Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 50.46 Billion |

| Market Size (2031) | USD 63.45 Billion |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Pump Market Analysis by Mordor Intelligence

The industrial pump market size was valued at USD 48.2 billion in 2025 and estimated to grow from USD 50.46 billion in 2026 to reach USD 63.45 billion by 2031, at a CAGR of 4.69% during the forecast period (2026-2031). Sustained replacement of aging municipal networks, petrochemical capacity additions, and tighter efficiency rules underpinned the market’s resilience through prolonged supply-chain volatility. Capital spending on water treatment remained the single largest pull-forward of demand, with the United States alone earmarking more than USD 50 billion for water infrastructure upgrades between 2022 and 2026. Mega-projects in Qatar and Saudi Arabia continued to lift orders for high-specification pumps capable of handling corrosive, high-temperature media in ethylene crackers and gas-processing trains. Asia-Pacific retained volumetric leadership on the back of large-scale industrialization across China, India, and Southeast Asia, while the Middle East and Africa posted the fastest growth trajectory as petrochemical diversification accelerated.

Key Report Takeaways

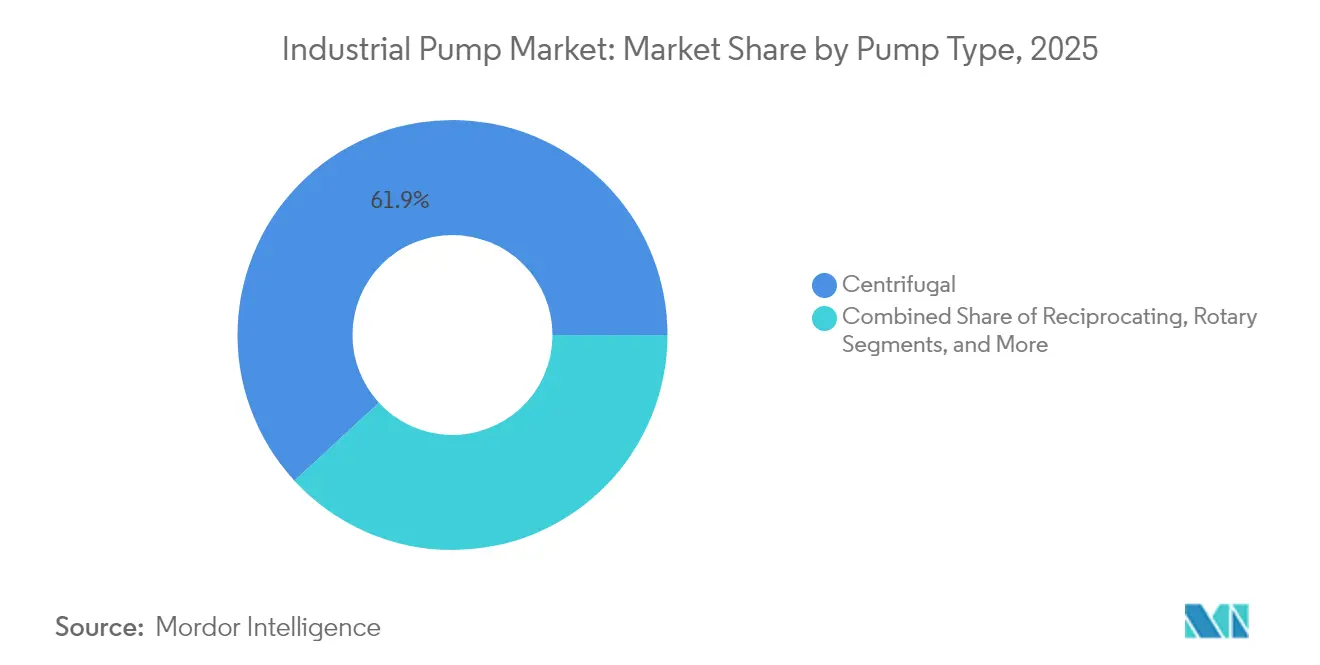

- By pump type, centrifugal designs led with 61.85% revenue share in 2025; progressing cavity pumps are forecast to expand at a 7.45% CAGR through 2031.

- By power source, electric-driven systems held 77.95% of the industrial pump market share in 2025, whereas solar-powered units are projected to grow at an 11.1% CAGR to 2031.

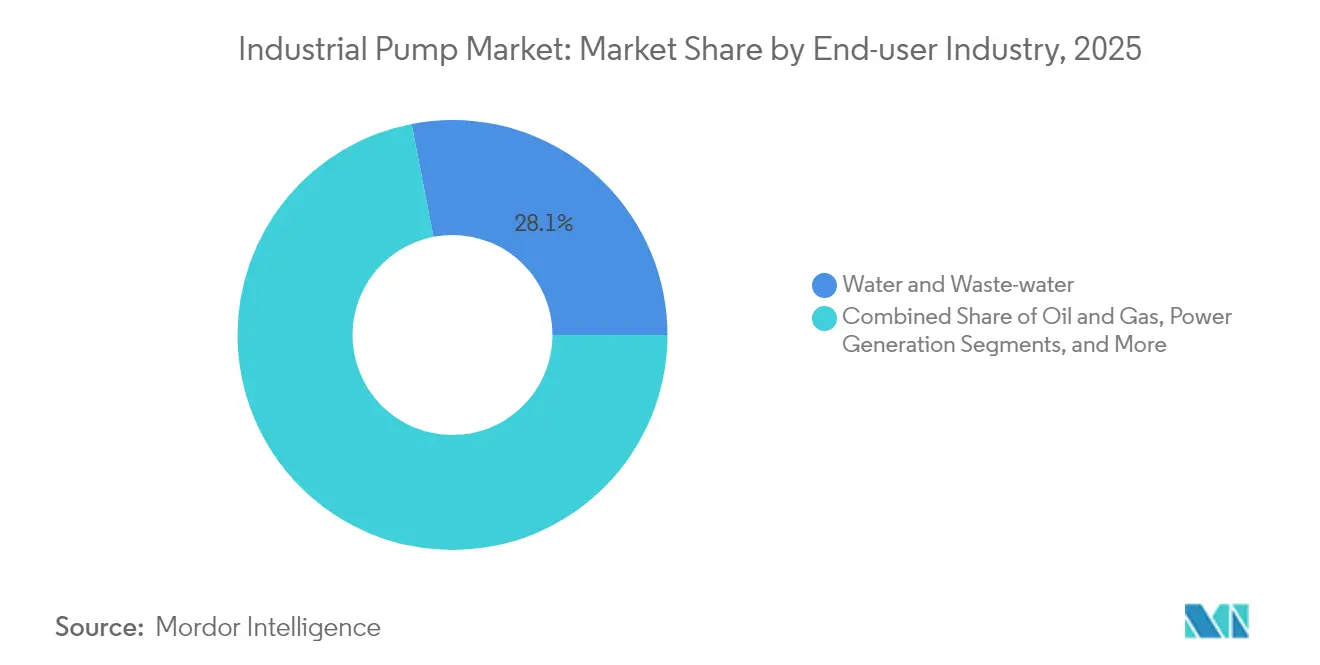

- By end-user industry, water and wastewater applications captured 28.05% share of the industrial pump market size in 2025; chemicals and petrochemicals are advancing at a 6.48% CAGR to 2031.

- By orientation, submersible units commanded 30.75% of 2025 revenue; surface pumps are on track for a 9.85% CAGR through 2031.

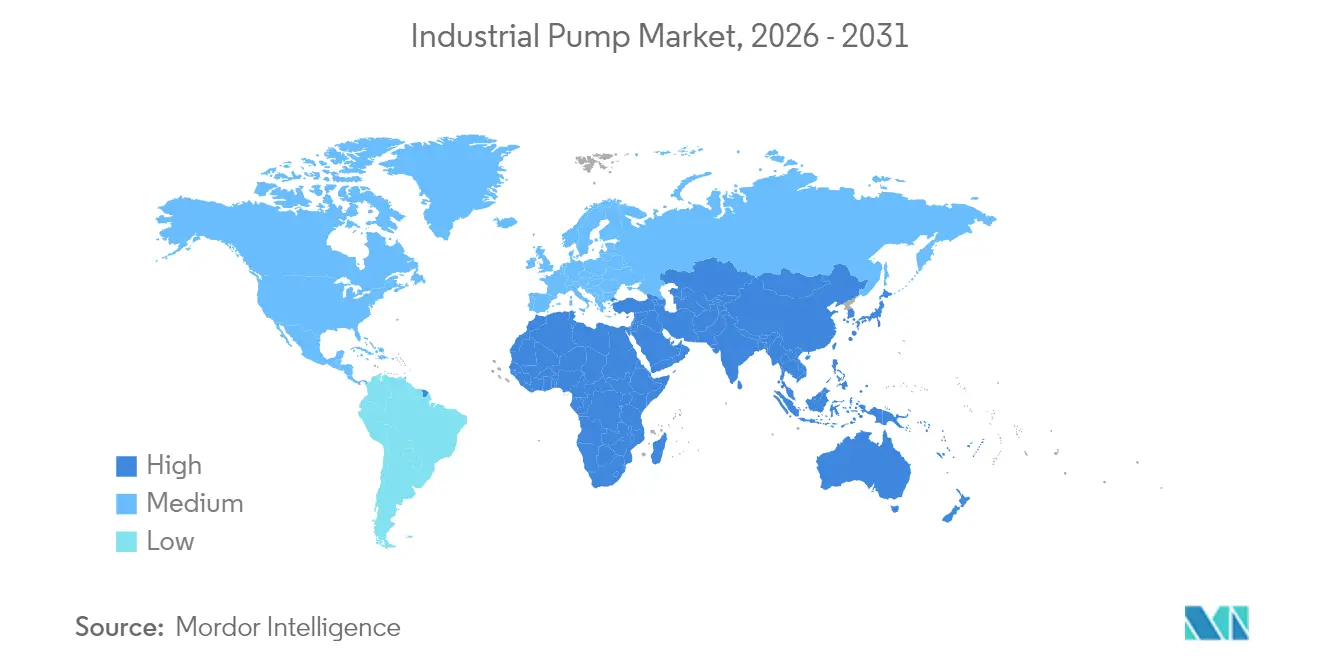

- By geography, Asia-Pacific accounted for 44.85% of 2025 revenue; the Middle East and Africa region is growing at a 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising water and wastewater treatment spending globally | +1.8% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of petrochemical capacity in MEA | +1.2% | Middle East and Africa, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Rapid industrial infrastructure build-out across Asia-Pacific | +1.5% | Asia-Pacific core, secondary impact in South America | Medium term (2-4 years) |

| Demand for corrosion-resistant pumps in green-hydrogen electrolyzers | +0.7% | Global, early adoption in Europe and North America | Long term (≥ 4 years) |

| Predictive-maintenance IoT service models unlocking aftermarket revenue | +0.9% | Global, led by developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Water and Wastewater Treatment Spending Globally

Record municipal budgets released in 2024 and early 2025 translated into larger tender volumes for high-capacity centrifugal and submersible sewage pumps. The US Environmental Protection Agency estimated long-term rehabilitation needs above USD 744 billion, prompting multi-phase upgrades such as Sioux City’s USD 465 million regional facility and Cape Fear’s USD 239 million Southside plant. Advanced treatment mandates drove interest in high-pressure reverse-osmosis trains, with Sulzer’s vertical multistage systems underpinning Egypt’s Al Mahsama drainage reclamation project.[1]Mary Scott Nabers, “A Multi-Billion-Dollar Water Industry Segment Not To Be Overlooked,” Water Online, wateronline.com Utilities are increasingly embedding wireless sensors that stream vibration and temperature data into cloud dashboards, shortening mean-time-to-repair on critical units. Procurement frameworks began weighting total-cost-of-ownership calculations that favor energy-efficient designs, nudging buyers toward premium efficiency motors that comfortably clear EU MEI thresholds. Heightened monitoring obligations also expanded aftermarket revenue pools, anchoring recurring service contracts for OEMs.

Expansion of Petrochemical Capacity in MEA

Gulf producers pushed downstream diversification agendas, awarding EPC contracts for crackers, polymer units, and gas-processing trains that collectively require thousands of corrosion-resistant pumps. Qatar’s Ras Laffan polymers complex, budgeted at USD 6 billion, incorporated a 2,080 KTA ethane cracker slated for 2027 on-stream dates. Saudi Arabia’s USD 11 billion Amiral project added 1.65 million tons of ethylene nameplate capacity integrated with SATORP’s refinery, multiplying demand for API 610 compliant pumps that withstand 400°F discharge temperatures. Local-content clauses inside procurement tenders intensified incentives for international OEMs to localize casing machining and final assembly. End-users prioritized variable-frequency drives to curb power draw, reinforcing adoption of smart motor controls that align with regional energy-efficiency ambitions.

Rapid Industrial Infrastructure Build-out Across Asia-Pacific

China’s SABIC-backed USD 6.4 billion Fujian complex and India’s ongoing Smart Cities Mission channeled funding into water, energy, and manufacturing assets, each a pull-through for the industrial pump market. Automated production lines demanded digitally controlled dosing and transfer pumps able to interface with factory IT networks. Mining houses in Indonesia and Mongolia increased procurement of high-chromium slurry pumps to manage tailings with solids content above 20%. Simultaneously, desalination plants in Australia contracted high-pressure multistage units designed for 70 bar feed pressures, reflecting rising water scarcity. Regional buyers proved receptive to pay-per-use service models that bundle analytics-driven maintenance, unlocking new subscription revenue for OEMs. Carbon-pricing schemes in South Korea and Japan further incentivized the adoption of pumps rated at higher wire-to-water efficiency, pressing suppliers to iterate hydraulic designs rapidly.

Demand for Corrosion-Resistant Pumps in Green-Hydrogen Electrolyzers

Electrolyzer installations surged from pilot scale to multi-megawatt arrays in Europe and North America, spurring an emergent niche for pumps fabricated from 316L stainless, super-duplex, and advanced polymer coatings. Process engineers required circulation systems that tolerate highly corrosive electrolytes while managing flow fluctuations within ±2%. Suppliers like Fluid Components International introduced SIL-2 certified flow switches tailored for PEM stacks, while IHI developed specialized bipolar-plate coatings that maintain low interfacial resistance at 30 bar operating pressures. As project developers chased levelized-hydrogen-cost targets, pump efficiency and uptime became differentiators shaping vendor shortlists. Although volumes remain modest, first-mover suppliers established reference plants that are expected to translate into follow-on orders as hydrogen hubs scale toward gigawatt levels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in steel and copper prices is inflating TCO | -0.8% | Global, particularly affecting manufacturing hubs | Short term (≤ 2 years) |

| Stricter pump-efficiency directives are delaying cap-ex cycles | -0.6% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Shift to motorless gravity micro-irrigation systems in arid economies | -0.3% | Middle East, North Africa, and arid regions globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Steel and Copper Prices Inflating TCO

Copper cleared USD 10,000 per metric ton in 2024 and flirted with USD 11,000 amid looming supply deficits, hiking producer input costs by 3.5%–4.2% on copper-intensive stators and windings. Carbon-neutral steel initiatives added further unpredictability as mills passed on green-premium surcharges linked to hydrogen-based production. Manufacturers responded by tightening hedging programs, redesigning casings for material thrift, and introducing dynamic price clauses into supply contracts. End-users, meanwhile, deferred discretionary replacements, stretching the mean equipment life and tempering near-term shipment volumes in the industrial pump market.

Stricter Pump-Efficiency Directives Delaying Cap-ex Cycles

The European Union’s MEI amendments under Regulation 547/2012 entered into enforcement in late 2024, while the US Department of Energy retained stringent Pump Efficiency Rating thresholds referenced in 10 CFR Part 431. Legacy designs struggled to pass mandated wire-to-water benchmarks, compelling OEMs to invest in new hydraulic geometries and expanded test-stand capacity. Certification backlogs extended product launch timelines, and end-users postponed purchases pending the availability of compliant models. Small regional fabricators lacking laboratory facilities risked market exit, accelerating consolidation trends that favored multinational brands with deep engineering benches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Centrifugal Dominance Faces Specialty Challenges

Centrifugal units retained 61.85% of 2025 revenue, anchoring the industrial pump market through their proven cost-performance balance in water supply, chemical transfer, and HVAC loops. The segment generated steady aftermarket volumes, given typical mean-time-between-overhauls of three years in municipal duty cycles. However, specialty demands in viscous slurry handling shifted incremental share toward progressing cavity designs, which are projected to clock 7.45% CAGR through 2031. The progressing cavity cohort captured a rising slice of the industrial pump market size for petrochemical and mining customers that prize low-shear conveyance. Meanwhile, reciprocating and diaphragm pumps preserved critical roles in high-pressure injection and sanitary production, respectively, albeit with niche footprints. IoT retrofits became common even on legacy centrifugal sets, enabling predictive vibration analytics that cut unscheduled downtime by up to 30%.

Progressing cavity manufacturers invested heavily in wear-resistant rotor coatings to extend service intervals beyond 8,000 hours under abrasive duty. Rotary gear and peristaltic pumps addressed emerging micro-dosing tasks within battery-materials manufacturing lines, underscoring the breadth of end-use innovation. Digital twins built from sensor telemetry allowed operators to simulate cavitation risk across the hydraulic envelope, driving process-control refinements that protect impellers. Suppliers continued to emphasize modular cartridge seals that simplify maintenance and shrink spare inventory. With regulatory spotlight fixed on energy intensity, efficiency upgrades in casing volutes and diffuser vanes became a competitive must-have across all pump types in the broader industrial pump market.

By Power Source: Electric Hegemony Challenged by Solar Innovation

Electric-driven assemblies held a commanding 77.95% share in 2025, benefitting from near-universal grid access in industrialized economies and the incremental efficiency yields of variable-frequency drives. Field data logged by Graco’s QUANTM platform demonstrated up to 85% motor efficiency thanks to transverse-flux topology, reinforcing the narrative of electricity-based lifecycle cost advantage. Solar-powered solutions, however, emerged as the fastest expanding slice of the industrial pump industry, advancing at an 11.1% CAGR on the back of rural irrigation projects in Africa and South Asia. Installation costs ranging from EUR 76.23 (USD 89.13) to EUR 1,219.59 (USD 1,425.95) translated to competitive levelized costs, particularly once fuel-logistics premiums on diesel sets were factored in.

Diesel-engine packages retained strategic relevance for oilfield fracturing and emergency stormwater evacuation, where grid resilience remained questionable. Hydraulic and pneumatic drives continued to serve hazardous-area placements and mobile plant equipment that prized power density and ignition safety. Hybrid microgrid solutions that pair PV arrays with lithium-ion storage entered the pilot stage at several Indonesian mines, offering 24/7 uptime without diesel supplementation. VFD retrofits on existing electric fleets shaved energy bills by up to 20% in continuous-duty desalination applications. Altogether, the power-source mix illustrated end-user pragmatism, but electric leadership in the industrial pump market is expected to persist through the forecast horizon.

By End-user Industry: Water Treatment Leads Amid Chemical Sector Surge

Municipal and industrial water operators commanded 28.05% of total 2025 revenue, underscoring the sector’s status as the backbone of the industrial pump market. Ongoing replacement of aging cast-iron pumps with corrosion-resistant duplex steel variants intensified as utilities sought longer asset lifecycles against rising salinity loads in coastal aquifers. The chemicals and petrochemicals segment, meanwhile, charted a brisk 6.48% CAGR for the rest of the decade, buoyed by mega-scale ethylene, polypropylene, and aromatics plants that call for thousands of process and utility pumps. Large cracker sites often specify single-stage overhung designs for lighter hydrocarbons and multistage radials for high-head reformate circulation, driving high-mix production runs at OEM factories.

Oil and gas, despite volatile CAPEX cycles, continued to represent a significant aftermarket revenue stream given stringent uptime requirements on injection, transfer, and loading pumps. Power generation owners shifted investment toward closed-loop cooling pumps compatible with advanced ultra-supercritical boilers and toward molten-salt pumps in emerging concentrated solar power plants. Mining operations prioritized robust slurry pumps with elastomer-lined casings; downtime on a single dewatering train could stall mill throughput worth USD 0.5 million a day. Food and beverage processors requested hygienic centrifugal and lobe designs to align with FSMA rules, while pharmaceutical manufacturers leaned on diaphragm pumps offering validated clean-in-place regimes. Digital service overlays cut across all verticals, turning raw operating data into predictive work orders and reinforcing service revenue stickiness for tier-one vendors within the industrial pump market.

By Pump Orientation: Submersible Advantage Meets Surface Innovation

Submersible equipment captured 30.75% of 2025 sales, its compact footprint and noise suppression proving invaluable in dense urban utilities and underground mines. Sealed motors shielded by oil-filled chambers exhibited strong reliability, yet in-situ repairs remained expensive, pushing operators to adopt wireless temperature probes that signal seal failures before catastrophic ingress occurs. Surface-mounted pumps, though historically maintenance-friendly, benefited from a recent wave of design improvements that narrowed noise and vibration gaps while retaining easy access. Their quicker mean-time-to-repair contributed to an anticipated 9.85% CAGR, overtaking submersibles in incremental volume growth.

Sulzer expanded its Easley, South Carolina facility in 2024 to localize submersible grinder pumps meeting Build America Buy America criteria, reflecting public-sector preference for domestically sourced equipment. Concurrently, surface-pump makers integrated composite wear rings and split-case construction to curb leakage losses and simplify impeller extraction. Both orientations adopted edge analytics modules that process vibration spectrums locally, minimizing bandwidth needs while still flagging anomalies through cloud dashboards. End-users increasingly deployed mixed fleets, opting for submersibles in space-constrained shafts and surface units where footprint allowed standard maintenance bays. This pragmatic blend reinforced the diversified, application-led nature of demand that characterizes the industrial pump market.

Geography Analysis

Asia-Pacific dominated with 44.85% revenue in 2025 after decades of industrial build-out, extensive municipal upgrades, and policy-driven manufacturing localization. New ethylene cracker complexes in Fujian and large-scale desalination schemes in Australia magnified the procurement of high-efficiency multistage pumps. China’s stimulus for wastewater reuse and India’s Production Linked Incentive program for chemicals continued to channel orders toward both global and domestic pump manufacturers. Regulatory pushes around electricity intensity and carbon footprints incentivized operators to retrofit VFDs, nudging market volume toward premium-efficiency product lines within the industrial pump market.

The Middle East and Africa posted the fastest 6.05% CAGR, propelled by USD 17 billion in combined petrochemical investments across Saudi Arabia, Qatar, and the United Arab Emirates. Desalination, such as NEOM’s 1 million m³/day seawater project, demanded high-pressure duplex-steel pumps tolerant to chloride stress-corrosion. African mining expansions in Zambia and the Democratic Republic of Congo increased orders for abrasion-resistant slurry units. Local content frameworks pushed OEMs to open service hubs in Oman and South Africa, shortening turnaround times on overhauls and reinforcing brand loyalty. North America experienced a steady replacement cycle driven by water infrastructure bills, with California, Texas, and Florida aggregating the bulk of tenders for replacement centrifugal and vertical turbine pumps. Energy policy incentives supported early adoption of hydrogen electrolysis, sparking niche orders for corrosion-resistant circulation pumps. Europe’s stringent MEI regulations stimulated demand for ultra-high-efficiency designs and encouraged plant owners to reassess total-cost-of-ownership metrics. Latin America, though smaller, witnessed steady uptake in agricultural irrigation pumps and mining-related demand in Chile and Peru. Across all regions, digital service propositions featuring predictive maintenance became a decisive factor in bid evaluations, further shaping competitive standings in the industrial pump market.

Competitive Landscape

Competition remained moderately fragmented as global leaders vied with strong regional specialists that supplied application-tailored solutions and swift aftermarket responses. Honeywell’s acquisition of Sundyne in March 2025 added a premium API 610 and integrally geared turbopump portfolio to its line-up, cementing a broader critical-equipment play. Grundfos similarly bolstered its European footprint through the EUR 100 million (USD 116.92 million) takeover of Culligan’s Commercial and Industrial arm, expanding water-treatment competence across three major EU markets.[4]“Grundfos To Acquire The Commercial & Industrial Business Of Culligan,” Grundfos, grundfos.com Xylem, meanwhile, posted USD 2.1 billion in Q1 2025 revenue on the back of differentiated digital offerings that integrate smart sensors with cloud analytics, a capability that sharpened its competitive edge in retrofit projects.

Tier-one OEMs doubled down on predictive-maintenance platforms—Grundfos Machine Health and Sulzer Sense—leveraging machine-learning models to forecast bearing failures weeks in advance. The pivot elevated service margins and deepened customer stickiness, particularly in mission-critical water and chemical plants where downtime costs run into millions per day. Consolidation also trickled into the mid-tier segment: Atlas Copco acquired Kracht GmbH, and ITT folded in Danish marine-pump specialist Svanehøj, signaling appetite for niche technologies that round out cross-industry portfolios. Suppliers without digital or energy-efficient credentials lost share to innovators that blended hardware, sensors, and cloud platforms in cohesive packages—a trend that is expected to persist as ESG metrics steer procurement in the industrial pump market.

Strategic alliances emerged between pump makers and material science companies to fast-track corrosion-resistant alloys destined for green-hydrogen applications. Sulzer partnered with Outokumpu to qualify super-duplex grades against upcoming ISO 19880-3 hydrogen-compatibility standards. Elsewhere, Graco licensed transverse-flux motor patents from a European research consortium to accelerate its high-efficiency roadmap. Competitive intensity was fiercest in commoditized centrifugal lines where local producers maintained cost advantages; premium niches such as electrolyzer circulation and high-pressure reverse-osmosis feed pumps offered healthier margins and insulation from price wars. Overall, the industrial pump market rewarded companies capable of pairing energy-saving designs with data-driven service models.

Industrial Pump Industry Leaders

Flowserve Corporation

Grundfos Holding A/S

KSB AG

Sulzer Ltd

Weir Group PLC,

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Honeywell announced the acquisition of Sundyne, extending its critical equipment and aftermarket platform.

- February 2025: Groundbreaking of the USD 6.4 billion SABIC Fujian complex in China, expected to require extensive pump infrastructure.

- May 2024: Grundfos agreed to acquire Culligan’s Commercial and Industrial business in Italy, France, and the UK for over EUR 100 million (USD 113 million).

- April 2024: Saudi Aramco awarded USD 7.7 billion in EPC contracts for the Fadhili Gas Plant expansion, elevating demand for specialized pumps.

Global Industrial Pump Market Report Scope

A pump uses mechanical action to transport liquid substances. Pumping uses for industrial pumps include well water pumping, aquarium filtration, pond filtration, water cooling, and fuel injection in the automotive sector and oil and gas operations in the energy business.

The industrial pump market is segmented by type, end-user industry, and geography. The market is segmented by type into centrifugal pump, reciprocating pump, rotary pump, and other pump types. The market is segmented by end-users into oil and gas, water and wastewater, chemicals and petrochemicals, mining, power generation, and other end-user industries. The report also covers the market size and forecasts for the industrial pump market across major regions. The market sizing and forecasts have been done for each segment based on revenue (USD).

By Pump Type

| Centrifugal |

| Reciprocating |

| Rotary |

| Diaphragm |

| Progressing Cavity |

| Others |

By Power Source

| Electric |

| Diesel |

| Solar |

| Hydraulic |

| Pneumatic |

By End-user Industry

| Oil and Gas |

| Water and Waste-water |

| Chemicals and Petrochemicals |

| Power Generation |

| Mining |

| Food and Beverage |

| Pharmaceuticals |

| Pulp and Paper |

| Others |

By Pump Orientation

| Submersible |

| Surface |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Turkey |

| Israel | ||

| GCC Countries | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Pump Type | Centrifugal | ||

| Reciprocating | |||

| Rotary | |||

| Diaphragm | |||

| Progressing Cavity | |||

| Others | |||

| By Power Source | Electric | ||

| Diesel | |||

| Solar | |||

| Hydraulic | |||

| Pneumatic | |||

| By End-user Industry | Oil and Gas | ||

| Water and Waste-water | |||

| Chemicals and Petrochemicals | |||

| Power Generation | |||

| Mining | |||

| Food and Beverage | |||

| Pharmaceuticals | |||

| Pulp and Paper | |||

| Others | |||

| By Pump Orientation | Submersible | ||

| Surface | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Taiwan | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Turkey | |

| Israel | |||

| GCC Countries | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the industrial pump market size in 2026, and how fast will it grow?

The industrial pump market stood at USD 50.46 billion in 2026 and is forecast to expand to USD 63.45 billion by 2031 at a 4.69% CAGR.

Which pump type holds the largest share of the industrial pump market?

Centrifugal pumps led with 61.85% revenue share in 2025 due to their versatility in water, oil, and gas, and general industrial services.

Why are solar-powered pumps gaining prominence?

Solar units offer attractive economics for off-grid irrigation and remote water supply, driving an 11.1% CAGR through 2031 as renewable adoption accelerates.

Which end-user segment is expanding the fastest?

Chemicals and petrochemicals are projected to grow at a 6.48% CAGR, supported by mega-crackers and refinery integration projects in the Middle East and Asia-Pacific.

How are efficiency regulations affecting pump purchases?

EU MEI and US PER rules are pushing buyers to delay upgrades until compliant designs enter the market, temporarily lengthening capital-expenditure cycles but ultimately favoring high-efficiency pumps.

What role does digitalization play in the industrial pump industry?

IoT-based monitoring and predictive maintenance platforms reduce unplanned downtime and create high-margin service revenue, becoming a key differentiator among leading suppliers.

Page last updated on: