Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

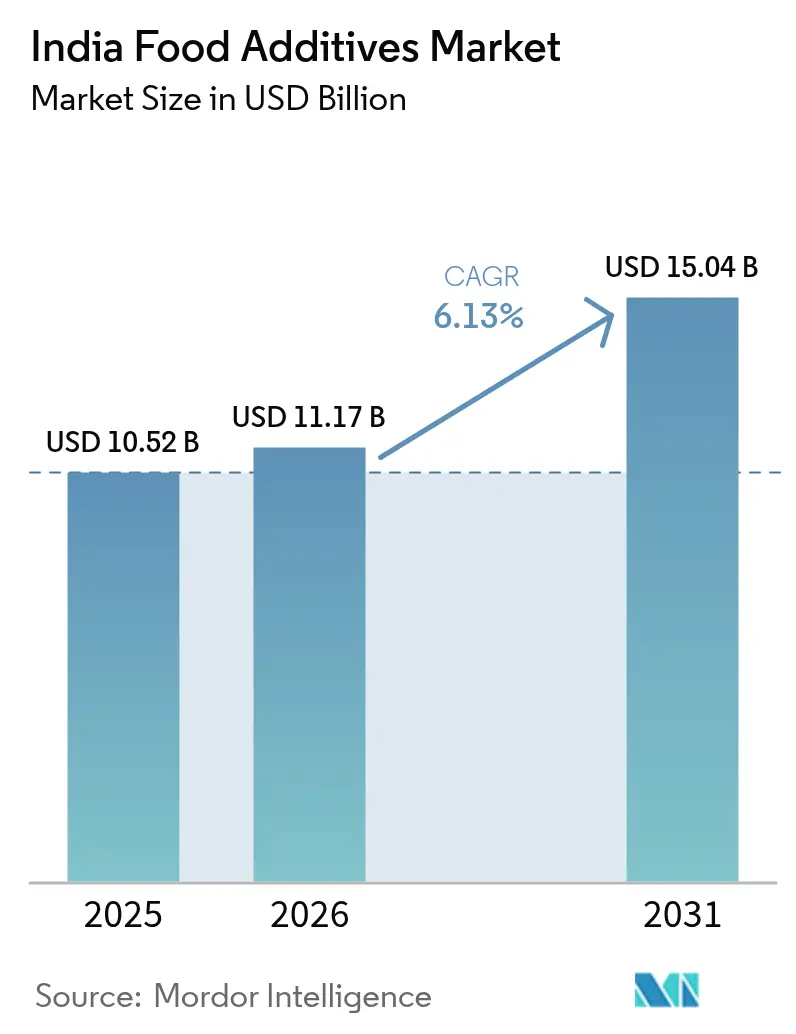

| Base Year Market Size (2025) | USD 10.52 Billion |

| Market Size (2026) | USD 11.17 Billion |

| Market Size (2031) | USD 15.04 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Food Additives Market Analysis by Mordor Intelligence

The India food additives market size is expected to grow from USD 10.52 billion in 2025 to USD 11.17 billion in 2026 and is forecast to reach USD 15.04 billion by 2031 at 6.13% CAGR over 2026-2031. Urban incomes in India are rising, dietary habits are shifting, and government incentives for food processing remain steadfast, all driving the market's expansion. Manufacturers are ramping up capacity, responding to the needs of packaged foods, quick-service restaurants, and e-commerce grocery platforms. These sectors demand solutions that enhance shelf life, optimize texture, and ensure consistent taste. Concurrently, as consumers become more discerning about labels, there's a noticeable shift in demand towards plant-based colorants, natural sweeteners, and preservatives derived from fermentation. With technology adoption, from AI-assisted formulations to enzyme fermentation, producers are not only boosting yields but also adhering to stricter quality standards. Despite challenges like fluctuating raw material costs and evolving safety regulations, these trends ensure the Indian food additives market continues its steady growth.

Key Report Takeaways

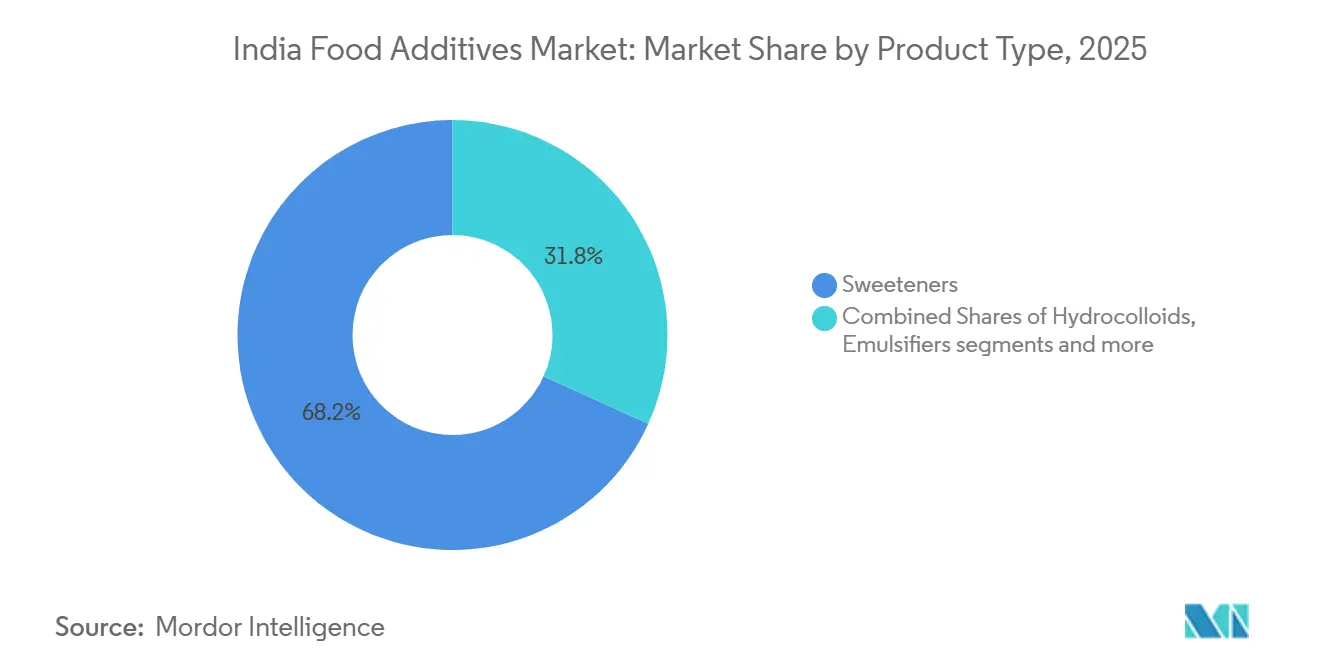

- By product type, sweeteners led with 68.23% of the Indian food additives market share in 2025, while food colorants are projected to expand at a 7.61% CAGR through 2031.

- By source, natural ingredients commanded 54.15% of the Indian food additives market in 2025 and are forecast to advance at a 7.46% CAGR between 2026 and 2031.

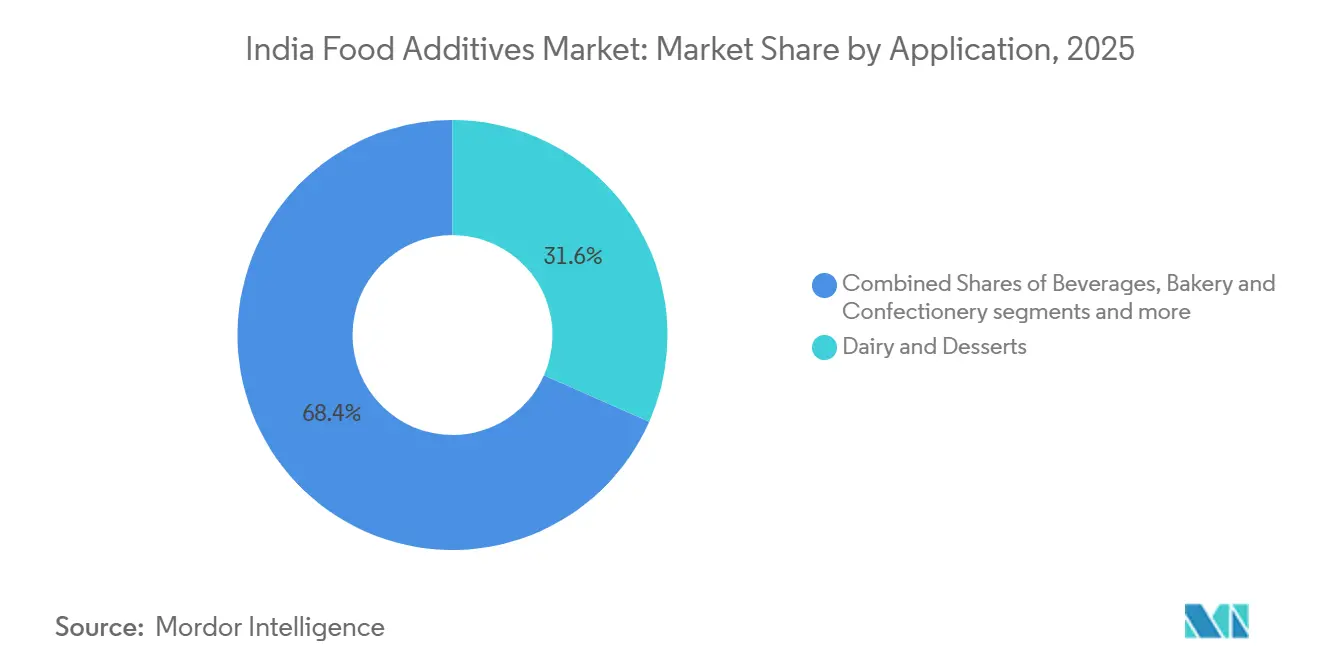

- By application, dairy and desserts accounted for a 31.61% share of the Indian food additives market in 2025; beverages represent the fastest-growing application and are poised for a 7.07% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Food Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for processed and convenience foods | +1.2% | National, with concentration in metro cities and tier-1 urban centers | Medium term (2-4 years) |

| Rising demand for natural, clean-label, and organic food additives | +1.5% | National, early adoption in Mumbai, Delhi NCR, Bengaluru, Pune | Long term (≥ 4 years) |

| Government initiatives supporting food processing industry growth | +1.0% | National, with manufacturing hubs in Gujarat, Maharashtra, Tamil Nadu, Andhra Pradesh | Short term (≤ 2 years) |

| Technological advancements in food processing | +0.8% | National, led by large-scale processors in Gujarat, Karnataka, Telangana | Medium term (2-4 years) |

| Increasing consumption of bakery and confectionery products | +0.7% | National, urban and semi-urban markets | Medium term (2-4 years) |

| Increasing health awareness boosting low-fat and fortified products | +0.9% | National, premium segments in metro cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for processed and convenience foods

Urbanization and the rise of dual-income households are significantly altering consumption trends, leading to an increased allocation of household food budgets towards ready-to-eat meals, packaged snacks, and instant mixes. The Ministry of Food Processing Industries highlighted a notable growth in the sector's GDP contribution, which rose to 8.6% in the fiscal year 2024-2025, compared to 8.2% in 2022-2023[1]Source: Ministry of Food Processing Industries, “Expansion of Food Processing Infrastructure through MoFPI Schemes”, pib.gov.in. This growth reflects a swift and widespread adoption of preservatives, emulsifiers, and flavor enhancers, which not only extend shelf life but also ensure consistent sensory quality across extensive distribution networks. As e-commerce continues to penetrate tier-2 and tier-3 cities, there is a growing demand for products with enhanced ambient stability. To meet this demand, manufacturers are increasingly incorporating additives such as potassium sorbate, sodium benzoate, and natural rosemary extracts into their product formulations. Additionally, the rise of quick-commerce platforms, which promise grocery deliveries within 10-15 minutes, is inadvertently driving greater reliance on these additives. This trend is primarily due to the need for suppliers to maintain product integrity across multiple handling touchpoints in the supply chain.

Rising demand for natural, clean-label, and organic food additives

Rising demand for natural, clean-label, and organic food additives is emerging as a significant growth driver in the India food additives market. Increasing health awareness and preference for minimally processed foods are encouraging consumers to scrutinize ingredient labels more closely. Consumer skepticism toward synthetic additives is compelling brands to reformulate with plant-derived alternatives, even when cost premiums reach 20–30%, reflecting a strong shift toward perceived safety and transparency. Regulatory developments are further reinforcing this transition. The 2024 amendments by FSSAI to the Food Products Standards and Food Additives Regulations tightened permissible limits for certain synthetic colors and mandated clearer labeling of preservatives, accelerating the shift toward natural solutions[2]Source: Food Safety and Standards Authority of India, “Compendium_Food_Additives_Regulations”, fssai.gov.in. Food manufacturers are proactively aligning formulations with evolving compliance standards to mitigate regulatory risks and enhance brand positioning. Additionally, the expansion of modern retail and premium health-focused product lines is strengthening demand for clean-label ingredients across urban and semi-urban markets.

Government initiatives supporting food processing industry growth

Government initiatives supporting the food processing industry are significantly driving growth in the India food additives market. Policy support aimed at strengthening domestic manufacturing and value addition is creating a favorable ecosystem for ingredient suppliers and processors. The Union Budget 2025–2026 allocated INR 1,200 crore (approximately USD 144 million) for the second phase of the Production Linked Incentive (PLI) scheme, with a focused emphasis on ingredient manufacturing and cold-chain infrastructure development[3]Source: Union Budget, “Union Budget Documents 2026-2027”, https://www.indiabudget.gov.in/. This allocation is expected to enhance local production capacities for specialty additives and reduce import dependence. Additionally, under the Pradhan Mantri Formalisation of Micro Food Processing Enterprises (PMFME) scheme, micro-enterprises are benefiting from credit-linked subsidies that facilitate access to advanced processing equipment such as spray dryers, homogenizers, and blending systems. This development is democratizing the adoption of functional ingredients, including enzyme-based dough conditioners and natural antioxidants, which were previously limited to large-scale manufacturers. Improved access to modern processing technologies is enabling smaller players to enhance product quality, extend shelf life, and meet regulatory standards.

Technological advancements in food processing

Technological advancements in food processing are playing a crucial role in driving the India food additives market. The adoption of advanced processing technologies such as spray drying, microencapsulation, high-pressure processing, and cold-chain optimization is enhancing the stability, functionality, and shelf life of food products. These innovations are increasing the demand for specialized additives, including emulsifiers, stabilizers, enzymes, and natural preservatives, to maintain product consistency and quality. Automation and digital monitoring systems are enabling precise ingredient dosing and quality control, thereby improving formulation efficiency and reducing wastage. The growth of ready-to-eat, convenience, and fortified food segments is further accelerating the need for functional additives that can withstand complex processing conditions. Additionally, advancements in extraction and fermentation technologies are supporting the commercial scalability of plant-based and clean-label additives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety regulations and compliance costs | -0.9% | National, with higher impact on small and medium enterprises | Short term (≤ 2 years) |

| Volatility in raw material prices | -0.7% | National, particularly affecting guar gum, pectin, gelatin suppliers | Short term (≤ 2 years) |

| Growing consumer preference for additive-free products | -0.5% | National, concentrated in premium urban segments | Long term (≥ 4 years) |

| Supply chain disruptions affecting ingredient availability | -0.4% | National, with spillover effects from global logistics constraints | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent food safety regulations and compliance costs

Stringent food safety regulations and rising compliance costs pose a significant restraint to the India food additives market. Regulatory oversight by authorities such as the Food Safety and Standards Authority of India (FSSAI) requires manufacturers to adhere to strict permissible limits, labeling requirements, and quality standards for additives. Frequent amendments to food safety regulations necessitate continuous reformulation, documentation updates, and product testing, increasing operational complexity. Compliance with evolving standards often requires investment in advanced testing laboratories, traceability systems, and third-party certifications, thereby raising production costs. Small and medium-sized enterprises (SMEs) face greater challenges in meeting these requirements due to limited financial and technical resources. Delays in regulatory approvals for new additives or novel ingredients can further slow product innovation and time-to-market.

Volatility in raw material prices

Volatility in raw material prices represents a key restraint in the India food additives market. Many additives, particularly natural colors, sweeteners, starch derivatives, and flavoring agents, are derived from agricultural commodities such as corn, sugarcane, turmeric, beetroot, and other crops. Fluctuations in agricultural output due to unpredictable weather patterns, monsoon variability, and climate change significantly impact raw material availability and pricing. Global supply chain disruptions, currency fluctuations, and geopolitical tensions further contribute to cost instability, especially for imported specialty ingredients and intermediates. Rising energy, transportation, and packaging costs also add pressure to overall production expenses. This pricing volatility reduces margin predictability for manufacturers and complicates long-term supply contracts with food processing companies. Small and medium-sized players are particularly vulnerable to sudden cost escalations, which may limit their competitiveness. Consequently, persistent raw material price fluctuations can constrain profitability and investment capacity within the sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sweeteners Anchor Market, Colorants Surge

Sweeteners accounted for the largest share of the India food additives market in 2025, capturing 68.23% of the total market revenue. This dominant position reflects their widespread use across multiple food and beverage categories, including packaged foods, carbonated drinks, dairy products, bakery items, and confectionery. The growing consumer preference for low-calorie and sugar-free alternatives has significantly contributed to the sustained demand for both natural and artificial sweeteners. Additionally, rising health awareness regarding diabetes, obesity, and lifestyle-related disorders has encouraged manufacturers to reformulate products with reduced sugar content. Food processing companies are increasingly incorporating high-intensity sweeteners and sugar substitutes to meet regulatory guidelines and evolving consumer expectations.

Food colorants are projected to register the fastest growth within the India food additives market, expanding at a CAGR of 7.61% through 2031. This accelerated growth is primarily driven by rising demand for visually appealing and aesthetically enhanced food products. As competition intensifies in packaged foods and beverages, manufacturers are leveraging vibrant and innovative colors to differentiate their products and strengthen brand appeal. The increasing popularity of ready-to-eat meals, bakery products, confectionery, and flavored beverages is further boosting the consumption of color additives. Moreover, the shift toward natural and plant-based colorants, in response to clean-label trends and consumer safety concerns, is creating new growth opportunities within the segment.

By Source: Natural Additives Command Premium, Synthetic Holds Cost Edge

In 2025, the Natural segment is poised to command a 54.15% market share and lead the growth trajectory with a 7.46% CAGR extending through 2031. This trend underscores a pronounced market pivot towards clean-label ingredients, spurred by health-conscious consumers and bolstered by regulatory endorsements for natural alternatives. Such a commanding position highlights consumers' readiness to invest in premium natural additives, with organic and plant-based components fetching 20-30% price surcharges over their synthetic counterparts. Yet, synthetic additives continue to hold a robust market stance, leveraging cost benefits and well-entrenched supply chains, especially in budget-sensitive sectors like bulk food processing and industrial baking.

Advancements in biotechnology are paving the way for cost-competitive natural additive production. Fermentation techniques are now yielding natural substitutes that rival the performance of synthetic additives. Industry players, such as DSM-Firmenich, are channeling investments into biotechnology platforms dedicated to natural ingredient synthesis. Concurrently, local manufacturers are honing extraction techniques for native plants and herbs. The regulatory landscape is increasingly tilting in favor of natural ingredients. For instance, FSSAI has expedited the approval process for plant-based additives, albeit with rigorous testing mandates for synthetic ones. Furthermore, the global export market is amplifying the shift towards natural additives, as overseas buyers, particularly from developed nations, are prioritizing these ingredients to align with evolving consumer preferences.

By Application: Dairy Dominates, Beverages Accelerate

By application, the dairy and desserts segment accounted for the largest share of the India food additives market in 2025, contributing 31.61% of total revenue. This strong position is primarily driven by the extensive use of additives such as stabilizers, emulsifiers, sweeteners, flavors, and colorants in products including ice cream, yogurt, flavored milk, puddings, and traditional dairy-based sweets. The growing demand for value-added and premium dairy products has further intensified the need for functional additives that enhance texture, shelf life, taste, and visual appeal. Rapid urbanization and rising disposable incomes have also supported higher consumption of packaged dairy desserts across metropolitan and tier-II cities. Additionally, increasing cold chain infrastructure and organized retail expansion have improved product availability and distribution reach.

The beverages segment is projected to witness the fastest growth in the India food additives market, registering a CAGR of 7.07% through 2031. This growth is largely fueled by rising consumption of carbonated soft drinks, fruit juices, functional beverages, sports drinks, and ready-to-drink teas and coffees. Increasing health awareness has encouraged manufacturers to introduce fortified, low-sugar, and natural-ingredient-based beverages, thereby driving demand for specialized additives such as natural sweeteners, preservatives, and colorants. The expanding young population and evolving lifestyle patterns have also accelerated on-the-go beverage consumption. Furthermore, aggressive marketing strategies and product innovation, including new flavors and clean-label formulations, are strengthening market penetration.

Geography Analysis

The India food additives market reflects strong concentration in economically advanced and industrialized regions. Western India, particularly states such as Maharashtra and Gujarat, represents a major hub due to its well-established food processing industry and strong manufacturing infrastructure. The presence of large-scale processing units, export-oriented production facilities, and developed port connectivity supports higher consumption of food additives in this region. Additionally, favorable industrial policies and ease of logistics contribute to the steady expansion of food ingredient manufacturers. The growth of organized retail chains and modern trade formats further strengthens demand for packaged and processed food products.

Southern India is another key contributor, driven by rising urbanization and a rapidly expanding middle-class population. States such as Karnataka, Tamil Nadu, and Telangana are witnessing strong growth in bakery, dairy, beverage, and ready-to-eat food production. The region’s growing IT workforce and urban consumer base have increased demand for convenience foods, directly boosting the use of sweeteners, stabilizers, preservatives, and colorants. Furthermore, the expansion of quick-service restaurant chains and food delivery platforms is accelerating additive consumption in processed food applications.

Northern and eastern regions are gradually emerging as promising markets, supported by increasing industrialization and rising disposable incomes. States such as Uttar Pradesh, Delhi NCR, West Bengal, and Bihar are experiencing higher demand for packaged snacks, dairy products, and beverages. Improvements in cold chain infrastructure and supply chain networks are facilitating deeper market penetration in semi-urban and rural areas. Government initiatives aimed at promoting food processing under schemes like “Make in India” and production-linked incentives are further stimulating regional development. The growing shift toward branded and hygienically packaged food products is creating additional demand for functional additives.

Regulatory Landscape

Food additives in India are regulated by the Food Safety and Standards Authority of India (FSSAI) under the Food Safety and Standards (Food Products Standards and Food Additives) Regulations, 2011, supported by the Compendium and the chapter on substances added to food (including GMP-based use conditions and category-wise permissions). The rulebook continues to evolve through frequent amendments, which increases the compliance burden for processors and ingredient suppliers across permissible limits, product standards, and labeling declarations for preservatives, colors, sweeteners, and processing aids.

A notable process change came through FSSAI's Office Order dated May 6, 2026, which requires applications for risk assessment and prior approval of food ingredients and non-specified food products to be submitted only through the electronic Product and Claim Approval Application System (ePAAS), effective June 1, 2026. Alongside periodic amendments notified in 2024 and 2025 to the 2011 framework, the shift toward portal-based workflows makes digital-ready dossiers, traceability documentation, and faster regulatory change management more important for both multinational and domestic ingredient manufacturers operating in India.

Value Chain Analysis

The value chain starts with upstream feedstocks and intermediates from agriculture and oleochemicals (e.g., sugarcane and corn streams for sweeteners and starch derivatives, botanicals for natural colors, and fermentation inputs for enzymes and bio-preservatives), then moves into processing to form functional ingredients such as sweeteners, hydrocolloids, emulsifiers, preservatives, flavors, enzymes, and colorants. India supplies specialty ingredients through a combination of domestic production and imports, with global ingredient firms and local manufacturers serving food processors across dairy, beverages, bakery, confectionery, and savory categories.

Midstream activities center on formulation, blending, application support, and quality testing to meet FSSAI requirements, often delivered through specialized distributors that handle specification matching and inventory availability for processors. Downstream, additives reach large organized processors and more fragmented customer bases through multi-layer distribution, where logistics, temperature control, and documentation can become bottlenecks. Infrastructure gaps, including cold-chain limitations highlighted in sector assessments, add handling risk for sensitive natural colors, cultures, and enzyme systems, making localized blending and application centers, as well as regional warehousing, important for service levels and compliance.

Competitive Landscape

The India food additives market is moderately fragmented, characterized by the presence of numerous domestic and international players competing across multiple product categories. The market structure includes large multinational ingredient manufacturers, mid-sized regional suppliers, and specialized local producers catering to niche applications. While global companies benefit from advanced research and development capabilities, diversified product portfolios, and strong distribution networks, local players compete effectively through cost advantages and customized solutions. The fragmented nature of the market intensifies pricing competition, particularly in high-volume segments such as sweeteners and preservatives. At the same time, brand reputation, product quality, and regulatory compliance play a critical role in securing long-term contracts with food processing companies.

Competitive positioning in the market is largely influenced by product innovation, clean-label offerings, and technological advancements. Companies are increasingly investing in research and development to introduce natural, plant-based, and low-calorie additives in response to evolving consumer preferences. Strategic collaborations with food and beverage manufacturers enable suppliers to co-develop customized ingredient solutions tailored to specific formulations. Additionally, players are expanding their manufacturing capacities and strengthening supply chain integration to improve cost efficiency and ensure consistent quality. Regulatory compliance with FSSAI standards and international quality certifications also serves as a key differentiator.

Companies are focusing on expanding their footprint in high-growth regions and investing in new production facilities to meet rising domestic demand. Furthermore, sustainability initiatives, including eco-friendly sourcing and clean manufacturing practices, are becoming an important competitive parameter. Digital transformation and data-driven formulation technologies are also enhancing operational efficiency and customer engagement. As the market evolves, competition is expected to shift from purely price-based rivalry toward value-added solutions and specialized ingredient offerings.

India Food Additives Industry Leaders

Cargill, Incorporated

BASF SE

Ingredion Incorporated

DSM-Firmenich AG

Kerry Group PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions in starch derivatives and adjacent ingredient platforms create room for locally produced functional additives used for texture, bulking, and stability in packaged foods and beverages. In March 2026, Gujarat Ambuja Exports commenced commercial production at a maltodextrin facility in Hubli, Karnataka, and in May 2026 Regaal Resources commissioned an expanded maize processing facility in Kishanganj, Bihar, adding liquid glucose and maltodextrin powder capacity. These moves expand domestic availability of key carbohydrate-based ingredients used across beverages, dairy desserts, confectionery, and instant mixes.

Government-led food processing incentives also provide a concrete pathway for scaling ingredient manufacturing and supporting downstream adoption. As of February 2026, the Ministry of Food Processing Industries reported PLISFPI disbursements totaling INR 2,162.55 crore and job creation of 3.39 lakh (direct and indirect) since 2021-22, reinforcing the investment cycle across processing and cold-chain infrastructure. On the demand side, cleaner labels and tighter compliance workflows raise the commercial value of application labs, fermentation-derived preservatives, and plant-based color systems, particularly as FSSAI digitizes prior-approval submissions through ePAAS from June 2026, shortening iteration cycles for companies that can maintain compliant digital dossiers and rapid reformulation capability.

Recent Industry Developments

- May 2026: Ingredion Incorporated announced a strategic partnership with Sanstar Limited, including a preferential equity investment of about INR 198.3 crore and the formation of a joint venture in India. The collaboration targets specialty excipients and high-value food ingredients, strengthening local manufacturing and technical capabilities for formulated additive systems used by large processors.

- March 2025: Cargill inaugurated a new corn milling plant in Gwalior, Madhya Pradesh, set up with its Indian partner Saatvik Agro Processors, with an initial capacity of 500 tons per day. The added domestic milling capacity supports supply continuity for starches and sweetener inputs used across beverages, dairy, and confectionery applications.

- September 2024: DSM-Firmenich earmarked an investment of over USD 100 million in India focused on capacity expansion, including plans for a new manufacturing plant. The commitment underscores multinational interest in localizing production for specialty ingredients aligned with clean-label reformulation and industrial food processing growth.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the India food additives market covers the value of additives sold for use in food and beverage manufacturing within India, counted at the point of commercial sale into the domestic demand pool.

Scope exclusions: the sizing does not include packaging materials, processing equipment, or finished packaged foods sold to consumers.

Segmentation Overview

- By Product Type

- Preservatives

- Sweeteners

- Emulsifiers

- Anti-Caking Agents

- Enzymes

- Hydrocolloids

- Food Flavors & Enhancers

- Food Colorants

- Acidulants

- By Source

- Natural

- Synthetic

- By Application

- Bakery and Confectionery

- Dairy and Desserts

- Beverages

- Meat and Meat Products

- Soups, Sauces, and Dressings

- Other Applications

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by building a clear view of India processed food output, trade flows for ingredient categories, and the core regulations that shape permitted additives and usage levels. Public sources were used to set the factual base, such as Food Safety and Standards Authority of India regulations and notifications, Ministry of Commerce and Industry trade statistics, FAOSTAT food production series, and commodity and inflation releases from India's national statistics system.

We also reviewed company annual reports, investor presentations, and credible industry association publications to understand portfolio mixes, end use exposure, and price movement language that shows up in management commentary. Where needed, paid subscriptions were used in a limited way for company financials and intelligence, patent lookups for formulation activity, and shipment level import and export records to cross check volume direction. These desk sources are not exhaustive, and additional public documents and datasets were also referred to for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with additive manufacturers, distributors, food processors, and regulatory and quality professionals who deal with specifications and reformulation cycles. The respondent input was used to validate which additive functions are gaining share, how pricing moves in contracts, and how quickly customers switch between natural and synthetic options across major application groups. Since this is an India specific study, coverage was balanced across key consuming hubs and manufacturing clusters to avoid over weighting one corridor.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | |

| Mid tier: 54% | Functional/Unit leaders: 40% | |

| Smaller Players: 15% | Managers: 47% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where processed food output and category consumption were used to reconstruct the demand pool for additives by application, and then translated into value using typical treat rates and realized pricing. To keep the model anchored, we corroborated totals using selective bottom-up checks, such as rolling up a sample of supplier revenues, channel discussions on throughput, and ASP-by-application sense checks, which were then used to adjust totals where gaps appeared.

Key inputs that were tracked include processed food volume growth, adoption of clean label and natural claims, reformulation triggers from labeling and safety updates, import dependence for specific ingredient groups, and observable price movement in key raw materials that drive additive pricing. Forecasting leaned on scenario analysis supported by simple multivariate relationships between processed food growth, premiumization, and the pace of category expansion in bakery, dairy, beverages, and savory foods. When bottom-up visibility was weak for smaller categories, shares were assigned using interview guidance and then pressure tested against trade and production signals before finalizing.

Data Validation & Update Cycle

Validation was done through multiple passes that compare model outputs against independent signals, including trade direction, major product launches that imply higher additive intensity, and pricing movement consistency across categories. Outliers were flagged when growth rates or implied per unit additive spend moved outside realistic bounds, and then the assumptions were revisited and, if required, respondents were re-contacted for clarification.

Before sign-off, the work is reviewed in steps so that calculation logic, inputs, and final tables align across sections. The report is refreshed annually, and interim updates are made when material events occur, such as regulatory changes or sharp raw material price shifts. Right before delivery, we do a fresh pass to ensure the latest available public data and market signals are reflected.

Mordor Intelligence's India Food Additives Market Size Compared Against Other Published Estimates

Published market numbers for India food additives often do not match because groups differ on what they count as an additive sale, which year they anchor to, and how they treat natural versus synthetic portfolios when prices move quickly. Differences also show up when some studies rely more on broad food industry growth, while others incorporate application level treat rate logic.

A common gap driver is scope, where some estimates fold in wider food ingredients or broader specialty ingredient baskets that go beyond additives used for functional purposes in formulations. Another driver is the pricing build, since results change when inflation is applied uniformly versus when pricing is updated by additive function and by application, and then checked against trade and procurement signals, which is how the model is kept tied to the additives demand pool in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.17 B (2026) | |

| Industry Publisher A | USD 9.64 B (2024) | Uses a different base year and forecast frame, and the valuation is presented without clear application level treat rate checks, which can shift totals when category mix changes. |

| Industry Publisher B | USD 3.74 B (2025) | The figure appears to reflect a narrower value capture, which can happen when only selected additive groups or only certain channels are counted, thereby excluding parts of the full additive basket. |

The spread across the three values mostly comes from year selection and what gets included in the counted basket, followed by how pricing is refreshed as portfolios move between natural and synthetic. By keeping the steps traceable to application demand signals and pricing logic that can be rechecked, the final number is easier to explain and reuse for planning decisions.

Key Questions Answered in the Report

How large is the India food additives market in 2026?

The market is valued at USD 11.17 billion in 2026 and is projected to reach USD 15.04 billion in 2031.

Which product type holds the biggest share?

Sweeteners command 68.23% of value, reflecting India’s sugar availability and the wide use of sugar substitutes.

Which segment is growing the fastest?

Food colorants are forecast to post a 7.61% CAGR through 2031 as natural pigments gain traction.

Which application drives additive demand the most?

Dairy and desserts lead with 31.61% share because of India’s large milk base and rising value-added dairy production.

Page last updated on: