Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

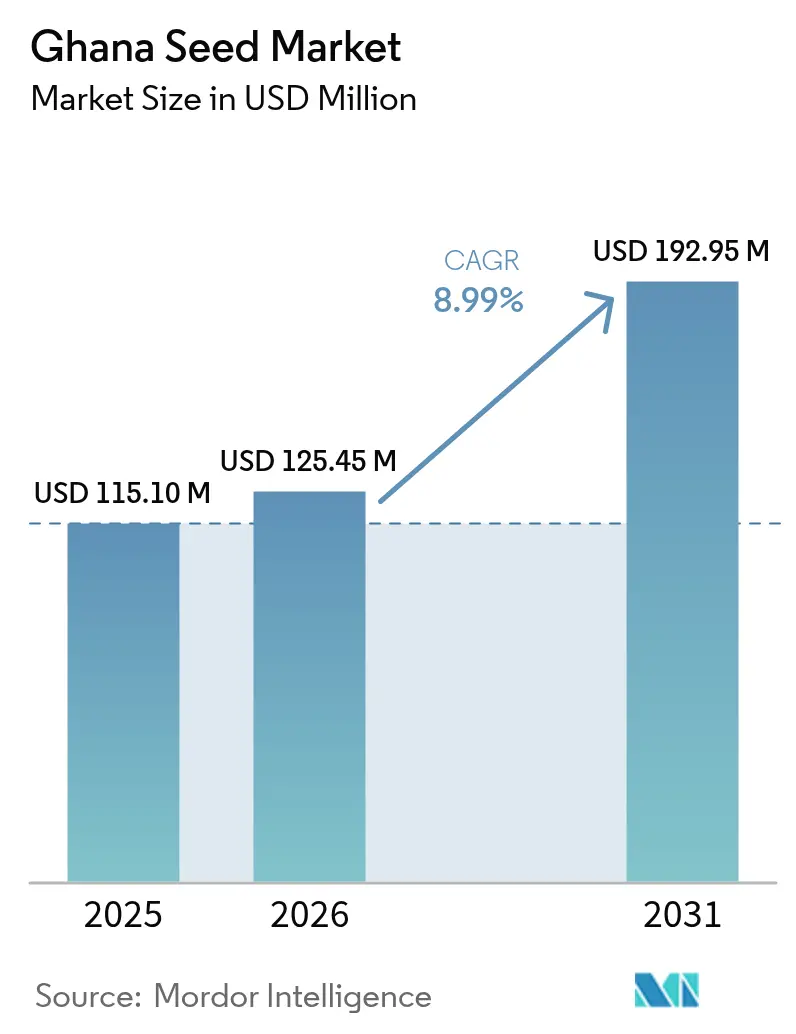

| Base Year Market Size (2025) | USD 115.10 Million |

| Market Size (2026) | USD 125.45 Million |

| Market Size (2031) | USD 192.95 Million |

| Growth Rate (2026 - 2031) | 8.99% CAGR |

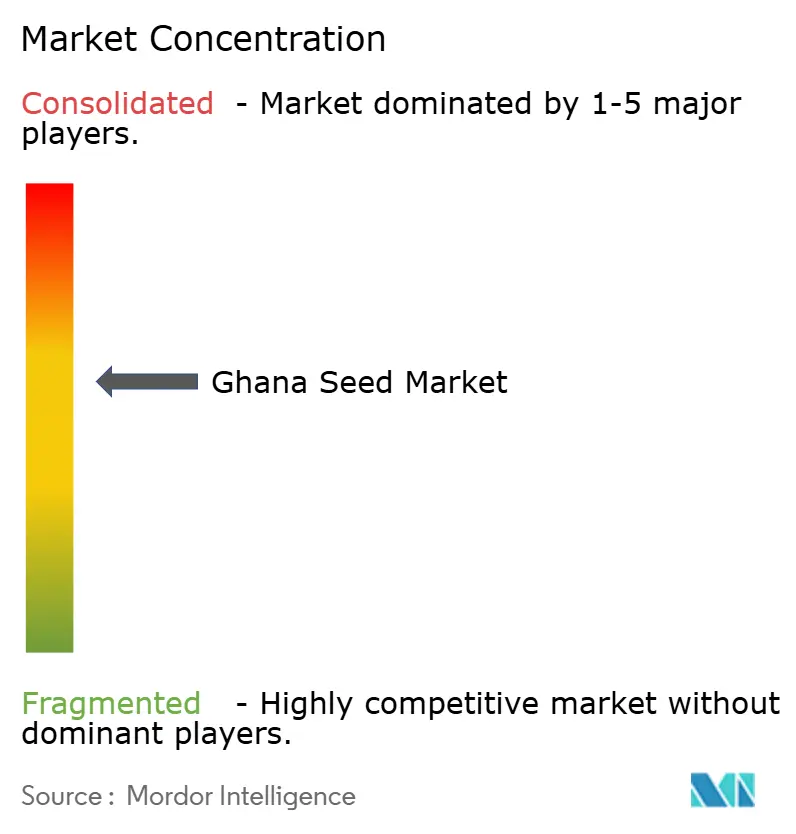

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ghana Seed Market Analysis by Mordor Intelligence

The Ghana seed market size is expected to grow from USD 115.10 million in 2025 to USD 125.45 million in 2026 and is forecast to reach USD 192.95 million by 2031 at 8.99% CAGR over 2026-2031. Strong public-sector backing, rising adoption of climate-smart varieties, and expanding digital distribution collectively lift demand for certified seed. The Planting for Food and Jobs 2.0 program now subsidizes up to 30% of certified seed costs, widening formal sales beyond larger commercial growers. Additional momentum comes from the World Bank’s USD 125.94 million boost to the West Africa Food System Resilience Program for Ghana, which funds digital advisory services and sustainable intensification practices that rely on quality seed [1]Source: World Bank Group, “Ghana: Building Resilience from Crisis,” worldbank.org . Climate-smart agriculture initiatives demonstrate a measurable impact, with Climate Research for Africa (AICCRA) reporting yield improvements of up to 62% in five regions through demonstration plots that promote drought- and pest-tolerant varieties [2]Source: Kyere R O, “Climate-smart seed varieties improve maize production in Ghana,” AICCRA, aiccra.cgiar.org.

Key Report Takeaways

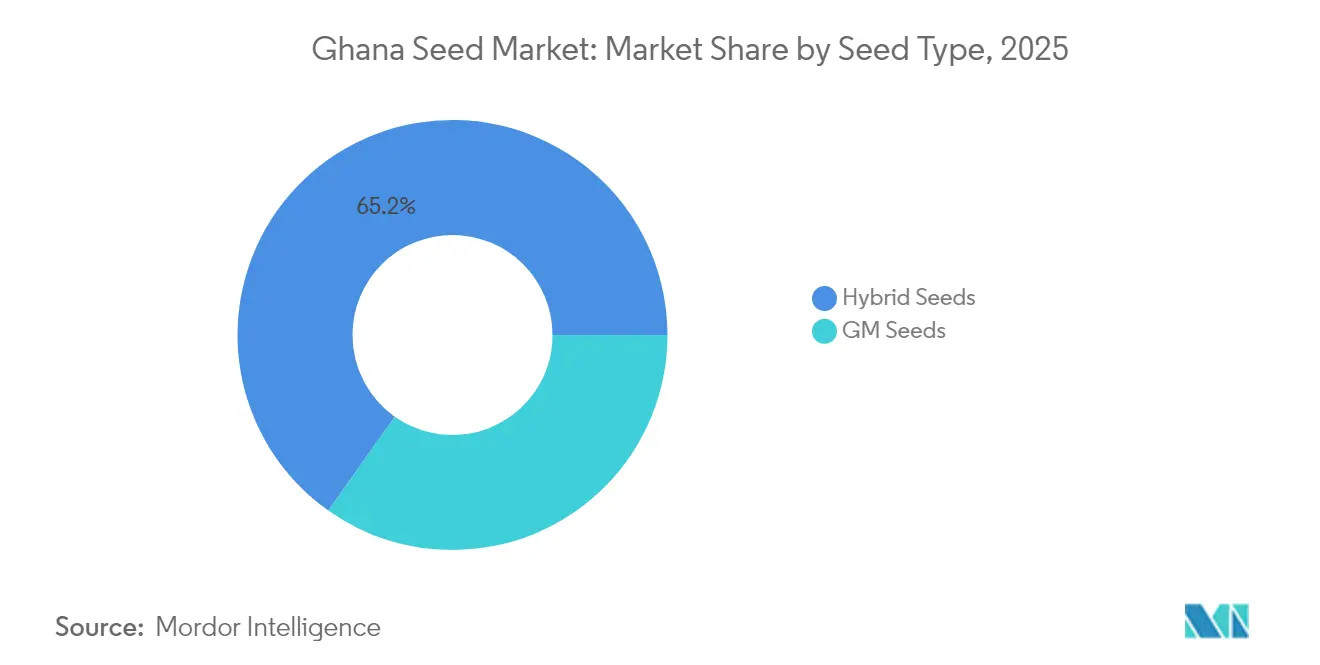

- By seed type, hybrid seeds held 65.20% of Ghana seed market share in 2025, while GM (Genetically Modified) seed is projected to accelerate at a 9.27% CAGR through 2031.

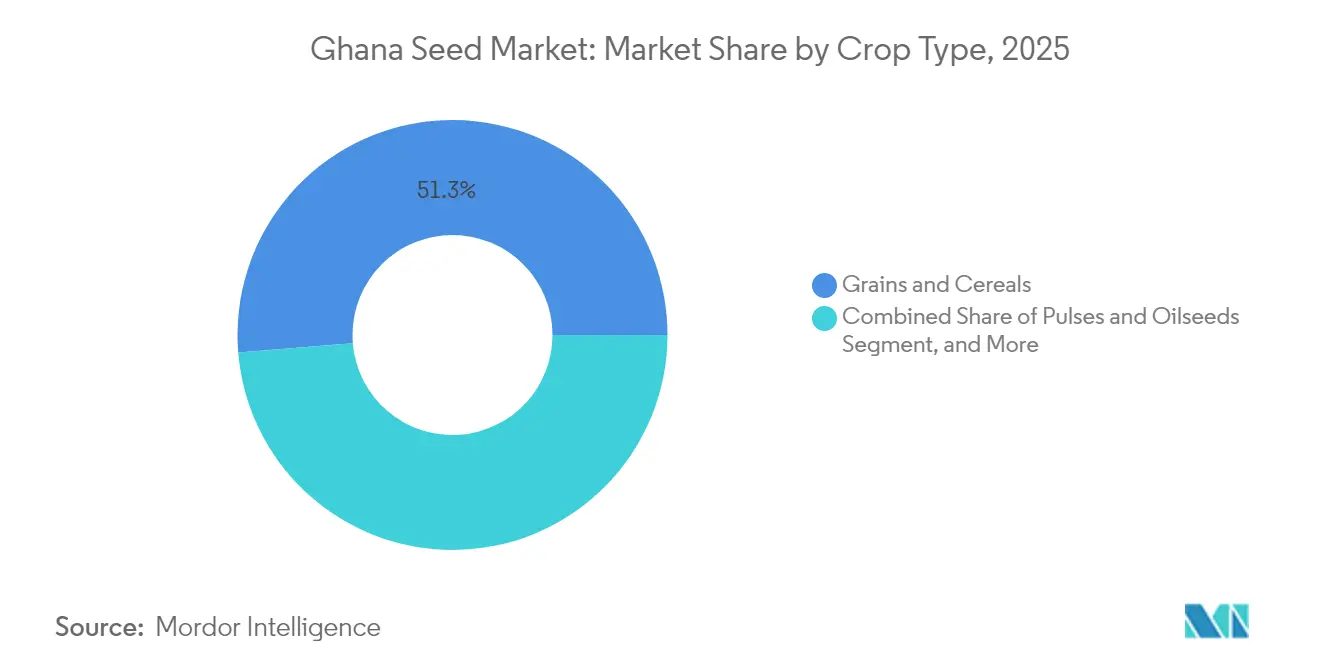

- By crop type, grains and cereals commanded 51.30% of Ghana seed market size in 2025, whereas fruits and vegetables are set to expand at an 8.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ghana Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government initiatives and agriculture policies | +2.8% | National, strongest in Northern and Upper Regions | Medium term (2–4 years) |

| Rising demand for improved crop varieties | +2.1% | Nationwide, with emphasis on the savanna and transitional zones | Long term (≥ 4 years) |

| Increasing awareness of seed quality | +1.4% | Rural communities through extension services | Short term (≤ 2 years) |

| Contract-farming models boosting certified seed uptake | +1.2% | Northern Ghana and Bono East | Medium term (2–4 years) |

| Climate-smart seed demand due to erratic rainfall | +1.8% | Highest in the drought-prone northern corridor | Long term (≥ 4 years) |

| Growth of ag-input e-commerce platforms | +0.9% | Urban and peri-urban markets expanding toward rural users | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Initiatives and Agriculture Policies

The Planting for Food and Jobs 2.0 program fundamentally reshapes seed demand dynamics by covering up to 30 % of certified seed costs for smallholder farmers, directly expanding formal market penetration beyond traditional commercial farming segments. The Ghana Agricultural Investment Plan earmarks sizeable capital for seed multiplication and promotes private participation, ensuring scale-up capacity beyond public research stations. World Bank financing further channels funds into digital advisory services, tying government support to data-driven agronomy. These coordinated policies collectively reshape demand by backing affordability, access, and technical adoption, though inefficiencies in input delivery could blunt impact.

Rising Demand for Improved Crop Varieties

Maize yields on smallholder plots hover below 2 metric tons per hectare, yet research confirms that modern hybrids can push output to 6 metric tons, supplying a 40–60% lift over local seed. Drought-tolerant maize lines like TZEE Y POP STR QPM and EVDT W 99 STR QPM yield up to 52% more grain, creating a compelling economic incentive to adopt certified seed. The resulting profitability cascades into higher market participation, with studies showing a 150% jump in farm income where drought-tolerant varieties are used. Farmer preference surveys consistently rank early maturity and drought-tolerance as top selection criteria, shaping breeding pipelines toward stress-resilient genetics.

Increasing Awareness of Seed Quality

More than 120 trained seed inspectors executed radio campaigns that reached 1.2 million farmers in 2024, boosting recognition of certification labels and germination standards [3]Source: Publications WASET, “Farmers’ Awareness of Planting for Food and Jobs Programme in Ghana,” publications.waset.org . The Ghana Standards Authority sets benchmarks that reinforce trust in formal channels, and participatory field days under Climate Research for Africa (AICCRA) expose growers to side-by-side plots that visually demonstrate performance differences. Although electronic agriculture services lag other pillars in awareness, field-based learning continues to pull demand toward quality-assured seed.

Contract-Farming Models Boosting Certified Seed Uptake

Brewer-led sorghum out-grower programs now link 25,000 smallholders to guaranteed markets and mandate certified seed, aligning risk sharing across the chain. These contracts embed financing for tractor services and extension support, strengthening seed performance and ensuring offtake security. Pioneer hybrids pushed through such schemes show pronounced yield gains, sparking spillover adoption among neighboring non-contract growers. However, the model's success depends on maintaining reliable off-taker relationships and ensuring contract terms remain economically attractive to smallholder participants.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited access to finance and technology | −2.3% | Highest in Northern and Upper Regions | Long term (≥ 4 years) |

| High seed production cost | −1.8% | Nationwide, affecting local and imported pricing | Medium term (2–4 years) |

| Counterfeit seed circulation from weak enforcement | −1.5% | Informal channels across rural markets | Short term (≤ 2 years) |

| Soil-nutrient decline reducing seed performance | −1.2% | Intensively cultivated southern and middle belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Access To Finance and Technology

Only 18% of growers qualify for formal bank credit, and modern hybrid seed can cost five times as much as traditional grain saved from the previous harvest. Loan aversion stems from collateral gaps and risk perceptions, pushing farmers toward informal lenders with punitive terms. Digital finance could close part of the gap, but smartphone penetration and data coverage remain uneven, stalling uptake. The digital divide compounds these challenges, with limited smartphone penetration and internet connectivity in rural areas restricting access to digital financial services and agricultural information platforms that could facilitate seed purchases.

Counterfeit Seed Circulation from Weak Enforcement

Seed Inspection Division raids seized 280 metric tons of fraudulent maize seed in 2024, signaling extensive leakage in informal trade channels. Counterfeit shipments erode farmer trust, cause crop failures, and create a drag on certified sales even as demand rises. Implementation gaps under the Plants and Fertiliser Act continue to hamper comprehensive surveillance, particularly in remote districts. Counterfeit seed circulation disproportionately affects resource-constrained farmers who seek lower-cost alternatives, creating a vicious cycle where those most needing productivity improvements face the highest risk of seed-related crop failures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Seed Type: Hybrid Leadership Faces Biotech Challenge

Hybrid seeds captured 65.20% of the Ghana seed market share in 2025 by virtue of decades-long extension and distributor familiarity. Within the Ghana seed market size, GM (Genetically Modified) seeds are projected to grow at a 9.27% CAGR through 2031, following the landmark release of pod-borer-resistant cowpea.

Farmer sentiment now weighs yield upside against perceived biosafety, and early field data show potential yield doubling with lower insecticide costs, tilting the calculus toward biotech acceptance. Regulatory clarity from the Ghana Biosafety Authority and public demonstrations will be decisive in broadening GM (Genetically Modified) penetration. Meanwhile, open-pollinated varieties persist among resource-limited households that prefer seed saving but face relative declines as productivity pressures mount.

By Crop Type: Cereals Dominance Meets Vegetable Upswing

Grains and cereals held a 51.30% share of the Ghana seed market size in 2025, anchored by maize’s staple status and continuous government support programs. The Ghana seed market for cereals grows steadily on the back of food-security imperatives and established milling capacity.

Conversely, fruit and vegetable seed demand is advancing at an 8.61% CAGR, propelled by urban dietary shifts and export opportunities. East-West Seed’s farmer training work underscores rising professionalism in high-value horticulture. Pulse and oilseed segments gain incrementally through nitrogen-fixation benefits and brewer-driven sorghum programs, while fodder and root crops target niche feed and processing outlets.

Geography Analysis

Northern Ghana positions itself as the fastest-moving territory within the Ghana seed market, catalyzed by climate stress, donor attention, and policy incentives that collectively heighten uptake of drought-tolerant maize and pest-resistant cowpea. Demonstrations under 31 tech parks have drawn 390,000 farmers and reported significant increases in yield gains, directly lifting regional demand for certified seed. Infrastructure deficits persist, yet the One Village One Dam scheme and improved feeder roads are progressively easing last-mile logistics.

Southern Ghana, particularly the Ashanti and Eastern regions, retains the largest share of the Ghanaian seed market size, owing to its higher purchasing power, dense dealer networks, and proximity to milling and poultry industries that consume maize output. Farmers here tend to favor early-maturing hybrids to accommodate two cropping cycles per year, leading to repeat seed purchases. Vegetable seed sales also spike in peri-urban belts where consumers diversify diets and traders target regional export channels.

The coastal and transitional zones form an intermediate band where diverse ecosystems support both cereal and horticultural growth. The adoption of quality protein maize hybrids remains strongest in the forest-savanna transition, driven by active extension and demand from school feeding programs. However, nutrient depletion in intensively cultivated pockets threatens yield sustainability, signaling an opportunity for integrated soil-seed packages that bundle fertilizer advice with high-response genetics.

Competitive Landscape

Ghana's seed market remains moderately concentrated, with Seed Co. Limited, Syngenta AG, Rijk Zwaan Zaadteelt en Zaadhandel B.V., East-West Seed International Ltd., and M&B Seeds Company Limited.

Technology intensity is the new battleground. Multinationals invest in AI breeding, on-farm data capture, and drone-based phenotyping to compress product-development cycles. Concurrently, digital platforms such as AgroCenta insert themselves between producers and growers, offering data analytics that feed back into breeding priorities. Compliance costs linked to export phytosanitary Certification favor capital-rich incumbents, yet whitespace persists in climate-smart niches, niche vegetable lines, and contract-farming ecosystems.

Strategic moves illustrate these dynamics. In March 2025, Bayer opened a maize seed facility designed to strengthen regional supply chains and enhance seed quality control, with a specific capacity earmarked for Ghana. Syngenta’s AI collaboration aims to decode complex genetics faster, giving it a head start on stacked traits. Local partnerships, such as those between CSIR-CRI and Arima Farms, working on wheat seed quality, showcase domestic innovation that could help reduce dependence on imports.

Ghana Seed Industry Leaders

Seed Co. Limited

Syngenta AG

Rijk Zwaan Zaadteelt en Zaadhandel B.V.

M&B Seeds Company Limited

East-West Seed International Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The World Bank approved USD 125.94 million in additional financing for the West Africa Food System Resilience Program to help Ghana recover from climate-related agricultural losses and enhance food security. The funding supports digital advisory services and sustainable intensification of crop production, including improved seed varieties.

- March 2025: Bayer launched a cutting-edge maize seed facility aimed at transforming African food security, with a specific focus on enhancing seed quality and production capacity across the continent, including Ghana. This facility represents a significant investment in local seed production infrastructure and technology transfer to support African agricultural development.

- July 2024: Ghana commercialized its first GM crop, the pod-borer-resistant cowpea, following clearance from the Biosafety Authority.

Ghana Seed Market Report Scope

A seed is the ripened fertilized ovule of a flowering plant containing an embryo and is capable of germination to produce a new plant. The Ghana Seeds Market is Segmented by Type (Non-GM/Hybrid Seeds, GM Seeds, and Open-pollinated Varieties) and Crop Type (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, and Other Crop Types). The report offers market size and forecast in terms of value (USD) and volume (Metric Tons) for the above segments.

Seed Type

| Hybrid Seeds |

| GM Seeds |

| Open-pollinated Varieties (OPVs) |

Crop Type

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Other Crop Types |

| Seed Type | Hybrid Seeds |

| GM Seeds | |

| Open-pollinated Varieties (OPVs) | |

| Crop Type | Grains and Cereals |

| Pulses and Oilseeds | |

| Fruits and Vegetables | |

| Other Crop Types |

Key Questions Answered in the Report

What is the current value of the Morocco seed market?

The Morocco seed market size stands at USD 125.45 million in 2026 and is projected to reach USD 192.95 million by 2031.

Which segment grows fastest through 2031?

GM seed shows the highest 9.27% CAGR, although actual sales remain modest until regulatory clarity improves.

How important are vegetables to overall seed demand?

Vegetables and cotton account for 37.65% of 2025 revenue, driven by tomato exports to the European Union.

Why is drought-tolerant seed critical for Moroccan farmers?

The 2024 drought cut cereal output 43%, so varieties that stabilize yields in water-stressed fields reduce income risk.

Page last updated on: