Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

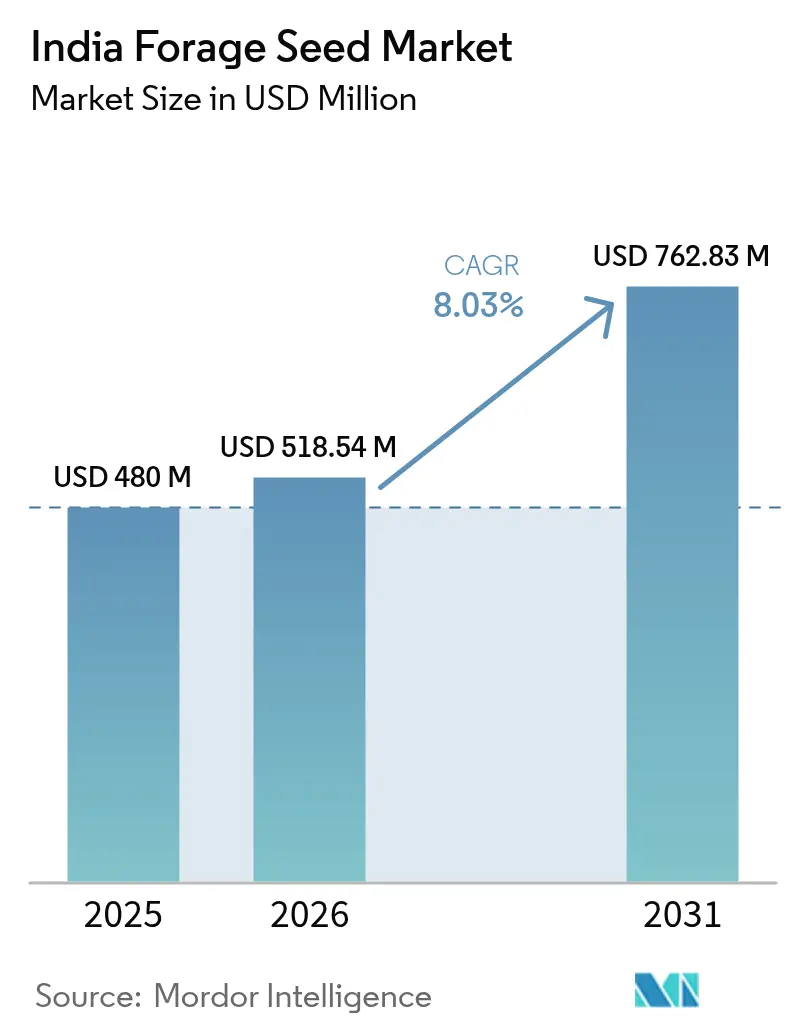

| Base Year Market Size (2025) | USD 480.0 Million |

| Market Size (2026) | USD 518.54 Million |

| Market Size (2031) | USD 762.83 Million |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Forage Seed Market Analysis by Mordor Intelligence

The India forage seed market size is expected to grow from USD 480.0 million in 2025 to USD 518.54 million in 2026 and is forecast to reach USD 762.83 million by 2031 at 8.03% CAGR over 2026-2031. Robust livestock intensification, policy-led fodder security programs, and steady improvement in breeding technologies collectively push demand beyond cyclical feed trends. Rising disposable income sustains higher dairy and meat consumption, while digital seed distribution platforms compress transaction costs, improve varietal authenticity, and deepen reach into underserved rural districts. Technology-enabled hybrids dominate planting decisions, yet open-pollinated varieties expand quickly among price-sensitive smallholders seeking cost relief without sacrificing productivity. Government intervention through the National Livestock Mission and Animal Husbandry Infrastructure Development Fund creates market conditions that favor technology adoption over traditional practices. The allocation of USD 1.8 billion (INR 15,000 crore) for livestock infrastructure development through 2025-26 specifically targets fodder production and seed distribution systems. Regional growth corridors emerge in Punjab, Haryana, and Uttar Pradesh because of cooperative dairy infrastructure. Maharashtra and Gujarat post the fastest acreage gains as commercial forage cultivation aligns with progressive irrigation practices.

Key Report Takeaways

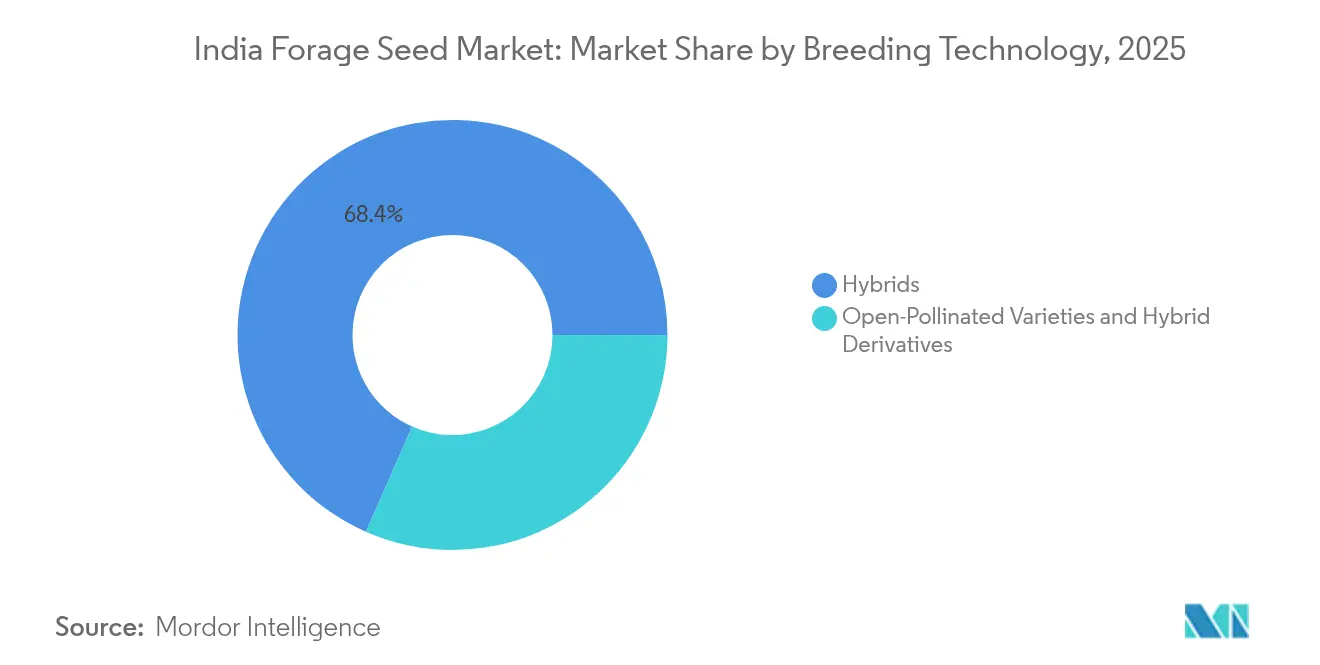

- By breeding technology, hybrids led with 68.40% of the India forage seed market share in 2025, while open-pollinated varieties and hybrid derivatives are forecast to expand at a 10.35% CAGR through 2031.

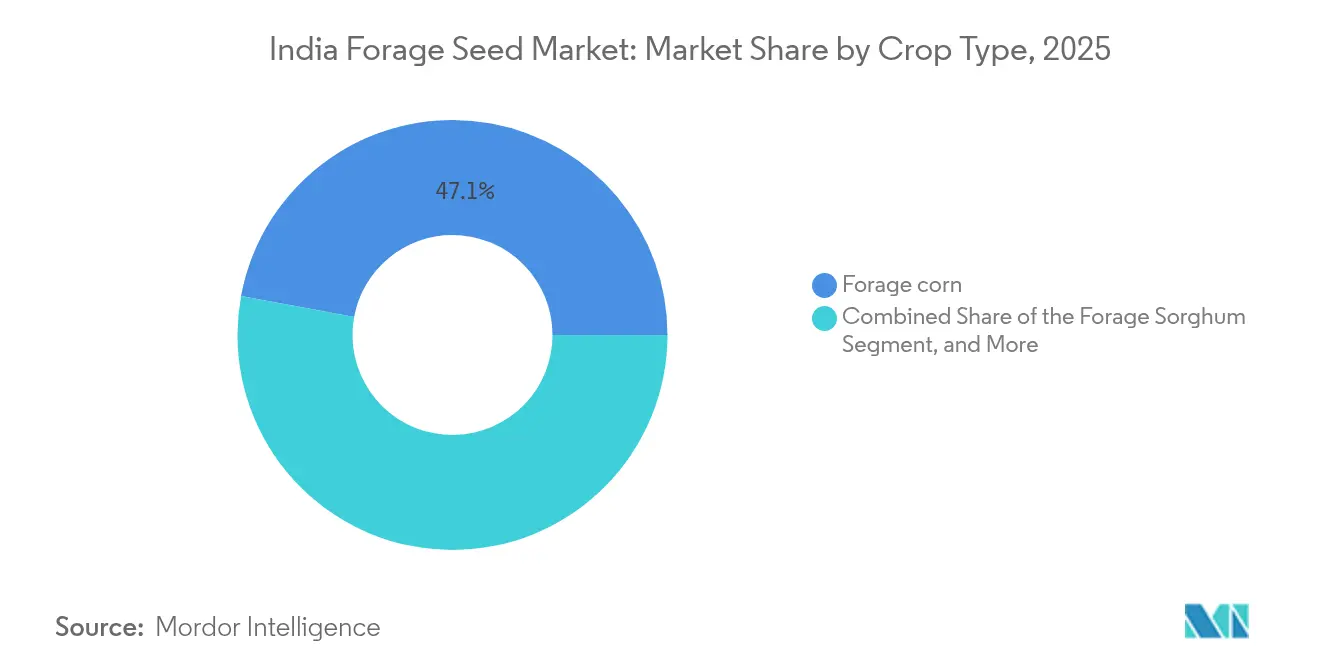

- By crop, forage corn accounted for a 47.10% share of the India forage seed market size in 2025, and forage sorghum posted the fastest segment growth, advancing at an 11.02% CAGR between 2026 and 2031.

- The forage seed market in India is moderately fragmented, with key players including Advanta Seeds International, Corteva Agriscience, Nuziveedu Seeds Limited, Mangalam Seeds Ltd, and Foragen Seeds Pvt Ltd.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Forage Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing livestock population | 2.1% | National, concentrated in Punjab, Haryana, Uttar Pradesh, and Rajasthan | Medium term (2-4 years) |

| Rising demand for dairy and meat products | 1.8% | National, with early gains in Gujarat, Maharashtra, and Karnataka | Medium term (2-4 years) |

| Advancements in forage-crop genetics | 1.5% | National, spill-over to marginal farming regions | Long term (≥ 4 years) |

| Government fodder-security schemes | 1.4% | National, targeted support in drought-prone regions | Short term (≤ 2 years) |

| Digitization of seed distribution networks | 0.9% | National, accelerated adoption in tech-forward states | Short term (≤ 2 years) |

| Climate-resilient forage varieties uptake | 1.2% | National, concentrated in water-stressed regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Livestock Population

India’s cattle herd climbs to 307.5 million head in 2025 as sustained animal health programs improve calving rates, lifting daily dry-matter requirements and enlarging the Indian forage seed market [1]Source: U.S. Department of Agriculture, “India: Livestock and Products Semi-annual,” usda.gov. Each additional dairy animal requires approximately 15 kg of dry matter daily, creating an immediate demand for multi-cut sorghum and legume mixes that balance energy and protein needs. Uttar Pradesh alone contributes 16.21% of national milk output, forming a concentrated demand hub for certified forage seed [2]Source: Ministry of Fisheries, Animal Husbandry and Dairying, “National Livestock Mission,” pib.gov.in. Breed-improvement grants within the National Livestock Mission stimulate on-farm fodder plots, further embedding quality seed use. The National Livestock Mission's focus on breed development and feed availability directly supports this expansion through certified fodder seed production initiatives.

Rising Demand for Dairy and Meat Products

Per-capita milk intake is projected to reach 550 g per day by 2030, underpinned by income growth and health awareness. Fluid milk alone is forecast to reach 91 million metric tons in 2025, forcing dairies to intensify their feeding programs, which hinge on high-digestibility forages. The shift toward processed dairy products, including cheese and yogurt, requires higher milk quality standards that depend on superior forage nutrition. Meanwhile, factory-use milk climbs toward 125.5 million metric tons as cheese and yogurt lines expand, spurring uptake of legume-rich silage blends for superior butterfat levels[3]Source: OECD-FAO, “OECD-FAO Agricultural Outlook 2020-2029,” oecd-ilibrary.org. Urban meat consumption also rises, particularly broiler demand, encouraging growers to incorporate fresh forage to enhance carcass quality. This trajectory necessitates systematic improvements in forage quality and availability to support the sustainable productivity of grains.

Advancements in Forage-Crop Genetics

The Indian Council of Agricultural Research released 69 new forage cultivars in 2024, including multi-cut sorghum capable of 22 metric tons/ha green matter, sharply above legacy varieties. Genome-edited rice approvals set a precedent that could hasten Clustered regularly interspaced short palindromic repeats (CRISPR) based forage sorghum and pearl millet pipelines, targeting traits such as drought resilience and higher crude protein. Hybrid breeding programs focus on heterosis exploitation to achieve 25-40% yield advantages over open-pollinated varieties, with companies like Advanta and Mahyco investing in proprietary germplasm development. Molecular marker-assisted selection accelerates variety development timelines from 10-12 years to 6-8 years, enabling faster response to emerging market needs and climate challenges.

Government Fodder-Security Schemes

The National Livestock Mission earmarks USD 204 million (INR 1,702 crore) for sustainable feed and animal husbandry, including 50% capital grants for fodder-seed units. Entrepreneur subsidies have already approved 145 projects in Uttar Pradesh, adding 28,000 MT annual fodder capacity. Budget 2025-26 established a National Mission on High-Yielding Seeds, specifically aimed at enhancing seed research and availability. This initiative also increased Kisan Credit Card limits from USD 3,410 to USD 5,680 (INR 3 lakh to Rs 5 lakh), thereby benefiting dairy farmers' access to quality inputs. The Digital Agriculture Mission further invests USD 339 million (INR 2,817 crore) in farmer registries, enabling the precise allocation of subsidized seed packets.

Digitization of Seed Distribution Networks

Indian Farmers Fertilizer Cooperative Limited (IFFCO) e-Bazar processed approximately USD 282 million (INR 2,350 crore) in agri-input sales during the 2024-2025 fiscal year, shipping orders to 27,000 postal codes and proving the viability of rural e-commerce. Blockchain pilots trace seed lots from breeder plots to farm gates, reducing adulteration and cutting middle-layer costs that once dampened smallholder buying power. Common Services Centre (CSC) and IFFCO (Indian Farmers Fertilizer Cooperative Limited) signed a Memorandum of Understanding (MOU) to supply fertilizers and certified seeds to 10,000 Farmer-Producer Organizations, thereby widening the last-mile reach and reducing procurement costs for smallholders.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition with food crops for acreage | -1.8% | National, acute in Punjab, Haryana, and western Uttar Pradesh | Medium term (2-4 years) |

| High input costs of hybrid seeds | -1.2% | National, pronounced impact on smallholder farmers | Short term (≤ 2 years) |

| Fragmented last-mile cold-chain for seeds | -0.9% | National, severe in eastern and northeastern states | Medium term (2-4 years) |

| Low seed-replacement rate among smallholders | -1.1% | National, concentrated in rain-fed farming regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition with Food Crops for Acreage

Minimum Support Price (MSP) incentives keep farmers centered on rice and wheat together, they captured more than 60% of field acreage in 2024, crowding out dedicated fodder plots. Summer maize for silage shows attractive margins in Punjab, yet groundwater extraction surpasses recharge by 10.66 MAF (Million Acre Feet), jeopardizing long-term viability. Ethanol blending targets create additional competition as sugarcane, rice, and maize are diverted for fuel production, with government restrictions on sugar and rice exports due to lower yields affecting land allocation decisions. The estimated cost of guaranteeing MSP (Minimum Support Price) across all crops at USD 2.38 billion (INR 21,000 crore ) suggests limited fiscal space for expanding support to forage crops in the near term.

High Input Costs of Hybrid Seeds

Hybrid corn seed averages USD 5.8 per kg against USD 2.1 per kg for open-pollinated types, a steep premium for marginal growers. The fertilizer subsidy structure's imbalance, with excessive nitrogen application and under-application of phosphorus and potassium, increases overall input costs while reducing soil health and crop productivity. Post-harvest losses of USD 18.5 billion (INR 1.53 trillion) annually indicate systemic inefficiencies that compound input cost pressures. The blockchain-based seed supply chain analysis reveals that intermediaries' involvement increases costs and reduces transparency, particularly affecting small farmers' access to quality seeds. Regional variations show that lease rates in Punjab have risen significantly, with farmers cultivating leased land facing additional cost pressures that limit their ability to invest in premium forage seed varieties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Drive Premium Market Expansion

Hybrid varieties contributed 68.40% of the India forage seed market share in 2025. Robust heterosis yields an additional 25-40% biomass, providing a decisive edge for professional dairies optimizing feed conversion. Strong performance secures repeated annual purchases, ensuring the India forage seed market size for hybrids climbs at the fastest-growing segment. Most demand concentrates in Punjab, Haryana, and Gujarat, where irrigation lets farmers exploit multi-cut cycles for hybrid Napier and forage corn. Firms such as Bayer and Syngenta complement seed with herbicide packages that simplify weed management, embedding hybrid loyalty.

Open-pollinated varieties and hybrid derivatives captured the remainder and are now exhibiting the swiftest expansion at a 10.35% CAGR through 2031. Seed-saving potential resonates with resource-constrained farmers in rain-fed areas, extending utility across seasons and reducing cash expenditures. The Indian Council of Agricultural Research (ICAR) pipeline supplies affordable, open-pollinated lines with protein gains of 1-2 percentage points, helping to close nutrition gaps in backyard dairies. Coupled with community seed banks, these varieties expand formal market penetration and balance access to technology across farm segments.

By Crop: Forage Corn Maintains Leadership Through Versatility

Forage corn held 47.10% of the India forage seed market share in 2025, reflecting its dual role in silage and green chop systems. The segment grows at an 7.68% CAGR, ensuring it remains the anchor crop for the India forage seed market size to 2031. High starch levels translate into higher milk output, drawing strong adoption among cooperatives that pay on fat content. Processing firms subsidize silage bunkers, which lock in corn’s advantage by safeguarding feed quality year-round.

Forage sorghum advances fastest at 11.02% CAGR as climate stress elevates water-efficient choices. Multi-cut and brown-midrib traits improve digestibility, inviting farmers in Maharashtra and Rajasthan to shift acreage. Alfalfa keeps modest expansion because of its protein boost and nitrogen fixation, embedded within organic and mixed-farming systems. Pearl millet and oats cater to niche windows such as arid summer feed gaps and winter fodder in temperate hill zones, collectively representing a flexible supplement that diversifies the India forage seeds market.

Geography Analysis

Northern India dominates demand with Punjab and Haryana supplying organized dairies that require consistent green fodder for high-yield cattle. Irrigated fields, mechanized harvesters, and cooperative milk collection underpin hybrid acceptance rates near 80% of acreage. Uttar Pradesh hosts the largest livestock headcount and, despite variable irrigation, is propelled by district-level fodder depots that bundle seed with agronomic advice.

Western growth corridors in Maharashtra and Gujarat expand acreage at double-digit rates. Gujarat’s cooperative model offers bonus payments for high-protein milk, which motivates farmers to adopt improved forage corn and sorghum. Micro-irrigation and reclaimed groundwater sustain year-round production. Maharashtra’s sugarcane belt incorporates forage crops in rotation, leveraging residual soil fertility to temper production cost. Strong local seed multipliers keep supply reliable and bolster the India forage seed market.

Eastern and northeastern states remain nascent yet promising. High rainfall supports tropical grasses, but cold-chain gaps limit hybrid seed viability. Government logistical grants target 500 village seed stores by 2027, anticipated to lift viability and accelerate adoption. Demonstrations in Assam show 35% milk yield gains from hybrid maize silage, signaling potential once infrastructure matures. The region’s transformation could add a fresh USD 75 million to the India forage seed market over the next five years.

Competitive Landscape

The India forage seed market remains moderately fragmented, with the top five players, including Advanta Seeds International, Corteva Agriscience, Nuziveedu Seeds Limited, Mangalam Seeds Ltd, and Foragen Seeds Pvt Ltd. Market positions hinge on genetic pipelines, regionalized extension teams, and value-added treatments such as biodegradable micronutrient coatings.

Strategic thrusts reflect a pivot toward collaborative R&D and digital outreach. Corteva’s non-GMO (Genetically Modified Organism) hybrid wheat platform, although not applicable to forage, showcases breeder innovation that can be applied to feed cereals, underscoring competitive differentiation. Royal Barenbrug Group and its domestic peers are racing to commercialize climate-ready cultivars, seeking a first-mover advantage in water-stressed zones. Seed firms also partner with fintech companies to integrate credit solutions, thereby lowering the entry barriers for small farmers.

Mid-tier and regional companies exploit localized knowledge, tailoring varietal mixes to micro-climates and cultivating dealer loyalty through agronomic training. Import competition is minimal due to phytosanitary hurdles, yet multinational know-how permeates through joint ventures. Overall, price competition yields ground to performance-based marketing as farmers weigh total feed economics against upfront seed costs.

India Forage Seed Industry Leaders

Corteva Agriscience

Nuziveedu Seeds Limited

Mangalam Seeds Ltd

Foragen Seeds Pvt Ltd

Advanta Seeds International (UPL Limited)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Rasi Seeds, the Indian Council of Agricultural Research (ICAR), and the Indian Grassland and Fodder Research Institute (IGFRI) have signed a Memorandum of Understanding (MOU) to enhance the production and availability of high-quality forage seeds for India's dairy sector. The collaboration aims to enhance livestock nutrition and increase milk productivity through improved forage cultivation.

- August 2024: The Indian Council of Agricultural Research developed 109 seed varieties, including 7 forage varieties, which Prime Minister Narendra Modi introduced. These varieties are high-yielding, climate-resilient, and biofortified, aimed at increasing agricultural productivity and farmer income.

- June 2023: Advanta and Nurture Farm have teamed up to introduce the Nutrifeed Germination Scheme. This initiative is designed to shield farmers from financial setbacks stemming from the germination failures of forage crops, such as millet and sorghum. Under the scheme, seeds that don't germinate within 15 days of sowing are covered, bolstering farmers' resilience against environmental challenges. Beyond financial protection, the scheme champions sustainable farming practices and provides dairy farmers with access to high-yield, nutritious fodder.

India Forage Seed Market Report Scope

Forage seeds are seeds used to grow crops specifically cultivated as animal feed, such as grasses and legumes, to provide fresh fodder, hay, or silage for livestock nutrition. The India Forage Seed Market Report is segmented by Breeding Technology (Hybrids [Non-Transgenic Hybrids and Transgenic Hybrids], Open-Pollinated Varieties and Hybrid Derivatives) and by Crop (Alfalfa, Forage Corn, Forage Sorghum, and Other Forage Crops). The market forecasts are provided in terms of value (USD).

By Breeding Technology

| Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide-Tolerant Hybrids | |

| Other Traits | ||

| Open-Pollinated Varieties and Hybrid Derivatives | ||

By Crop

| Alfalfa |

| Forage Corn |

| Forage Sorghum |

| Other Forage Crops |

| By Breeding Technology | Hybrids | Non-Transgenic Hybrids | |

| Transgenic Hybrids | Herbicide-Tolerant Hybrids | ||

| Other Traits | |||

| Open-Pollinated Varieties and Hybrid Derivatives | |||

| By Crop | Alfalfa | ||

| Forage Corn | |||

| Forage Sorghum | |||

| Other Forage Crops | |||

Key Questions Answered in the Report

What is the current value of the India forage seeds market?

The India forage seeds market is valued at USD 518.54 million in 2026.

How fast is the market projected to grow?

It is projected to post an 8.03% CAGR and reach USD 762.83 million by 2031.

Which crop segment leads demand?

Forage corn holds 47.10% of 2025 sales because of its silage versatility.

How do hybrids compare with open-pollinated varieties?

Hybrids deliver 25-40% higher biomass but cost more, open-pollinated varieties grow faster among price-sensitive farmers.

Page last updated on: