Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

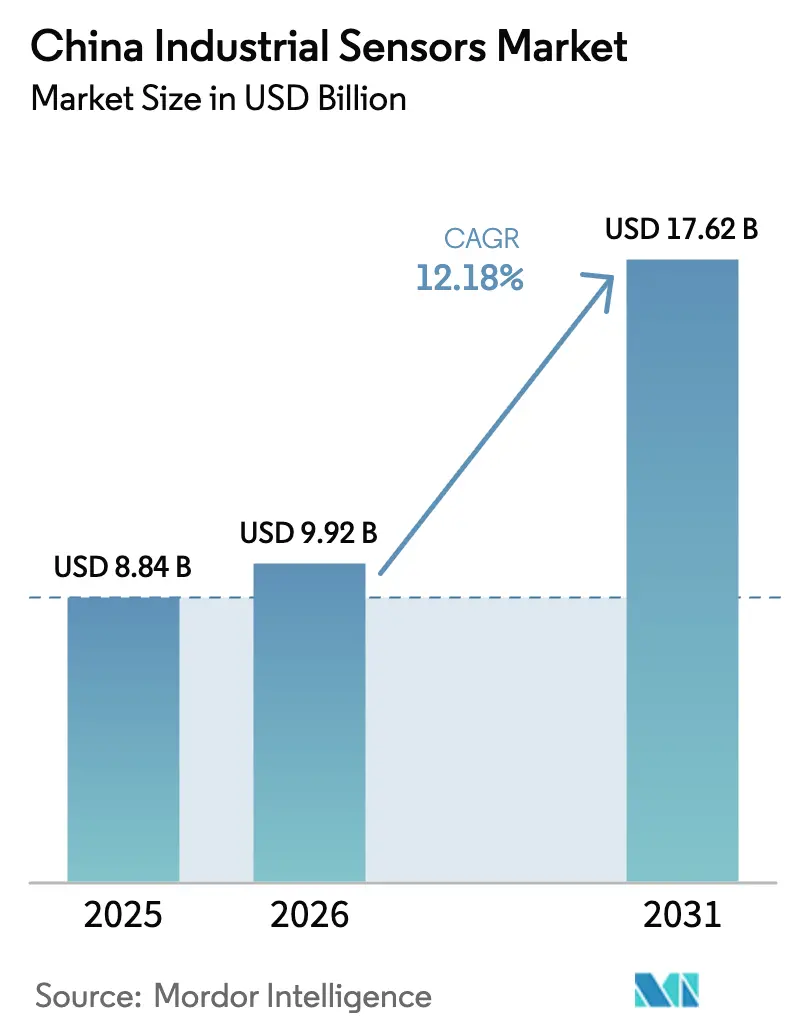

| Base Year Market Size (2025) | USD 8.84 Billion |

| Market Size (2026) | USD 9.92 Billion |

| Market Size (2031) | USD 17.62 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

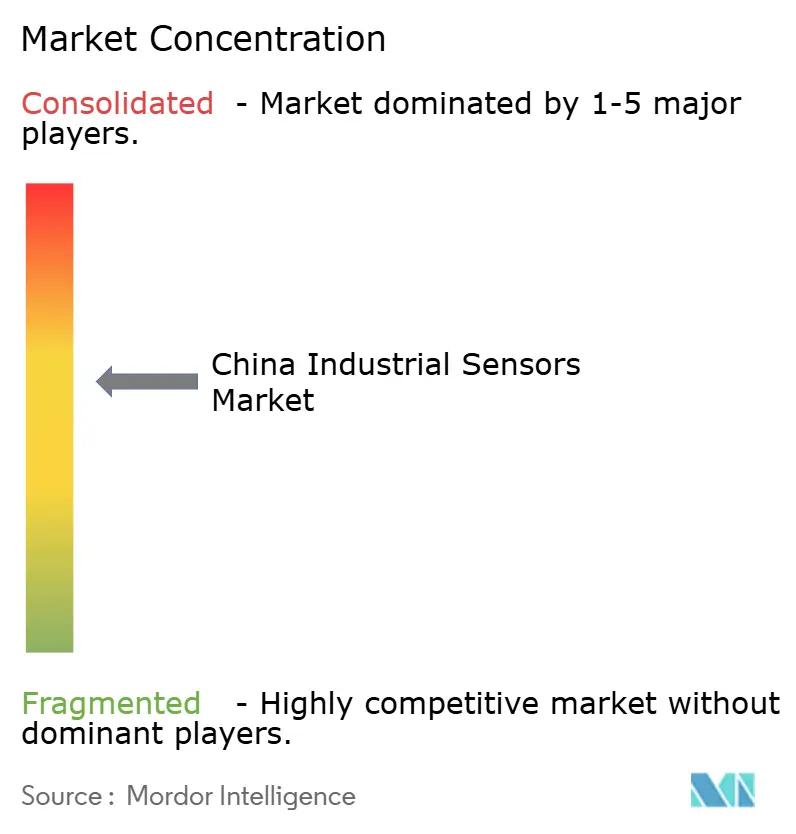

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Industrial Sensors Market Analysis by Mordor Intelligence

The China industrial sensors market size is projected to be USD 8.84 billion in 2025, USD 9.92 billion in 2026, and reach USD 17.62 billion by 2031, growing at a CAGR of 12.18% from 2026 to 2031. Government-backed retrofits that overlay smart nodes on legacy programmable-logic controllers, and a localization drive that shifts procurement toward domestic sensor dies. Mandatory carbon-accounting rules that entered force nationwide in early 2025 are catalyzing large-scale gas-sensor deployments, while 12.4 million electric vehicles produced in 2024 boosted multi-sensor demand across traction inverters, battery packs, and ADAS modules. Renewable-energy buildouts, exemplified by 430 gigawatts of wind and solar commissioned in 2024, require hundreds of pressure, flow, and temperature nodes per gigawatt to stabilize variable output, further lifting orders. At the same time, shortages of 12-inch MEMS capacity and new European encryption mandates inflate bill-of-materials costs, triggering a bifurcated export-grade and China-standard product mix. Multinational incumbents still dominate safety-instrumented niches, yet domestic challengers priced 20–30% below imported equivalents are winning power-generation and petrochemical tenders.

Key Report Takeaways

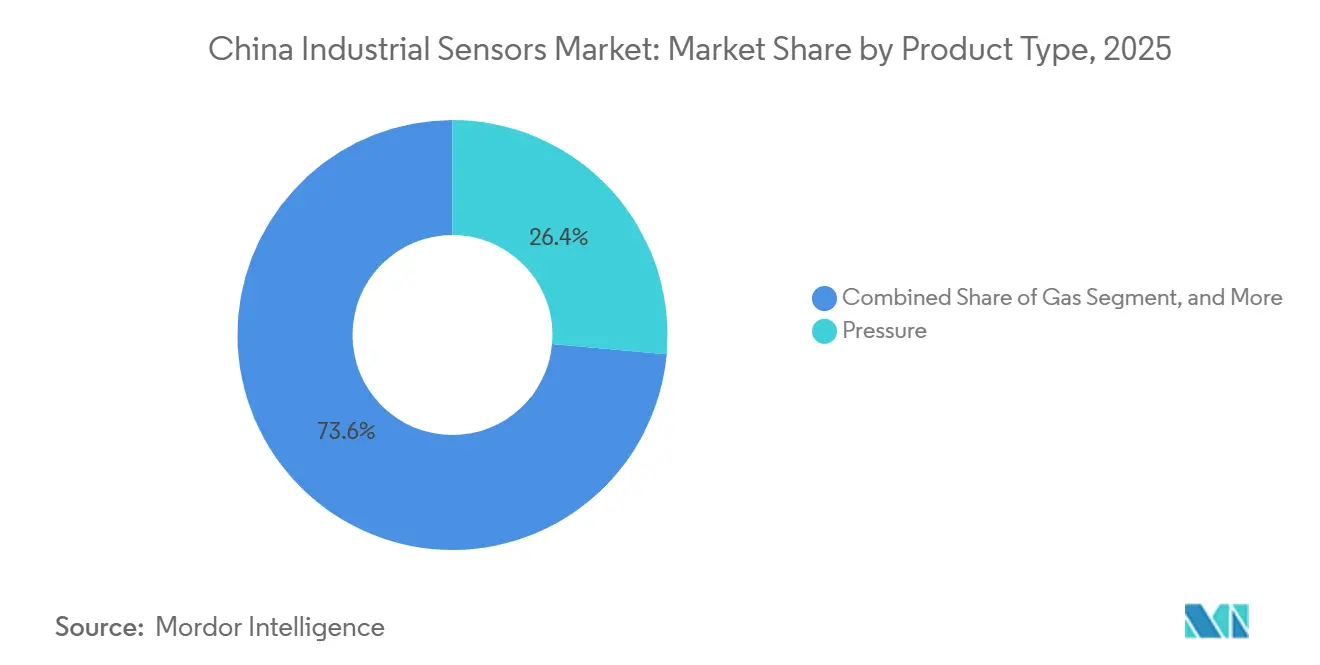

- By product type, pressure sensors led with 26.43% of the China industrial sensors market share in 2025, while gas sensor is projected to expand at a 13.92% CAGR through 2031.

- By end user, automotive accounted for 19.89% of 2025 revenue, whereas power generation is forecast to post the fastest 13.81% CAGR to 2031.

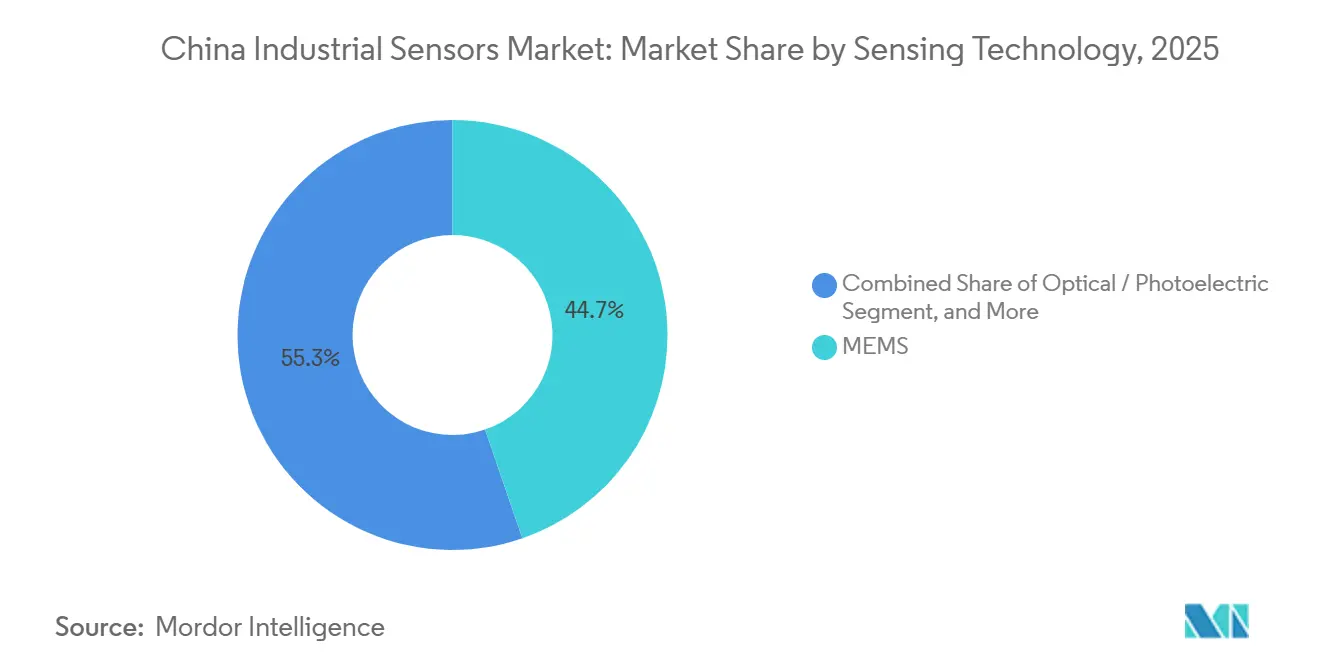

- By sensing technology, MEMS held 44.73% of the market share in 2025, and the optical or photoelectric variant is advancing at a 12.96% CAGR through 2031.

- By form factor, discrete sensors retained 39.57% of the 2025 market size, yet the wireless smart node is set to grow at 12.92% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Industrial Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industry 4.0 Deployment Accelerates Smart-Factory Sensor Retrofits | +2.8% | East China, South China, with spillover to Central China manufacturing corridors | Medium term (2-4 years) |

| Government Incentives for Domestic Sensor Localization | +2.1% | National, with concentrated impact in Beijing, Shanghai, Shenzhen innovation zones | Long term (≥ 4 years) |

| EV Production Surge Increases Multi-Sensor Demand | +2.5% | South China (Guangdong, Guangxi), Central China (Hubei, Hunan) EV hubs | Short term (≤ 2 years) |

| Predictive-Maintenance Programs Boost Pressure and Vibration Sensors | +1.6% | East China heavy industry, Northeast China legacy manufacturing bases | Medium term (2-4 years) |

| Mandated Carbon-Accounting at Industrial Parks Drives Flow and Gas Sensors | +1.9% | National, early enforcement in Yangtze Delta and Pearl River Delta industrial zones | Short term (≤ 2 years) |

| AI-Enabled Edge Analytics Makes Sensor-as-a-Service Viable for SMEs | +1.3% | National, fastest uptake in Zhejiang, Jiangsu SME clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industry 4.0 Deployment Accelerates Smart-Factory Sensor Retrofits

Thirty-thousand certified smart factories were online by end-2025, each averaging 1,500 sensor nodes that monitor temperature, pressure, vibration, and flow.[1]CAICT, “Smart Manufacturing Development Report 2025,” Ministry of Industry and Information Technology, miit.gov.cn Public subsidies covering 20–30% of retrofit capital outlay shorten payback cycles and boost penetration beyond heavy industry into textiles and ceramics. Overlay architectures keep legacy controllers in place while wireless meshes feed cloud-based twins, reducing installation labor by 40%. Edge gateways now filter 70% of data onsite, cutting cloud-storage fees by 60% and easing compliance with the Personal Information Protection Law. Node density still trails Germany, implying a multi-year runway that sustains the China industrial sensors market through the forecast horizon.

Government Incentives for Domestic Sensor Localization

Made in China 2025 set a 60% local-content goal that remains just shy of target, but fresh tax breaks and USD 3.2 billion of wafer-fab co-financing aim to close the gap. State-owned enterprises must now source at least half of non-safety-critical sensors domestically, redirecting roughly USD 800 million of annual spend. Automakers such as BYD and SAIC built in-house packaging lines in 2025, mirroring earlier battery vertical integration. Harmonization of GB and JB codes with IEC standards remains two to three years away, yet incremental alignment already trims export-requalification cycles, bolstering the China industrial sensors market competitiveness.

EV Production Surge Increases Multi-Sensor Demand

China produced 12.4 million electric vehicles in 2024 and each car integrates 40–60 sensors for thermal management, position feedback, and ADAS.[2]Charles Li, “China’s EV Sales Hit Record in 2024,” Reuters, reuters.com Battery packs alone use up to a dozen temperature probes under GB 38031-2020 safety rules. Shift to 800-volt systems forces pressure sensors to tolerate 1,000 bar coolant loops, narrowing the supplier field. Domestic MEMSIC introduced a 175 °C accelerometer in late 2024, closing performance gaps with foreign peers. Sensor content per EV climbed 18% year on year in 2025, adding momentum to the China industrial sensors market.

Mandated Carbon-Accounting at Industrial Parks Drives Flow and Gas Sensors

The national carbon-trading scheme expanded in 2024, installing 80,000 new gas-monitor points and spurring a replacement cycle from electrochemical cells to NDIR modules. Accuracy thresholds of ±2% above 100 ppm push factories toward five-year calibration sensors with wireless telemetry for remote auditing. Hanwei Electronics logged a 35% jump in gas-sensor orders in 1H-2025, 60% tied to carbon-accounting retrofits. Penalties of RMB 50-200 per ton of unreported emissions create a strong compliance incentive, underpinning long-term gas-sensor growth in the China industrial sensors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Import Dependence for High-End MEMS Dies Inflates BOM Costs | -1.8% | National, most acute in automotive and aerospace supply chains | Medium term (2-4 years) |

| Fragmented National Standards Complicate OEM Qualification | -1.2% | National, with regional variation in enforcement stringency | Long term (≥ 4 years) |

| 12-Inch MEMS Wafer Shortages Delay Localized Pressure-Chip Ramp-Up | -1.5% | East China and Central China fab clusters | Short term (≤ 2 years) |

| New EU Cybersecurity Rules Add Encryption Cost to Export-Grade Sensors | -0.9% | Export-focused manufacturers in Guangdong, Zhejiang, Jiangsu | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Import Dependence for High-End MEMS Dies Inflates BOM Costs

Domestic foundries supplied only 35% of precision dies in 2025, leaving pressure-chip costs 15–20% above vertically integrated European competitors.[3]Standards Administration, “National Standards Database,” SAC, sac.gov.cn U.S. export controls on lithography tools slow the 12-inch ramp, delaying cost parity. Workarounds like substituting 500-bar sensors where 700-bar units are specified constrain addressable aerospace and oil-and-gas business, tempering the otherwise robust China industrial sensors market expansion.

Fragmented National Standards Complicate OEM Qualification

Three overlapping regimes GB, JB, and provincial codes, stretch qualification by up to nine months. Suppliers often maintain multiple part numbers for different provinces, elevating inventory and certification overhead. Smaller Western firms frequently avoid bids below USD 5 million because compliance erodes margins, leaving local integrators in pole position but slowing the introduction of new technologies into the China industrial sensors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gas Sensors Capture Carbon-Monitoring Tailwinds

Gas sensors posted the quickest 13.92% CAGR outlook, propelled by continuous-emissions mandates that require 5–15 analyzer nodes per site. Pressure sensors retained the largest 26.43% slice of the China industrial sensors market share thanks to entrenched use across hydraulics and process controls. Temperature sensors benefit from tighter battery-thermal management in electric vehicles, while level and flow devices ride smart-metering rollouts in water and natural-gas networks. Magnetic and acceleration sensors scale with robotics and L2+ ADAS take-rates.

Electrochemical gas sensors are ceding share to NDIR and MOS variants that offer five-year calibration and embedded telemetry, lowering life-cycle costs by 40%. Pressure sensors remain resilient because petrochemical and power plants follow 10-year replacement cycles, locking in a stable revenue anchor for the China industrial sensors market size. Thermal probes multiply inside data centers that added 120 gigawatts of IT load in 2024. Flow and level sensors expand in food-processing lines to meet traceability under GB 14881, while magnetic sensors grow with brushless-motor adoption in appliances.

By End User: Power Generation Outpaces Automotive on Grid-Modernization Spend

Automotive held 19.89% of 2025 demand, but renewable-heavy power generation is forecast to top the segment growth league at 13.81% through 2031. Each gigawatt of wind or solar requires 200–300 nodes for inverter health, substation temperature, and frequency stabilization. Ultra-high-voltage DC links planned by State Grid deploy 1,500 sensors per line, favoring fiber-optic arrays over resistive detectors.

Chemical plants upgrade safety loops under GB 36894, aerospace demands radiation-hardened units, and hospitals added 180,000 ICU beds in 2024, all lifting specialty-sensor uptake. Semiconductor fabs seek ISO Class 1 air purity, embedding 1,200 particulate and gas sensors per line. Oil-field operators adopt wireless nodes at wellheads, trimming install costs by 30%, while water-treatment retrofits follow Yangtze River discharge limits, cementing diversified end-user pull across the China industrial sensors market size.

By Sensing Technology: Optical Variants Gain as Fab Tolerances Tighten

MEMS retained 44.73% shipment dominance owing to wafer-level economics and CMOS integration, yet optical or photoelectric sensors will advance 12.96%, capturing particulate detection below 10 nm in leading-edge fabs. Fiber-optic temperature arrays span 40 km pipelines at 1-meter resolution, slashing installed points by 60%. Non-MEMS bulk technologies still occupy brownfield niches due to lower upfront capital.

LiDAR proliferation saw 1.2 million units ship in 2024, each packing 64–128 photodetectors. Magnetic sensors rise with brushless DC motors, while sapphire-based optical probes address >150 °C zones that silicon cannot. The widening performance envelope sustains a healthy technology mix inside the China industrial sensors market.

By Form Factor: Wireless Nodes Unlock SME Digitization

Discrete sensors delivered 39.57% of 2025 revenue, anchored in safety loops where wired 4-20 mA meets SIL 3 availability. Wireless smart nodes, however, will grow 12.92% on the back of edge-AI chips that compress vibration data 10-fold before transmission. Payback drops under three years because installers forgo costly conduit labor.

Sensor-as-a-service packages priced at RMB 200–500 per node per year democratize predictive maintenance for 2.8 million small manufacturers. Integrated modules combine sensing element and communications inside compact shells for EV battery packs and medical devices where EMI shielding is critical. The co-existence of wired reliability and wireless flexibility diversifies growth avenues for the China industrial sensors market share.

Geography Analysis

East China generated 31.76% of 2025 spending, with 12,000 smart factories and aggressive 300 mm fab builds demanding up to 1,800 nodes per plant. Semiconductor leaders SMIC and YMTC alone added 150,000 wafers per month capacity, embedding thousands of environmental sensors to uphold ISO Class 1 cleanliness.

South China captured 24% of revenue, propelled by 3.8 million EVs assembled in Guangdong in 2024 and dense electronics export clusters. North China delivered 18% share due to heavy-industry retrofits that swapped manual exhaust sampling for continuous gas analyzers across steel mills.

Southwest China is forecast to grow 13.18% as Chengdu-Chongqing hubs lure manufacturing relocation with 20-30% retrofit subsidies. Central provinces contribute 14% of shipments, Northeast 8% as legacy machines digitize, and Northwest 5% tied to upstream energy and giga-scale solar farms. This regional mosaic underscores multiple growth vectors that reinforce the China industrial sensors market across coastal and inland provinces.

Competitive Landscape

The China industrial sensors market exhibits moderate fragmentation. The top five global suppliers, Honeywell, Emerson, Siemens, STMicroelectronics, and Bosch Sensortec, held major share of 2025 revenue, while leading domestic firms such as Hanwei Electronics, MEMSIC, and Shanghai Zhaohui controlled 28%, leaving 34% to over two hundred smaller integrators. Multinationals remain entrenched in SIL-rated safety systems and aerospace, but pricing pressure and domestic-content rules allow local players to win flow and level tenders by undercutting imports 20–30%. Patent filings for MEMS pressure dies jumped 40% in 2024, signaling a technology catch-up by 2028.

Wireless nodes bundled with cloud dashboards at USD 28–70 per year are being deployed at 40,000 SME sites in Zhejiang and Jiangsu. Edge-AI chipmakers now integrate inference engines into modules, cutting bandwidth needs by an order of magnitude. Automakers such as BYD and SAIC internalize packaging to secure supply and margin.

Incumbents respond with capacity expansions, joint ventures, and localized test centers. Siemens earmarked USD 128 million for Nanjing, STMicro teamed with SAIC on automotive MEMS, and Emerson opened a Suzhou calibration hub. These moves illustrate escalating investment as firms compete for a rising share of the China industrial sensors market.

China Industrial Sensors Industry Leaders

Honeywell International Inc.

Emerson Electric Co. (Rosemount Inc.)

STMicroelectronics N.V.

Shanghai Zhaohui Pressure Apparatus Co., Ltd.

Bosch Sensortec GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Siemens Process Instrumentation committed EUR 120 million (USD 128 million) to expand its Nanjing plant for MEMS pressure transmitters.

- November 2025: Hanwei Electronics won a RMB 680 million (USD 95 million) three-year deal to supply 85,000 NDIR modules for carbon-accounting retrofits.

- October 2025: STMicroelectronics and SAIC formed a USD 200 million Shanghai joint venture targeting 50 million automotive MEMS units annually by 2027.

- September 2025: Bosch Sensortec released a 175 °C MEMS accelerometer tailored for EV inverters and motor controls.

China Industrial Sensors Market Report Scope

Industrial Sensors are devices used in industrial environments to detect, measure, and transmit information about physical conditions so machines or control systems can monitor processes and operate automatically.

The China Industrial Sensors Market Report is Segmented by Product Type (Pressure, Temperature, Level, Flow, Magnetic Field, Acceleration and Yaw Rate, Gas), End User (Automotive, Aerospace and Military, Chemical and Petrochemical, Medical, Electronics and Semiconductor, Power Generation, Oil and Gas, Food and Beverage, Water and Wastewater, Other End Users), Sensing Technology (MEMS, Non-MEMS Bulk, Optical/Photoelectric, Magnetic/Hall), Form Factor (Discrete Sensors, Integrated Modules, Wireless Smart Nodes). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Pressure |

| Temperature |

| Level |

| Flow |

| Magnetic Field |

| Acceleration and Yaw Rate |

| Gas |

By End User

| Automotive |

| Aerospace and Military |

| Chemical and Petrochemical |

| Medical |

| Electronics and Semiconductor |

| Power Generation |

| Oil and Gas |

| Food and Beverage |

| Water and Wastewater |

| Other End Users |

By Sensing Technology

| MEMS |

| Non-MEMS (Bulk) |

| Optical / Photoelectric |

| Magnetic / Hall |

By Form Factor

| Discrete Sensors |

| Integrated Modules |

| Wireless Smart Nodes |

| By Product Type | Pressure |

| Temperature | |

| Level | |

| Flow | |

| Magnetic Field | |

| Acceleration and Yaw Rate | |

| Gas | |

| By End User | Automotive |

| Aerospace and Military | |

| Chemical and Petrochemical | |

| Medical | |

| Electronics and Semiconductor | |

| Power Generation | |

| Oil and Gas | |

| Food and Beverage | |

| Water and Wastewater | |

| Other End Users | |

| By Sensing Technology | MEMS |

| Non-MEMS (Bulk) | |

| Optical / Photoelectric | |

| Magnetic / Hall | |

| By Form Factor | Discrete Sensors |

| Integrated Modules | |

| Wireless Smart Nodes |

Key Questions Answered in the Report

What revenue level do analysts expect China industrial sensors to reach by 2031?

Forecasts point to USD 17.62 billion in 2031, up from USD 9.92 billion in 2026.

At what pace are wireless smart sensor nodes projected to advance between 2026 and 2031?

Shipments are set to rise at a 12.92% CAGR, making them the fastest-growing form-factor segment.

Which product type shows the strongest growth outlook through 2031?

Gas sensors lead with a 13.92% CAGR, driven by mandatory carbon-accounting requirements.

What key factor is pushing optical and photoelectric sensors into semiconductor fabs?

Sub-10 nm particulate detection thresholds exceed MEMS capability, so fabs adopt laser-scattering and fiber-optic modules.

Which Chinese region is expected to deliver the quickest expansion rate?

Southwest China, anchored by the Chengdu-Chongqing corridor, is projected to grow at 13.18% CAGR through 2031.

How concentrated is supplier competition in China’s industrial sensor space?

The concentration score is 6, reflecting roughly 38% combined share for the top five vendors and moderate fragmentation.

Page last updated on: