Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.86 Billion |

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.19 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Cotton Seed for Sowing Market Analysis by Mordor Intelligence

The India cotton seed market size for sowing is expected to grow from USD 0.86 billion in 2025 to USD 0.91 billion in 2026 and is forecast to reach USD 1.19 billion by 2031 at 5.62% CAGR over 2026-2031. Rising demand for quality fiber from textile clusters, sustained government support through the Technology Mission on Cotton, and rapid diffusion of High Density Planting System practices are expanding seed replacement rates nationwide[1]Source: Press Information Bureau, “Government Initiatives Aim to Make India a Preferred Cotton Supplier for Global Brands,” pib.gov.in . Farmers continue to favor transgenic hybrids because they simplify insect control and deliver dependable yields, even as bollworm resistance pressures companies to accelerate trait stacking. Growing interest in climate-resilient short-duration hybrids for rain-fed belts, stronger export premiums under the Kasturi Cotton Bharat branding, and digital agriculture platforms that nudge smallholders toward certified seed purchases are all reinforcing the positive outlook. Lingering regulatory uncertainty around new genetically modified events, legally mandated seed price ceilings, and the still-dominant informal seed trade temper near-term growth.

Key Report Takeaways

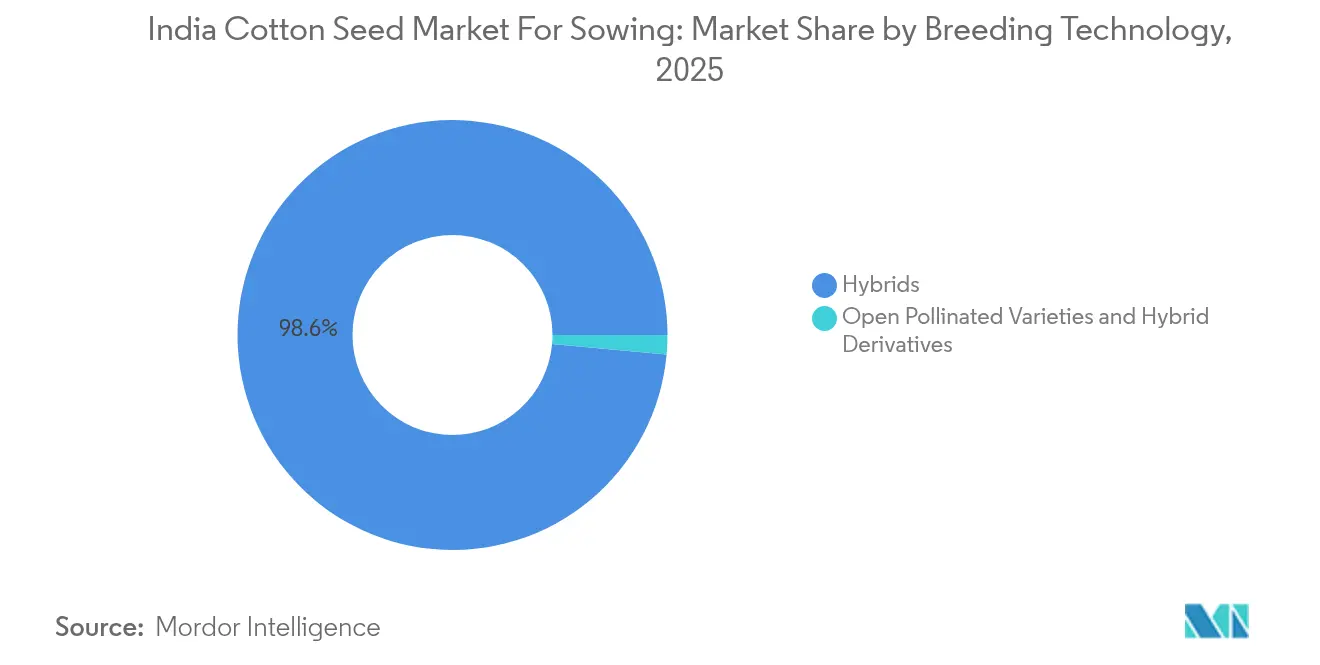

- By breeding technology, hybrid cotton seed commanded 98.55% of the India Cotton Seed for Sowing Market share in 2025 and is advancing at a 5.78% CAGR through 2031.

- By state, Maharashtra accounted for 22.35% of the India Cotton Seed for Sowing Market size in 2025, while Odisha is projected to expand at a 9.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Cotton Seed for Sowing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High adoption of Bt cotton hybrids | +1.2% | Nationwide, with a focus on Maharashtra, Gujarat, and Telangana | Medium term (2-4 years) |

| Government minimum support price incentives | +0.8% | All cotton-growing states | Short term (≤ 2 years) |

| Rising export demand for cotton lint | +0.6% | Processing hubs in Gujarat and Maharashtra | Medium term (2-4 years) |

| Pipeline of herbicide-tolerant trait approvals | +1.0% | Early uptake in Punjab and Haryana | Long term (≥ 4 years) |

| Digital ag-advisory platforms boosting seed replacement | +0.4% | Tech-savvy districts in several states | Medium term (2-4 years) |

| Climate-resilient short-duration hybrids for rain-fed areas | +0.7% | Drought-prone belts in the central and southern zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Adoption of Bt Cotton Hybrids

Bt hybrids dominate 98.7% of national sales, yet pink bollworm resistance has reduced trait efficacy from initial near-total control to levels that now require integrated pest management. The Central Institute for Cotton Research has approved 619 Bt hybrids, underscoring both genetic diversity and the relentless shift toward stacks that combine multiple Cry proteins with herbicide tolerance. Persistent farmer preference for cost-effective insect control ensures Bt cotton remains essential to the India cotton seed (seed for sowing) market[2]Source: Cotton Corporation of India, “A Profile of Indian Cotton: At a Glance,” cotcorp.org.in. Companies are responding by accelerating breeding cycles, strengthening refuge seed distribution, and preparing next-generation constructs such as Bayer’s IP4 lines, which promise broader spectrum control.

Government Minimum Support Price Incentives

Cotton Corporation of India procured 42.11 lakh bales in 2024 under the minimum support price program, disbursing significant value directly to 775,000 growers via Aadhaar-authenticated payments. The assured floor price limits downside risk, enabling smallholders to allocate a larger share of working capital to certified hybrid seed rather than farm-saved seed. Real-time SMS payment confirmations and stricter quality audit protocols have elevated farmer confidence, though global price softness keeps profit margins tight and limits willingness to pay steep premiums for advanced traits. Predictable income from MSP procurement enables farmers to purchase certified hybrid seed instead of relying on farm-saved seed.

Rising Export Demand for Cotton Lint

India's cotton exports are projected to double, supported by global supply disruptions and quality improvements through the Kasturi Cotton Bharat branding initiative. Export demand creates a quality premium that incentivizes farmers to adopt certified hybrid seeds with superior fiber characteristics. The government's Quality Control Order for mandatory cotton bale certification under IS12171:2019 standards reinforces this quality focus, requiring specific staple length, micronaire, and strength parameters that can only be achieved through appropriate seed selection.

Pipeline of Herbicide-Tolerant Trait Approvals

The illegal herbicide-tolerant cotton market scale with 15% penetration in 2024, reveals massive pent-up demand that formal seed companies cannot currently address due to regulatory bottlenecks. Bayer's BG-II RRF application remains pending with the Genetic Engineering Appraisal Committee (GEAC), while farmers increasingly resort to unauthorized varieties to manage labor-intensive weed control challenges. This regulatory delay is creating market distortions where illegal seeds command premium prices, indicating a strong willingness to pay for herbicide tolerance traits. The eventual approval of HT-BT cotton combinations could trigger rapid market share shifts, as demonstrated by similar trait introductions in other crops. Seed companies are positioning their trait pipelines and distribution networks to capitalize on this regulatory opening, with Corteva's Enlist HT cotton representing another potential game-changer awaiting approval.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty around Genetically modified (GM) approvals | -0.9% | Nationwide, with a larger effect on innovation-driven firms | Long term (≥ 4 years) |

| Seed price caps eroding breeder margins | -0.6% | Varies by state enforcement rigor | Medium term (2-4 years) |

| Pink bollworm resistance dampening yield gains | -0.8% | Punjab, Haryana, and western Gujarat | Short term (≤ 2 years) |

| Informal seed trade fragmenting certified demand | -0.5% | Remote districts nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty Around GM (Genetically Modified) Approvals

The Genetic Engineering Appraisal Committee's (GEAC) prolonged evaluation process for new GM traits creates strategic uncertainty that constrains long-term R&D investments and market planning. Bayer's BG-II RRF herbicide-tolerant cotton application exemplifies this bottleneck, where regulatory delays enable illegal seed proliferation while formal companies cannot commercialize approved technologies. The Seeds Act (1966) and state-specific regulations such as Maharashtra's Cotton Seeds Act (2009) create multiple approval layers that extend commercialization timelines and reduce competitiveness. This regulatory fragmentation particularly impacts multinational companies with global trait pipelines, as India-specific approval delays can render technologies obsolete by the time they reach farmers [3]Source: Gujarat Government, “The Gujarat Cotton Seeds Act 2008,” indiacode.nic.in. The uncertainty also affects venture capital investment in agricultural biotechnology startups, limiting innovation ecosystem development.

Seed Price Caps Eroding Breeder Margins

Cotton Seed Price Control Orders at the federal level and complementary state statutes fix maximum retail prices. These ceilings often overlook rising costs for trait licensing, parental maintenance, and grow-out testing. Margin compression pushes firms toward volume-led strategies rather than high-science hybrids, curbing the pace at which advanced germplasm enters the India cotton seed (seed for sowing) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrid Dominance Reshaping Innovation Priorities

Hybrids held 98.55% market share of India Cotton Seed for Sowing Market size in 2025, this overwhelming dominance is attributed to the superior characteristics of hybrid seeds, including higher productivity, enhanced insect resistance, improved stress tolerance, and superior fiber quality. Within the hybrids segment, transgenic hybrids, particularly those with Bt technology, hold the majority share, while non-transgenic hybrids comprise the remainder. The segment's leadership position is further strengthened by the widespread adoption of Bt cotton technology among Indian farmers, who recognize its benefits in terms of pest resistance and yield enhancement. The segment is also experiencing the fastest growth in the market, driven by continuous innovation in seed technology, increasing demand for high-yielding varieties, and the development of seeds with multiple beneficial traits such as drought tolerance and disease resistance.

The hybrid segment's 5.78% CAGR (2026-2031) reflects continued investment in trait development and breeding programs, despite pink bollworm resistance challenges that are driving companies toward trait stacking and next-generation technologies. Non-transgenic hybrids maintain relevance in export-oriented cotton where GM-free certification commands premiums, particularly for organic and specialty fiber markets. Insect-resistant hybrids within the transgenic category are undergoing technological evolution as single-gene Bt traits give way to multi-gene constructs designed to delay resistance development.

Geography Analysis

Maharashtra's 22.35% market share in 2025 stems from its dual advantage of favorable Vertisol soils and established seed distribution infrastructure. Gujarat and Telangana represent mature markets with sophisticated farmer networks and high technology adoption rates, creating demand for premium hybrid varieties and next-generation traits. Punjab and Haryana's cotton areas are increasingly focused on herbicide-tolerant varieties due to labor constraints and mechanization trends, making these states early adopters of new trait technologies.

Odisha's emergence as the fastest-growing state at 9.72% CAGR (2026-2031) reflects cotton's expansion into eastern India's rice-fallow systems. Odisha's rapid growth trajectory is supported by government initiatives promoting cotton in coastal districts where salinity-tolerant varieties can utilize previously uncultivated lands. The state-wise distribution reflects India's cotton belt evolution from traditional northwestern regions toward central and eastern states where land availability and lower input costs create competitive advantages.

Southern states represent the modest percentage of acreage but exhibit high varietal diversity due to heterogenous agro-ecologies. Telangana’s success with High Density Planting has increased seed rate per acre and shifted preference to compact-canopy hybrids. Karnataka spans black to red soils, fostering demand for broad-adaptation genetics, whereas coastal Andhra Pradesh requires salinity tolerance. Proximity to spinning mills in Tamil Nadu tightens feedback loops between fiber quality and seed choice, creating direct market incentives for premium seed procurement.

Competitive Landscape

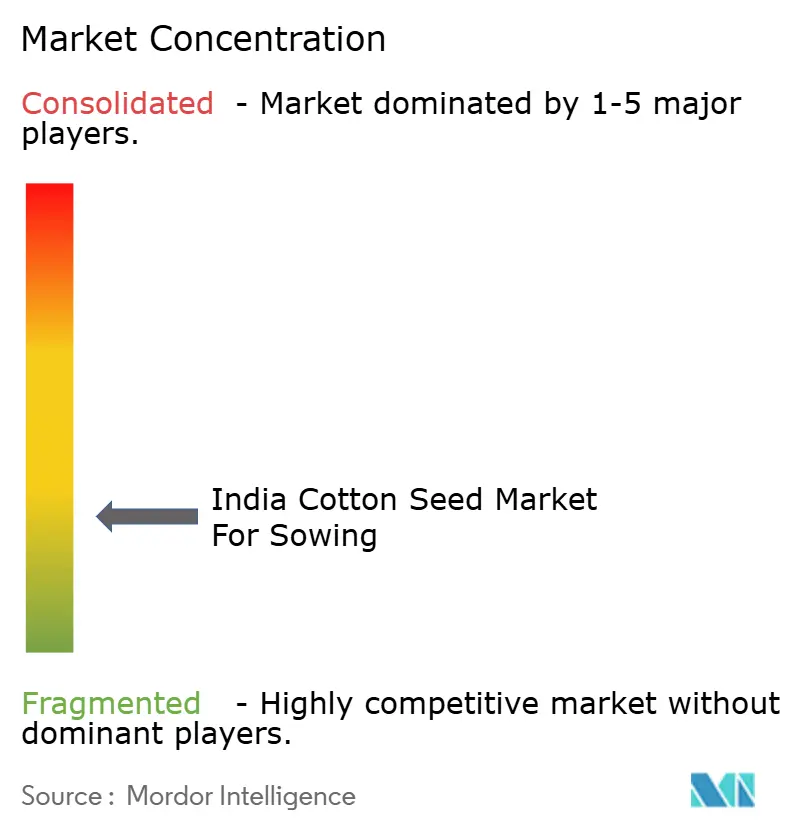

The India Cotton Seed for Sowing Market exhibits a fragmented structure with a mix of large established players and numerous regional seed companies. Local players hold a significant market share due to their deep understanding of regional agricultural conditions and strong distribution networks. Companies such as Kaveri Seeds, Maharashtra Hybrid Seeds Co. (Mahyco), Bayer AG, Krishak Bharati Co-Op Limited (KRIBHCO), and Rallis India Limited leverage extensive research capabilities and established farmer relationships to maintain their market positions.

The industry has witnessed limited consolidation through mergers and acquisitions, with companies instead focusing on organic growth and strategic collaborations. Joint ventures and technology licensing agreements, particularly for transgenic varieties, have emerged as preferred growth strategies over outright acquisitions. Companies are increasingly establishing partnerships with international research institutions and agricultural universities to enhance their technological capabilities and expand their product portfolios. The market structure is further influenced by the strong presence of state agricultural universities and research institutions that contribute to variety development and seed production.

Success in the India Cotton Seed for Sowing Market increasingly depends on companies' ability to develop innovative seed varieties that address specific regional challenges while maintaining high yield potential. Market leaders are strengthening their position through continuous investment in research and development, focusing on developing seeds with multiple traits such as insect resistance, drought tolerance, and improved fiber quality. Companies are also expanding their presence across different agro-climatic zones through strategic partnerships with local seed producers and distributors, while simultaneously building direct relationships with farming communities through extensive extension programs.

India Cotton Seed for Sowing Industry Leaders

Kaveri Seeds

Maharashtra Hybrid Seeds Co. (Mahyco)

Bayer AG

Krishak Bharati Co-Op Limited (KRIBHCO)

Rallis India Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ministry of Textiles announced the Technology Mission on Cotton with budgetary support aimed at making India the preferred global cotton supplier through enhanced yield and quality improvements. The mission emphasizes High Density Planting System (HDPS) adoption and collaboration with NABARD and state agencies to scale the Akola Model pilot program, requiring high quantities of quality seeds for successful implementation

- October 2024: Multi Commodity Exchange (MCX) launched cottonseed wash oil futures contract with 5-tons trading units and delivery basis ex-tank Kadi, Gujarat, providing price risk management tools for cottonseed crushers and oil refineries. The contract addresses high price volatility from raw material availability and competing vegetable oil markets affecting the broader cottonseed value chain.

India Cotton Seed for Sowing Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Andhra Pradesh, Gujarat, Haryana, Karnataka, Madhya Pradesh, Maharashtra, Odisha, Punjab, Rajasthan, Telangana are covered as segments by State.Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Insect Resistant Hybrids | |

| Open Pollinated Varieties and Hybrid Derivatives | ||

State

| Andhra Pradesh |

| Gujarat |

| Haryana |

| Karnataka |

| Madhya Pradesh |

| Maharashtra |

| Odisha |

| Punjab |

| Rajasthan |

| Telangana |

| Other States |

| Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Insect Resistant Hybrids | ||

| Open Pollinated Varieties and Hybrid Derivatives | |||

| State | Andhra Pradesh | ||

| Gujarat | |||

| Haryana | |||

| Karnataka | |||

| Madhya Pradesh | |||

| Maharashtra | |||

| Odisha | |||

| Punjab | |||

| Rajasthan | |||

| Telangana | |||

| Other States | |||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms