Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

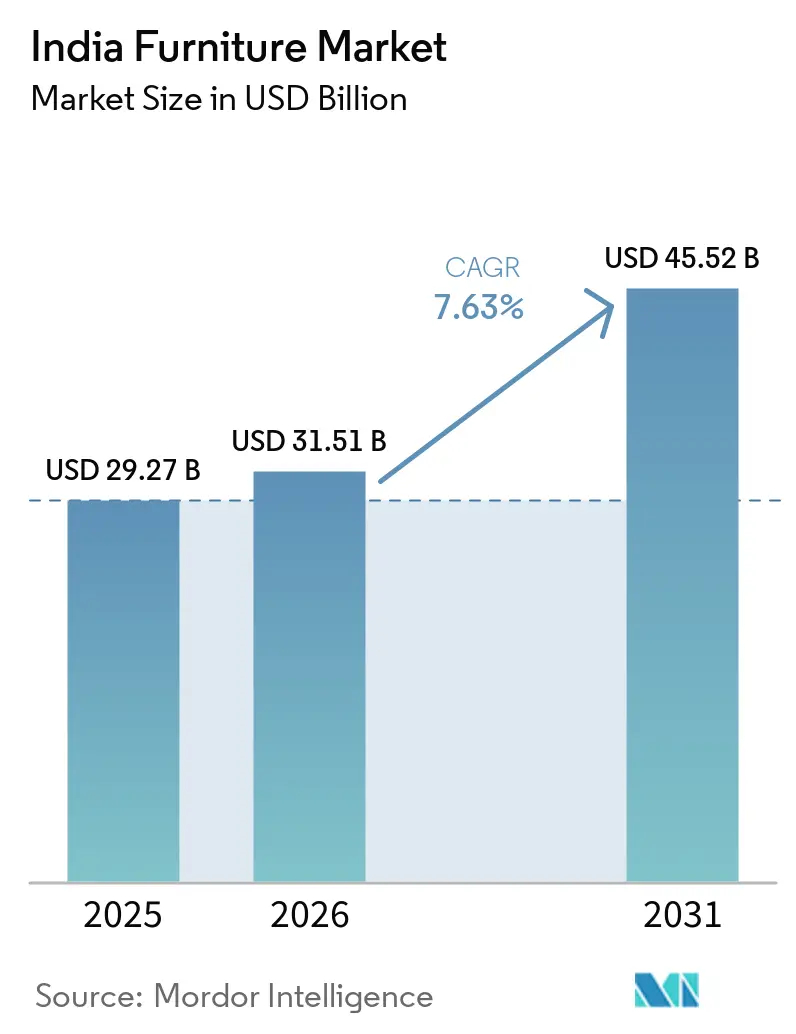

| Base Year Market Size (2025) | USD 29.27 Billion |

| Market Size (2026) | USD 31.51 Billion |

| Market Size (2031) | USD 45.52 Billion |

| Growth Rate (2026 - 2031) | 7.63% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Furniture Market Analysis by Mordor Intelligence

The India furniture market size is expected to grow from USD 29.27 billion in 2025 to USD 31.51 billion in 2026 and is forecasted to reach USD 45.52 billion by 2031 at a 7.63% CAGR over 2026-2031. The India furniture market is benefiting from structural housing programs, formalization incentives for MSMEs, and rising urban household formation, which together expand the addressable base for economy and mid-range products. The enforcement of the Furniture Quality Control Order from February 2026 is reshaping compliance, warranty, and after-sales standards, which improves access to government and institutional demand while nudging unorganized producers toward certification. Public procurement channels through the Government e-Marketplace and MSME sourcing mandates increase the share of project-based ordering and raise the bar on documentation and lifecycle costing. Sustainability criteria embedded in Indian Green Building Council guidelines, coupled with the expansion of FSC chain-of-custody certificates, support the diffusion of engineered wood, low-VOC finishes, and eco-labeled furniture in premium and institutional projects.

Key Report Takeaways

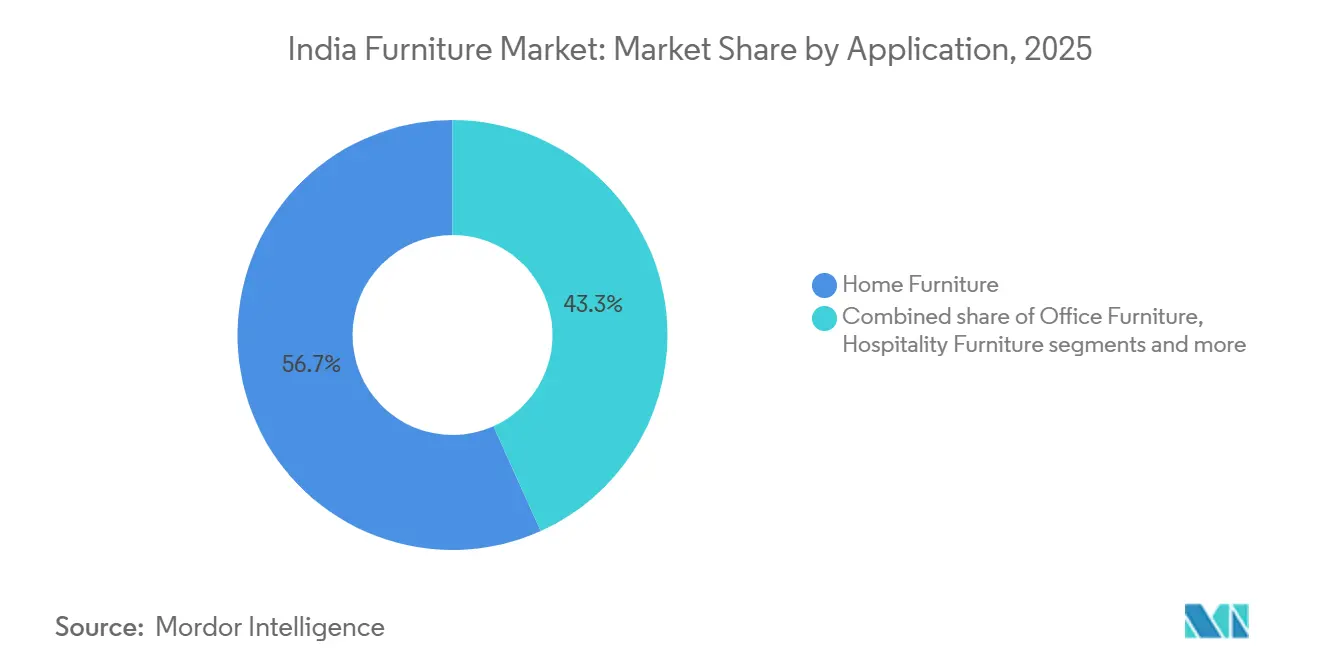

- By application, home furniture captured 56.74% of the India furniture market share in 2025, while office furniture is projected to grow at an 11.65% CAGR through 2031.

- By material, wood captured 57.35% of the India furniture market share in 2025, while metal is projected to grow at a 13.73% CAGR through 2031.

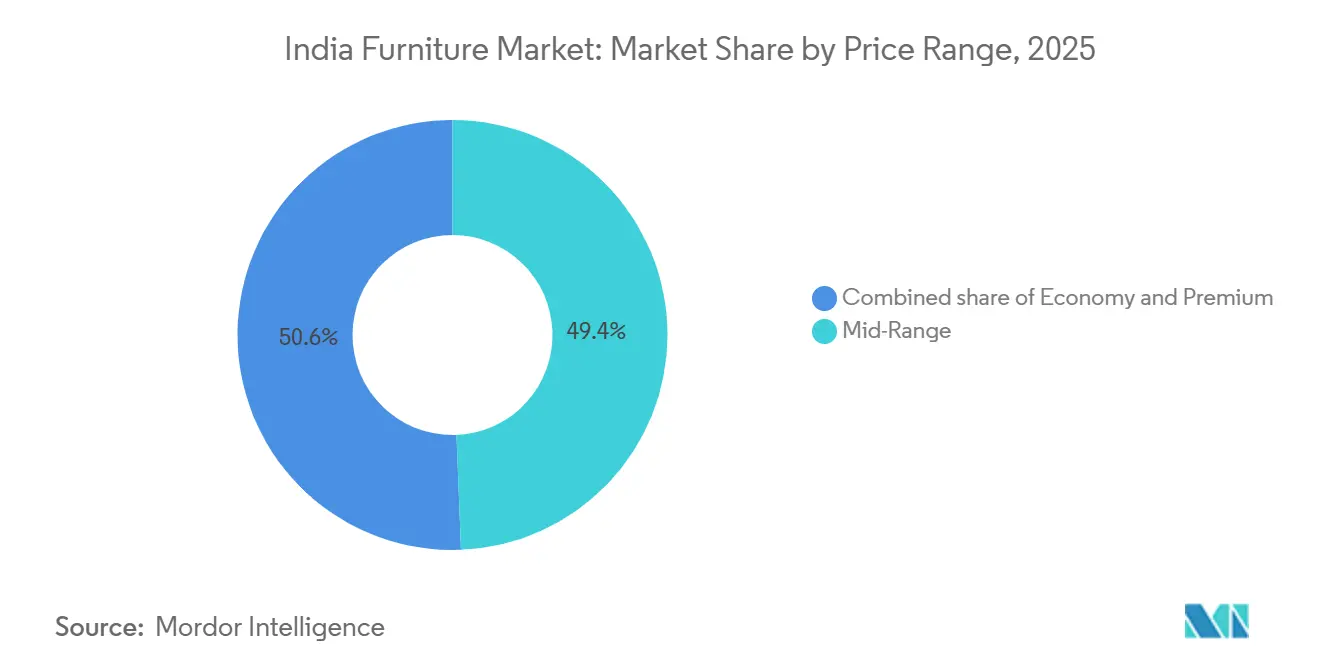

- By price range, mid-range captured 49.37% of the India furniture market share in 2025, while premium is projected to grow at a 12.23% CAGR through 2031.

- By distribution channel, B2C retail captured 68.37% of the India furniture market share in 2025, while B2B and project procurement are projected to grow at an 11% CAGR through 2031.

- By geography, South India captured 26.73% of the India furniture market share in 2025, while East India is projected to grow at an 11.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urban migration | +2.1% | National, concentrated in tier-II cities such as Surat, Indore, Lucknow, and Visakhapatnam. | Medium term (2-4 years) |

| Omnichannel and AR visualization | +1.8% | Urban metros and tier-I cities, including Delhi NCR, Mumbai, Bengaluru, Hyderabad, with spillover to tier-II cities | Short term (≤ 2 years) |

| Government housing push under PMAY | +2.3% | Pan-India with rural PMAY-G and urban EWS/LIG coverage | Long term (≥ 4 years) |

| Sustainability preference and eco-labels | +0.9% | Urban educated consumers and IGBC-certified commercial projects | Medium term (2-4 years) |

| Commercial and hospitality expansion | +1.6% | Tourism hubs and IT corridors across Goa, Kerala, Rajasthan, Bengaluru, Pune, Hyderabad | Medium term (2-4 years) |

| Rising disposable income and lifestyle upgrading | +1.4% | Urban and semi-urban middle-income households across metros and tier-II cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban Migration Elevating Demand for Furniture

India’s urban population share is on course to exceed 40% by 2030 from 34.5% in 2021, which intensifies housing formation and furnishing cycles in newer urban clusters that absorb internal migrants. Periodic Labour Force Survey records show that 18.9% of internal migrants move from rural to urban areas, translating into a steady queue of new household formations that energize the furniture industry in India. Emerging tier-II cities such as Surat, Indore, Lucknow, Jaipur, and Visakhapatnam capture an increasing share of migrant flows as manufacturing and IT services decentralize, which channels demand toward the economy and mid-range furniture suited to smaller apartments. The latest Household Consumption Expenditure Survey shows narrowing rural-urban spend gaps and a modest but consistent share for durable goods in monthly outlays, which signals rising propensity to spend on beds, wardrobes, and tables as incomes stabilize post-migration. [1]MOSPI.GOV.IN https://www.mospi.gov.in/sites/default/files/publication_reports/HCES%20FactSheet%202023-24.pdf Online shopping penetration into tier-II and tier-III locations also helps first-time buyers discover catalog options and transparent pricing, even though last-mile constraints and building access conditions keep some demand within local carpenter networks.

Surge in Omnichannel Platforms Leveraging AR/VR for See-in-Room Visualization

Retailers and marketplaces in the India furniture market have accelerated AR adoption in shopping journeys, which lowers return rates by improving pre-purchase fit assessment for sofas, beds, and storage solutions. [2]IBEF.ORG https://www.ibef.org/industry/retail-india Enterprises procure through e-portals that require BIS documentation and lifecycle cost disclosures, which favors vendors whose inventories and logistics are ERP-integrated for predictable deliveries. The Open Network for Digital Commerce onboarded furniture artisans and MSMEs under PM Vishwakarma, which expands institutional access beyond traditional distributors. The Government e-Marketplace added tens of thousands of furniture sellers and channels a sizable portion of public procurement through standardized tenders, improving discoverability for compliant MSMEs. As large-format chains and international entrants deepen local sourcing and enhance omnichannel coverage, the balance of showroom experiences and digital visualization continues to raise conversion and fulfillment predictability.

Government Housing Push PMAY Triggering Mass Residential Furniture Uptake

PMAY-Urban reported 96.32 lakh completed homes and PMAY-Gramin reported 2.92 crore completed homes as of late 2025, which expands the base of first-time buyers for essential furniture such as cots, storage, and basic kitchen platforms. [3]PMAYMIS.GOV.IN https://pmaymis.gov.in/, PIB.GOV.IN https://www.pib.gov.in/PressReleasePage.aspx?PRID=2210378®=3&lang=1 The Union Cabinet approved PMAY-U 2.0, targeting 1 crore additional urban households through 2029 with central assistance of Rs 2.30 lakh crore, which supports demand visibility for the economy and mid-range furnishings in the India furniture market. Beneficiary profiles in EWS and LIG categories weigh durability and price over heirloom aesthetics, which steers spending toward metal cots and engineered-wood wardrobes with practical finishes. The PM Vishwakarma scheme has enabled carpenters to upgrade tools and access collateral-free finance, which reduces cycle times for made-to-order items and supports village-level supply where organized retail is thin. As sanctioned-to-completion timelines normalize and families settle post-relocation, deferred purchases for sofas, dining sets, and modular kitchen components begin to accelerate in years two and three of occupancy.

Sustainability Preference Spurring Engineered-Wood and Eco-Labeled Products

Growth in FSC-certified areas and chain-of-custody certifications, along with steady IGBC adoption, strengthens the premium and institutional shift toward low-emission substrates and finishes. [4]FSC.ORG https://asiapacific.fsc.org/fsc-india IGBC guidelines specify thresholds for indoor emissions in seating and system furniture, which has widened adoption of E1 or E2 adhesives and low-TVOC coatings in projects that target Gold or Platinum certifications. The Furniture Quality Control Order and BIS standards align with this trajectory by raising conformance on safety and durability across chairs, desks, storage, and beds. Corporate and banking facilities that earn Green Interiors ratings offer visible case studies for procurement teams, and this signals a durable shift in specifications for future fitouts. While eco-label premiums continue to limit mass-market penetration, the certification pathway has consolidated demand in the upper decile of households and in IGBC-certified buildings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity and GST slab | -1.4% | National, acute in rural and tier-III markets | Short term (≤ 2 years) |

| Certified timber supply bottlenecks | -0.8% | North India import-reliant corridors and Kerala rubber-wood zones | Medium term (2-4 years) |

| High reverse-logistics cost for online heavy-bulk deliveries | -0.6% | Urban tier-II and tier-III cities | Short term (≤ 2 years) |

| Large, unorganized sector dominance | -0.9% | Pan-India with concentration in UP, Bihar, and Rajasthan rural clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity and GST Slab Curtailing Premium Category Penetration

Household spending patterns show durable goods at a modest share of monthly outlays for both rural and urban consumers, which reinforces price sensitivity when households prioritize education and healthcare. The standard 18% GST on most furniture raises landed prices and discourages lower-income cohorts from upgrading beyond engineered wood, while bamboo and cane furniture attract a lower slab under specific headings. Recent GST Council decisions have adjusted rates for some construction-linked goods and bamboo items, yet standard furniture remains at 18%, which sustains psychological price thresholds for big-ticket purchases. Trade bodies have argued for a 12% slab to improve competitiveness and margin headroom amid higher raw material and energy costs. With headline inflation moderating and housing inflation steady, disposable income support has improved, yet the step-up to premium seating and solid-wood cabinetry still faces resistance in the India furniture industry.

Supply-Chain Bottlenecks in Certified Timber Raising Input Volatility

India’s timber supply draws from managed forests, farm forestry, and imports, yet traceability gaps in agroforestry and compliance burdens on imports create periodic volatility in input costs. Plant quarantine requirements for imported timber and phytosanitary treatments add time and cost, which complicates planning for MSMEs serving time-bound project orders. Regulatory exemptions for furniture units using sawn timber and imported wood reduce licensing burdens, but they still require registration with state forest departments and sensitivity to siting rules. The trade compliance framework has tightened for species under CITES listings, which increases documentation and legality verification requirements for exporters. Regional clusters dependent on specific hardwoods report price swings when auction schedules change or when imports slow, which affects both cost and delivery timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Office Infrastructure Upgrades Outpace Home Replacement Cycles

Home furniture holds a 56.74% market share in 2025 within the India furniture market, driven by bed, wardrobe, dining, and sofa requirements across tens of millions of households that have completed PMAY homes or moved into new urban dwellings. Modular kitchens are gaining traction in apartments larger than 900 square feet, with expanding adoption in metro markets that support specialist installers and verified component supply. Sofas and dining sets serve the household shift from joint family to nuclear arrangements in limited space, which changes configurations toward compact sectionals and 4- to 6-seater options. Outdoors and balcony furniture are nascent but growing with urban apartment layouts that allocate small outdoor areas, which sustains demand for weather-resistant finishes. The PMAY completion base continues to create a replacement cycle for essential items within 8–10 years, reinforcing recurring demand in the economy and mid-range price points for the furniture industry in India.

Office furniture, the fastest-growing application segment, is projected to grow at 11.65% CAGR through 2031 within the India furniture market, supported by steady office absorption and hybrid work-driven reconfiguration toward height-adjustable desks and modular collaboration spaces. Government and public-sector procurement through GeM adds a predictable workflow of tenders that specify BIS compliance and service-level commitments, which creates an advantage for organized suppliers. Seating tends to command the highest share within office furniture due to per-employee requirements, while storage and conference solutions expand with new fitout patterns. Hospitality projects resumed standardized procurement for beds and seating with enforceable warranties and conformity to fire safety norms, which stabilizes supplier funnel management in the India furniture market. Educational and healthcare facilities add incremental growth through centrally funded programs and state infrastructure upgrades, which require durable designs and compliant finishes.

By Material: Engineered Substrates Displace Solid Wood as Timber Scarcity Intensifies

Wood maintains a 57.35% market share in 2025 within the India furniture market, yet the mix tilts toward engineered boards because of cost, consistency, and the regulatory environment that favors certified inputs. BIS Quality Control Orders for plywood and wood-based boards standardize minimum performance for inputs like MDF, plywood, and particle board, which improve product reliability. IGBC criteria and FSC chain-of-custody systems reinforce the shift to lower-emission adhesives and verifiable sourcing pathways in premium and institutional demand. Engineered boards deliver predictable machineability and finish quality, which reduces rework and enables modular cabinetry at scale for mid-range wardrobes and kitchens. Solid wood continues to hold cultural appeal, but its usage growth is moderated by timber volatility and export compliance for specific species, which raises the comparative appeal of engineered alternatives in the India furniture market.

Metal is projected to grow at 13.73% CAGR through 2031, driven by urban apartment constraints that favor slimmer profiles for cots and by durability preferences in hospitality and office environments where maintenance must be fast and uniform. Steel frames with powder-coated finishes deliver long service life with wipe-clean surfaces, which fit high-traffic areas and budget-conscious institutional buyers. Plastic and polymer products remain relevant in outdoor seating and economic indoor use, though environmental concerns and GST parity limit premium substitution. Bamboo and cane inputs benefit from clarified regulatory treatments and cluster support in the Northeast, which facilitates chairs, stools, and accent pieces with lighter weights and lower tooling costs. Standardization through the Wood-Based Boards and Plywood QCOs raised quality baselines and tempered low-quality imports, which supports domestic capacity utilization.

By Price Range: Premium Gains as Institutional LEED Projects Mandate Eco-Certifications

In price range segments, the mid-range captured 49.37% of the market size in 2025 with average selling prices that align with middle-income affordability and financing options through retail partners and lenders. Household expenditure statistics show durable goods at a steady share of monthly spend across urban and rural cohorts, which stabilizes the core for mid-range wardrobes, sofas, and beds. Specialist chains and marketplaces support this segment with EMI and buy-now-pay-later solutions that smooth cash flows for higher-ticket living and bedroom sets. The economy segment is deeper in rural and tier-III markets, where durability and price arbitrage across metal cots and engineered-wood storage are often purchased post-PMAY possession. Institutional policies that encourage female ownership in EWS and LIG housing shape household preferences for durable and functional items as the first wave of purchases.

Premium is projected to grow at 12.23% CAGR through 2031, lifted by corporate headquarters and hospitality projects that specify low emissions, eco-labels, and long warranties in line with IGBC and international benchmarks. GreenPro and FSC pathways consolidate the vendor base around organized firms that can amortize certification costs across larger volumes and stable margins. Premium residential projects with higher budgets continue to adopt imported veneers, bespoke walk-in wardrobes, and modular kitchens that align with aspirational design. Lower inflation supports discretionary upgrades in metro and emerging city segments as incomes rise, which encourages experiments with new materials and integrated lighting or ergonomic features. Over time, certification-driven standardization is expected to diffuse some premium features into higher mid-range offerings in the India furniture market.

By Distribution Channel: GeM Institutionalizes B2B While Unorganized Retail Resists E-Commerce Encroachment

B2C retail captured 68.37% of the India furniture market share in 2025, anchored by specialty stores and home centers where touch-and-feel preferences drive conversion for larger-ticket categories. Omnichannel journeys and AR-based visualization strengthen discovery and fit validation, which trims return rates and improves checkout confidence on marketplaces. Unorganized retailers in smaller towns continue to command loyalty on customization and quick delivery, which remains a structural factor in B2C behavior. Online penetration grows in double digits but still faces last-mile and reverse logistics challenges for heavy-bulk items despite steady improvements in service design. Large-format entrants are expanding online coverage and local sourcing to improve availability in more cities, which deepens the reach of organized B2C within the India furniture market.

B2B and project procurement is projected to grow at an 11% CAGR through 2031, buoyed by standardized tenders from hotels, offices, hospitals, and education institutions that require compliance documentation, scale production, and installation capabilities. The Government e-Marketplace and MSME procurement policies have improved transparency for buyers and have encouraged more MSMEs to formalize where feasible. Project buyers enforce warranty and service terms with site-level scheduling, which naturally filters toward vendors with established networks and certified products. B2B growth outpaces B2C as larger developers and corporate tenants move from fixed cubicles to modular collaborative spaces, which refreshes furniture footprints and rebalances channel mix in the Indian furniture industry. Over the forecast, project pipelines, smart city works, and public infrastructure programs maintain a steady base for institutional procurement.

Geography Analysis

South India commands a 26.73% share in 2025 within the India furniture market, supported by dense IT corridors and manufacturing clusters in Karnataka, Tamil Nadu, and Kerala that strengthen both demand and supply ecosystems. State and district cluster programs nurture facility upgrades, common service centers, and capacity additions, which improve quality and delivery reliability for domestic and export buyers. The design and machinery ecosystem in Bengaluru and Chennai underpins the adoption of advanced edge-banding, CNC routing, and spray finishing solutions, which lifts output uniformity and reduces rework. South India’s historical growth outpaced the national average due to office fitout cycles and rubber-wood availability, but the forward outlook moderates as growth diffuses to tier-II locations. As PMAY completions and institutional procurement spread into second-tier cities, South India continues to lead on capability while growth in other regions converges.

East India is projected to grow at an 11.46% CAGR, supported by infrastructure catch-up in Kolkata and other urban nodes, plus PMAY-G delivery that generates essential furniture demand across rural districts. State-level MSME counts and cluster initiatives across West Bengal, Bihar, Jharkhand, Odisha, and the Northeast point to rising formal participation and targeted support for bamboo and wood-based units. Northeast bamboo resources benefit from regulatory clarity for processing units, which promotes chair and stool production with supportive common facility centers under SFURTI. Railway, metro, and smart city projects in the region further stimulate institutional furniture purchases for public offices and community spaces, which improves order visibility for compliant suppliers. As logistics corridors improve and private construction accelerates, East India narrows its gap with the South and West in the India furniture market.

West India and North India together account for a large share of organized capacity, exports, and institutional consumption, with Maharashtra, Gujarat, Rajasthan, Delhi NCR, and Uttar Pradesh anchoring demand and supply. Maharashtra’s manufacturing profile includes furniture as a focus sector, while Gujarat and Rajasthan host metal and wooden furniture hubs that serve both domestic distribution and export channels. North India’s growth is tempered by timber volatility and import constraints, but poplar and farm forestry in Punjab and Haryana reduce raw material friction for selected units. Public procurement and corporate fit-outs in Delhi NCR maintain steady project pipelines, which support BIS-compliant vendors that can execute site services. Central India adds incremental share through PMAY-G housing and tribal artisan clusters that bridge into formal channels over time, which broadens the geographic dispersion of the India furniture market.

Competitive Landscape

The India furniture market remains highly fragmented. Organized firms differentiate through BIS compliance, omnichannel coverage, installation networks, and warranty enforcement that align with government and corporate procurement expectations. Unorganized workshops retain agility on bespoke dimensions, material mixes, and festival-timed deliveries, which preserves their relevance even as formal channels scale. Certification and audit costs remain a hurdle for many micro units, although Udyam registrations and PM Vishwakarma support gradually expand the formal base. As project-led demand rises, organized suppliers capture a larger portion of institutional orders, while unorganized players continue to dominate neighborhood retail in the India furniture market.

International and domestic leaders have accelerated investments and local sourcing to improve availability and cost positions across more Indian cities. International retailers deepen omnichannel and logistics to increase coverage and reduce delivery friction, while domestic incumbents scale specialty store formats and showrooms. Office furniture specialists are aligning with BIS and BIFMA benchmarks for ergonomics as hybrid work stabilizes, which supports demand for height-adjustable and collaborative systems. Premium segments lean on eco-labels to win IGBC-linked projects, which concentrate orders among vendors with GreenPro and FSC pathways. Export growth in wood-based products is supported by compliance with new regulatory regimes and by digital traceability pilots that reduce legality risks and enhance buyer confidence.

Strategy patterns include backward integration into panels and polymers, robotic edge-banding and CNC investments to improve tolerances and coating uniformity, and take-back pilots that align with circular economy goals. Banks and service companies with IGBC-certified interiors demonstrate how procurement preferences influence supply, which reinforces eco-labeled adoption at scale. Marketing acquisition costs in online D2C continue to rise, which drives consolidation and hybrid showroom models for categories that benefit from touch-and-feel experiences. Government schemes for clusters and technology upgradation reduce the capital burden for micro exporters to adopt kiln-drying and CNC capabilities, which raises productivity and consistency. As compliance windows close for the Furniture QCO in 2026, the India furniture market is set for a more defined separation between certified organized players and informal producers that focus on local customization.

India Furniture Industry Leaders

Zuari Furniture

IKEA

Godrej Interio

Nilkamal Limited

Durian Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: IKEA announced a second-phase investment that strengthens local sourcing, logistics, and omnichannel expansion to widen coverage to more Indian cities, building on earlier commitments in the country.

- February 2025: DPIIT notified the Furniture Quality Control Order mandating ISI certification for work chairs, general-purpose chairs, tables, storage units, beds, and bunk beds, with enforcement from February 13, 2026, and specified MSME exemptions.

- June 2025: Pepperfry raised INR 430 million (USD 4.91 million) from existing investors for studio expansion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the India furniture market as the total revenue generated from the sale of newly manufactured seating, sleeping, storage, work, and decorative units across wood, metal, plastic, and engineered composites distributed through physical stores, digital platforms, and direct project channels to residential, commercial, and institutional customers.

Scope Exclusion: Built-in carpentry, second-hand goods, and antique resale are not covered.

Segmentation Overview

- By Application

- Home Furniture

- Tables (side tables, coffee tables, dressing tables, etc.)

- Beds

- Wardrobes

- Sofas

- Dining Tables/Dining Sets

- Kitchen Cabinets

- Other Home Furniture (bathroom furniture, outdoor furniture, etc.)

- Office Furniture

- Chairs

- Tables

- Storage Cabinets

- Desks

- Sofas and Other Soft Seating

- Other Office Furniture

- Hospitality Furniture

- Educational Furniture

- Healthcare Furniture

- Other Applications (public places, retail malls, government offices, etc.)

- Home Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B/Project

- B2C/Retail

- By Geography

- North India

- West India

- South India

- East India

Detailed Research Methodology and Data Validation

Primary Research

Interviews with mid-scale manufacturers, plywood processors, large e-commerce retailers, and regional trade bodies in North, West, and South India give us current price points, channel margins, and informal-sector penetration that secondary data miss, letting us refine assumptions and validate every interim output.

Desk Research

We begin with national data sets from the Ministry of Commerce & Industry, CMIE, the GST Network, and the Trade Promotion Council of India that quantify production, import, and GST-paid sales of HS 9401-9403 items. Macro signals such as disposable income and housing completions are added from Reserve Bank of India releases and Census projections.

Mordor's analysts then tap D&B Hoovers and Dow Jones Factiva for company financials, while technical shifts are traced through Bureau of Indian Standards notifications and peer-reviewed journals. The sources named are illustrative; many additional open and licensed references underpin the evidence base.

Market-Sizing & Forecasting

A top-down construct converts household counts and commercial floor-space completions into demand pools, which are then split by price tier and material. Supplier roll-ups and sampled average selling prices act as bottom-up checks before totals are locked. Key variables include urban housing completions, furniture GST filings, plywood output index, online furniture GMV, and real disposable income per capita. Multivariate regression projects each driver, and region-specific penetration ratios bridge gaps where channel data prove patchy.

Data Validation & Update Cycle

We run variance screens against independent trade and macro series, escalate anomalies for analyst review, and re-contact respondents when deviations breach thresholds. Reports refresh annually, with interim passes for material events, ensuring clients receive the latest validated view.

Why Mordor's India Furniture Market Baseline Earns Trust

We observe that published estimates often diverge because firms vary in scope, data cadence, and exchange-rate treatment.

Mordor Intelligence currently values the market at USD 29.97 billion for 2025. External publications place the size between USD 23.8 billion and USD 30.6 billion for recent years. The widest gaps arise when others confine coverage to household items, assume uniform margins for the vast unorganized tier, or extend a single growth curve from pandemic troughs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 29.97 Bn (2025) | Mordor Intelligence | - |

| USD 23.8 Bn (2024) | Global Consultancy A | Household scope only; unorganized tier excluded |

| USD 30.6 Bn (2025) | Industry Analyst B | Producer revenue unadjusted for retail mark-ups; single growth curve |

The comparison shows that Mordor's disciplined scope selection, variable-level audits, and yearly refresh deliver a balanced, transparent baseline that decision-makers can track and replicate with confidence.

Key Questions Answered in the Report

What is the India furniture market size and growth outlook to 2031?

The India furniture market size is USD 31.51 billion in 2026 and is projected to reach USD 45.52 billion by 2031 at a 7.63% CAGR.

Which application segments lead demand within India’s furniture sector?

Home furniture leads with 56.74% share in 2025, while office furniture records the fastest growth at 11.65% CAGR through 2031 due to hybrid work and institutional procurement.

How are regulations affecting the India furniture market?

BIS’s Furniture QCO, effective in 2026, mandates ISI certification for key categories, raising quality and compliance thresholds for public and corporate procurement.

What materials are gaining traction in the India furniture market?

Engineered wood boards and metal frames are gaining share, supported by BIS standards, IGBC low-emission norms, and FSC traceability in premium and institutional projects.

Which regions will grow fastest in India’s furniture demand?

East India is projected to grow at an 11.46% CAGR on infrastructure catch-up and PMAY-led housing, while South India continues to anchor capability with a 26.73% share in 2025.

Page last updated on: