| Chemicals |

| Pharmaceuticals |

| Oil and Gas |

| Concentrated Solar Power |

| Other End-user Industries |

| By Type | Mineral Oils |

| Silicone and Aromatics | |

| Glycols | |

| Other Types | |

| By End-user Industry | Food and Beverage |

| Chemicals | |

| Pharmaceuticals | |

| Oil and Gas | |

| Concentrated Solar Power | |

| Other End-user Industries |

Key Questions Answered in the Report

How large is the India thermic fluid market today?

The market reached 44.54 kilotons in 2025, is estimated to rise to 46.66 kilotons in 2026, and is forecasted to reach 59.76 kilotons by 2031.

What is the expected growth rate for thermic fluids in India?

Over 2026-2031 the market is projected to grow at a 5.07% CAGR, reaching 59.76 kilotons by 2031.

Which segment of thermic fluids is expanding fastest?

Silicone and aromatic formulations are set to post a 7.45% CAGR through 2031, outpacing mineral oils.

Why is CSP important for fluid demand?

Each new parabolic-trough project circulates high-temperature synthetic oils and requires fluid top-ups every three to five years, driving recurring volumes.

Page last updated on: