India Electrical Enclosures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Growth Rate | 5.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Electrical Enclosures Market Analysis by Mordor Intelligence

India electrical enclosures market size is expected to register a CAGR of 5.31% during the forecast period.[1]Power Ministry, “National Electricity Plan 2022-2032,” POWERMINGOV.IN Rapid grid-modernization programs, hyperscale data-center expansion, and stringent fire-safety regulations are accelerating procurement of robust, smart, and weather-resistant enclosures. Accelerating state-utility CAPEX exceeding INR 1 lakh crore, particularly for 765 kV transmission corridors, is lifting unit volumes, while mix shifts toward higher-spec metallic designs sustains value growth. Hyperscale facilities scaling from 1,150 MW in 2024 to an expected 2,100 MW by 2027 are driving fresh demand for IP54-plus, thermally managed cabinets, especially in Mumbai, Chennai, and Hyderabad.[2]India Brand Equity Foundation, “Data Centers Industry in India,” IBEF.ORG Compliance with the National Building Code 2016 is stimulating retrofit orders across hospitals, schools, and public offices, and Indian Railways’ 98% network electrification milestone is underpinning recurring maintenance demand. Together, these vectors create a multi-year runway for the India electrical enclosures market amid moderate competitive intensity and increasing localization incentives.

Key Report Takeaways

- By application, power generation and distribution commanded 29.05% of the India electrical enclosures market share in 2025, while commercial buildings and data centers are expanding at an 7.88% CAGR through 2031.

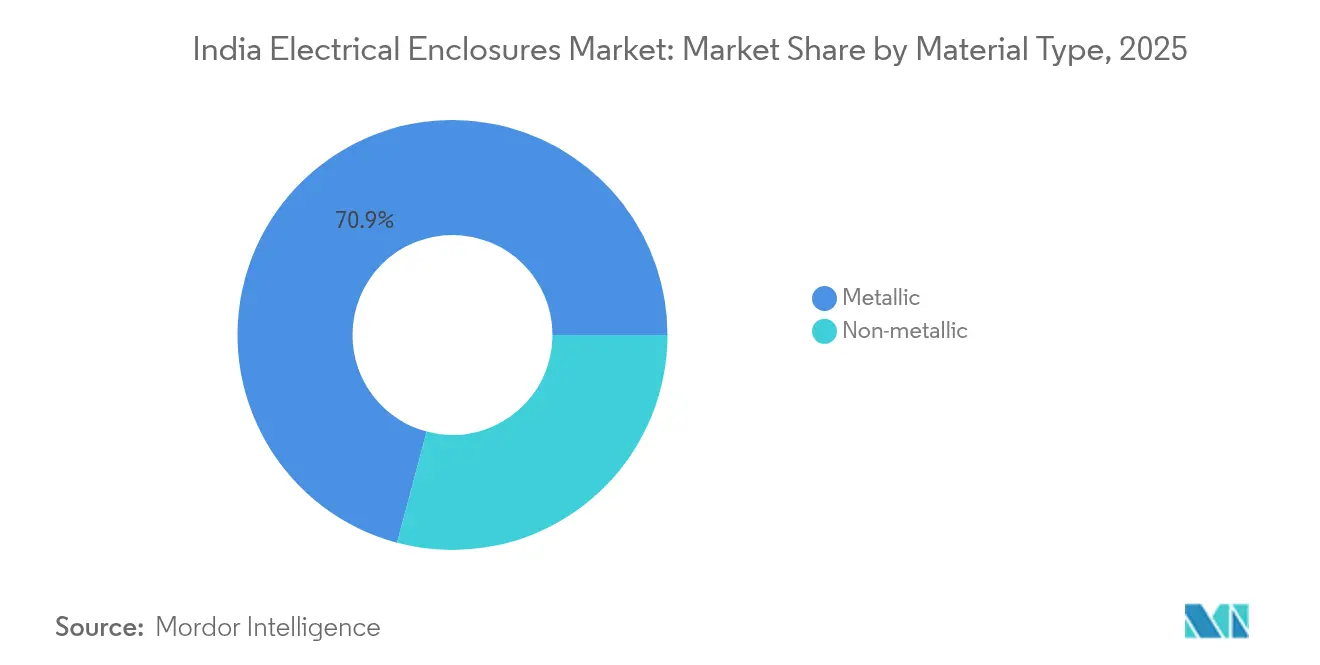

- By material type, metallic solutions captured 70.85% market share of the India electrical enclosures market size in 2025. Non-metallic alternatives are projected to log a 7.42% CAGR to 2031.

- By form factor, wall-mount units led with 36.25% share in 2025; modular and custom formats are forecast to grow at 6.98% CAGR.

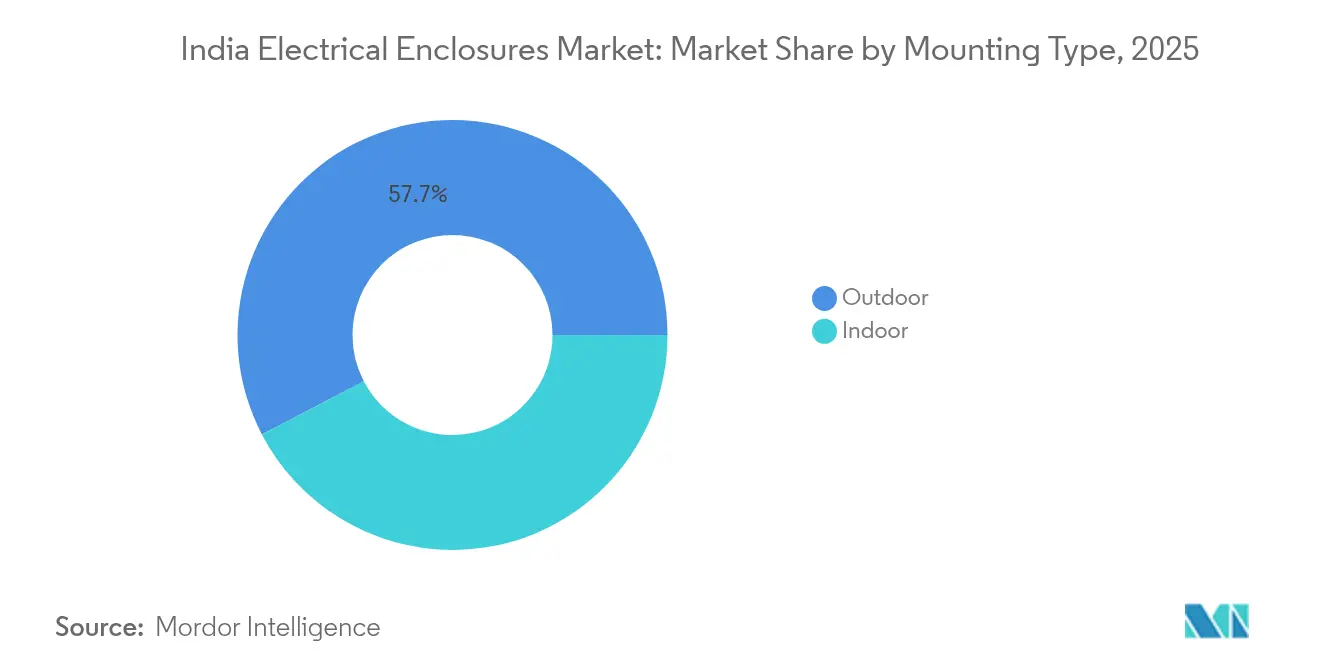

- By mounting, outdoor installations accounted for a 57.65% share of the India electrical enclosures market size in 2025 and are set to rise at a 6.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Electrical Enclosures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging grid-modernization CAPEX by state utilities | +1.20% | National, with concentration in Gujarat, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| Rising hyperscale data-centre build-outs | +0.90% | National, with early gains in Mumbai, Chennai, Hyderabad | Short term (≤ 2 years) |

| Mandatory fire-safety upgrades in public buildings (NBC-2016) | +0.70% | Urban centers, particularly Delhi NCR, Mumbai, Bangalore | Medium term (2-4 years) |

| Rapid electrification of Indian Railways | +0.60% | National rail network, concentrated in northern and eastern corridors | Long term (≥ 4 years) |

| Production-Linked Incentive push for switch-gear localisation | +0.50% | Manufacturing hubs in Gujarat, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| Growth of rooftop-solar OandM ecosystem | +0.40% | Solar-rich states including Rajasthan, Gujarat, Maharashtra | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Grid-Modernization CAPEX by State Utilities

State electricity boards are channelling record investments into high-voltage corridors, with the central allocation of INR 1 lakh crore for inter-state transmission alone. Gujarat’s INR 15,000 crore upgrade plan typifies the scale, necessitating larger IP65-rated housings for protection relays along new 765 kV lines. Demand rises for galvanized steel and aluminium cabinets with advanced climate controls, propelling both volumes and average selling prices within the India electrical enclosures market. Vendors able to certify products under BIS IS 2147 and integrate smart-grid sensors see heightened tender success. As installations shift from indoor substations to space-saving outdoor yards, corrosion-resistant coatings and dual-door sealing emerge as key differentiators. The medium-term impact is significant, sustaining a solid order pipeline for principal OEMs.

Rising Hyperscale Data-Centre Buildouts

Total installed IT load is projected to grow from 1,150 MW in 2024 to 2,100 MW by 2027, doubling enclosure demand for high-density power distribution units, bus-ducts, and battery-backup switchboards. Hyperscale specifies modular steel frames with integrated thermal barriers and cable management to handle rack densities above 10 kW. Procurement cycles are rapid, favouring suppliers that keep local assembly lines agile and inventory buffered. Because uptime requirements exceed 99.999%, operators insist on IP54-plus sealing, dual-redundant cooling fans, and digital trip breakers pre-fitted into enclosures. Tier-1 cities remain the launch pads, but edge nodes in Tier-2 markets now drive incremental volumes. Short-term uplift is pronounced as pre-committed hyperscale capacity converts to civil works and electrical fitouts.

Mandatory Fire-Safety Upgrades in Public Buildings (NBC-2016)

NBC-2016 compliance checks gained momentum after 2024, compelling hospitals, schools, and malls to replace outdated distribution boards with flame-retardant, compartmentalized enclosures.[3]Bureau of Indian Standards, “National Building Code 2016,” BIS.GOV.IN Retrofit projects favour powder-coated steel bodies rated to 960°C glow-wire tests and fitted with automatic fire-damper assemblies. Because many public buildings remain occupied during works, compact wall-mount designs that minimize downtime are preferred. BIS-certified manufacturers have a clear advantage as municipal auditors mandate visible ISI stamping. The regulatory drive marginally lifts CAPEX for facility owners yet unlocks a robust, mid-ticket order stream for enclosure suppliers into 2027.

Rapid Electrification of Indian Railways

With 98% of route kilometres now under electric traction, attention turns to maintenance and capacity-boost projects such as dedicated freight corridors. Railways specify high-vibration-resistance enclosures for traction substations, signalling huts, and level-crossing panels.[4]Ministry of Railways, “Railway Electrification Progress Report 2024,” INDIANRAILWAYS.GOV.IN Requirements include IP66 sealing, stainless-steel hinge, and EMI shielding. Indigenous value addition is encouraged under the Production-Linked Incentive scheme, giving local fabricators access to long-term rate contracts. The long-term nature of rail projects provides revenue visibility, while safety audits ensure recurring retrofit cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel and aluminium price volatility | -0.80% | National, with higher impact in manufacturing hubs | Short term (≤ 2 years) |

| Proliferation of counterfeit IP-rated products | -0.60% | National, concentrated in unorganized market segments | Medium term (2-4 years) |

| Fragmented state-level certification regimes | -0.40% | State boundaries, particularly affecting inter-state projects | Medium term (2-4 years) |

| Supply-chain bottlenecks for silicone gaskets | -0.30% | National, with acute impact on coastal and chemical applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Steel and Aluminium Price Volatility

HRC steel swung by INR 3,000 per tonne during 2024 as anti-dumping duties on Chinese supply intersected with fluctuating coking-coal costs. Aluminium premiums tracked LME spikes driven by energy-price volatility. Smaller enclosure shops operating on quarterly rate contracts struggle to hedge, forcing margin resets or component downsizing. Some OEMs responded by redesigning side-panels at 1.6 mm thickness versus 2 mm, a trade-off that risks stiffness in larger cabinets. Elevated raw-material risk deters long-duration fixed-price bids, delaying awards on state-utility tenders. Although volatility should moderate past 2026, near-term headwinds shave 80 basis points off CAGR forecasts.

Proliferation of Counterfeit IP-Rated Products

BIS raids on e-commerce warehouses seized over 10,000 fake IP-marked enclosures in 2024, revealing widespread forgery of ISI logos and test certificates. Substandard units corrode prematurely, spark short circuits and erode customer confidence. Legitimate vendors incur additional costs for holographic labels and QR-code tracing while price-cutting rivals flood low-awareness industrial clusters. Installation contractors face liability exposure, tightening their approved vendor lists and, over time, restoring share to compliant producers. Until enforcement fully scales, counterfeit penetration remains a material drag on revenue realization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Metallic Endurance Versus Non-Metallic Momentum

Metallic housings held 70.85% India electrical enclosures market share in 2025, with galvanized steel dominating traction substations and high-current switchboards. The India electrical enclosures market size for metallic products was USD 186.39 million in 2025 and is projected to expand at 4.78% CAGR to 2031. Aluminium earns favour in rooftop solar combiner boxes where weight matters. Rising OPEX on anti-corrosion repainting is nudging coastal utilities toward fiberglass and polycarbonate alternatives that clock a 7.42% CAGR. Non-metallic cabinets also absorb less heat, benefitting data-hall aisle containment. Schneider’s Kolkata polymer plant and ABB’s Vadodara FRP line illustrate supplier bets on composite growth. Imported resin costs and BIS IS 14772 testing fees keep unit prices at a 15-20% premium, yet total-cost-of-ownership analyses still tilt some specifiers toward polymer choices in saline or chemical environments.

Second-generation engineering plastics are now meeting vertical-flame and UV-aging standards, underscoring their readiness for utility deployments. Polycarbonate molds allow ergonomic latch integration and transparent doors for quick visual inspection, perks that bolster occupational safety audits. Conversely, metallic cabinets remain unrivalled for electromagnetic shielding when sensitive SCADA relays share space with high-fault-current busbars. The balance of use-cases points to sustained metallic dominance but with growing composite niches in coastal and data infrastructure.

By Form Factor: Wall-Mount Stability with Modular Upside

Wall-mount products accounted for 36.25% of 2025 shipments and remain indispensable for distribution-panel retrofits in commercial towers and metro stations. Their compact footprint, hinged doors, and rear cable entry simplify tenant fit-outs. Meanwhile, modular aisle-based systems are surging at 6.98% CAGR as hyperscale operators pre-fabricate skids populated with MCCBs, transformers, and monitoring PLCs off-site. Like-for-like price premiums of 25% are offset by 35% faster go-live timelines, a metric valued by colocation providers chasing occupancy SLAs.

Free-standing floor cabinets service substations, steel mills, and wastewater plants where heavy gear and large-cross-section busbars require bottom cable entry and plinth-mount anchoring. Junction-box volumes track rooftop solar rollouts, especially in Rajasthan and Gujarat. For OEMs, form-factor diversification underpins cross-selling: Schneider’s Prisma-Plus lends wall-mount segments while the SM AirSeT draws floor-mount demand. System integrators increasingly issue framework bids bundling multiple form factors, rewarding suppliers with broad catalogues and standardized internal mounting grids.

By Mounting Type: Outdoor Builds Dominate

Outdoor units contributed 57.65% of 2025 revenues, with the India electrical enclosures market size in this segment projected at USD 222.58 million by 2031, rising 6.62% CAGR. IP66 sealing, triple-layer powder coatings, and 1,000-hour salt-spray ratings differentiate leading offers. Smart-city pole-top controllers, EV-charger feeders, and rail-signalling huts all add to the outdoor tally. Vendors craft cooling strategies ranging from passive sunshields to thermoelectric units integrated behind double walls.

Indoor cabinets persist in data centers, hospitals, and process plants where HVAC environments let thinner-gauge sheet metal and natural convection suffice. NBC-2016 drives fire-retardant powder types and smoke-tight gasketing for indoor boxes in public structures. Hybrid configurations are surfacing outdoor primary breakers feeding indoor secondary panels interconnected by pre-terminated armoured cables. Such system-level selling unlocks bundle margins and demand visibility for enclosure manufacturers.

By Application: Power Leads While Digital Transformation Accelerates

Power generation and T&D installations owned a 29.05% share of 2025 shipments, equating to USD 76.46 million of the India electrical enclosures market size. Transmission mega-projects require skid-mounted protection panels and line-monitoring cabinets, typically 3 mm steel with anti-condensation heaters. Renewable assets layer additional orders for inverter MV isolator boxes and string combiner casings.

Commercial buildings and data centers post the fastest 7.88% CAGR, fuelled by enterprise cloud migration, fintech adoption, and OTT streaming traffic. Each incremental megawatt of IT load translates to roughly 22 wall-mount or aisle-containment enclosures for PDU, UPS bypass, and battery monitoring functions. Transportation applications—metro rail, airports, highways—are steady, whereas oil and gas demand hinges on capex cycles in refinery revamps. Process industries gradually standardize on stainless-steel NEMA 4X boxes to meet GMP and FDA cleanliness mandates. Collectively, this diversity shields the India electrical enclosures market against single-sector downturns.

Geography Analysis

Maharashtra generates the highest consumption, anchored by Mumbai’s data-center corridor and Pune’s automotive belt. Policy support via the state’s Information Technology Investment Region further entices hyperscale’s, translating into sizable wall-mount and modular rack orders. Gujarat follows, driven by 10 GW-plus solar farms in Kutch and robust port-led industrialization along the Dholera SIR; corrosion-proof FRP cabinets are routine here. Tamil Nadu leverages its automotive OEM hub and 15-GW wind base, while Karnataka rides Bengaluru’s tech sector and startup ecosystem, stimulating low-to-mid current panel needs.

Northern cluster demand stems from Delhi NCR’s metro expansion and smart-grid pilots around Noida and Gurugram. Haryana’s IMT Manesar auto component park adopts advanced busbar enclosures, and Uttar Pradesh channelizes capex toward expressway electrification. Extreme summer heat drives the selection of light-coloured powder coats and solar-reflective roofs.

Eastern states such as West Bengal and Odisha clock rising uptake from steel, aluminium, and petrochemical complexes. Coastal humidity pushes specifiers toward 316-grade stainless or UV-stabilized polymers, mitigating rust in saline air. Government port-modernization spend amplifies the requirement for marine-grade, IP67 junction boxes on jetties and crane feeds.

Competitive Landscape

Multinationals and domestic majors jostle in a market where the top five combined held roughly 38% share in 2024, indicating moderate fragmentation. Schneider Electric’s fresh 1.2 million sq. ft greenfield campuses at Hyderabad and Ahmednagar will expand sheet-metal punching and polymer injection capacity, shaving lead times for export as well as domestic buyers. ABB India leverages its Bengaluru digital hub to integrate predictive-maintenance sensors into cabinets, bundling hardware with cloud analytics. Siemens is pouring INR 1,000 crore into clean-air switchgear lines at Aurangabad, embedding SF6-free breaker modules into its enclosure suites.

Larsen and Toubro couples EPC wins with captive enclosure supply, recently securing INR 2,500 crore grid-modernization packages spanning Gujarat to Rajasthan. Tier-2 regional fabricators, often family-owned, prosper in contract manufacturing for OEM brands, yet counterfeit risks and tightening BIS audits may thin their ranks. Technology differentiation centers on IoT gateways, arc-flash sensors, and modular design libraries that allow late-stage customization without tooling alterations.

Government localization mandates and RoDTEP export incentives spur capacity additions, but raw-material volatility and widening compliance demands test capital discipline. M&A opportunities surface as multinationals scout specialty FRP formulators and gasket suppliers to secure upstream inputs.

India Electrical Enclosures Industry Leaders

BCH Electric Ltd

Schneider Electric

ABB Ltd

Eaton Corporation

Emerson Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ministry of Electronics and Information Technology confirmed that the Machinery and Electrical Equipment Safety Order 2024 will take full effect in August 2025, giving manufacturers a seven-month window to secure BIS marks for higher-rated enclosures.

- September 2024: Schneider Electric pledged INR 3,200 crore capacity expansion across Kolkata, Hyderabad, and Ahmednagar over 2024-2026 to meet domestic and export demand for LV and MV enclosures.

- August 2024: BIS launched an online traceability platform enabling installers to verify ISI licenses via QR scans, targeting counterfeit electrical products.

- July 2024: ABB India posted record Q2 revenue of INR 3,047 crore and a 32% order backlog surge, buoyed by smart enclosure and switchgear sales.

India Electrical Enclosures Market Report Scope

An electrical enclosure is a cabinet for electronic equipment to mount switches, knobs, and displays to control electrical shock to equipment users and protect the contents from the environment.

India's Electrical Enclosures Market is segmented by material type (metallic enclosures and non-metallic enclosures) and application (power generation and distribution, transportation, oil and gas, commercial spaces and buildings, and process industries). The impact of COVID-19 on the market and impacted segments is also covered under the scope of the study. Further, the disruption of the factors affecting the market's expansion in the near future has been covered in the study regarding drivers and restraints. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Metallic |

| Non-metallic |

| Wall-mount |

| Floor-mount / Free-standing |

| Junction / Terminal boxes |

| Modular / Custom |

| Indoor |

| Outdoor |

| Power Generation and Distribution |

| Transportation (Rail, Metro, Airports) |

| Oil and Gas |

| Commercial Buildings and Data Centres |

| Process Industries (FandB, Pharma, Chemicals) |

| Others Applications |

| By Material Type | Metallic |

| Non-metallic | |

| By Form Factor | Wall-mount |

| Floor-mount / Free-standing | |

| Junction / Terminal boxes | |

| Modular / Custom | |

| By Mounting Type | Indoor |

| Outdoor | |

| By Application | Power Generation and Distribution |

| Transportation (Rail, Metro, Airports) | |

| Oil and Gas | |

| Commercial Buildings and Data Centres | |

| Process Industries (FandB, Pharma, Chemicals) | |

| Others Applications |

Key Questions Answered in the Report

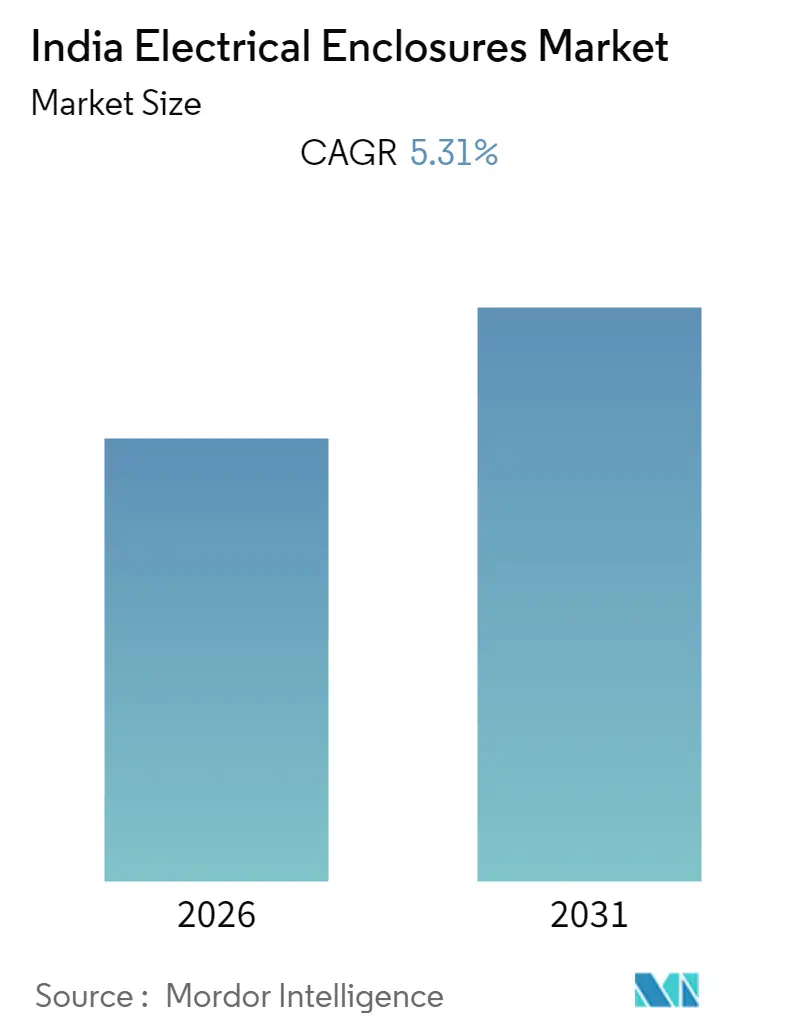

What is the 2026 value of the India electrical enclosures market?

It is USD 277.06 million, and it is forecast to grow at a 5.31% CAGR to reach USD 358.68 million by 2031.

Which application segment is expanding fastest?

Commercial buildings and data centers show the fastest growth with an 7.88% CAGR through 2031, fueled by hyperscale capacity doubling plans.

How large is the metallic share of shipments?

Metallic housings captured 70.85% India electrical enclosures market share in 2025, thanks to grid and rail projects.

Why are counterfeit products a concern?

BIS seized over 10,000 fake enclosures in 2024, and such products erode revenue and pose safety risks due to substandard ingress protection.

Which regions contribute most to demand?

Maharashtra and Gujarat lead purchases, with Tamil Nadu and Karnataka closely following thanks to renewables, automotive and tech-sector expansion.

What impact do steel prices have on suppliers?

HRC steel swings of INR 3,000 per tonne compress margins and can delay fixed-price tenders, shaving roughly 0.8 percentage points off CAGR forecasts.

Page last updated on: