Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

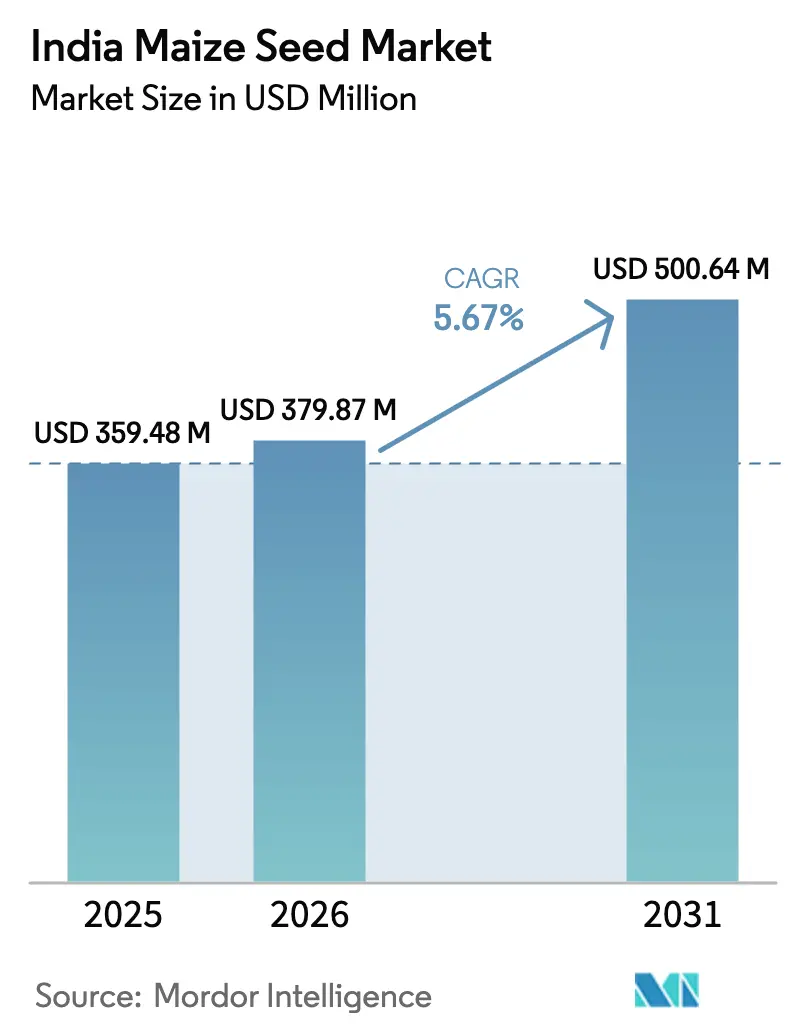

| Base Year Market Size (2025) | USD 359.48 Million |

| Market Size (2026) | USD 379.87 Million |

| Market Size (2031) | USD 500.64 Million |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Maize Seed Market Analysis by Mordor Intelligence

The India maize seed market size was valued at USD 359.48 million in 2025 and estimated to grow from USD 379.87 million in 2026 to reach USD 500.64 million by 2031, at a CAGR of 5.67% during the forecast period (2026-2031). Steady policy support for crop diversification, rising demand from the poultry feed sector, and continuous hybrid innovation are shaping expansion prospects across major producing states. Industry participants are benefiting from the government’s higher minimum support price for maize, which adds predictable revenue potential for farmers while encouraging the switch from rice–wheat rotations. Growth also tracks the ethanol blending mandate that channels incremental demand for high-starch hybrids suited to industrial processing. Competitive intensity remains moderate, with the top five companies holding a modest share of the India maize seed market in 2024, creating space for regional breeders that specialize in niche agro-climatic zones. Downside risks stem from persistent regulatory uncertainty around transgenic traits and climate-driven monsoon variability, although resilient hybrid portfolios and digital agronomy tools help mitigate the impact.

Key Report Takeaways

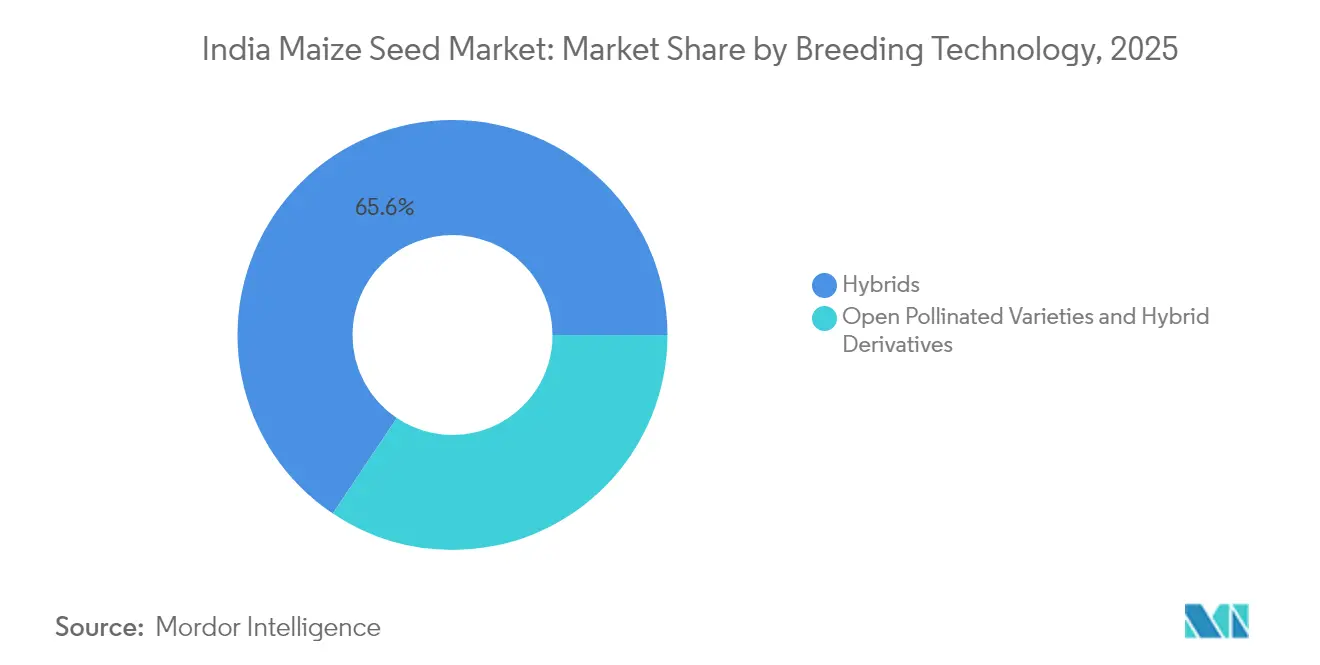

- By breeding technology, hybrids led with a 65.60% revenue share of the India maize seed market in 2025, and are projected to grow at a 5.86% CAGR through 2031.

- By state, Karnataka accounted for a 16.30% share of the India maize seed market size in 2025, while Tripura is advancing at a 9.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Maize Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government push for crop diversification | +1.2% | Punjab, Haryana,and Uttar Pradesh | Medium term (2-4 years) |

| Rising demand from poultry‐feed industry | +0.8% | Andhra Pradesh, Tamil Nadu,and Maharashtra | Short term (≤ 2 years) |

| Rapid hybrid-seed replacement rate | +0.6% | Karnataka, Telangana, Bihar | Short term (≤ 2 years) |

| Expansion of contract farming by starch processors | +0.5% | Maharashtra, Karnataka, and Andhra Pradesh | Medium term (2-4 years) |

| Emergence of drought-tolerant Quality Protein Maize (QPM) hybrids | +0.4% | Rajasthan, Madhya Pradesh, Maharashtra | Long term (≥ 4 years) |

| Digital agronomy platforms driving seed choices | +0.3% | Punjab, Haryana, and Western Maharashtra | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Push for Crop Diversification

The central government's strategic pivot toward maize cultivation represents a fundamental shift in India's agricultural policy framework, moving beyond traditional rice-wheat systems to embrace crops that offer superior water-use efficiency and market returns. The Ministry of Agriculture's National Mission for Sustainable Agriculture allocated impressive funds in 2024 specifically for crop diversification programs, with maize identified as a priority crop across 15 states[1]Source: Ministry of Agriculture and Farmers Welfare, “Crop Diversification and MSP Policy Updates,” Government of India, agricoop.nic.in . This policy momentum is creating unprecedented demand for high-yielding hybrid varieties, particularly in traditionally wheat-dominant regions where farmers are discovering maize's potential for double-cropping systems. The diversification push gains additional urgency from groundwater depletion concerns in Punjab and Haryana, where state governments are offering direct financial incentives for farmers transitioning from paddy to maize cultivation.

Rising Demand from Poultry-Feed Industry

India's poultry sector expansion is fundamentally reshaping maize demand patterns, with the industry consuming approximately 60% of total maize production and driving specifications for higher protein content and mycotoxin-free varieties. The Compound Animal Feed Manufacturers Association of India reported a 12.8% increase in feed production during 2024, with maize comprising 55-60% of typical broiler feed formulations. This demand surge is particularly pronounced in southern states, where integrated poultry operations are expanding rapidly, creating opportunities for seed companies to develop specialized feed-grade hybrids with enhanced nutritional profiles. The industry's shift toward contract farming models is establishing direct linkages between poultry processors and maize growers, ensuring premium pricing for varieties meeting specific quality parameters, including moisture content, aflatoxin levels, and kernel characteristics.

Rapid Hybrid-Seed Replacement Rate

The accelerating adoption of hybrid maize varieties reflects farmers' growing sophistication in seed selection and their recognition of yield advantages that can exceed 25-30% compared to traditional open-pollinated varieties. Agricultural extension data from the Indian Council of Agricultural Research indicates that hybrid replacement rates have increased to 78% in 2024, up from 65% in 2020, with the most dramatic shifts occurring in mechanized farming systems. This trend is particularly evident in contract farming arrangements, where processors specify hybrid varieties to ensure consistent quality and supply reliability, creating captive demand for premium seed products. The replacement cycle is shortening as farmers experiment with newer varieties offering specific traits like early maturity, disease resistance, or enhanced nutritional content, driving continuous innovation pressure on seed companies.

Expansion of Contract Farming by Starch Processors

The rapid expansion of starch processing capacity in India is creating structured demand for specific maize varieties, fundamentally altering traditional spot-market dynamics and establishing long-term partnerships between processors and farming communities. Major starch manufacturers like Gulshan Polyols and Sukhjit Starch increased their contracted acreage by 35% in 2024, under direct procurement agreements. These arrangements typically guarantee premium pricing of INR 200-300 per quintal above market rates for varieties meeting specific starch content and moisture specifications, creating strong incentives for farmers to adopt recommended hybrid varieties. The contract farming model is particularly attractive in Maharashtra and Karnataka, where established processing infrastructure provides reliable offtake channels and technical support for optimal cultivation practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Policy ban on transgenic maize seeds | -0.7% | Maharashtra and Karnataka | Long term (≥ 4 years) |

| Fragmented smallholder landholdings | -0.5% | West Bengal, Bihar, and Eastern Uttar Pradesh | Long term (≥ 4 years) |

| Counterfeit seed circulation in informal channels | -0.4% | Bihar, Jharkhand, and Eastern Madhya Pradesh | Medium term (2-4 years) |

| Climate-induced erratic monsoon patterns | -0.3% | Maharashtra, Karnataka, and Telangana | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Policy Ban on Transgenic Maize Seeds

India's regulatory stance on genetically modified crops continues to constrain the maize seed market's technological advancement, limiting access to traits like herbicide tolerance and enhanced insect resistance that have proven successful in global markets. The Genetic Engineering Appraisal Committee has maintained its moratorium on GM (Genetically modified) crop approvals since 2010, despite ongoing field trials and industry advocacy for trait-based solutions to emerging pest pressures [2]Source: Department of Biotechnology, “Genetic Engineering Guidelines,” dbt.gov.in. This regulatory environment forces seed companies to rely exclusively on conventional breeding techniques, extending development timelines and limiting trait stacking possibilities that could address multiple stress factors simultaneously.

Fragmented Smallholder Landholdings

The prevalence of small and marginal farming operations across India's maize-growing regions creates structural barriers to seed market development, limiting mechanization adoption and reducing farmers' ability to invest in premium hybrid varieties. National Sample Survey data indicate that 86% of maize farmers operate holdings smaller than 2 hectares, with average farm sizes continuing to decline due to inheritance patterns and population pressure. These fragmented operations often lack the scale economics necessary to justify investments in high-quality seeds, precision agriculture tools, and mechanized harvesting equipment that maximize hybrid variety potential. The constraint is particularly acute in Eastern states like West Bengal and Bihar, where land fragmentation is most severe and farmers often prioritize subsistence over commercial production objectives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Drive Market Evolution

Hybrids commanded 65.60% market share in 2025 and are projected to grow at 5.86% CAGR through 2031, driven by their superior yield potential and adaptability to diverse agro-climatic conditions across India's maize-growing regions.. This dominance is primarily attributed to the widespread adoption of hybrid corn seed across major maize-producing states, particularly in Bihar and Tamil Nadu, where hybridization rates have reached 100%. Hybrid maize varieties have gained significant traction due to their superior characteristics, including uniform cobs, enhanced resistance to diseases, pests, and drought conditions, as well as superior grain quality and higher cob counts.

Recent innovations in marker-assisted breeding are accelerating hybrid development cycles, with companies like Bayer and Corteva introducing varieties that combine multiple stress tolerance traits through advanced genomic selection techniques . The segment's dominance reflects farmers' increasing recognition of hybrid varieties' economic advantages, with yield premiums of 25-35% over open-pollinated varieties justifying higher seed costs in commercial farming operations. Non-transgenic hybrids represent the fastest-growing subsegment within this category, benefiting from regulatory clarity and consumer acceptance while delivering enhanced traits through conventional breeding approaches.

Geography Analysis

Karnataka's market leadership position with 16.30% share in 2025 stems from its diversified agricultural economy, extensive irrigation infrastructure, and strong institutional support for hybrid seed adoption through cooperative networks and agricultural universities. The state's maize cultivation spans both kharif and rabi seasons, creating year-round demand for different hybrid varieties suited to varying moisture and temperature conditions. Government initiatives like the Pradhan Mantri Fasal Bima Yojana have reduced weather-related risks, encouraging farmers to invest in premium hybrid varieties that offer higher yield potential but require greater input investments.

Tripura's emergence as the fastest-growing state market at 9.42% CAGR reflects strategic government investments in agricultural infrastructure, including micro-irrigation systems and post-harvest processing facilities that enhance the economic viability of maize cultivation. The state's focus on contract farming arrangements with poultry and starch processing industries creates stable demand for specific hybrid varieties, reducing market price volatility and encouraging farmer adoption of recommended varieties.

Maharashtra, Andhra Pradesh, and Telangana collectively represent significant market opportunities, benefiting from favorable agro-climatic conditions, progressive farming communities, and strong presence of agricultural input companies that provide comprehensive support services to maize growers. These states demonstrate successful integration of traditional farming knowledge with modern hybrid seed technology, resulting in productivity improvements that justify premium seed investments.

Competitive Landscape

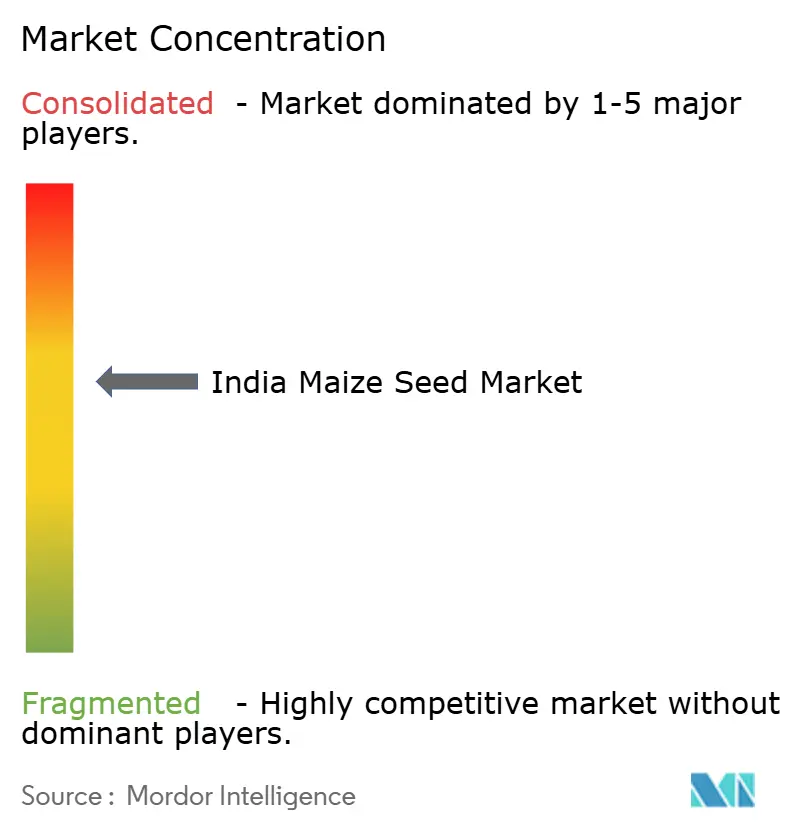

The Indian maize seeds market exhibits a moderately consolidated and balanced mix of global agricultural conglomerates and established domestic players, with both segments wielding significant influence in different regions. Global players like Bayer AG, Syngenta Group, and Corteva Agriscience Ltd are leveraging their extensive research capabilities and international experience, while domestic companies such as Kaveri Seeds maize and Nuziveedu Seeds maize capitalize on their deep understanding of local farming conditions and strong distribution networks. The market structure shows moderate consolidation, with the top five players accounting for a significant share, while still leaving room for regional players to maintain strong positions in their respective territories.

The competitive dynamics are shaped by a combination of organic growth strategies and strategic acquisitions, though large-scale mergers and acquisitions have been limited in recent years. Companies are increasingly focusing on building long-term relationships with farming communities through extensive farmer education programs and demonstration activities. The market is characterized by strong brand loyalty, particularly in regions where specific hybrids have proven successful, making it challenging for new entrants to establish themselves without significant investment in both product development and market development activities.

Success in the Indian maize seed market increasingly depends on companies' ability to develop products tailored to specific regional requirements while maintaining cost competitiveness. Incumbent players must continue investing in research and development to enhance their product portfolio with varieties that offer improved resistance to emerging diseases and pests, better adaptation to climate change, and higher yield potential. Building and maintaining strong relationships with seed production farmers, ensuring consistent seed quality, and expanding distribution reach in underserved areas are crucial for maintaining market position.

India Maize Seed Industry Leaders

Bayer AG

Syngenta AG

Corteva Agriscience

Kaveri Seeds

Nuziveedu Seeds Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Syngenta Group established a new seed production facility in Karnataka, targeting increased production of specialty hybrids for southern Indian markets. The facility incorporates advanced seed processing and quality control technologies to ensure consistent germination rates and genetic purity standards.

- March 2023: Pioneer Seeds, a subsidiary of Corteva Agriscience, launched 44 new corn seed hybrid varieties with new Vorceed Enlist corn technology to help manage corn rootworms.

- March 2023: Corteva Agriscience introduced gene-editing technology for added protection to corn hybrids, which helps in providing resistance to multiple diseases.

India Maize Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Andhra Pradesh, Bihar, Karnataka, Madhya Pradesh, Maharashtra, Rajasthan, Tamil Nadu, Telangana, Uttar Pradesh, West Bengal are covered as segments by State.Breeding Technology

| Hybrids | Non-Transgenic Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

State

| Andhra Pradesh |

| Bihar |

| Karnataka |

| Madhya Pradesh |

| Maharashtra |

| Rajasthan |

| Tamil Nadu |

| Telangana |

| Uttar Pradesh |

| West Bengal |

| Other States |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives | ||

| State | Andhra Pradesh | |

| Bihar | ||

| Karnataka | ||

| Madhya Pradesh | ||

| Maharashtra | ||

| Rajasthan | ||

| Tamil Nadu | ||

| Telangana | ||

| Uttar Pradesh | ||

| West Bengal | ||

| Other States |

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms