India Construction Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

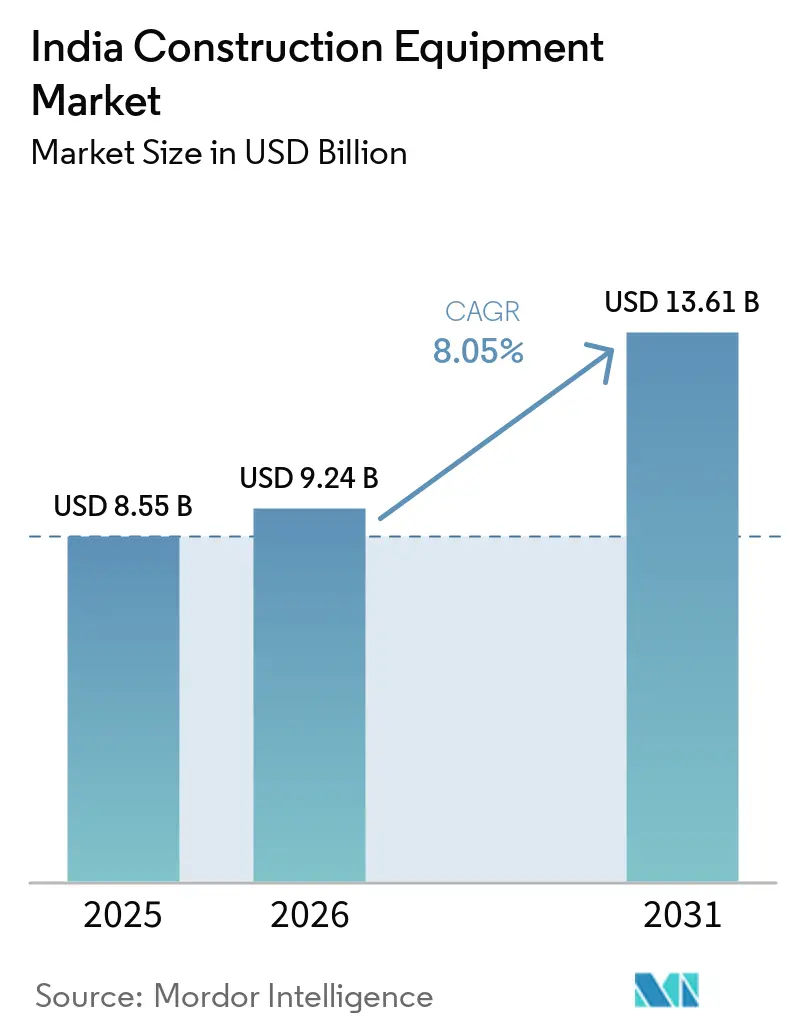

| Base Year Market Size (2025) | USD 8.55 Billion |

| Market Size (2026) | USD 9.24 Billion |

| Market Size (2031) | USD 13.61 Billion |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Construction Equipment Market Analysis by Mordor Intelligence

The Indian construction equipment market size is expected to grow from USD 8.55 billion in 2025 to USD 9.24 billion in 2026 and is forecast to reach USD 13.61 billion by 2031 at 8.05% CAGR over 2026-2031. Growth is underpinned by the National Infrastructure Pipeline, a USD 1.4 trillion program accelerating orders for earthmoving, road-building, and material-handling machinery. Stricter CEV Stage V emission norms in 2025 catalyze investment in cleaner drive systems while localization programs shorten supply chains and temper import costs. Regional demand is shifting as the government channels funds toward the North-East, mining reforms open high-horsepower equipment opportunities, and rental platforms broaden access for small contractors.

Key Report Takeaways

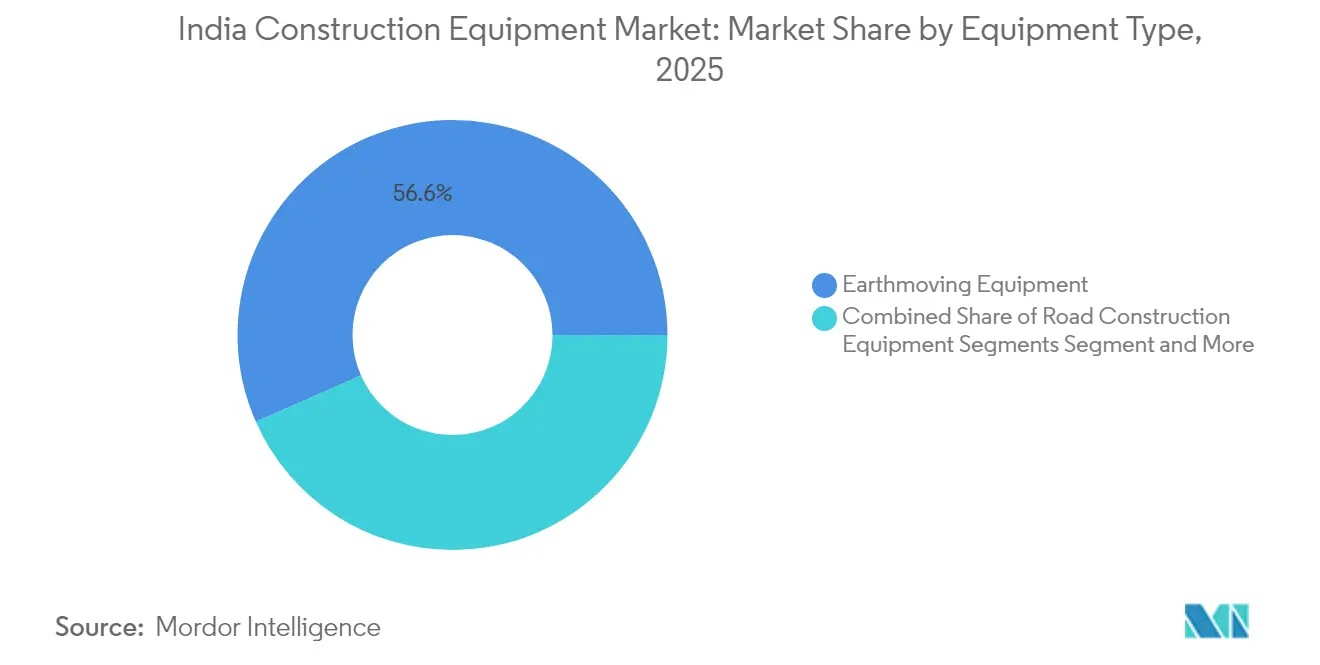

- By equipment type, earthmoving equipment captured 56.62% of the Indian construction equipment market share in 2025; road construction machinery is projected to expand at a 10.05% CAGR through 2031.

- By drive type, diesel equipment held 94.72% of the Indian construction equipment market size in 2025, while electric/hybrid models are advancing at a 15.68% CAGR to 2031.

- By end-user, infrastructure projects commanded 42.78% of the Indian construction equipment market size in 2025; mining is the fastest-growing user segment at an 10.72% CAGR to 2031.

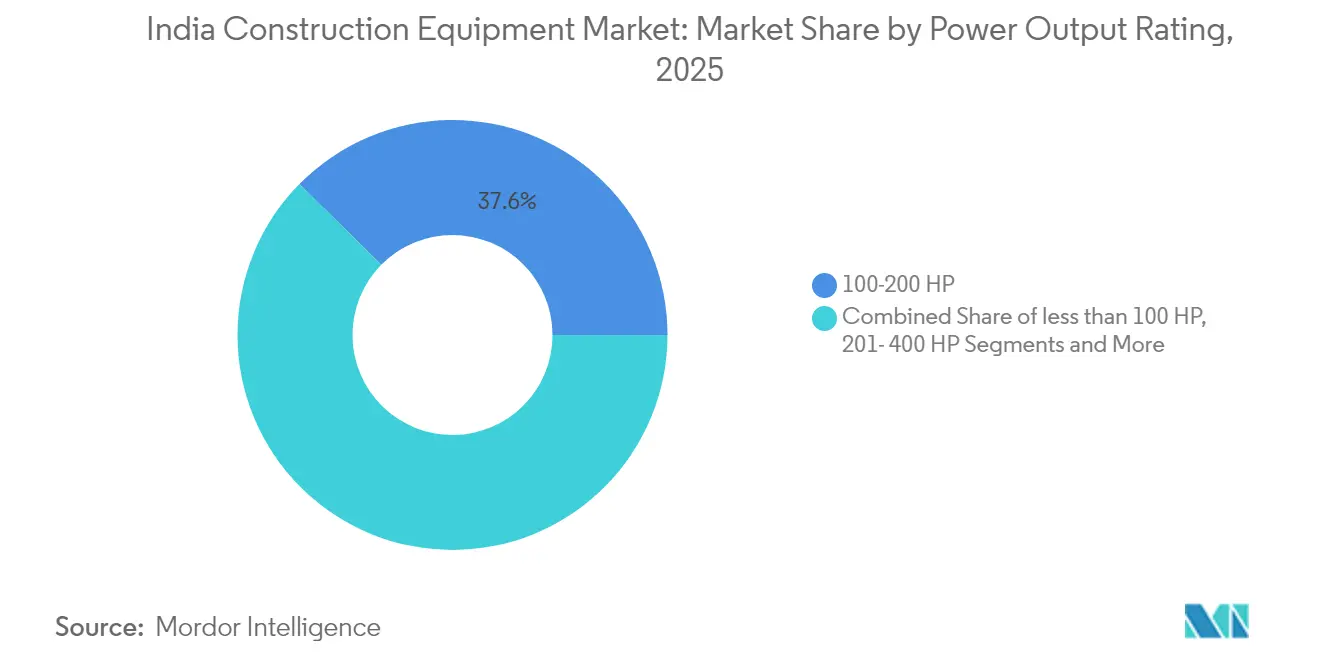

- By power output rating, the 101-200 HP class led with a 37.62% share of the Indian construction equipment market in 2025, whereas the >400 HP class is forecasted to rise at a 11.76% CAGR.

- By ownership model, contractor-owned fleets dominated with a 71.48% share in 2025; rental fleets are growing at an 12.69% CAGR through 2031.

- By region, South India led with a market share of 32.12%, whereas the North-East India projected to expand at a 12.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelines |

|---|---|---|---|

| National Infrastructure Pipeline Projects | +2.1% | National, with concentration in South and North-East India | Medium term (2-4 years) |

| Tier II & III Cities Urbanization | +1.5% | West and South India, with emerging impact in North India | Long term (≥ 4 years) |

| Bharatmala & Gati Shakti Programs | +1.8% | National, with emphasis on North and North-East connectivity | Short term (≤ 2 years) |

| Mining Sector Reforms | +1.2% | East and Central India, with spillover to North-East | Medium term (2-4 years) |

| Equipment Rental Platform Growth | +1.0% | Urban centers across all regions, with emerging rural penetration | Medium term (2-4 years) |

| Localized Manufacturing Investment | +0.7% | Manufacturing hubs in West and South India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-led Mega Infrastructure Projects

The National Infrastructure Pipeline spans 9,742 projects worth USD 3.08 trillion across transport, energy and urban sectors. Equipment sales jumped 26% in FY 2023-24 on the back of this pipeline, led by earthmoving machines and road finishers[1]Press Information Bureau, “Infrastructure Development in India – PIB,” pib.gov.in. Flagship corridors such as the Delhi-Mumbai Industrial Corridor and Bharatmala Phase I alone account for USD 172 billion of spending and drive sustained demand for excavators, backhoe loaders and compactors.

Rapid Urbanization in Tier II & III Cities

Middle-class migration to cities such as Lucknow, Jaipur, and Coimbatore is pushing high-rise residential starts 35% higher than 2023 levels. These constrained sites favor compact excavators, truck-mounted cranes, and telehandlers that maneuver in tight spaces[2]Indian Construction Equipment Manufacturers Association, “Activity Report 2023-24,” i-cema.in. Equipment makers offering smaller footprints and telematics-enabled safety features are capturing share in this urban infill wave.

Mining Sector Reforms

Mining sector reforms have fundamentally altered equipment procurement patterns, with the >400 HP segment projected to grow at 12% CAGR through 2030, significantly outpacing the overall market. The Commercial Coal Mining policy's implementation has opened 41 new coal blocks for private sector participation, creating unprecedented demand for high-capacity excavators and dump trucks. This structural shift is evidenced by the 61% growth in material handling equipment sales in FY 2023-24, compared to the previous fiscal year[3]Equipment India, “India’s CE Sales Surge 26% in FY24,” equipmentindia.com.

Fast-Track Road Corridor Execution

The accelerated implementation of Bharatmala Pariyojana and PM Gati Shakti initiatives has fundamentally transformed the road construction equipment landscape, strengthening the construction equipment industry in India and creating unprecedented demand for specialized machinery. The Bharatmala program, targeting 34,800 km of optimized road corridors, has already completed 18,926 km by November 2024, with the remainder under accelerated construction. This has driven a 40% year-on-year increase in road construction equipment sales in FY 2023-24, with asphalt pavers and motor graders experiencing the most significant growth. The PM Gati Shakti National Master Plan, with its integrated approach to infrastructure development, has further amplified demand by synchronizing project timelines across 16 ministries and departments.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Volatile Steel Prices | -1.2% | National, with higher impact on domestic manufacturers | Short term (≤ 2 years) |

| CEV Stage V Emission Norms Uncertainty | -1.0% | National, with higher impact on smaller OEMs | Short term (≤ 2 years) |

| Land Acquisition Delays | -0.9% | National, with acute impact in densely populated states | Medium term (2-4 years) |

| Limited Charging Infrastructure | -0.7% | Urban centers and project sites in remote locations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Steel Prices

Steel price volatility has emerged as a critical constraint on market growth, with raw material costs accounting for 60-65% of construction equipment manufacturing expenses. Price fluctuations of 15-20% within short timeframes have disrupted production planning and eroded profit margins for OEMs, particularly domestic manufacturers with limited hedging capabilities. These cost pressures are increasingly being passed on to end-users, with equipment prices rising by 8-12% in 2024 compared to the previous year.The situation is further complicated by the implementation of CEV Stage V emission norms, which is expected to add another 12-15% to equipment costs[4].

Persistent Land Acquisition Delays

Land acquisition challenges continue to undermine equipment utilization rates across the construction equipment industry in India, with approximately 815 out of 1,643 large-scale government projects experiencing delays as of 2024, resulting in a 19.48% cost overrun. These delays create significant inefficiencies in equipment deployment, with utilization rates for heavy machinery falling to 55–60% on affected projects compared to the optimal 75–80%. The problem is particularly acute in densely populated states where land fragmentation and ownership disputes complicate acquisition processes. This utilization gap translates directly to reduced returns on equipment investments and creates cash flow challenges for contractors with significant fleet commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Earthmoving Retains Commanding Lead

Earthmoving machinery generated 56.62% of 2025 unit sales. Backhoe loaders alone secured more than half of that volume, a testament to their versatility in excavation, trenching, and minor lifting tasks. Road-building equipment, logged the sharpest 40% annual growth as highway and corridor projects accelerated. However, road construction machinery is projected to expand at a 10.05% CAGR through 2031.

Earthmoving remains the anchor of the Indian construction equipment market thanks to cross-sector utility in infrastructure, mining, and real estate. Meanwhile, material-handling units sales surge as logistics parks and port modernization absorbed wheel loaders, forklifts, and reach stackers. Telematics adoption is rising swiftly, turning formerly “dumb iron” into connected assets that cut idle time and fuel burn.

By Drive Type: Diesel Dominance Faces Emerging Electric Alternative

Diesel-hydraulic rigs controlled 94.72% of deliveries in 2025, supported by mast-ready fuel infrastructure and proven ruggedness. Yet the electric/hybrid cohort, though only 5.28% of shipments, is scaling at a 15.68% CAGR as OEMs unveil Stage V-compliant loaders, compactors, and mini excavators.

Battery density gains, modular charging containers at project sites, and tightening emission norms are tilting buyer economics in favor of zero-tailpipe machines. Early adopters in metro rail and airport builds cite lower lifetime operating costs and easier compliance for urban projects with strict noise and emission caps. The Indian construction equipment market size for electric models is projected to triple by 2031.

By End-User Industry: Infrastructure Remains the Demand Bedrock

Infrastructure developments absorbed 42.78% of machines in 2025, reflecting steady federal outlays. Rail, road, and urban-renewal projects keep backhoe loaders, graders, and batching plants in continuous rotation. Mining and quarrying, at roughly one-fifth of demand, is the fastest-expanding customer sector at 10.72% CAGR on the back of commercial coal auctions and robust iron ore pricing.

Real estate follows with about a one-fourth share as tier II and III cities add high-rise towers and township formats. Industrial capital spending, especially in renewable energy and manufacturing corridors, rounds out demand, favoring cranes, piling rigs, and specialized foundation equipment. The diversified end-user base buffers the Indian construction equipment market against cyclical swings.

By Power Output Rating: Mid-Range Machines Dominate

The 101-200 HP segment leads the market with a 37.62% share in 2025, reflecting its optimal balance of power, versatility, and cost-effectiveness for a wide range of applications. This power range is particularly dominant in the backhoe loader and mid-size excavator categories that form the backbone of India's construction equipment fleet. The segment's prominence is reinforced by its suitability for the diverse operating conditions encountered across India's varied terrain and project types.

The >400 HP segment, though currently smaller market share but, is the fastest-growing category with a projected CAGR of 11.76% through 2031. This accelerated growth is driven primarily by increased mining activities and large-scale infrastructure projects that require high-capacity equipment for efficient operations. The diversification across power ratings reflects the market's maturation and the increasing specialization of equipment to meet specific project requirements.

By Ownership Model: Rental Growth Outpaces Traditional Purchasing

The contractor-owned segment dominates with 71.48% market share in 2025, reflecting the traditional preference for equipment ownership among established construction companies seeking long-term asset control and consistent availability. However, this segment's growth is moderating as financial constraints and project uncertainties drive interest in more flexible procurement models. The rental fleet segment is experiencing rapid expansion with a projected CAGR of 12.69% through 2031, more than double the overall market growth rate.

This shift toward rental models is driven by several factors, including the high initial costs of equipment, technological advancements that accelerate obsolescence, and the increasing project-specific nature of equipment needs. The rental market in India has transformed significantly. Digital platforms are enhancing the accessibility and efficiency of equipment rental services, while rental companies are expanding their fleets to include the latest technologies and specialized equipment. This trend is particularly pronounced among small and medium contractors who benefit from access to advanced machinery without prohibitive capital investments.

Geography Analysis

South India anchored 32.12% of the 2025 demand, buoyed by industrial corridors, technology parks, and port expansions in Tamil Nadu, Karnataka, and Telangana. Well-established dealer support and higher adoption of connected fleet technologies underpin its status as the most mature regional market.

North-East India is the breakout growth center, posting a projected 12.74% CAGR through 2031. Government schemes such as NESIDS and PM-DevINE inject funds into roads, bridges, and energy grids, pulling in excavators, dozers, and concrete pumps. Ongoing highway packages covering 3,582 km will sustain elevated equipment orders until at least 2028.

North India holds roughly one-quarter of sales, driven by the Delhi-Mumbai Industrial Corridor and metro expansions. West India accounts for close to 19.96%, powered by Mumbai’s urban makeover and Gujarat’s industrial investments. East and Central India, together near 15.26%, hinge on mineral extraction and logistics nodes that create steady call-offs for high-horsepower earthmoving gear. The evolving regional mix is broadening the Indian construction equipment market’s revenue base.

Competitive Landscape

Competition within the Indian construction equipment market is moderate. JCB India leads on the strength of its backhoe portfolio and a robust dealer footprint that guarantees parts within 24 hours across most districts. Tata Hitachi leverages domestic manufacturing in Dharwad and Kharagpur to trim lead times and achieve 60% localization. Caterpillar, Komatsu, and Volvo Construction Equipment round out the top tier, emphasizing technology differentiators such as machine-health analytics and autonomous haulage options.

Chinese brands SANY and XCMG are scaling fast by blending aggressive pricing with incremental localization. SANY’s plant now builds 12,000 units annually and targets 50% local content. Domestic specialist ACE integrates IoT to offer predictive maintenance and uptime contracts, an approach that turns equipment into a managed service.

Strategic collaborations with component suppliers are common as OEMs race to meet Stage V norms without steep price shocks. Dealer consolidation is underway in metro clusters, and financing arms owned by OEMs or banks are deepening, making credit easier for first-time buyers. These moves collectively reshape the Indian construction equipment market into a more value-driven, service-oriented ecosystem.

India Construction Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Volvo Construction Equipment

JCB

Tata Hitachi Construction Machinery Company Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vedanta Group confirmed an INR 80,000 crore (USD 9.6 billion) investment across six North-Eastern states, generating heavy demand for earthmoving and material-handling fleets.

- May 2025: The Centre earmarked INR 10 billion to upgrade navigation on the Brahmaputra and Barak rivers, lifting orders for dredgers and hydraulic excavators.

- April 2025: CASE Construction Equipment launched BS (CEV) Stage V-compliant compactors and backhoes with FPT F28 engines.

- March 2025: Ministry of Road Transport and Highways pledged completion of all 3,582 km of under-construction national highways in the North-East by 2028.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the India construction equipment market as the annual value of new, factory-built earthmoving, road-building, material handling, concrete, and material-processing machines that enter domestic service, whether purchased or leased, across all Indian states and union territories. Attachments, parts, compact hand tools, and used or rebuilt machines fall outside this scope.

Scope exclusion: after-market parts, attachments, and used-equipment imports are not included.

Segmentation Overview

- By Equipment Type

- Earthmoving Equipment

- Excavator

- Backhoe Loader

- Wheeled Loader

- Bulldozer

- Motor Grader

- Compaction Roller

- Road Construction Equipment

- Asphalt Paver & Finishers

- Cold Planers & Milling Machines

- Material Handling Equipment

- Mobile Cranes

- Forklift & Telehandler

- Aerial Work Platforms

- Concrete Equipment

- Transit Mixer

- Concrete Pump

- Batching Plant

- Material Processing & Crushing Equipment

- Jaw & Cone Crushers

- Screening Plants

- Pile-Driving & Drilling Rigs

- Earthmoving Equipment

- By Drive Type

- Conventional Hydraulic / Diesel

- Electric / Hybrid

- By End-User Industry

- Infrastructure (Roads, Rail, Airports, Ports)

- Real Estate (Residential, Commercial)

- Mining & Quarrying

- Industrial & Energy

- By Power Output Rating

- less than 100 HP

- 101- 200 HP

- 201- 400 HP

- greater than 400 HP

- By Ownership Model

- Rental Fleet

- Contractor-Owned

- By Region

- North India

- South India

- West India

- East India

- Central India

- North-East India

Detailed Research Methodology and Data Validation

Primary Research

We held structured interviews with OEM finance heads, rental-fleet owners in the south and west regions, procurement managers at EPC firms, and dealer associations. Their inputs validated utilization rates, rental mix, and hybrid-electric adoption assumptions that were only partially visible in public data.

Desk Research

Our analysts gathered foundational data from tier-1 public sources such as the Ministry of Road Transport & Highways, Department for Promotion of Industry & Internal Trade, Reserve Bank of India, the Indian Construction Equipment Manufacturers' Association (ICEMA) unit-sales bulletins, and UN Comtrade shipment records. These datasets framed baseline demand, import penetration, and public-capex momentum.

To refine price curves and technology shifts, we consulted company 10-Ks, investor decks, and tender portals, supplemented by paywalled tools like D&B Hoovers for contractor financials and Dow Jones Factiva for deal tracking. The sources listed are illustrative; numerous additional publications were reviewed to cross-check figures and narrative insights.

Market-Sizing & Forecasting

Mordor's model begins with a top-down reconstruction of domestic demand using ICEMA unit shipments, average selling prices, and import-export balances. Results are then pressure-tested through selective bottom-up roll-ups of OEM sales disclosures and dealer channel checks. Key variables include National Infrastructure Pipeline outlay, highway lane-kilometer awards, urban housing starts, average fleet age, and diesel-electric price spread. A multivariate regression links these drivers to historical equipment sales, while an ARIMA overlay captures election-cycle and monsoon seasonality before extending the forecast to 2030. Gaps in bottom-up data, notably for smaller OEMs, are bridged by applying validated market-share ratios from primary discussions.

Data Validation & Update Cycle

Outputs undergo three-layer review: analyst, senior domain lead, and research quality board, where anomalies beyond ±5 percent of external benchmarks trigger re-checks. Our figures refresh annually, with interim updates if policy shifts (for example, CEV Stage V mandates) materially alter demand.

Why Mordor's INDIA CONSTRUCTION EQUIPMENT Baseline Commands Reliability

Published estimates differ because research firms vary machine scope, rental inclusion, price bases, and refresh cadence.

The largest gaps stem from (1) some studies folding in used-equipment resale, (2) divergent ASP assumptions for high-horsepower mining units, and (3) currency conversions frozen at older exchange rates rather than quarterly averages, which this study employs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.55 Bn (2025) | Mordor Intelligence | - |

| USD 7.23 Bn (2023) | Regional Consultancy A | excludes concrete & crushing machinery; uses FY-23 ASPs without inflation adjustment |

| USD 11.38 Bn (2025) | Global Consultancy B | counts used imports and rental revenue; applies aggressive multi-segment markup |

Taken together, the comparison shows that Mordor Intelligence offers a balanced, transparent baseline tied to clearly documented variables, refreshed data, and repeatable steps that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the Indian construction equipment market?

The market was valued at USD 9.24 billion in 2026 and is forecast to reach roughly USD 13.61 billion by 2031, growing at an 8.05% CAGR.

Which equipment segment holds the highest India construction equipment market share?

Earthmoving machines dominate with a 56.62% share, led by backhoe loaders and crawler excavators.

How fast is the electric equipment segment growing?

Electric and hybrid models represent about 5.28% of 2025 sales but are expanding at a 15.68% CAGR under upcoming Stage V emission norms.

Which region is the fastest growing for construction equipment demand?

North-East India is projected to grow at a 12.74% CAGR through 2031 due to focused federal infrastructure investments.

Why is rental gaining ground in the Indian construction equipment market?

High capital costs, tighter project schedules, and rising obsolescence risk are driving SMEs toward rental platforms that provide flexible, pay-as-you-use access to modern fleets.

Page last updated on: