Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

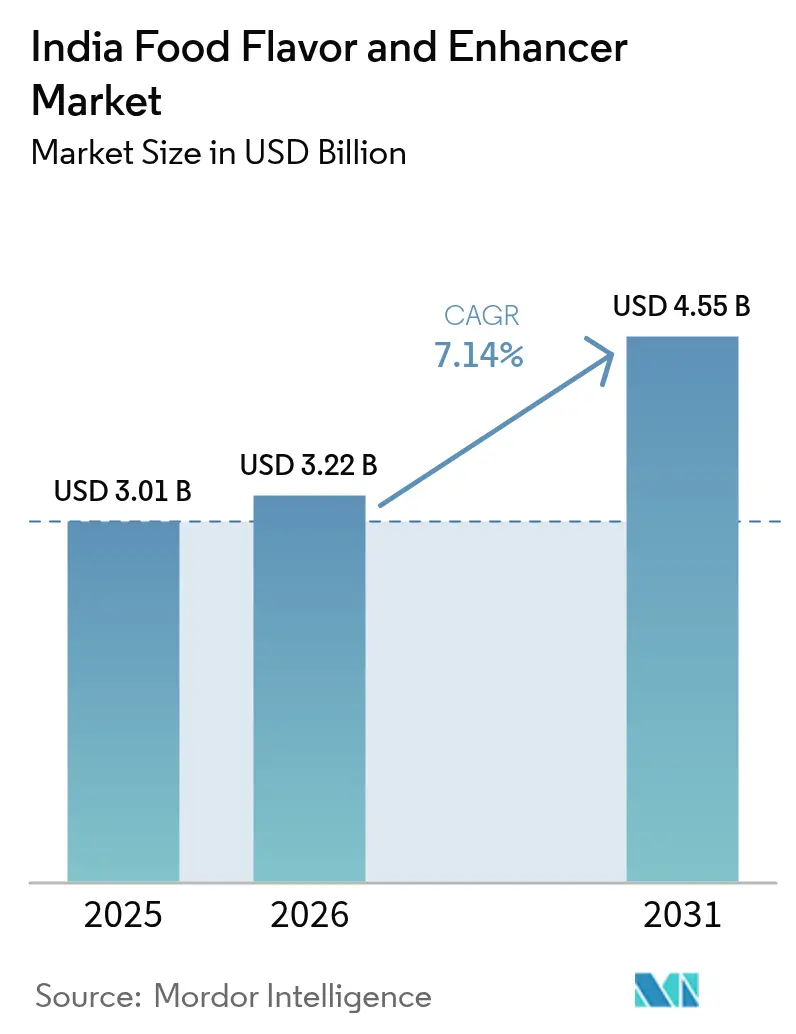

| Base Year Market Size (2025) | USD 3.01 Billion |

| Market Size (2026) | USD 3.22 Billion |

| Market Size (2031) | USD 4.55 Billion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Food Flavors And Enhancers Market Analysis by Mordor Intelligence

The Indian food flavors and flavor enhancers market size in 2026 is estimated at USD 3.22 billion, growing from 2025 value of USD 3.01 billion with 2031 projections showing USD 4.55 billion, growing at 7.14% CAGR over 2026-2031. The growth trajectory mirrors the rapid rise of processed and convenience foods across urban and rural channels, the fast-expanding organized retail network, and a policy environment that rewards investments in modern food processing capacities. The market's expansion aligns with India's broader food processing sector, which grew at 7.3% annually from 2015-2022 and is projected to reach USD 1,274 billion by 2027, according to the India Brand Equity Foundation[1] Invest India, “Food Processing Industry in India,” investindia.gov.in Demand also accelerates as rising disposable incomes reshape taste expectations, prompting manufacturers to replace basic seasonings with complex, multi-layered flavor systems that replicate regional dishes at an industrial scale. Parallel gains in cold-chain logistics, e-commerce penetration, and quick-service restaurant expansion sustain a steady stream of formulation opportunities for suppliers able to deliver shelf-stable, clean-label solutions tailored to diverse climatic zones. Technology adoption further propels the Indian food flavors and flavor enhancers market as precision fermentation, biocatalysis, and AI-driven recipe design shorten product-development cycles, while public incentives under the Production Linked Incentive Scheme (PLISFPI) reduce financing hurdles for capacity upgrades.

Key Report Takeaways

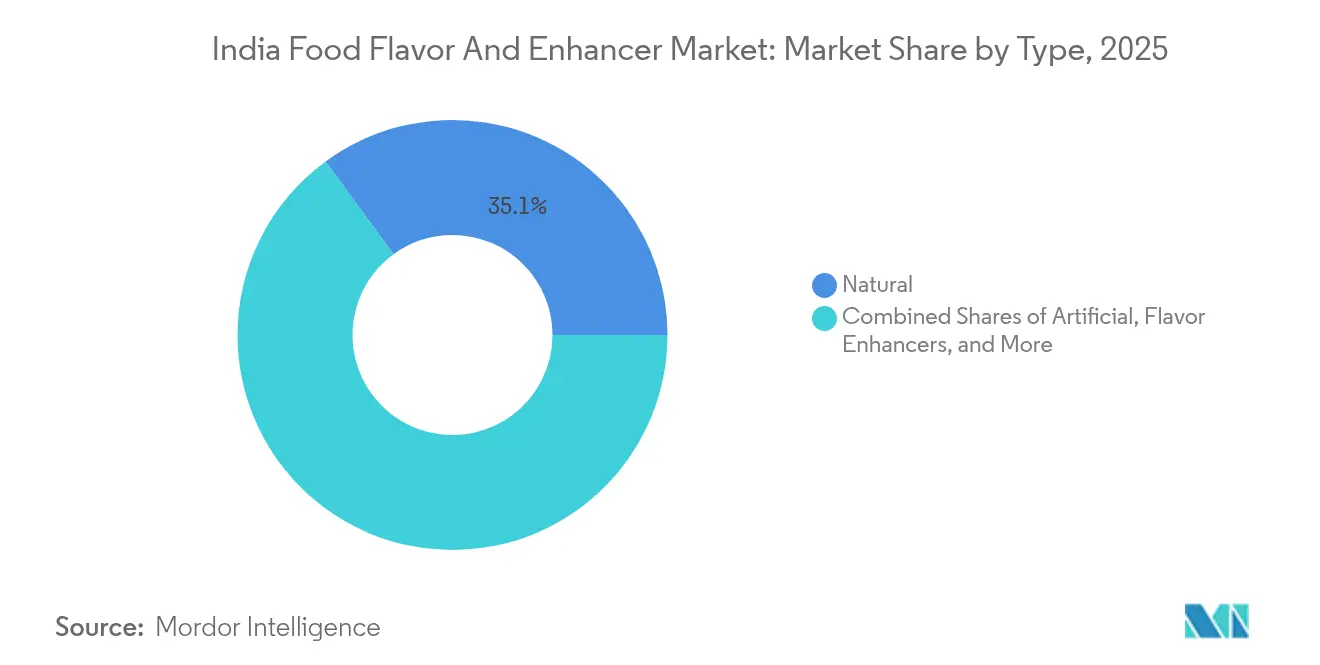

- By type, natural flavors held the largest 35.05% share of the Indian food flavors and flavor enhancers market in 2025, whereas flavor enhancers are projected to expand at an 7.87% CAGR to 2031.

- By form, liquid products accounted for 53.78% of the Indian food flavors and flavor enhancers market share in 2025, while powder variants recorded the fastest 8.05% CAGR through 2031.

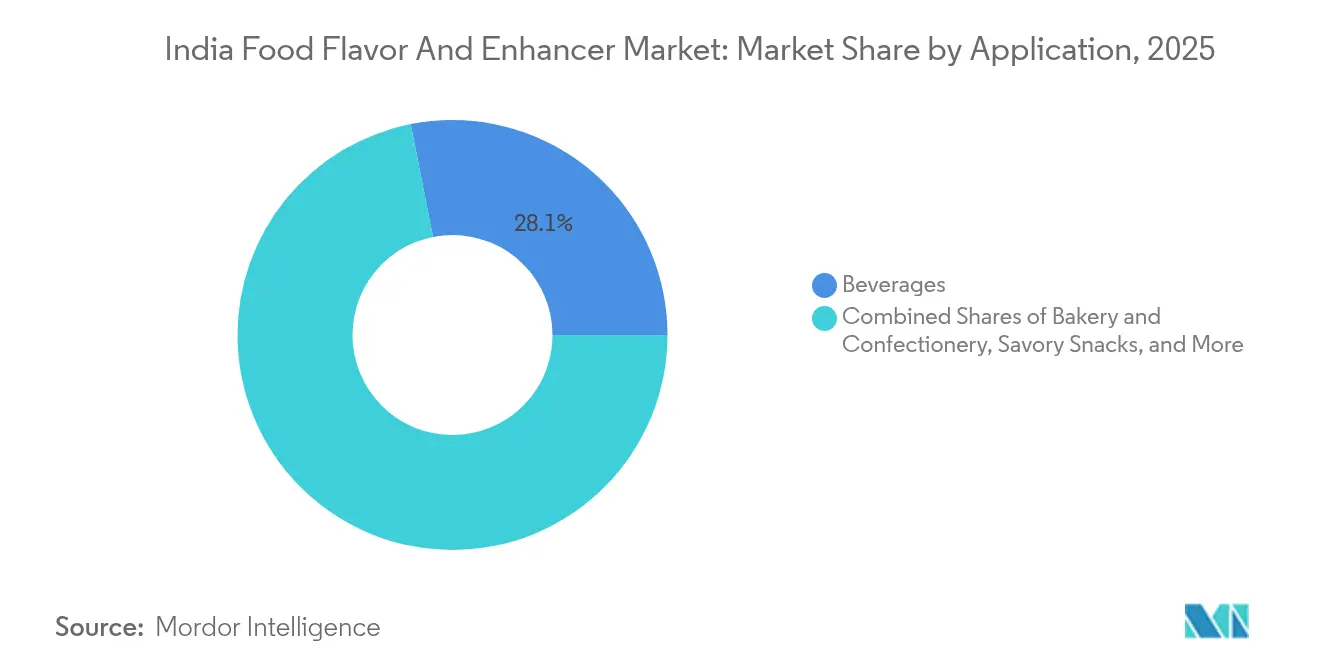

- By application, beverages led with 28.12% revenue share in 2025; bakery and confectionery is forecast to advance at a 9.19% CAGR to 2031.

- By geography, North India commanded a 27.22% share of the Indian food flavors and flavor enhancers market size in 2025, and West India is set to grow quickest at an 8.59% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Food Flavors And Enhancers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for processed and convenience foods | +2.1% | National, with early gains in North India, West India, South India | Medium term (2-4 years) |

| Clean label, natural, and organic ingredient trends | +1.8% | National, strongest in urban centers across all regions | Long term (≥ 4 years) |

| Technological advancements in flavor development | +1.2% | National, concentrated in West India, South India manufacturing hubs | Long term (≥ 4 years) |

| Government initiatives regarding flavor manufacturing and utilization | +0.9% | National, with policy implementation focus in North India, West India | Medium term (2-4 years) |

| Rising investment in R&D and innovation labs | +0.7% | National, primarily West India, South India industrial clusters | Long term (≥ 4 years) |

| Demand for region-specific and ethnic flavors | +0.6% | National, with regional variations across North, South, East, West India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Processed and Convenience Foods

In India, a surge in processed food consumption signals a shift in lifestyle, with time-strapped consumers now prioritizing convenience while still valuing authentic taste. As the domestic food market is set to grow by 47%, reaching a projected USD 1,274 billion by 2027, there's an unprecedented demand for flavor solutions that mimic traditional cooking methods on an industrial scale. This shift is especially advantageous for the ready-to-eat and ready-to-cook segments, where consistent flavor can distinguish premium products from their commodity counterparts. The trend gains momentum with e-commerce making inroads into rural markets, emphasizing the need for shelf-stable formulations that retain their sensory appeal over long distribution journeys. Urban millennials and Gen-Z are at the forefront of this evolution, craving products that offer restaurant-quality experiences at home. This demand paves the way for intricate flavor profiles, once reserved for fresh preparations, to find a place in the market.

Clean Label, Natural, and Organic Ingredient Trends

In India, 71.6% of consumers now prioritize products devoid of synthetic chemicals and additives. Furthermore, 53.7% of these consumers assert that clean label products confer enhanced health benefits. This shift in consumer preference is pushing manufacturers to not only reformulate their existing products but also to innovate new ones that align with these transparency demands, all while ensuring taste and functionality remain intact. However, the task is daunting: achieving the desired performance of natural flavor compounds often necessitates advanced extraction and stabilization technologies, traditionally associated with their synthetic counterparts. Enter biocatalysis: a game-changer that provides environmentally-friendly synthesis routes for natural flavoring compounds. This innovation adeptly reconciles the gap between the heightened demands of consumers and the scalability needs of industries. On the regulatory front, the FSSAI's push for stringent labeling and ingredient transparency bolsters this industry shift. Companies that can authentically showcase their natural sourcing and processing methods stand to gain a significant market edge.

Technological Advancements in Flavor Development

Flavor technology is undergoing a revolution, harnessing precision fermentation, enzymatic synthesis, and cutting-edge extraction methods. These innovations not only unveil new taste profiles but also drive down production costs. The use of biocatalysts in crafting natural flavors marks a significant shift towards sustainable manufacturing, resonating with both environmental standards and the growing consumer demand for eco-conscious products. Thanks to these advancements, manufacturers can now replicate intricate cooking techniques—like slow-roasting and fermentation—within controlled industrial settings. Moreover, the infusion of artificial intelligence and machine learning into flavor development is speeding up the identification of unique taste pairings and fine-tuning existing recipes to cater to regional tastes. Firms that embrace these technologies are reaping rewards, launching products to market more swiftly and tailoring flavors to specialized market segments that were once deemed too niche to pursue.

Government Initiatives Regarding Flavor Manufacturing and Utilization

Through infrastructure development, technology upgrades, and export promotion initiatives, the Pradhan Mantri Kisan Sampada Yojana (PMKSY) and Production Linked Incentive Scheme (PLISFPI) bolster the ecosystem for flavor manufacturers, as highlighted by Invest India[2]Indian Brand Equity Foundation, “India’s Food Processing Industry: Growth & Opportunities,” www.ibef.org. These initiatives are especially advantageous for small and medium enterprises, which often lack the capital for independent modernization. Such support empowers these enterprises to adopt cutting-edge flavor processing technologies and meet global quality benchmarks. With the government aiming to position India as a global hub for millets and traditional grains, flavor companies now have the chance to craft authentic taste profiles, aligning with these strategic crops in processed foods. Furthermore, the Food Safety and Standards Authority of India (FSSAI)[3]Food Safety and Standards Authority of India, "FSSAI: First Amendment on Food Safety and Standard(Packaging) Regulation", www.myfssai.in has streamlined regulations by updating packaging and labeling standards. This move not only simplifies compliance without compromising food safety but also allows companies to channel more resources into innovation rather than navigating bureaucratic challenges.

Restraints Impact Analysis*

| Restraints | ~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs and supply fluctuations | -1.4% | National, acute in North India, East India spice-producing regions | Short term (≤ 2 years) |

| Proliferation of counterfeit and low-quality products | -0.8% | National, concentrated in unorganized retail channels | Medium term (2-4 years) |

| Sustainability and traceability pressures | -0.6% | National, export-focused operations in West India, South India | Long term (≥ 4 years) |

| Fragmented and unreliable supply chains | -0.5% | National, rural-urban connectivity gaps across all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Costs and Supply Fluctuations

Flavor manufacturers face significant margin pressures due to raw material price volatility. Climatic disruptions and shifting cultivation patterns have caused dramatic price fluctuations in key spices. For example, turmeric production has declined by 15-20%, while demand continues to rise. Similarly, red chili prices are surging, driven by a 15% increase in export demand. These cost pressures make it difficult for manufacturers to pass on expenses to price-sensitive consumers. The situation is further complicated by China's entry into the spice extraction market, which heightens competition for Indian suppliers and threatens established pricing structures and supply chains. Additionally, cumin prices are impacted by weather disruptions, and global supply constraints are tightening the availability of black pepper. To address these challenges, manufacturers are adopting advanced hedging strategies and diversifying their sourcing networks. However, companies with limited financial resources face greater difficulties in managing these fluctuations, potentially leading to market consolidation as smaller players struggle with working capital needs and inventory management complexities.

Proliferation of Counterfeit and Low-Quality Products

The unorganized sector's prevalence in India's food supply chain creates opportunities for substandard products that undermine consumer confidence and brand equity for legitimate manufacturers. Counterfeit flavoring products often contain harmful adulterants or fail to meet basic safety standards, creating regulatory scrutiny that affects the entire industry through increased compliance requirements and testing protocols. This challenge particularly impacts premium and organic flavor segments where authenticity commands price premiums, as counterfeit products erode consumer trust and willingness to pay for genuine quality. The fragmented retail landscape complicates enforcement efforts, as counterfeit products often enter markets through informal distribution channels that operate outside regulatory oversight. FSSAI's enhanced labeling and traceability requirements aim to address these issues, but implementation remains inconsistent across different market tiers and geographic regions

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Natural Ingredients Drive Premium Positioning

In 2025, natural flavors commanded a dominant 35.05% share of India's food flavors and flavor enhancers market, buoyed by a clean-label trend. Meanwhile, flavor enhancers, driven by processors' quest for cost-effective taste intensity, recorded the swiftest growth at an 7.87% CAGR. The market size for natural flavors in India is set to rise from USD 1.06 billion in 2025 to an anticipated USD 1.55 billion by 2031. Manufacturers are leveraging enzymatically derived vanillin, citrus terpenes, and spice oleoresins, all aligning with FSSAI’s “nature-derived” guidelines. This alignment allows them to command premium prices in functional drinks and gourmet sauces. Mid-tier snack producers are increasingly turning to nature-identical compounds, which help them navigate the delicate balance between cost and consumer perception, effectively blurring the lines between synthetic and natural. While the synthetic segment's share is dwindling, it remains steadfast in sugar-confectionery and powdered beverage bases, where high-temperature stability is paramount.

Flavor enhancers are witnessing growth, driven by rising demand for nucleotide- and yeast-based umami boosters. These enhancers not only reduce sodium content but also amplify flavor, making them especially popular in instant noodles and savory seasonings. As consumers adapt to low-salt diets, the market share for flavor enhancers in India’s food flavors and flavor enhancers sector may surpass the projected 7.87% CAGR. Suppliers introducing label-friendly alternatives to monosodium glutamate—like tomato concentrate powders and fermented soy extracts—are resonating well with health-conscious consumers.

By Form: Liquid Dominance Meets Powder Innovation

Powder formats are projected to grow at a CAGR of 8.05% through 2031, fueled by their enhanced shelf stability, lower transportation costs, and suitability for dry mix applications, which dominate India's convenience food sector. This upward trend underscores manufacturers' efforts to streamline supply chain economics. By opting for powder forms, they sidestep cold chain necessities and simplify packaging, especially for products aimed at rural areas with limited refrigeration. In 2025, liquid flavors command a 53.78% market share, thanks to their quick solubility and superior dispersion in beverages, the leading application category.

Advancements in encapsulation and spray-drying technologies now allow powder formats to replicate flavor release profiles once exclusive to liquid systems, broadening their use across various food categories. Manufacturers are increasingly adopting dual-format portfolios: liquid forms cater to premium segments where instant flavor impact justifies a higher price, while powder variants meet the mass market's demand for budget-friendly flavor solutions. The choice between formats also influences distribution strategies. Liquid flavors, needing specialized handling and storage, lean towards organized retail channels. In contrast, powder forms boast wider market reach through traditional trade networks.

By Application: Beverages Lead While Bakery Accelerates

India's evolving snack culture and the modern twist on traditional sweets are propelling bakery and confectionery applications to a leading 9.19% CAGR growth rate through 2031. Manufacturers are adeptly blending nostalgic flavors with contemporary packaging and convenience, catering to both traditional tastes and modern consumption habits. Meanwhile, beverages command the largest application share at 28.12% in 2025, buoyed by India's surging soft drink demand and the rise of functional beverages, which lean heavily on advanced flavor masking and enhancement techniques.

As cold chain infrastructure matures and consumers warm up to processed dairy, dairy and frozen foods are seizing significant market opportunities, moving beyond just ice cream. Urbanization trends show working families gravitating towards these segments, seeking quick meal solutions that echo the authentic taste of home-cooked dishes. Savory snacks are diversifying, drawing on regional flavor innovations to resonate with local palates while appealing to a broader audience. This trend opens doors for flavor companies that can harmonize authenticity with scalability. The "Others" category highlights burgeoning sectors like plant-based alternatives and functional foods, underscoring the pivotal role of flavor technology in winning consumer trust and achieving market success.

Geography Analysis

In 2025, North India holds a significant 27.22% share of the regional market, leveraging its extensive consumer base, well-established food processing infrastructure, and strategic role as a gateway to domestic and international markets. Urban centers such as Delhi, the extended metropolitan influence of Mumbai, and Punjab's agricultural processing strengths enable seamless integration from raw material sourcing to finished product distribution. Leading global flavor companies have established their Indian headquarters and primary manufacturing facilities in this region, attracted by the availability of skilled labor, proximity to regulatory bodies, and efficient nationwide distribution networks. Government initiatives under PMKSY further drive the region's growth by focusing on infrastructure development in food processing clusters, enhancing economies of scale for flavor manufacturers catering to diverse application segments. The intersection of traditional culinary practices with modern processing requirements allows manufacturers to create flavor profiles that meet authentic taste expectations while ensuring industrial scalability.

West India is the fastest-growing region, with an 8.59% CAGR projected through 2031. This growth is driven by the region's advantages in export-oriented manufacturing, port connectivity, and the development of industrial clusters that attract both domestic and international flavor companies. The region combines its traditional expertise in spice trading with modern flavor technology, creating a competitive edge in raw material sourcing and finished product development. Maharashtra and Gujarat's industrial policies actively promote food processing investments through streamlined approvals, infrastructure subsidies, and export incentives, benefiting flavor manufacturers targeting global markets. DSM-Firmenich's acquisition of VKL Seasoning highlights the region's global recognition for its capabilities in spices and clean label ingredients, while local companies capitalize on these strengths to expand their market presence. The region's proximity to major ports facilitates the import of raw materials and the export of finished products, providing cost advantages that support competitive pricing for domestic market penetration.

South India significantly contributes to market growth as India's leading spice-producing region, with traditional food processing industries increasingly adopting modern flavor technologies. Tamil Nadu leads in the export of processed fruits, juices, and nuts, offering natural synergies for flavor companies to utilize existing supply chains and processing expertise. The region's growing startup ecosystem focuses on innovative food processing solutions, including millets, ready-to-eat products, and plant-based alternatives, all of which require advanced flavor development capabilities. East India presents an emerging opportunity as infrastructure improvements enhance connectivity and industrial growth creates new demand centers. However, the region's contribution remains limited due to logistical challenges and a lower concentration of industries compared to western and northern regions. The geographic diversity of India's flavor market reflects broader economic development trends, with established industrial hubs driving immediate growth and emerging regions offering long-term expansion potential as infrastructure and consumer purchasing power continue to improve.

Competitive Landscape

In the India Food Flavors and Flavor Enhancers Market, a moderate concentration score of 6 out of 10 highlights a competitive landscape. Here, established global leaders vie for dominance alongside assertive domestic players, each employing distinct positioning strategies. Take Givaudan, for instance: the international behemoth notched a 20.9% like-for-like growth in South Asia in 2024. They harness technological prowess and robust R&D capabilities, allowing them to dominate premium market segments. On the other hand, local entities like Keva Flavours and Synthite Industries leverage their regional insights, cost efficiencies, and deep understanding of local palates.

The competitive landscape is further complicated as the lines blur between traditional flavor houses and ingredient suppliers. A case in point is S H Kelkar, which reported a 17.4% year-on-year revenue growth in H1 FY2025, thanks to its strategic move beyond fragrances and into food applications. From 2024 to 2025, strategic consolidations gained momentum. Companies increasingly sought vertical integration and geographic expansion, aiming to harness greater value across the supply chain. A notable instance is DSM-Firmenich's acquisition of VKL Seasoning. This move not only underscores the trend of melding international technical expertise with local market insights but also highlights the pursuit of competitive edges in clean label ingredients and genuine regional flavors.

Meanwhile, the realm of biotechnology applications presents untapped potential. Companies delving into biocatalysis and fermentation technologies are carving out sustainable advantages, thanks to proprietary production methods that slash costs and align with clean label mandates. However, the regulatory landscape, shaped by FSSAI, poses challenges. It erects barriers for smaller entrants but offers a leg up to firms boasting stringent quality systems and compliance prowess. This dynamic could further fuel market consolidation, especially as regulatory intricacies deepen.

India Food Flavors And Enhancers Industry Leaders

-

International Flavors & Fragrances, Inc.

-

Symrise AG

-

Kerry Group plc

-

Givaudan SA

-

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: International Flavors and Fragrances opened a new facility in Hyderabad, India. The facility has an area of 75,000 square feet and is designed to accommodate up to 600 employees. The purpose of this expansion was to reach more customers.

- March 2025: Symega Foods opened a new manufacturing facility in Sonipat, Haryana. The purpose of this expansion was to ensure faster delivery services and to reach a larger consumer base across the country.

- May 2024: Mane Group invested USD 24.4 million in flavors and fragrances manufacturing in Hyderabad, India. The facility is especially opened for the manufacturing of snacks and savory flavors.

India Food Flavors And Enhancers Market Report Scope

A food flavor and enhancer can be defined as a flavoring agent, like a food additive, being utilized to enhance the food's texture, color, taste, or smell. India's food flavor and enhancer market is segmented into type and application. By type, the market is segmented into natural flavor, synthetic flavor, nature-identical flavoring, and flavor enhancers. By application, the market is segmented into dairy, bakery, confectionery, processed food, beverage, and other applications. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Type

| Natural Flavors |

| Synthetic Flavor |

| Nature-Identical Flavors |

| Flavor Enhancers |

By Form

| Liquid |

| Powder |

By Application

| Beverages |

| Bakery and Confectionery |

| Dairy and Frozen Foods |

| Savory Snacks |

| Others |

By Geography

| North India |

| West India |

| East India |

| South India |

| By Type | Natural Flavors |

| Synthetic Flavor | |

| Nature-Identical Flavors | |

| Flavor Enhancers | |

| By Form | Liquid |

| Powder | |

| By Application | Beverages |

| Bakery and Confectionery | |

| Dairy and Frozen Foods | |

| Savory Snacks | |

| Others | |

| By Geography | North India |

| West India | |

| East India | |

| South India |

Key Questions Answered in the Report

What is the current value of the India food flavors and flavor enhancers market?

The market is valued at USD 3.22 billion in 2026.

How fast will the market grow through 2031?

It is projected to expand at a 7.14% CAGR, reaching USD 4.55 billion by 2031.

Which segment records the highest growth rate?

Flavor enhancers lead with an 7.87% CAGR between 2026-2031.

Which region will post the fastest regional growth?

West India is set to grow at an 8.59% CAGR through 2031.

Page last updated on: