Market Overview

| Study Period | 2021 - 2031 |

|---|---|

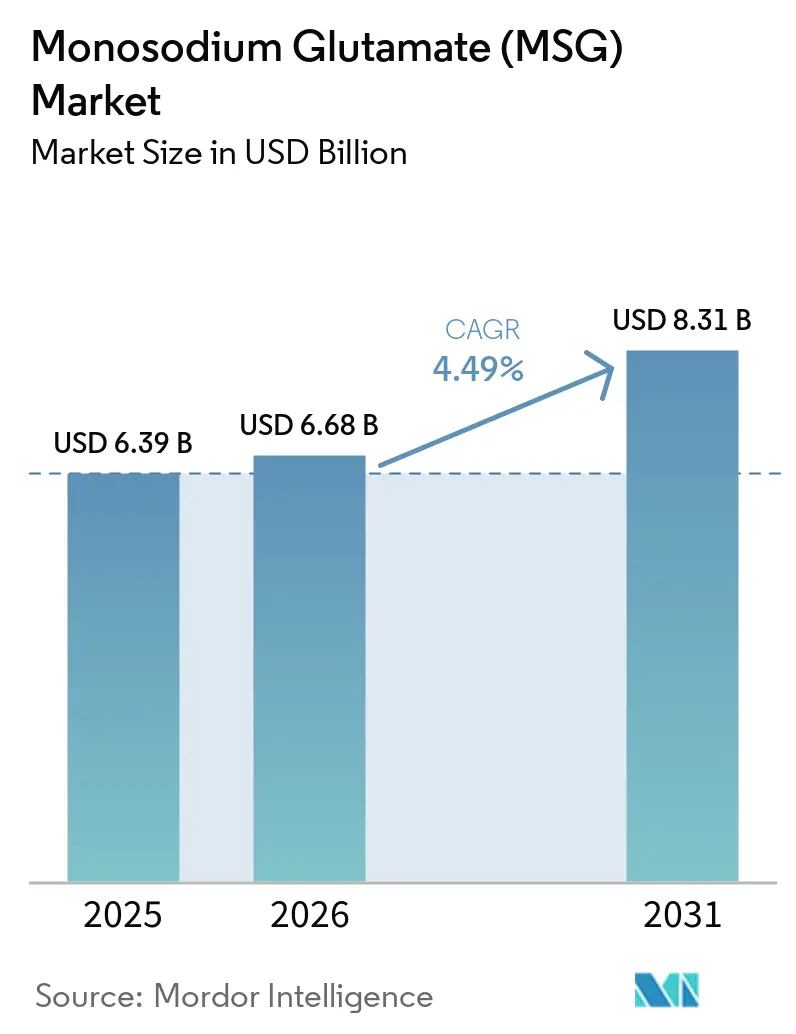

| Market Size (2026) | USD 6.68 Billion |

| Market Size (2031) | USD 8.31 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Monosodium Glutamate (MSG) Market Analysis by Mordor Intelligence

The MSG market size was valued at USD 6.39 billion in 2025 and estimated to grow from USD 6.68 billion in 2026 to reach USD 8.31 billion by 2031, at a CAGR of 4.49% during the forecast period (2026-2031). Growing regulatory pressure to trim sodium across packaged foods, the rebound of full-service and quick-service restaurants, and continuous investments in fermentation technology keep the MSG market on a solid expansion path. Manufacturers are leveraging MSG’s dual role as a flavor enhancer and partial sodium substitute to satisfy clean-label mandates while preserving palatability, which is now critical as front-of-package labeling rules tighten in North America and Europe. Asia Pacific retains manufacturing scale advantages, yet rising Western adoption—especially through foodservice chains—signals a geographic re-balancing of demand. Encapsulation technologies, AI-guided bioreactors, and verified carbon-reduction pathways are shifting competitive focus away from pure volume and toward margin-rich, application-specific MSG systems. Industry consolidation is intensifying as leading producers bankroll regional plants to sidestep anti-dumping duties and shorten logistics routes, safeguarding supply in the face of trade frictions

Key Report Takeaways

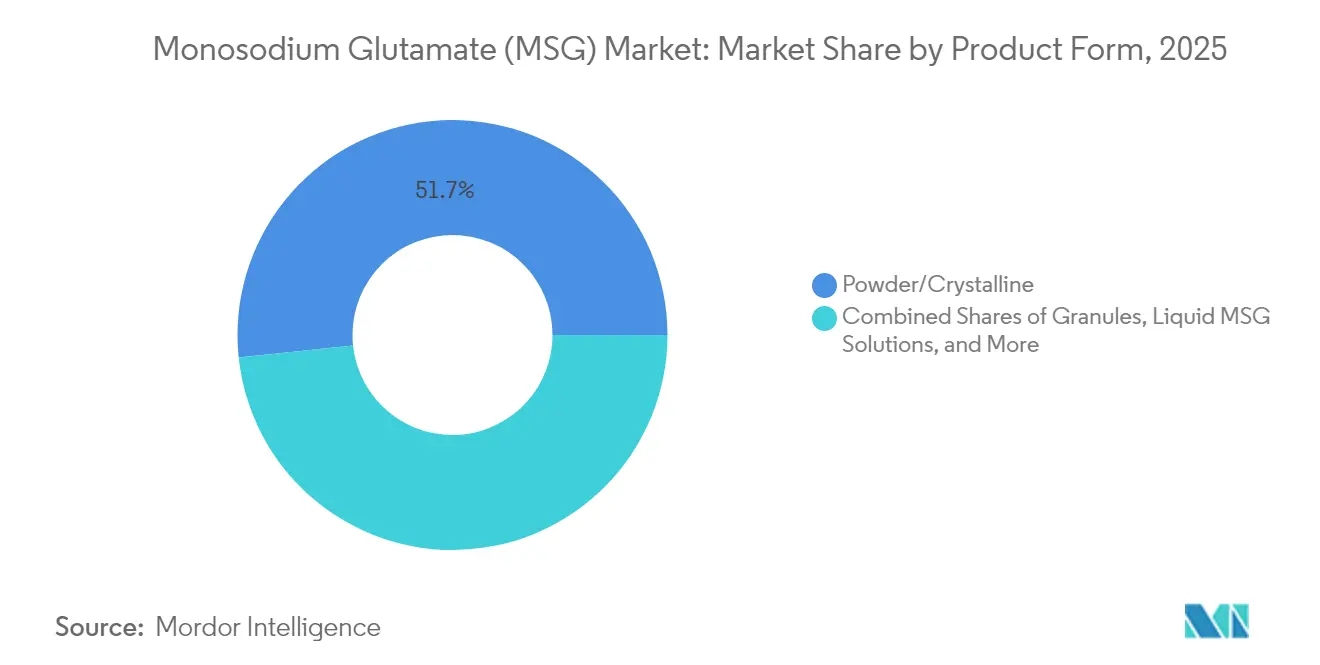

- By product form, powder/crystalline variants held 51.67% of the MSG market share in 2025; micro-encapsulated MSG is projected to log the fastest 5.12% CAGR to 2031.

- By application, food processing commanded a 47.85% share of the MSG market size in 2025, while foodservice is advancing at the highest 6.05% CAGR through 2031.

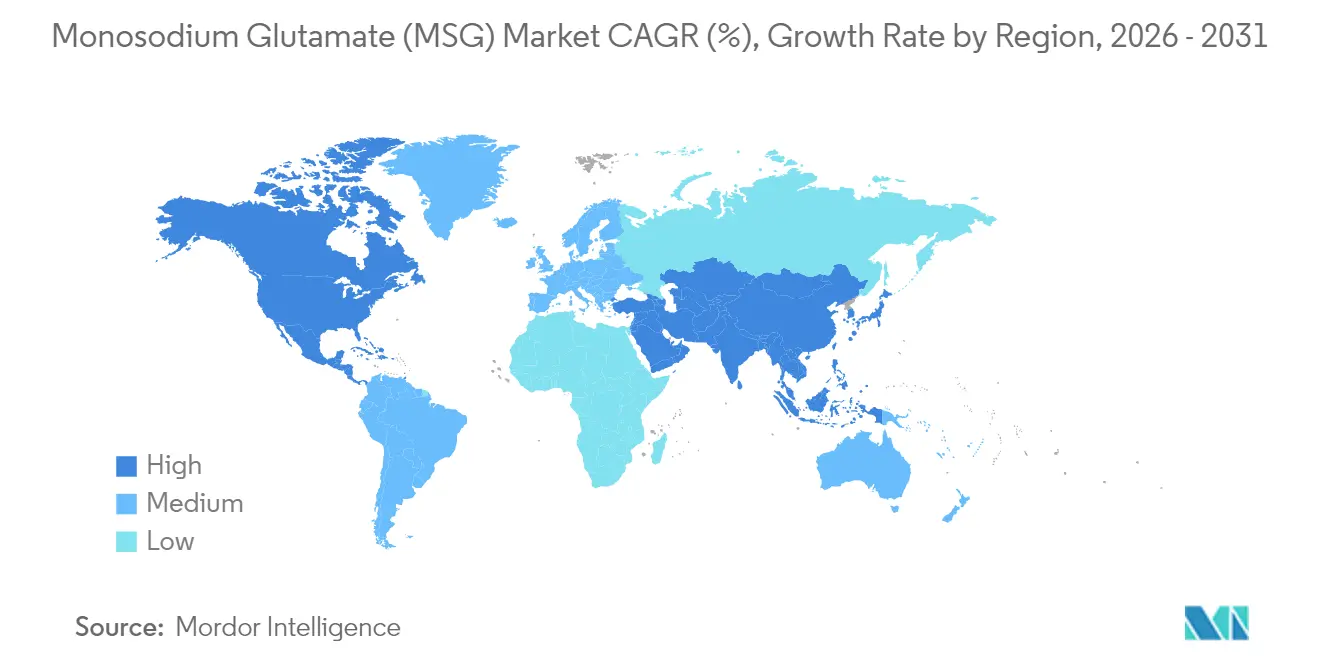

- By geography, Asia Pacific led with 61.55% MSG market share in 2025, while North America is forecast to expand at a 6.21% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Monosodium Glutamate (MSG) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Application of MSG in Various Food Products | +1.2% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Rising Substitution of Salt with MSG in Sodium-Reduction Reformulations | +1.5% | North America & EU, expanding to APAC urban centers | Long term (≥ 4 years) |

| Rising Disposable Income in Emerging Market | +1.0% | Global, led by developed markets with regulatory mandates | Long term (≥ 4 years) |

| Technological Advancements in Production | +0.8% | APAC core, spill-over to emerging markets | Medium term (2-4 years) |

| Expansion of Foodservice Industry | +1.1% | Global, led by North America & Europe recovery | Short term (≤ 2 years) |

| Cost Effectiveness in Flavor Enhancement | +0.6% | Global, particularly emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Application of MSG in Various Food Products

Manufacturers are strategically incorporating MSG to address consumer demands for enhanced flavors while maintaining nutritional priorities. Food processors are utilizing MSG to not only enhance flavors but also reduce sodium content by up to 30% in reformulated products, providing a competitive advantage in health-conscious markets. Recent research underscores MSG's ability to improve the palatability of vegetables, enabling manufacturers to increase vegetable content in their products without compromising consumer satisfaction. MSG's application has expanded beyond its traditional use in Asian cuisine to mainstream Western food categories, such as ready-to-eat meals, snacks, and plant-based protein alternatives. The FDA's classification of MSG as Generally Recognized as Safe (GRAS) offers regulatory assurance, allowing manufacturers to incorporate MSG into new product formulations without requiring extensive safety documentation. Emerging uses in functional foods and nutraceuticals indicate that MSG's role is evolving beyond flavor enhancement to nutritional optimization, particularly in products designed for older consumers with diminished taste sensitivity.

Rising Substitution of Salt with MSG in Sodium-Reduction Reformulations

Sodium reduction mandates in developed markets are driving demand for MSG as a direct salt replacement. Regulatory bodies increasingly recognize umami enhancement, such as MSG, as a viable public health strategy. The World Health Organization's sodium reduction targets, along with front-of-package labeling requirements, are prompting food manufacturers to reformulate products. By incorporating MSG-based solutions, manufacturers can maintain product palatability while meeting regulatory standards. A 2024 clinical study highlights that Vietnamese populations using MSG-rich seasonings have significantly lower sodium intake and reduced systolic blood pressure compared to those relying on traditional salt-based seasonings. This evidence strengthens MSG's acceptance as a functional ingredient rather than merely a flavor enhancer, creating opportunities for health claim substantiation in key markets. From an economic perspective, MSG adoption is advantageous, enabling manufacturers to meet sodium reduction goals without costly ingredient substitutions or complex reformulations. Additionally, advanced enzyme production technologies now allow food processors to produce glutamic acid on-site, offering clean-label alternatives that align with consumer preferences while delivering the same umami enhancement.

Shift toward Low-Sodium Food Formulations

The global shift toward low-sodium food formulations marks a significant transformation in the industry, driven by increasing evidence linking high sodium intake to cardiovascular disease and regulatory pressures from health authorities worldwide. Food manufacturers are realizing that traditional sodium reduction methods often compromise taste, creating opportunities for MSG-based solutions that maintain flavor while meeting nutritional goals. Recent studies on condiment reformulation reveal that microencapsulated ingredients can reduce sodium by 25-52% without affecting sensory quality, with MSG playing a vital role in preserving the umami flavors consumers associate with enjoyable taste experiences. Regulatory frameworks, such as the European Union's sodium reduction guidelines and similar initiatives in North America, support MSG adoption as a practical solution for achieving compliance without undermining commercial viability. In premium food segments, low-sodium credentials are increasingly marketed as key differentiators, with consumers willing to pay a premium that offsets reformulation and ingredient substitution costs. This trend also extends to foodservice applications, where restaurants and institutional food providers aim to cater to health-conscious consumers while maintaining flavor consistency and operational efficiency across their menus.

Cost Effectiveness in Flavor Enhancement

MSG's superior cost-performance ratio compared to alternative flavor enhancement technologies creates sustainable competitive advantages for food manufacturers operating under margin pressure from inflation and supply chain disruptions. Economic analysis reveals that MSG delivers equivalent umami enhancement at approximately 60% lower cost per serving compared to natural flavor alternatives, enabling manufacturers to maintain product quality while managing input cost inflation. The ingredient's stability and extended shelf life reduce inventory carrying costs and waste generation, creating additional economic benefits that compound over time in high-volume production environments. Small-scale food processors increasingly adopt MSG-based formulations to compete with larger manufacturers who benefit from economies of scale in ingredient procurement and processing efficiency. Regional price variations create arbitrage opportunities for manufacturers with flexible supply chain configurations, particularly as anti-dumping measures on Chinese MSG create pricing disparities across geographic markets, Federal Register[1]Federal Register, "Monosodium Glutamate From the People's Republic of China: Preliminary Affirmative Determination of Circumvention", www.federalregister.gov. The development of MSG-based seasoning systems reduces the need for complex flavor profiles that require multiple ingredients, simplifying supply chain management and reducing formulation costs for food manufacturers.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Concerns and Negative Perceptions | -0.9% | North America & Europe, limited impact in APAC | Long term (≥ 4 years) |

| Stringent Regulatory Policies | -0.6% | EU & North America, emerging in developing markets | Medium term (2-4 years) |

| Availability of Natural Alternatives | -0.4% | Global, strongest in premium segments | Medium term (2-4 years) |

| Volatility of Raw Material Prices | -0.7% | Global, particularly affecting cost-sensitive segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health Concerns and Negative Perceptions

Although extensive scientific validation exists, consumer misconceptions about MSG safety persist, limiting its market penetration in Western regions where clean-label preferences strongly influence purchasing decisions. Industry associations are leading consumer education initiatives but face significant challenges in combating misinformation spread through social media and celebrity-endorsed anti-MSG campaigns, many of which lack scientific credibility. Premium food segments show notable resistance to MSG, as consumers often associate it with lower-quality processed foods, disregarding its ability to enhance nutritional profiles by reducing sodium content. This issue is further complicated in the organic and natural food sectors, where regulatory definitions may exclude MSG, even though it is produced through natural fermentation processes similar to other accepted ingredients. To address these challenges, food manufacturers are increasingly adopting alternative labeling strategies, such as "yeast extract" or "natural flavors," to provide umami enhancement without provoking negative consumer reactions. However, these strategies often lead to higher formulation costs and added complexity.

Stringent Regulatory Policies

Across various jurisdictions, evolving food safety regulations and labeling requirements create a complex compliance landscape. This challenge is particularly pronounced for smaller MSG manufacturers and food processors with limited regulatory expertise. For example, the European Union[2]European Parliament and Council, “Regulation 1333/2008 on Food Additives,” europa.eu requires extensive documentation and periodic re-evaluation for MSG applications. According to the European Parliament and Council, these requirements result in ongoing compliance costs, which larger manufacturers with dedicated regulatory teams are better equipped to manage. Additionally, supply chain uncertainties stem from anti-dumping investigations and trade disputes. A prominent example is the US Department of Commerce's ongoing inquiry into Malaysian MSG imports, as reported by the Federal Register, which complicates long-term procurement strategies for food manufacturers. As emerging markets increasingly adopt Western regulatory standards, MSG manufacturers pursuing geographic expansion face additional compliance hurdles. For instance, the Food Safety and Standards Authority of India imposes restrictions on MSG use in specific food categories, such as pasta and noodles. These regional regulatory variations not only restrict market access but also necessitate product reformulation. While certifications like halal, kosher, and organic add complexity and cost to production processes, they also create opportunities to tap into premium markets for compliant manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Powder Dominance Faces Encapsulation Innovation

Powder/crystalline products retained 51.67% MSG market share in 2025 on the back of long-established production lines and simple dry-mix compatibility in instant noodles, bouillon cubes, and snack seasonings. Seasoning plants that invested decades ago in powder conveyance systems face latent switching costs, buttressing powder’s lead. Granules serve niche retail packs where visual cues and controlled dissolution matter, while emerging liquid formulations appeal to centralized kitchens moving toward pump-fed automation.

Micro-encapsulated formats are sprinting ahead with a 5.12% CAGR due to mandated dust-exposure limits in industrial bakeries and meat plants. Encapsulation also unlocks staged release that preserves umami during high-heat or high-salt processing, a crucial feature for retorted soups and canned meat. Although encapsulated MSG carries a pricing premium, processors offset that increment by cutting flavor wastage and improving product stability across supply chains.

By Application: Food Processing Leads While Foodservice Accelerates

In 2025, food processing manufacturers are projected to contribute 47.85% of MSG demand, leveraging its cost-effectiveness and versatility. MSG is utilized across a wide range of products, including noodles, soups, meat items, and seasonings. As consumption of these products is increasing, the applications are also increasing. According to the DEFRA data from 2023, the average per person per week consumption of soup in the United Kingdom was 59 grams. Their expertise in ingredient application and efficient supply chains provides a sustainable competitive advantage. Within the food processing segment, noodles and soups emerge as the largest sub-segment, highlighting MSG's traditional importance in Asian cuisine and its critical role in instant food products requiring flavor intensity and shelf stability. Additionally, meat products increasingly use MSG to enhance umami profiles while reducing sodium content, aligning with regulatory standards and consumer health trends.

Foodservice and quick-service restaurants are experiencing the fastest growth in MSG applications, with a 6.05% CAGR. This growth is driven by post-pandemic recovery and the industry's focus on ensuring flavor consistency across multiple locations and preparation methods. Restaurant operators are increasingly recognizing MSG's ability to improve perceived food quality while managing ingredient costs. This is particularly significant as labor shortages drive greater reliance on standardized preparation processes. In the household/retail segment, MSG usage is rising due to growing consumer awareness of umami flavors and increased home cooking. However, growth in this segment is limited by persistent negative perceptions among certain demographic groups. Meanwhile, animal feed and pharmaceutical applications are emerging as promising opportunities for MSG, requiring high levels of purity and consistency. These specialized demands justify premium pricing, offsetting lower sales volumes. Pet food manufacturers, in particular, value MSG for its ability to enhance palatability, aligning with the trend of pet owners prioritizing nutrition and taste in premium product categories.

Geography Analysis

Asia Pacific’s commanding 61.55% share reflects economies of scale in fermentation plants, abundant corn feedstocks, and deep-rooted culinary reliance on umami seasonings. China remains the production nucleus despite price-suppressing oversupply cycles; still, investment outflows into Kazakhstan and Vietnam mark a diversification push designed to cushion against trade friction. Japan channels R&D toward low-carbon MSG lines verified by lifecycle audits, enabling premiums in eco-sensitive EU retail programs. Southeast Asia sees demand acceleration as rising income boosts instant-noodle and snack consumption, keeping regional capacity tight.

North America’s conversion from skepticism to adoption is underway. Supermarket chains increasingly accept MSG-formulated ready meals after reformulators prove sodium cuts of 20–30% without sensory loss. Anti-dumping circumvention findings against Malaysian trans-shipments prompted Ajinomoto to boost domestic output, signaling confidence in local demand staying strong. Meanwhile, foodservice adoption surges as pan-Asian chains expand their footprint, creating a feedback loop of menu familiarity that chips away at consumer wariness.

Europe’s MSG narrative revolves around compliance rigor and consumer scrutiny. The European Commission’s 2024 probe into Malaysian imports underscores a vigilant trade posture, yet it simultaneously provides breathing room for EU-based contract formulators free from dumping duties. Premium organic/artisanal brands sometimes eschew MSG, but mid-tier processors adopt encapsulated forms that pass stricter workplace dust thresholds. South American processors capitalize on competitive corn costs, although inflationary headwinds and exchange-rate swings complicate capex decisions. Middle East and Africa markets are nascent yet enticing; rapid urban retail expansion is unlocking new shelf space for MSG-enriched convenience foods, especially in Gulf Cooperation Council states keen on international cuisine.

Competitive Landscape

The Monosodium glutamate market scores a 7/10 on concentration, with top fermentation specialists controlling a steep share through scale, integrated supply chains, and regulatory know-how. CJ CheilJedang’s planned USD 4 billion bio-unit sale illustrates asset re-allocation toward higher-margin, application-specific MSG and amino acids. Meihua Holdings leverages certified carbon-reduced portfolios to meet Western customer ESG demands, clinching long-term contracts at elevated price points. Ajinomoto anchors regional resilience through incremental investments in U.S. and Malaysian plants while defending domestic markets via trade petitions that curb under-priced imports.

White-space entrants focus on natural or enzymatically derived glutamate systems to tap clean-label premiums; however, scale economics and patent estates around encapsulation often stymie rapid ascent. Strategic alliances—notably Glanbia’s USD 300 million acquisition of Flavor Producers—signal broader ingredient houses angling for umami capabilities to round out holistic flavor portfolios. Supply security has taken center stage since COVID-era bottlenecks; diversified plants in Hungary, South Dakota, and future Central Asian hubs aim to compress lead times and blunt tariff shock.

Competitive tactics increasingly revolve around IP-protected delivery systems, ESG branding, and proximity manufacturing, rather than brute-force capacity. Encapsulation patents raise functional differentiation barriers, while blockchain traceability projects assure downstream customers of ethical sourcing. Altogether, the landscape favors incumbents that can flex raw-material procurement muscle, innovate on process sustainability, and deftly navigate customs regimes.

Monosodium Glutamate (MSG) Industry Leaders

-

Fufeng Group

-

Meihua Holdings Group Co., Ltd

-

Gremount International Co.,Ltd

-

Cargill Inc.

-

Ajinomoto Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Marubeni Corporation acquired additional shares in AIG Asia Ingredients Corporation, a key Vietnamese food ingredients supplier experiencing rapid growth, operating an innovation center to meet consumer demand for convenience and healthy foods, while supporting its growth strategy in expanding the Southeast Asian food market

- April 2024: Glanbia PLC agreed to acquire Flavor Producers LLC for USD 300 million initial consideration, a leading US flavor platform specializing in organic and natural ingredients that aligns with Glanbia's strategy to enhance flavor offerings within its Nutritional Solutions business serving major FMCG companies and emerging brands

- February 2024: Ajinomoto Co. Inc. has expanded its corporate venture capital (CVC) arm with a new United States headquarters to grow its investments in the United States and global companies. The company is known for its monosodium glutamate, and it owns a cosmetic brand, Jino, and is active in medical and electronic material fields.

- October 2023: Ningxia Eppen Biotech Co. Ltd invested USD 600 million in Amino acid production in Brazil. The primary goal of this project is to achieve an annual production of approximately 350 thousand tons of different amino acids including MSG, as well as by-products totaling about 200 thousand tonnes. This initiative is expected to create around a thousand job opportunities.

Global Monosodium Glutamate (MSG) Market Report Scope

Monosodium glutamate (MSG) is a flavor enhancer often added to restaurant foods, canned vegetables, soups, deli meats, and other foods.

The global monosodium glutamate (MSG) market is segmented by application into noodles, soups and broth, meat products, seasonings and dressings, and other applications. Other MSG applications include other savory foods such as sauces and snacks/meals. In terms of geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts were made based on value (USD).

By Product Form

| Powder/Crystalline |

| Granules |

| Micro-encapsulated (low-dust) |

| Liquid MSG Solutions |

By Application

| Food Processing | Noodles, Soups & Broth |

| Meat Products | |

| Seasonings & Dressings | |

| Sauces & Condiments | |

| Others | |

| Food-service/QSR & Catering | |

| Household/Retail | |

| Animal Feed & Pet Food | |

| Pharmaceuticals |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Form | Powder/Crystalline | |

| Granules | ||

| Micro-encapsulated (low-dust) | ||

| Liquid MSG Solutions | ||

| By Application | Food Processing | Noodles, Soups & Broth |

| Meat Products | ||

| Seasonings & Dressings | ||

| Sauces & Condiments | ||

| Others | ||

| Food-service/QSR & Catering | ||

| Household/Retail | ||

| Animal Feed & Pet Food | ||

| Pharmaceuticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the MSG market?

The MSG market size stands at USD 6.68 billion in 2026 and is projected to reach USD 8.31 billion by 2031.

Which region is expanding fastest in MSG consumption?

North America leads growth with a 6.21% CAGR through 2031 as sodium-reduction mandates and foodservice recovery propel adoption.

Which MSG product form is growing most quickly?

Micro-encapsulated MSG is the fastest-growing form, registering a 5.12% CAGR thanks to dust-control and controlled-release benefits.

How does MSG help reduce sodium in processed foods?

Replacing part of the salt with MSG preserves flavor while cutting total sodium by up to 30%, helping brands comply with tightening labeling regulations.

Page last updated on: