Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

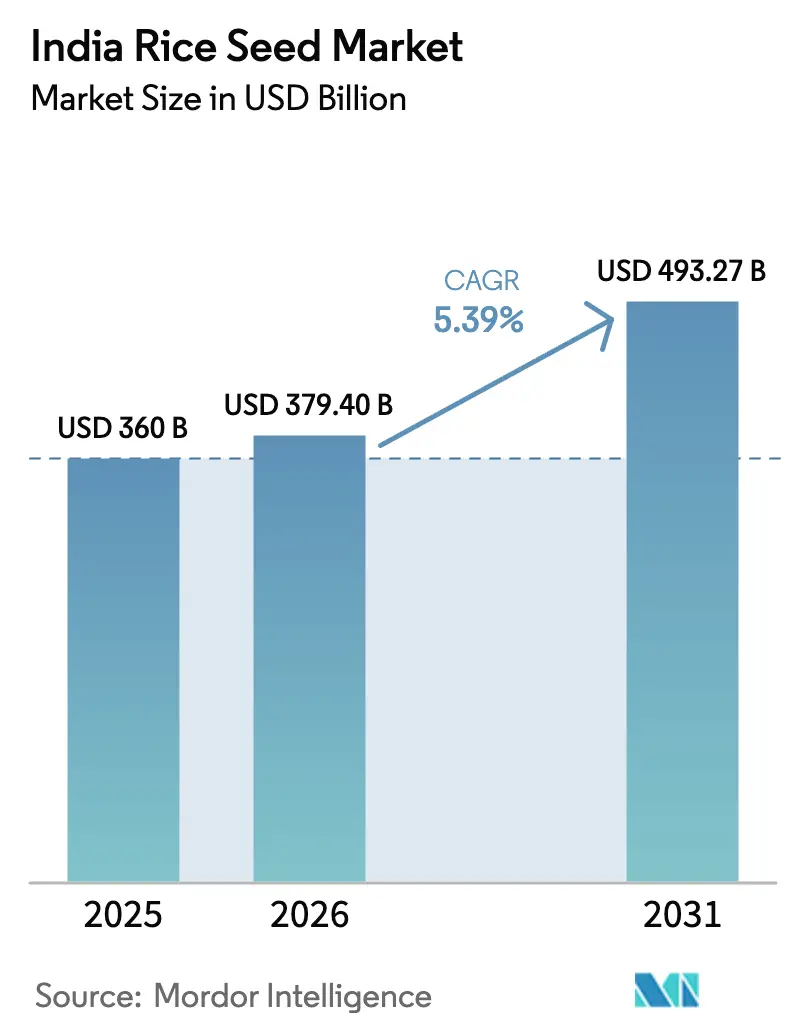

| Base Year Market Size (2025) | USD 360 Billion |

| Market Size (2026) | USD 379.4 Billion |

| Market Size (2031) | USD 493.27 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Rice Seed Market Analysis by Mordor Intelligence

The India rice seed market size was valued at USD 360 million in 2025 and estimated to grow from USD 379.4 million in 2026 to reach USD 493.27 million by 2031, at a CAGR of 5.39% during the forecast period (2026-2031). Government subsidies, accelerating seed-replacement reforms, and climate-resilient breeding breakthroughs drive adoption, while digital logistics platforms streamline rural distribution, cutting intermediary leakages and improving authenticity verification. Private and public research institutions are shortening variety cycles through genomic selection, letting firms refresh portfolios in under five years and sustain competitive differentiation. Rising consumer preference for biofortified zinc-rich rice creates predictable institutional demand from public feeding schemes, adding a nutrition dimension to seed strategy. Hybrid seed production costs continue to climb on double‐digit labor inflation, and counterfeit networks erode farmer confidence in branded varieties, moderating near-term growth.

Key Report Takeaways

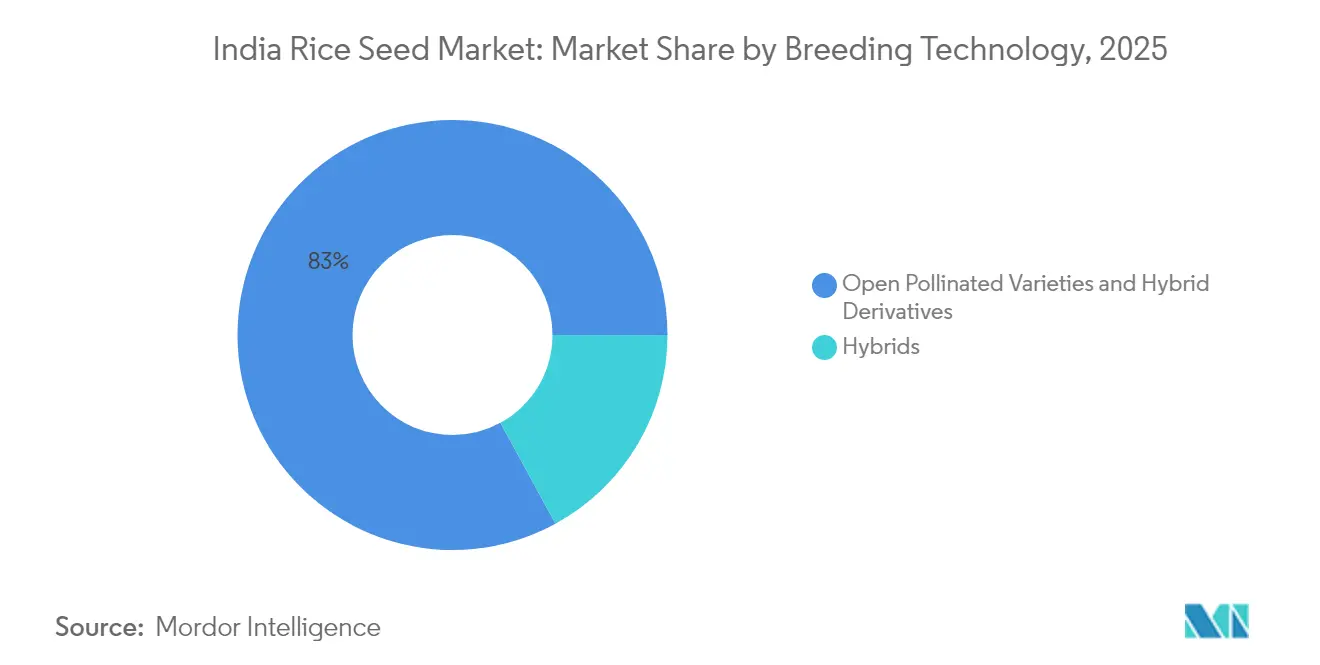

- By breeding technology, open-pollinated varieties and hybrid derivatives held 82.95% of India's rice seed market share in 2025, while hybrids are advancing at a 5.47% CAGR to 2031.

- By States, West Bengal led with 12.20% of India's rice seed market share in 2025, and Tamil Nadu recorded the fastest CAGR at 7.72% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Rice Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government hybrid-seed subsidies sustained under National Food Security Mission (NFSM) and Rashtriya Krishi Vikas Yojana (RKVY) | +1.2% | National, with higher penetration in Uttar Pradesh, Bihar, and West Bengal | Medium term (2-4 years) |

| ICAR-NRRI (Indian Council of Agricultural Research - National Rice Research Institute) release pipeline of climate-resilient inbred and hybrid varieties | +0.9% | Asia-Pacific core, particularly Odisha, Chhattisgarh, and Assam, flood-prone regions | Long term (≥ 4 years) |

| Rising seed-replacement rate (SRR) in major states after 2024 reforms | +1.1% | National, with early gains in Punjab, Haryana, and Andhra Pradesh | Short term (≤ 2 years) |

| Digital B2B seed-commerce platforms expanding rural reach | +0.7% | National, spill-over to rural districts in Tamil Nadu, Karnataka | Medium term (2-4 years) |

| Rapid-generation genomic breeding (IRRI OneRice framework) cuts variety cycle time | +0.5% | Global, with technology transfer to Indian breeding programs | Long term (≥ 4 years) |

| Growing consumer demand for biofortified zinc-rich rice in Public Distribution System (PDS) and mid-day-meal programs | +0.8% | National, concentrated in nutritional security focus states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Hybrid-Seed Subsidies Sustained Under National Food Security Mission (NFSM) and Rashtriya Krishi Vikas Yojana (RKVY)

Central subsidies covering up to 40% of certified seed costs improve affordability for smallholders who historically reused farm-saved grain, a shift that directly feeds the India rice seed market[1]Source: Ministry of Agriculture and Farmers Welfare, “National Food Security Mission Guidelines 2024,” Government of India, agricoop.nic.in. Farmers gain incremental yield and higher marketable surplus, reinforcing the habit of buying new seed each season instead of defaulting to retained stock. Seed producers, in turn, secure volume commitments that justify investments in climate-resilient germplasm and larger processing capacity. Over the medium term, the subsidy lever acts as a market equalizer by narrowing the cost gap between conventional and hybrid seed, accelerating technology diffusion in lagging eastern regions.

ICAR-NRRI (Indian Council Of Agricultural Research - National Rice Research Institute) Release Pipeline of Climate-Resilient Inbred and Hybrid Varieties

ICAR-NRRI (Indian Council of Agricultural Research - National Rice Research Institute) released several notable varieties in recent years, integrating Sub-1 submergence and drought-tolerance QTLs to counter monsoon volatility of paddy land. International collaboration through the OneRice genomic platform compresses variety development from eight to five years, letting breeders swiftly introgress multiple stress traits into single lines. Private companies license this germplasm, stack proprietary qualities such as grain aroma or herbicide tolerance, and commercialize regionally adapted packages. Adoption rates surge in Odisha and Assam, where floods routinely wipe out traditional varieties. By enhancing yield stability, climate-smart seed mitigates farmer risk and builds a premium tier within the India rice seed market, supporting both pricing power and regional food security goals.

Rising Seed-Replacement Rate (SRR) in Major States After 2024 Reforms

New state mandates require at least 15% certified seed use for minimum support price eligibility, linking quality seed directly to government market access. Punjab and Haryana moved early, verifying farmer compliance at procurement centers, lifting their seed-replacement rates above 85%. This regulatory nudge breaks entrenched dependence on farm-saved seed, especially among medium-scale growers. Seed firms benefit from more consistent offtake, enabling them to synchronize production schedules and reduce inventory write-downs. The policy also raises agronomic performance baselines, stimulating demand for value-added hybrids that deliver higher returns on the same acreage. Overall, strengthened procurement rules embed quality seed as a prerequisite for revenue security, boosting near-term volumes within the India rice seed market.

Digital B2B Seed-Commerce Platforms Expanding Rural Reach

Rural e-commerce players such as DeHaat processed around INR 500 crore (USD 60 million) in seed sales in 2024, with rice comprising 28% of volume. These platforms collapse multilayer supply chains, lower transaction costs, and finance working capital for village-level retailers, ensuring timely availability of premium seed. Embedded traceability functions authenticate brand integrity, discouraging counterfeit infiltration that historically diluted farmer trust. Data analytics forecast demand at district granularity, letting companies ship calibrated stock and minimize return freight. The digital channel also delivers agronomic advisories that reinforce correct hybrid management, indirectly raising realized yield and repeat purchases. As mobile penetration widens, online seed commerce amplifies penetration of branded product even in remote pockets, supporting an inclusive expansion of the India rice seed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High farmer dependence on farm-saved seed in Eastern states | -1.4% | Asia-Pacific core, concentrated in West Bengal, Bihar, Odisha | Long term (≥ 4 years) |

| Proliferation of counterfeit seed in informal channels | -0.8% | National, with a higher incidence in Bihar, Jharkhand, and Chhattisgarh | Medium term (2-4 years) |

| Hybrid seed production labor costs rising | -0.6% | National, affecting all hybrid seed production centers | Short term (≤ 2 years) |

| Phytosanitary rejections of imported parental lines slowing genetic introgression | -0.4% | Global, impacting international breeding programs and technology transfer | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Farmer Dependence on Farm-Saved Seed in Eastern States

Persistent farmer reliance on farm-saved seeds, particularly in eastern states, constrains certified seed market growth as approximately 46% of total seed usage in 2024 remained farmer-retained, reflecting deep-rooted cultural practices and economic constraints that resist policy interventions. West Bengal and Bihar show the highest dependence rates, with over 60% of farmers using farm-saved seeds due to fragmented land holdings averaging 0.8 hectares and limited access to formal credit systems [2]Source: Department of Agriculture and Cooperation, “Counterfeit Seed Enforcement Report 2024,” Ministry of Agriculture, agricoop.nic.in. This practice perpetuates lower productivity cycles where reduced yields limit farmers' capacity to invest in certified seeds, creating a self-reinforcing pattern that seed companies struggle to penetrate despite product improvements. The challenge is compounded by traditional knowledge systems where seed selection and storage practices are passed through generations, making behavioral change particularly difficult to achieve through conventional marketing approaches.

Proliferation of Counterfeit Seed in Informal Channels

The proliferation of counterfeit seeds through informal distribution channels causes estimated crop losses exceeding 12% annually and undermines farmer confidence in certified seed brands, particularly affecting hybrid varieties where genetic purity is critical for performance. Bihar and Jharkhand report the highest incidence of spurious seeds, with enforcement agencies seizing over 2,400 quintals of counterfeit seed packets in 2024. These counterfeit products often contain lower-quality genetic material or incorrect varietal labeling, leading to yield disappointments that discourage farmers from purchasing certified seeds in subsequent seasons. The informal channel network exploits price-sensitive segments by offering products at 20-30% discounts, making detection difficult until crop performance issues emerge during the growing season.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Traditional Varieties Maintain Dominance

Open-Pollinated Varieties and Hybrid Derivatives command 82.95% market share in 2025, reflecting farmer preferences for seed types that offer genetic stability and cost-effectiveness in diverse growing conditions. This dominance stems from the varieties' ability to be replanted without significant yield penalties, making them particularly attractive to resource-constrained farmers in eastern states where average farm sizes remain below 1.5 hectares. The segment's strength is further reinforced by the lower input requirements for fertilizers and pesticides compared to hybrid varieties, making them particularly attractive to low-income farmers. Additionally, OPVs demonstrate superior adaptability to local growing conditions and reduce dependence on hybrid seed imports. The public sector seed corporations, including 15 state seed corporations and two national seed corporations, maintain a strong presence in this segment, ensuring widespread availability and distribution. The segment's popularity is also driven by the traditional preferences of Indian farmers, who value specific tastes, aromas, textures, and cooking qualities that are characteristic of traditional rice varieties such as amsipiti dhan, chomala, and samba.

Hybrids are projected to grow at a 5.47% CAGR through 2031, driven by superior yield potential that can exceed traditional varieties by 20-30% under optimal management conditions. The breeding technology landscape is experiencing a gradual shift as hybrid seed production infrastructure expands and government subsidies reduce the cost differential between hybrid and traditional seeds. Companies are investing in two-line hybrid systems that eliminate cytoplasmic male sterility requirements, reducing production complexity and enabling more consistent seed supply.

Geography Analysis

West Bengal leads the India rice seed market with a 12.20% share in 2025, driven by the state's position as the country's largest rice producer with strong government support for certified seed adoption through state-sponsored distribution programs. The state's dominance in Open-Pollinated Varieties reflects farmer preferences for traditional Indica types that perform well in the region's flood-prone deltaic conditions and monsoon-dependent agriculture systems. West Bengal's seed replacement rate has improved to 38% in 2024, supported by state agricultural universities' variety development programs and cooperative seed distribution networks that reach remote rural areas.

Tamil Nadu collectively represents the fastest growing state, 7.72% CAGR through 2031, with these states leading hybrid rice adoption at penetration rates exceeding 60% due to strong private sector presence and farmer awareness of yield benefits. The region's emphasis on two-line hybrid systems and trait-stacked varieties positions it at the forefront of technological adoption, with companies like Kaveri Seeds and Nuziveedu maintaining significant market presence through extensive dealer networks.

Uttar Pradesh is leveraging its extensive rice cultivation area and progressive adoption of hybrid varieties in the state's western districts, where irrigation infrastructure supports intensive agriculture. The state demonstrates higher hybrid adoption rates compared to eastern regions, with districts like Meerut and Muzaffarnagar showing 45% hybrid penetration due to better market access and farmer education programs. Punjab maintains a significant market share despite a smaller cultivation area, reflecting the state's high seed replacement rates exceeding 85% and preference for certified varieties that meet procurement quality standards.

Competitive Landscape

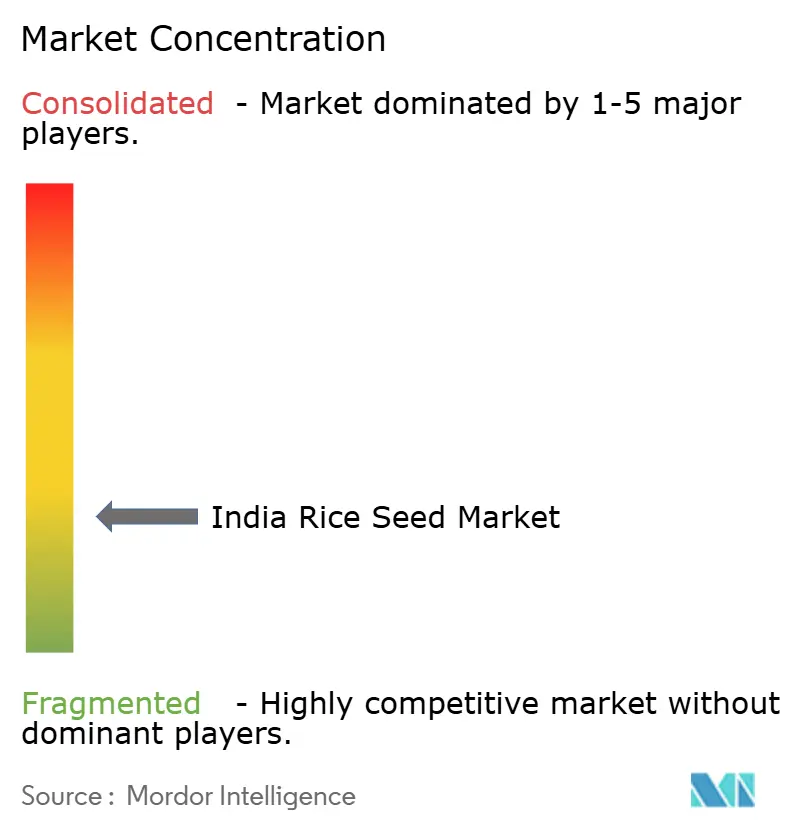

The competitive landscape is highly fragmented, with a mix of large multinational corporations and established local players like Kaveri Seeds, Advanta Seeds - UPL, Maharashtra Hybrid Seeds Co. (Mahyco), Nuziveedu Seeds Ltd, and Syngenta Group. The market structure shows a strong presence of domestic companies that have built significant market share through their understanding of local agricultural conditions and farmer preferences. While global agrochemical giants maintain their presence through advanced research capabilities and international germplasm access, local seed companies dominate through their extensive distribution networks and regional expertise. The market shows limited consolidation, with the top players collectively holding only about one-third of the market share, indicating significant opportunities for growth and expansion.

The market demonstrates a notable absence of significant merger and acquisition activities, with companies instead focusing on organic growth and strategic collaborations. Public sector seed corporations maintain a strong presence in the cereals segment, including rice seeds, with multiple state and national seed corporations actively operating in the market. The competitive dynamics are further shaped by the presence of numerous small and medium-sized seed companies that cater to specific regional markets and maintain strong relationships with local farming communities.

Success in the market increasingly depends on companies' ability to develop improved varieties that address specific regional challenges while maintaining cost-effectiveness. Market leaders are focusing on strengthening their research and development capabilities, particularly in developing varieties with enhanced traits such as disease resistance and drought tolerance. Companies need to establish strong partnerships with agricultural research institutions and maintain robust quality control systems to ensure consistent seed performance. Additionally, building and maintaining extensive distribution networks has become crucial for market success, as it ensures timely availability of seeds to farmers across different regions.

India Rice Seed Industry Leaders

Kaveri Seeds

Advanta Seeds - UPL

Maharashtra Hybrid Seeds Co. (Mahyco)

Nuziveedu Seeds Ltd

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Kaveri Seeds publicised a strategic partnership with IRRI to develop next-generation hybrid rice varieties incorporating climate resilience traits, with an investment commitment of INR 150 crore (USD 18 million) over three years for joint breeding programs targeting drought and submergence tolerance. This collaboration aims to reduce variety development cycles and introduce advanced genomic selection techniques in the company's breeding pipeline.

- August 2024: UPL's Advanta Seeds division established a new rice breeding center in Hyderabad, focusing on two-line hybrid development and genomic breeding technologies. The facility will serve as the company's Asia-Pacific hub for rice variety development and trait integration.

India Rice Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Andhra Pradesh, Assam, Bihar, Chhattisgarh, Odisha, Punjab, Tamil Nadu, Telangana, Uttar Pradesh, West Bengal are covered as segments by State.Breeding Technology

| Hybrids | Non-Transgenic Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

State

| Andhra Pradesh |

| Assam |

| Bihar |

| Chhattisgarh |

| Odisha |

| Punjab |

| Tamil Nadu |

| Telangana |

| Uttar Pradesh |

| West Bengal |

| Other States |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives | ||

| State | Andhra Pradesh | |

| Assam | ||

| Bihar | ||

| Chhattisgarh | ||

| Odisha | ||

| Punjab | ||

| Tamil Nadu | ||

| Telangana | ||

| Uttar Pradesh | ||

| West Bengal | ||

| Other States |

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms