India Industrial Sensors And Transmitters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

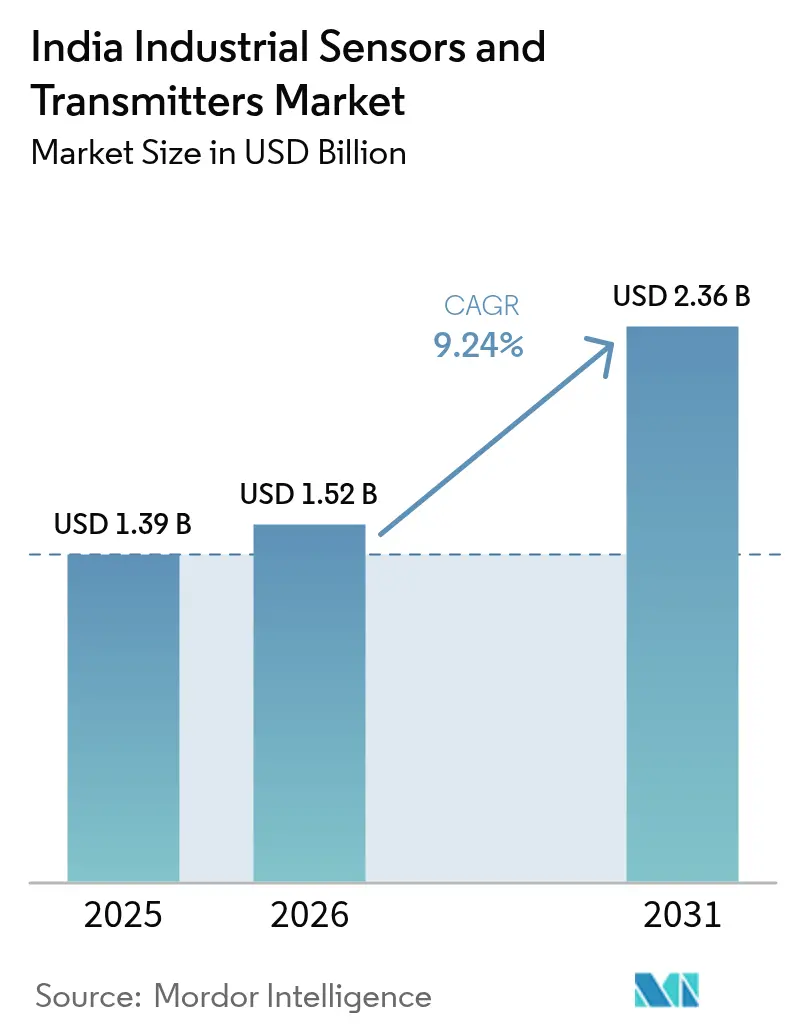

| Base Year Market Size (2025) | USD 1.39 Billion |

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 9.24% CAGR |

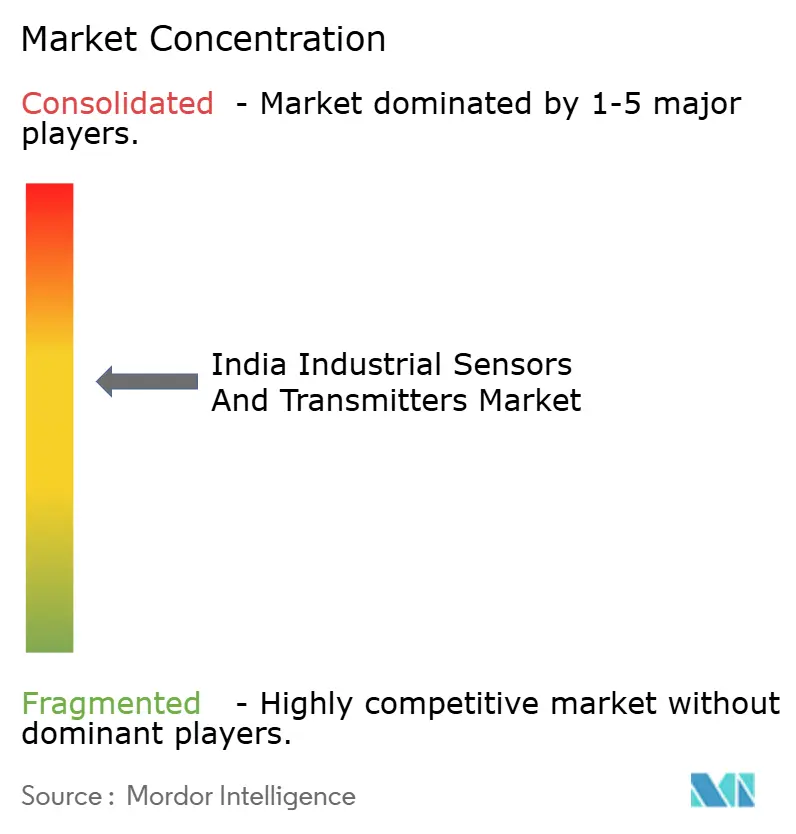

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Industrial Sensors And Transmitters Market Analysis by Mordor Intelligence

The India industrial sensors and transmitters market size is expected to grow from USD 1.39 billion in 2025 to USD 1.52 billion in 2026 and is forecast to reach USD 2.36 billion by 2031 at 9.24% CAGR over 2026-2031. This advance mirrors India’s accelerated transition toward digitalized, data-driven production environments, spurred by government incentive programs, widening Industry 4.0 adoption, and greater demand for predictive maintenance solutions. Large capital commitments from multinational firms, such as Schneider Electric’s INR 3,200 crore (USD 384 million) manufacturing expansion, point to deepening localization strategies that reduce import exposure and shorten delivery cycles. Meanwhile, stricter quality regulations in pharmaceuticals and food processing, combined with energy-efficiency mandates for heavy industry, expand the addressable base for pressure, flow, and temperature sensing solutions. Persistent semiconductor import reliance, however, continues to expose the India industrial sensors and transmitters market to global supply disruptions, potentially elongating lead times and inflating costs. Growing data-center capacity in key metros further amplifies demand for precision HVAC sensors capable of meeting stringent uptime requirements, reinforcing momentum across specialty sensor categories.

Key Report Takeaways

- By sensor type, pressure sensors held 27.12% India industrial sensors and transmitters market share in 2025, while vibration and condition-monitoring units are set to post an 10.95% CAGR through 2031.

- By end-user, oil and gas retained a 26.15% share of the India industrial sensors and transmitters market size in 2025, but life sciences is projected to expand at a 11.02% CAGR over the same horizon.

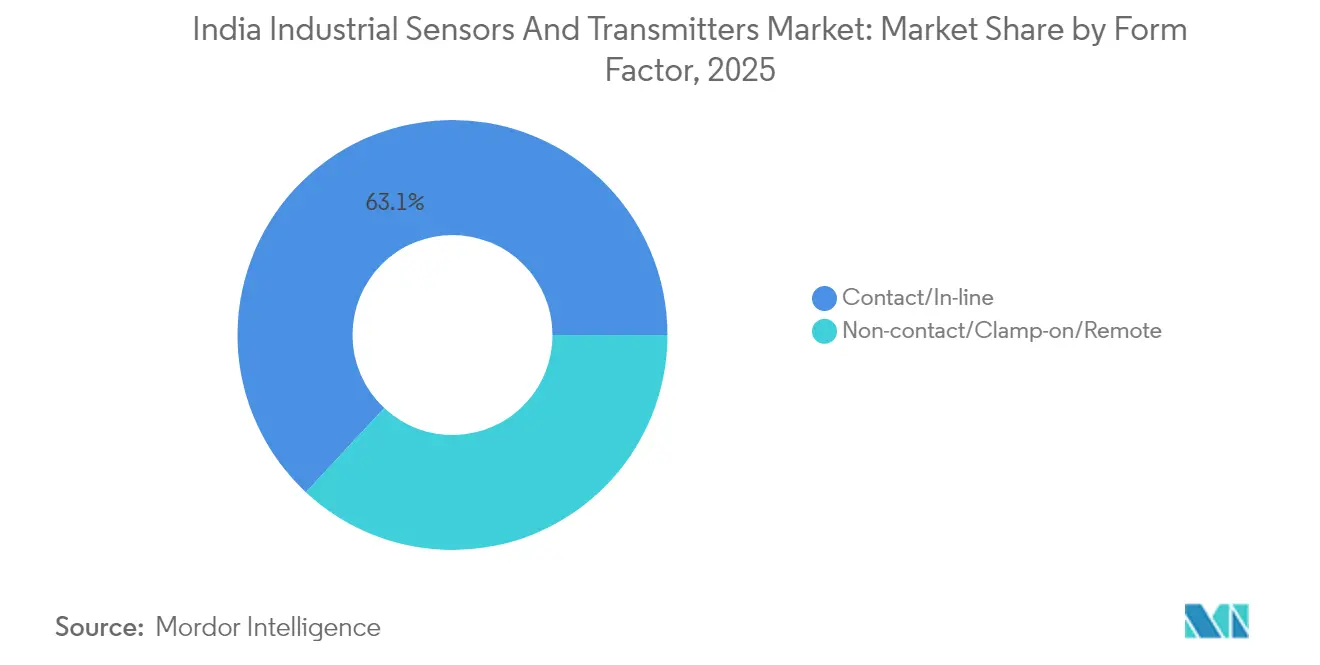

- By form factor, contact sensors accounted for 63.05% of the 2025 India industrial sensors and transmitters market size; non-contact solutions are on track for a 9.88% CAGR to 2031.

- By communication technology, wired systems generated 50.95% revenue in 2025 of the India industrial sensors and transmitters market, whereas wireless platforms are forecast to grow at 10.22% CAGR through 2031.

- By geography, West India led with 38.10% market share of the India industrial sensors and transmitters market in 2025, yet South India is expected to record the fastest 10.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Industrial Sensors And Transmitters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government "Make-in-India" and PLI schemes catalyzing smart factories | +2.1% | National, with early gains in West India, South India | Medium term (2-4 years) |

| Rising Industry 4.0 adoption across discrete manufacturing | +1.8% | West India, South India core, spill-over to North India | Short term (≤ 2 years) |

| Quality-centric regulations in pharma and Food and Beverage sectors | +1.4% | National, concentrated in Maharashtra, Karnataka, Telangana | Long term (≥ 4 years) |

| Energy-efficiency mandates for utilities and process industries | +1.2% | National, with early gains in industrial states | Medium term (2-4 years) |

| Data-center boom demanding precision HVAC sensors | +0.9% | South India, West India, North India metros | Short term (≤ 2 years) |

| Localization of sensor component supply chains | +0.7% | National, manufacturing hub focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government “Make-in-India” and PLI Schemes Catalyzing Smart Factories

Performance-linked incentives worth INR 76,000 crore (USD 9.1 billion) reward manufacturers that demonstrate sustained capital expenditure and output growth, tilting sourcing decisions toward domestically produced sensor components.[1]Press Information Bureau, “Production Linked Incentive Scheme for Large Scale Electronics Manufacturing,” pib.gov.in Multinationals have responded by building vertically integrated plants that reduce logistics costs, compress lead times, and adapt product lines to Indian operating conditions. Larger domestic content also shields buyers in the India industrial sensors and transmitters market from exchange rate volatility. Over the medium term, a denser local vendor ecosystem is likely to compress price premiums for advanced smart sensors, further accelerating adoption across mid-tier manufacturers.

Rising Industry 4.0 Adoption Across Discrete Manufacturing

Automakers transitioning to electric vehicles, electronics assemblers optimizing line changeovers, and capital-goods makers deploying predictive analytics share a common need for real-time condition data. Factory leaders report up to 30% downtime reduction after embedding vibration, thermal, and power-quality sensors into production assets, which translates to notably higher throughput per square foot. Success stories such as Daifuku’s sensor-rich material-handling plant in Hyderabad catalyze copy-cat projects among Tier-2 suppliers keen to preserve OEM rankings. The India industrial sensors and transmitters market will therefore benefit from a virtuous loop: performance gains justify larger sensor budgets, and larger installations yield more data, which in turn feeds higher-value analytics services.

Quality-Centric Regulations in Pharma and Food and Beverage sectors

Revisions to GMP and FSSAI guidelines stipulate uninterrupted logging of pressure, temperature, and humidity conditions during drug formulation, packaging, and cold-chain transit.[2]Central Drug Standard Control Organization, “Good Manufacturing Practice Guidelines,” cdsco.gov.in Non-compliance risks plant shutdowns and export license suspensions, compelling manufacturers to migrate from manual batch checks to networked sensing platforms that feed audit-ready digital records. The India industrial sensors and transmitters market thus finds steady pull from compliance budgets even when capital allocations for broader automation remain tight. Moreover, successful adopters leverage the same sensor backbone to launch real-time process optimization projects, widening the technology’s payback narrative beyond mere regulatory insurance.

Energy-Efficiency Mandates for Utilities and Process Industries

The Perform, Achieve and Trade scheme sets plant-specific energy intensity targets and levies penalties for under-performance, making granular flow, pressure, and temperature measurements economically mandatory.[3]Bureau of Energy Efficiency, “Perform, Achieve and Trade Scheme Guidelines,” beeindia.gov.in Petrochemical complexes and steel mills installing multivariable transmitters and ultrasonic flow meters report double-digit megawatt-hour savings within two years of deployment, often surpassing target obligations. Energy savings certificates earned by over-achievers can be traded, providing an additional revenue stream that further sweetens sensor ROI calculations. The India industrial sensors and transmitters market, therefore, becomes integral to national energy-productivity goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for smart-sensor retrofits | -1.3% | National; acute in SME clusters | Short term (≤2 years) |

| Interoperability and legacy integration issues | -0.9% | National; mature industrial belts | Medium term (2-4 years) |

| Skilled instrumentation technician shortage | -0.7% | National; fast-growing industrial zones | Long term (≥4 years) |

| Semiconductor import dependence | -0.5% | National; supply chain vulnerability | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High CAPEX of Advanced Smart-Sensor Retrofits

Smart units with built-in diagnostics and wireless modules often cost triple the price of legacy counterparts, and comprehensive facility conversions can require USD 2–5 million in fresh outlays. SMEs with slim margins hesitate to lock capital into five-year payback horizons, delaying sizable orders that would otherwise lift the India industrial sensors and transmitters market. Government low-interest loans and accelerated depreciation allowances partially offset sticker shock, yet awareness of such schemes remains patchy outside tier-one industrial parks.

Interoperability and Legacy System Integration Issues

Plants that grew organically over decades usually host heterogeneous control architectures. Introducing Ethernet-based or wireless sensors demands protocol converters, bespoke firmware, and extended validation cycles that push integration costs 20-30% above hardware lists. System downtime during switchover further discourages aggressive timelines, softening near-term revenue prospects for the India industrial sensors and transmitters market. Vendor coalitions promoting open standards show promise, but real-world convergence is still several budget cycles away.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Pressure Sensors Lead Industrial Modernization

Pressure devices accounted for 27.12% of 2025 shipments, underscoring their foundational role in safe and efficient hydrocarbon processing, chemical synthesis, and power-generation boiler operations. The India industrial sensors and transmitters market size tied to pressure measurement is expected to compound at a steady clip as regulatory bodies enforce tighter safety margins in high-pressure pipelines. Manufacturers continue to widen portfolios with explosion-proof and differential configurations suited to the diverse viscosity and corrosiveness profiles seen in Indian refineries. Meanwhile, vibration and condition-monitoring sensors are set to post an 10.95% CAGR through 2031, propelled by maintenance digitization programs that aim to slash unplanned downtimes across automotive, cement, and steel plants. Suppliers that bundle sensors with predictive analytics dashboards secure annuity-style service revenue streams, strengthening overall value capture within the India industrial sensors and transmitters market.

Beyond the top two categories, temperature probes retain durable demand in pharma sterilization loops and dairy pasteurization lines where precise thermal control guards against batch spoilage. Flow sensors enjoy rising penetration in effluent treatment and desalination projects funded by municipal smart-water schemes. Level sensors migrate from discrete silo monitoring toward integrated inventory-management suites, providing ERP-ready feedstock visibility. Gas and humidity sensing extend from cleanrooms into next-generation data centers, where consistent air quality boosts server lifespan. Across all classes, OEMs increasingly push multi-parameter platforms that condense several sensing modalities into a single housing, lowering installation labor while expanding the India industrial sensors and transmitters market’s average selling price.

By End-user Industry: Oil and Gas Dominance Faces Life Sciences Challenge

Hydrocarbon value-chain participants commanded 26.15% of 2025 revenue, anchored by capital projects such as Indian Oil Corporation’s INR 24,000 crore (USD 2.88 billion) petrochemical expansion. Safety instrumentation ranging from SIL-rated pressure transmitters to combustible-gas detectors forms the bulk of oil-and-gas outlays, with environmental authorities mandating continuous emissions monitoring that further enlarges the India industrial sensors and transmitters market. Over the forecast period, however, pharma and biotech facilities are poised for an 11.02% CAGR, narrowing the share gap as vaccine and biologics plants scale GMP-compliant sensor grids spanning cold-chain storage, lyophilization chambers, and classified cleanrooms.

Utilities deploy smart metering and sub-station automation, driving uptake of power-quality transducers and fiber-optic temperature loops in transformers. Petrochemicals, chemicals, and fertilizers chase throughput optimization via multivariable sensors that monitor cross-linked reaction parameters. Food and beverage processors move beyond HACCP checklists, integrating cloud-linked sensors for real-time traceability from blending to packaging. Water and wastewater operators embrace clamp-on ultrasonic flow meters that eliminate service disruptions during tie-ins. Metals and mining companies adopt ruggedized vibration probes to anticipate drivetrain wear in conveyors and ball mills. Collectively, these verticals diversify the India industrial sensors and transmitters market, reducing over-reliance on any single commodity cycle.

By Form Factor/Installation: Contact Sensors Maintain Dominance Despite Remote Sensing Growth

Traditional in-line configurations represented 63.05% of 2025 shipments due to their proven accuracy, chemical compatibility, and body of calibration best practices. Pharma regulators and quality auditors continue to favor direct-contact thermocouples and diaphragm-sealed pressure transmitters, solidifying the segment’s baseline demand within the India industrial sensors and transmitters market. However, clamp-on and optical methods are growing at a 9.88% CAGR as brownfield operators seek minimal downtime installations. Ultrasonic flow meters that strap onto existing pipes allow capacity upgrades without hot-work permits, while infrared pyrometers find favor in steel rollers and glass furnaces where invasive probes are impractical.

Emerging non-contact platforms now feature self-powered energy harvesting and wireless backhaul, cutting both wiring and maintenance burdens. Pilot studies in dairy chilling plants show 15% faster deployment and 30% lower lifecycle costs compared with wired equivalents, validating the commercial thesis for remote sensing adoption. Yet harsh process conditions, abrasion, fouling, and high-pressure wash-downs still tilt many buyers toward contact devices, ensuring the India industrial sensors and transmitters market retains a healthy product mix over the forecast horizon.

By Communication Technology: Wired Systems Face Wireless Disruption

HART, MODBUS, and PROFIBUS networks delivered 50.95% of 2025 revenue because plant engineers prize deterministic performance and cyber-secure point-to-point topologies. The India industrial sensors and transmitters market size attributed to wired nodes will expand at a measured pace as Industrial Ethernet options such as PROFINET gain currency for high-bandwidth vision and robotics workloads. Operators appreciate Ethernet’s seamless handshake with cloud gateways, facilitating edge-to-cloud data harmonization without protocol converters.

Conversely, wireless shipments are accelerating at a 10.22% CAGR, catalyzed by retrofit friendliness in sprawling refineries, tank farms, and conveyor-heavy mines. ISA100.11a and WirelessHART now offer regulatory-grade reliability, earning acceptance in SIL-rated loops at gas-compression stations. Low-power wide-area networks like NB-IoT underpin battery-powered pressure nodes monitoring remote pipelines, slashing field inspection runs. Still, operational-technology cybersecurity frameworks must mature before wireless can fully erode wired incumbency, keeping the India industrial sensors and transmitters market finely balanced between both architectures.

Geography Analysis

West India generated 38.10% of 2025 revenue, anchored by dense automotive, petrochemical, and pharmaceutical corridors stretching from Pune to Vadodara. The India industrial sensors and transmitters market size in this region benefits from entrenched vendor ecosystems and port-enabled export logistics that shorten replenishment cycles. Multinationals leverage these strengths when allocating incremental capex, as noted by continuous production line upgrades at long-standing plants in the Chakan auto hub.

South India, posting an 10.76% forecast CAGR, has emerged as the nation’s fastest-growing locus for sensor deployment. Karnataka’s electronics clusters, Tamil Nadu’s expanding aerospace parks, and Telangana’s med-tech valley collectively pull advanced instrumentation demand upward. The knowledge-worker density around Bengaluru accelerates proof-of-concept pilots for wireless and AI-driven sensors, injecting innovation velocity into the India industrial sensors and transmitters market. Recent greenfield investments, including EBM-Papst’s fan-system plant and Daifuku’s material-handling facility, further cement the region’s momentum.

North India, East and Northeast, and Central India present sequential catch-up opportunities. Delhi-NCR’s metro expansion and smart-city pumps require distributed pressure and flow meters. Assam’s refinery capacity build-outs drive specialized explosion-proof sensor orders, while Jharkhand’s mineral extraction projects install ruggedized probes for conveyor vibration alerts. Collectively, these corridors will supply consistent incremental volumes, ensuring the India industrial sensors and transmitters market enjoys geographic risk diversification.

Competitive Landscape

Competition is moderate, with global majors and agile domestic firms vying for a customer base that values reliability, conformity to Indian standards, and price-performance balance. Schneider Electric, ABB, and Emerson have scaled local production to cut tariffs and qualify for PLI incentives, translating into quicker order-to-delivery cycles and controlled cost structures that reinforce brand loyalty. ABB’s threefold jump in data-center orders illustrates how specialization in high-growth verticals can outpace overall market velocity.[4]ABB India Limited, “ABB India Reports Strong Growth in Data Center Business,” abb.com

Most tier-one vendors are shifting from pure hardware plays toward solution stacks bundling gateways, analytics, and lifecycle services. Subscription-based monitoring arrangements convert lump-sum capex into predictable opex, attractive to customers navigating budget constraints. Domestic upstarts differentiate by customizing transmitters for India-specific ambient conditions at price points 15–20% below imported units, capturing opportunities in cost-sensitive municipal and SME projects. Nonetheless, the India industrial sensors and transmitters market remains technology-driven; firms that sustain R&D pipelines in diagnostic algorithms and chip-level integration will secure durable competitive moats.

Partnerships with systems integrators and cloud providers multiply channel reach. Schneider Electric’s tie-ups with hyperscale operators for pre-certified sensor-to-cloud reference designs illustrate cooperative ecosystems that reduce buyer integration pain. Fragmented aftermarket service networks remain a weakness; firms offering nationwide calibration and spares availability gain a decisive edge in maintenance-intensive sectors like oil and gas. Cyber-security accreditations are turning into a gating factor for refinery and pharma tenders, adding a new layer of differentiation within the India industrial sensors and transmitters market.

India Industrial Sensors And Transmitters Industry Leaders

ABB India Limited

Honeywell Automation India Limited

Siemens Limited

Yokogawa India Ltd.

Emerson Process Management (India) Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Schneider Electric confirmed INR 3,200 crore (USD 384 million) manufacturing investment in Karnataka to expand sensor and automation component output.

- July 2025: ABB India reported a tripling of data-center orders, citing hyperscale construction that demands precision HVAC sensors.

- June 2025: Daifuku completed an INR 2.27 billion (USD 272 million) smart factory in Hyderabad, integrating end-to-end sensor networks for zero-defect production.

- May 2025: Indian Oil Corporation and GPS Renewables signed an INR 1,200 crore (USD 144 million) biogas plant agreement requiring extensive process sensors.

- April 2025: Ebm-Papst inaugurated an INR 340 crore (USD 41 million) Chennai facility focused on sensor-integrated fan systems.

- March 2025: Oilmax Energy announced INR 450 crore (USD 54 million) Assam refinery expansion incorporating advanced safety sensors.

- February 2025: CG Pumps launched SmartSENSE wireless water pump controller for predictive maintenance in agriculture and industry.

- January 2025: Modine expanded Chennai operations to build sensor-equipped data-center cooling solutions.

India Industrial Sensors And Transmitters Market Report Scope

Industrial sensors are devices that can detect events or changes in the environment and provide the corresponding output. The study of the scope included various types of sensors and transmitters that are used for industrial automation purposes across multiple end-user industries in India.

India Industrial Sensors and Transmitters Market is segmented by Type of Sensor (Flow, Temperature, Pressure, Level, Transmitters) and by End-user (Power, Petrochemicals, Chemicals and Fertilizers, Food and Beverage, Water and Wastewater, Life Sciences, Oil and Gas).

| Flow |

| Temperature |

| Pressure |

| Level |

| Vibration/Condition-Monitoring |

| Gas and Humidity |

| Other Sensor Types |

| Power Generation and Utilities |

| Oil and Gas |

| Petrochemicals, Chemicals and Fertilizers |

| Food and Beverage |

| Life Sciences (Pharma, Biotech and Medical Devices) |

| Water and Waste-water |

| Metals and Mining |

| Other Manufacturing (Textile, Pulp and Paper, Auto, etc.) |

| Contact/In-line |

| Non-contact/Clamp-on/Remote |

| Wired (HART, MODBUS, PROFIBUS, etc.) |

| Industrial Ethernet (PROFINET, EtherNet/IP, etc.) |

| Wireless (ISA100, WirelessHART, Wi-SUN, LPWAN) |

| North India |

| West India |

| South India |

| East and North-East India |

| Central India |

| By Sensor Type | Flow |

| Temperature | |

| Pressure | |

| Level | |

| Vibration/Condition-Monitoring | |

| Gas and Humidity | |

| Other Sensor Types | |

| By End-user Industry | Power Generation and Utilities |

| Oil and Gas | |

| Petrochemicals, Chemicals and Fertilizers | |

| Food and Beverage | |

| Life Sciences (Pharma, Biotech and Medical Devices) | |

| Water and Waste-water | |

| Metals and Mining | |

| Other Manufacturing (Textile, Pulp and Paper, Auto, etc.) | |

| By Form Factor/Installation | Contact/In-line |

| Non-contact/Clamp-on/Remote | |

| By Communication Technology | Wired (HART, MODBUS, PROFIBUS, etc.) |

| Industrial Ethernet (PROFINET, EtherNet/IP, etc.) | |

| Wireless (ISA100, WirelessHART, Wi-SUN, LPWAN) | |

| By Region | North India |

| West India | |

| South India | |

| East and North-East India | |

| Central India |

Key Questions Answered in the Report

What is the current size of the India industrial sensors and transmitters market?

The market is worth USD 1.52 billion in 2026 and is projected to reach USD 2.36 billion by 2031.

Which sensor category leads in terms of revenue?

Pressure sensors accounted for 27.12% of 2025 shipments, driven by oil, gas, and process-plant safety requirements.

Which end-user vertical is growing fastest?

Life sciences is anticipated to record an 11.02% CAGR through 2031 as GMP mandates intensify real-time monitoring needs.

Why are wireless sensor networks gaining traction?

They lower retrofit costs and enable condition monitoring in hard-to-cable locations while supporting predictive maintenance programs.

Which region is forecast to grow the quickest?

South India is set for an 10.76% CAGR through 2031, fueled by technology-sector expansion and greenfield advanced-manufacturing projects.

What is the main challenge limiting rapid market adoption?

High upfront capital costs for smart-sensor retrofits, especially among SMEs, remain the principal brake on accelerated deployment.

Page last updated on: