Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

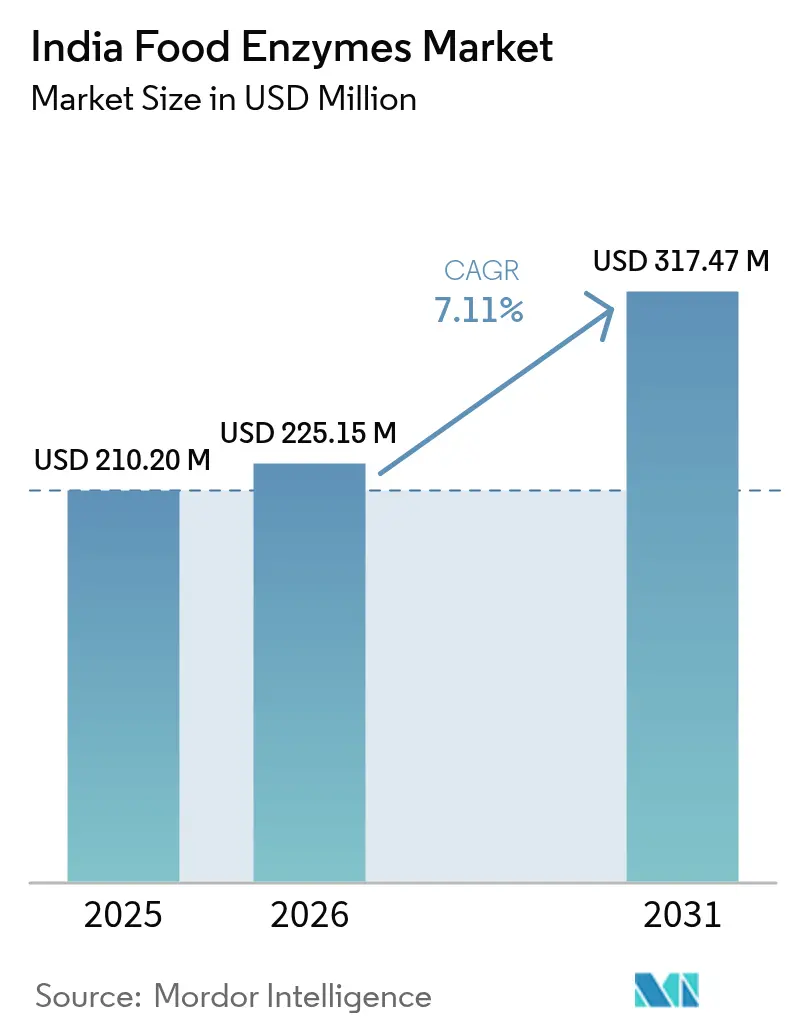

| Base Year Market Size (2025) | USD 210.20 Million |

| Market Size (2026) | USD 225.15 Million |

| Market Size (2031) | USD 317.47 Million |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

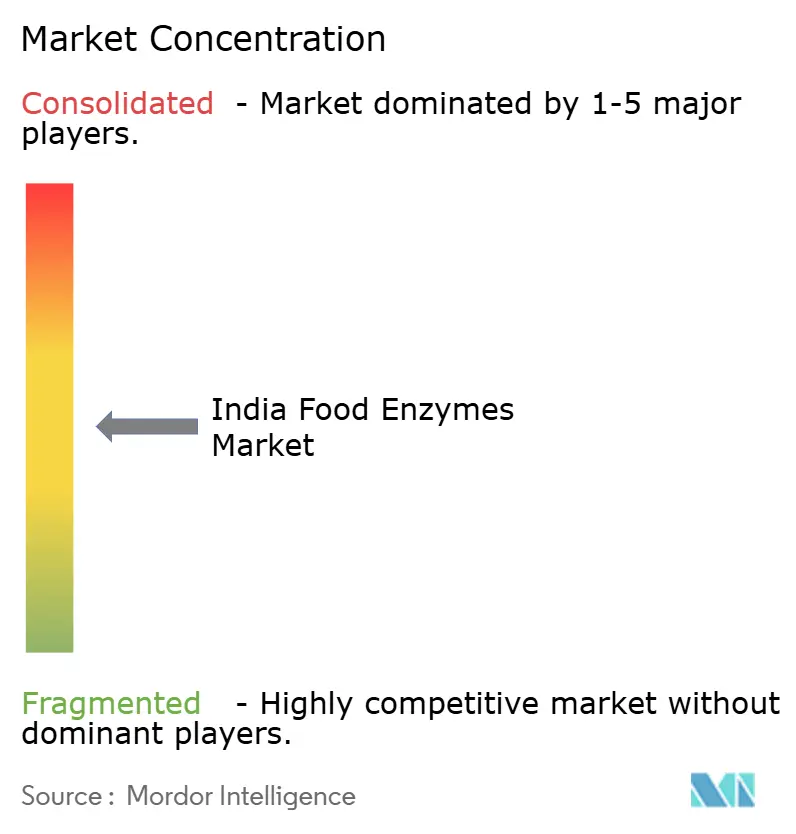

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Food Enzymes Market Analysis by Mordor Intelligence

The India food enzymes market size is expected to grow from USD 210.20 million in 2025 to USD 225.15 million in 2026 and is forecast to reach USD 317.47 million by 2031 at 7.11% CAGR over 2026-2031. This growth trajectory is bolstered by strong policy incentives, the consolidation of organized bakery chains, and the swift expansion of modern dairy plants. Both multinational and domestic players are in a race to localize manufacturing, enhance cold-chain reliability, and introduce clean-label formulations catering to urban consumers. Public-sector investments through the Production-Linked Incentive scheme, along with state-level mega food parks, have spurred capacity additions in bakery, beverage, and dairy sectors. This, in turn, has heightened enzyme demand as processors aim for better yields, extended shelf life, and quality suitable for exports. The market's addressable base is further expanded by a growing preference for natural processing aids, increasing disposable incomes in Tier-1 cities, and a rise in craft brewery start-ups. However, industry experts warn that challenges like fragmented cold storage, stringent five-day import testing, and persistent misconceptions about genetically modified microorganisms could temper short-term growth.

Key Report Takeaways

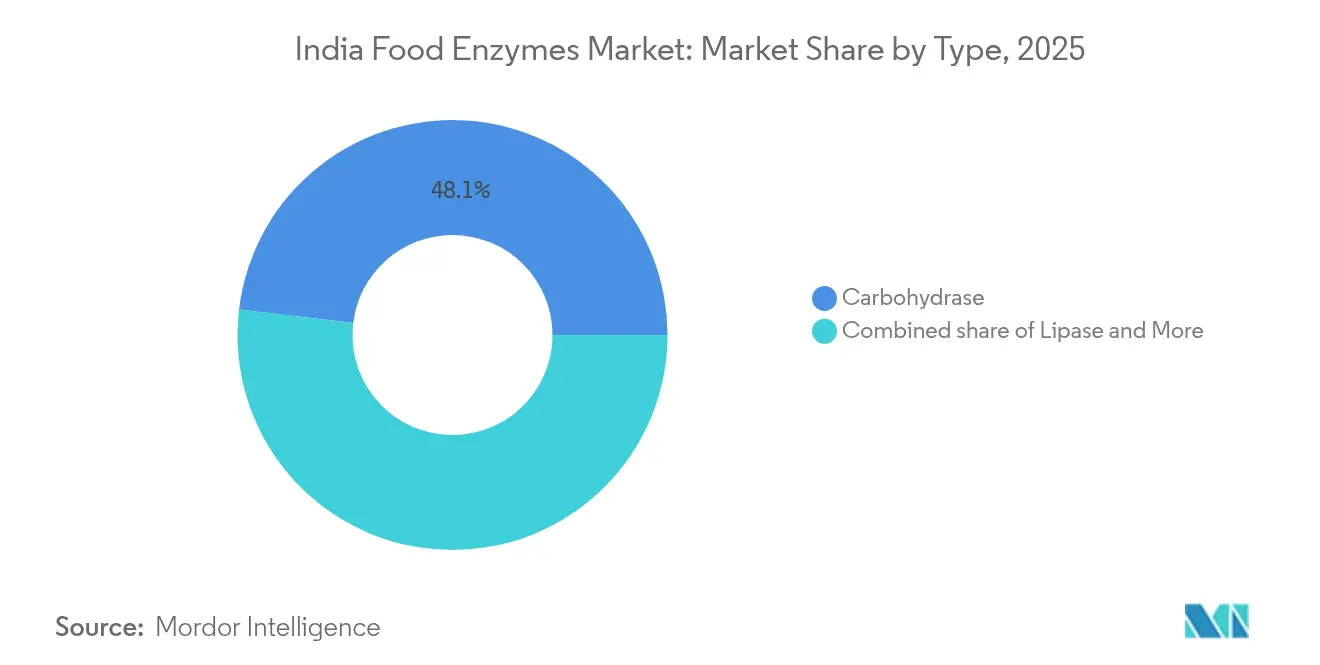

- By Type, carbohydrase enzymes captured 48.10% of 2025 revenue, the highest India food enzymes market share, whereas lipase is forecast to advance at a 7.12% CAGR through 2031.

- By Form, powder formulations accounted for a 70.85% share of the India food enzymes market size in 2025, yet liquid concentrates record a stronger 6.95% CAGR to 2031.

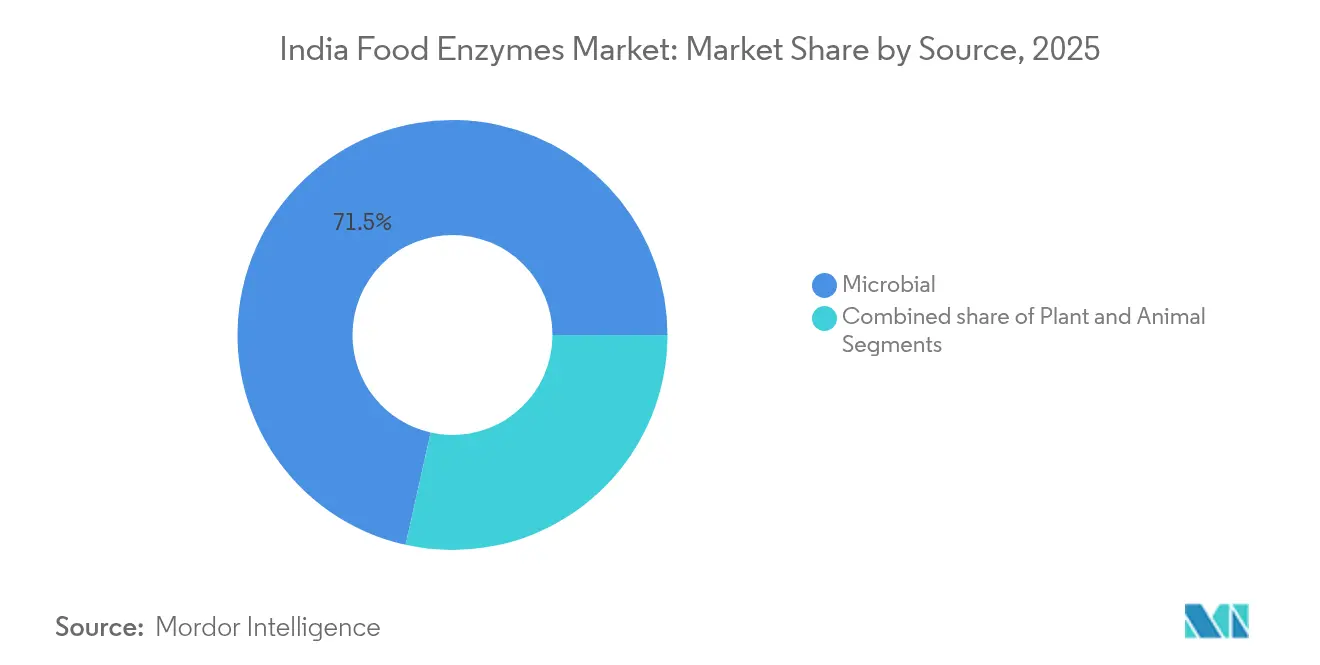

- By Source, microbial sources held 71.50% of 2025 sales, but plant-derived alternatives are expanding at a 6.98% CAGR through 2031.

- By Application, bakery and confectionery led demand with a 46.10% revenue share in 2025, while dairy and desserts are projected to register a 7.15% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Food Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of India's organised bakery sector | +1.2% | National, with concentration in Maharashtra, Gujarat, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| Government Production-Linked Incentive (PLI) scheme for food processing | +1.5% | National, with early gains in states with mega food parks (Punjab, Andhra Pradesh, Gujarat) | Short term (≤ 2 years) |

| Rising demand for clean-label/natural ingredients | +1.1% | National, urban metros and Tier-1 cities leading adoption | Medium term (2-4 years) |

| Growth of India's dairy and cheese processing capacity | +1.3% | National, with strongholds in Gujarat, Uttar Pradesh, Rajasthan, Punjab | Long term (≥ 4 years) |

| Surge in craft brewery start-ups adopting enzyme blends | +0.8% | Urban clusters in Bengaluru, Pune, Gurgaon, Mumbai | Medium term (2-4 years) |

| Adoption of precision-fermented enzymes by SME manufacturers | +0.7% | National, with early adoption in industrial hubs (Maharashtra, Gujarat, Tamil Nadu) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid expansion of India’s organized bakery sector

Organized bakery chains and industrial bread manufacturers are increasingly capturing market share, sidelining unbranded kirana-store suppliers. This shift has led to a heightened demand for standardized enzyme improvers, which ensure a consistent crumb texture, extend shelf life, and lessen the dependence on chemical emulsifiers. As the trend leans towards packaged breads, buns, and sweet goods, the adoption of enzymes has surged. This is because large-scale production lines now demand precise dough rheology and predictable fermentation windows, capabilities that only enzyme blends can offer, especially amidst varying flour quality and ambient humidity. Puratos India, with its enzyme-based bread improvers like Soft'r Toast, utilizes amylase and hemicellulase technologies. These not only enhance softness and resilience but also adhere to non-bromated regulatory standards. This strategic positioning allows Puratos to tap into the growing volume as regional bakeries refine their formulations. Meanwhile, Kerry's June 2024 introduction of Biobake Fresh Rich, a starch-acting enzyme tailored for high-sugar baked goods, fills a crucial void. This enzyme extends the shelf life of sweet products boasting over 20% sugar content, a market segment that organized bakeries are aggressively targeting to rival traditional mithai. Additionally, the PLI scheme's focus on value addition and export readiness is nudging bakeries towards enzyme solutions. These solutions not only curtail food waste but also bolster supply-chain resilience, marrying cost efficiency with sustainability, a narrative that holds significant weight in export markets.

Government production-linked incentive (PLI) scheme for food processing

With an outlay of Rs 10,900 crore, the PLI scheme has already disbursed Rs 1,155 crore to 171 beneficiaries by 2024. This reshaping of capital allocation in food processing sees enzyme suppliers emerging as indirect beneficiaries. As processors invest in yield optimization, waste valorization, and product differentiation to meet subsidy thresholds, enzyme applications play a pivotal role[1]Source: Press Information Bureau, “PLI Scheme Disbursements,” pib.gov.in . From juice clarification and dairy protein modification to extending bakery shelf life, these applications align with the scheme's mandate for value-added products and bolstering export competitiveness. However, the scheme's emphasis on large-scale projects, as highlighted by FSSAI, inadvertently amplifies the technology gap. While PLI recipients benefit, the 2.5 million unregistered food businesses, lacking the capital for enzyme formulation co-investment, find themselves at a disadvantage. Furthermore, the scheme's ambitious target of creating 289,000 jobs by 2024 hints at a workforce expansion in food processing. This growth is likely to elevate technical literacy and foster a greater adoption of enzyme-based innovations, especially as trained personnel transition between firms. Additionally, the government's Pradhan Mantri Kisan Sampada Yojana, which backs mega food parks and cold-chain infrastructure, works in tandem with the PLI. By easing logistical challenges for enzyme distribution, it aims to bridge the gaps, though connectivity issues in Tier-2 and Tier-3 regions still pose a challenge.

Rising demand for clean-label/natural ingredients

As consumers increasingly scrutinize ingredient lists and social media amplifies concerns over food additives, processors are gravitating towards enzyme-based solutions. These solutions are replacing synthetic emulsifiers, preservatives, and texturants, but the shift is not uniform between urban and rural markets. Puratos' Intens Soft and Fine, an enzyme formulation that mimics mono- and diglycerides (E471) and promotes cleaner labels, showcases how enzyme suppliers are marketing technical functionalities as consumer benefits. However, the adoption of such solutions is contingent on processors' willingness to shoulder the 2 to 3 times higher costs of enzyme improvers compared to traditional chemical aids. This clean-label movement aligns with FSSAI's October 2024 amendments to food additive regulations, which impose stricter labeling requirements and elevate compliance costs. These changes inadvertently benefit enzyme suppliers, as their products, qualifying as processing aids rather than additives, encounter lighter disclosure obligations. Furthermore, enzyme manufacturers are capitalizing on India's BioE3 policy, unveiled in August 2024, which sets an ambitious USD 300 billion bioeconomy target by 2030[2]Source: Department of Biotechnology, “BioE3 Policy Highlights,” dbtindia.gov.in . They are positioning precision-fermented enzymes as congruent with national sustainability objectives, even as commercial-scale production is still in its infancy.

Growth of India's dairy and cheese processing capacity

India's rising milk production, now funneled into factory processing, is bolstering demand for enzymes pivotal in cheese making, yogurt texturing, lactose hydrolysis, and whey valorization. With a Rs 11,500 crore investment plan, GCMMF, India's largest dairy cooperative, is not just expanding capacity but also diversifying its product range. This move underscores a strategic bet on value-added segments like enzyme-modified cheese and probiotic dairy desserts. These products, reliant on microbial lipases and proteases, aim for enhanced flavor profiles and extended shelf stability. Enzyme suppliers are keenly attuned to this evolving landscape. Novonesis showcases this with its SpiceIT M100, a microbial lipase tailored for cheese, and the Vertera Umami MG enzyme, enhancing umami in plant-based products. As the dairy sector eyes a growth spurt to 300 million metric tons by 2030, the strain on existing enzyme supply chains becomes evident, especially for liquid formulations reliant on cold chains. Yet, this challenge presents a golden opportunity for domestic enzyme manufacturers to localize production and curtail import reliance. Highlighting the strategic importance of enzymes in this landscape, Kerry's November 2024 acquisition of Novonesis' lactase business for EUR 145.4 million (around USD 155 million) spotlights the burgeoning lactose-free dairy segment in India. As urban consumers increasingly self-diagnose lactose intolerance, the demand for digestive-health solutions surges.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost-to-benefit ratio for small food processors | -0.9% | National, acute in Tier-2/3 cities and rural processing clusters | Short term (≤ 2 years) |

| Stringent FSSAI approval and labelling requirements | -0.6% | National, with a compliance burden higher for importers and new entrants | Medium term (2-4 years) |

| Enzyme cold-chain gaps in Tier-2/3 cities | -0.5% | Tier-2/3 cities across Uttar Pradesh, Bihar, Madhya Pradesh, Odisha | Medium term (2-4 years) |

| Consumer misconceptions linking enzymes to GMOs | -0.4% | National, with higher sensitivity in urban metros exposed to social media | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost-to-benefit ratio for small food processors

Enzyme formulations, priced at 2 to 3 times the cost of traditional processing aids like potassium bromate or chemical emulsifiers, pose a financial hurdle for India's 2.5 million unregistered food businesses. This challenge is particularly pronounced for the 98% of food processing units classified as micro, small, and medium enterprises, as highlighted by the FSSAI. In Tier-2 and Tier-3 cities, small processors, often operating on tight margins, frequently lack the technical know-how to assess the total-cost-of-ownership benefits of enzymes. These benefits include yield improvement, waste reduction, and extended shelf-life. As a result, they often resort to cheaper chemical alternatives, overlooking the long-term economic and regulatory advantages that enzymes offer. While the government's Pradhan Mantri Formalisation of Micro Food Processing Enterprises scheme, boasting a Rs 10,000 crore outlay, aims to provide credit access and capacity-building support, its impact is limited. Notably, it doesn't directly subsidize the adoption of enzymes. Amano Enzyme's corporate article from March 2024 underscores the cost savings from enzymes, highlighting benefits like faster processing times, lower temperatures, and diminished spoilage. However, this message hasn't resonated with rural processor networks, where informal knowledge transfer and price sensitivity heavily influence purchasing decisions.

Stringent FSSAI approval and labelling requirements

FSSAI's October 2024 amendment to import regulations mandates a 5-day laboratory turnaround for enzyme consignments and tightens contaminant limits for heavy metals, pesticides, and mycotoxins. These changes elevate compliance costs and working-capital demands for importers[3]Source: Food Safety and Standards Authority of India, “Import Regulation Amendments 2024,” fssai.gov.in. Smaller distributors, lacking in-house testing infrastructure, feel the brunt of these regulations. In March 2024, FSSAI introduced a temporary active list for processing aids, including enzymes. This move, while reducing uncertainty through a pre-approval pathway, inadvertently lengthens the time-to-market for novel enzyme formulations. As a result, innovators find themselves at a disadvantage compared to incumbents with legacy approvals. FSSAI's 2022 clarification states that if genetically modified microorganism-derived enzymes have a GMM content exceeding 1%, they necessitate separate labeling. Some processors view this disclosure burden as a potential consumer-facing liability, despite enzymes being processing aids not present in final products. Collectively, these regulations seem to bolster large, well-capitalized enzyme suppliers, equipped with regulatory affairs teams and established relationships with FSSAI. Conversely, they pose heightened challenges for new entrants and niche biotechs, especially those developing precision-fermented enzymes under the BioE3 policy framework.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Carbohydrase Dominance Anchors Bakery and Beverage Demand

In 2025, carbohydrase enzymes accounted for 48.10% of the market revenue, highlighting their roles in dough conditioning, juice clarification, and fiber modification. Lipase is the fastest-growing enzyme, with a 7.12% CAGR through 2031, driven by increased enzyme-modified cheese production and craft breweries exploring flavor-release formulations. Within the carbohydrase segment, amylases dominate, aiding bakery improvers in controlling starch retrogradation and maintaining crumb softness, critical for packaged bread manufacturers targeting a 7 to 14-day shelf life in India's humid climate. Pectinases enhance yield and clarity for juice and beverage processors, while cellulases are used in fiber-enriched breads and plant-based protein texturing, though adoption is limited by cost and lack of technical support in Tier-2 cities. Protease enzymes, the second-largest category, are used in dairy protein hydrolysis, meat tenderization, and brewing, with Advanced Enzymes Technologies reporting significant growth in its food bio-processing segment.

Lipase growth is fueled by India's expanding enzyme-modified cheese market and the rise of plant-based dairy alternatives, which use lipases to replicate butterfat flavors. Novonesis' SpiceIT M100 microbial lipase, designed for cheese applications, and Kerry's EUR 145.4 million acquisition of Novonesis' lactase business in November 2024, underscore the strategic importance of specialty enzymes in India's dairy sector. Amano Enzyme's Lipase GS "Amano" 250G, showcased at Food Ingredients Asia 2024, targets enzyme-modified cheese and cocoa butter equivalent production, aligning with India's growing confectionery and premium dairy segments. Other enzymes, such as transglutaminases and glucose oxidases, are gaining traction in meat restructuring and gluten-free baking, supported by CSIR-NIIST's research on phytase thermostability and enzyme engineering for Indian food matrices.

By Form: Powder Formulations Retain Cost and Handling Advantages

In 2025, powder enzymes accounted for 70.85% of total revenue, driven by their cost-effectiveness, ambient-temperature stability, and ease of handling, especially for small and medium enterprises (SMEs) lacking refrigerated storage. However, this segment is projected to grow at only 5.71% through 2031, indicating a shift toward liquid concentrates in automated production lines. Powder formulations suit India's fragmented food processing sector, where 98% of units are MSMEs in Tier-2 and Tier-3 cities with limited cold-chain access and intermittent power supply. Products like Puratos India's Soft'r Toast and Intens Freshness, both powdered enzyme-based improvers, demonstrate how suppliers adapt to infrastructure constraints while ensuring performance in bakery applications. Liquid enzymes, though growing more slowly, offer benefits like precise dosing, faster dispersion, and reduced dust exposure, making them preferred by large-scale dairy and beverage processors with automated systems.

The choice between powder and liquid enzymes also reflects regulatory and cost considerations. Liquid enzymes require cold-chain logistics, but India's 8,671 cold storage facilities cannot uniformly support this, especially in Tier-2 and Tier-3 cities, where only 15% to 20% of national capacity exists, according to the National Centre for Cold-chain Development. Powder enzymes avoid this issue but face challenges in achieving uniform dispersion during high-speed mixing, which suppliers address with granulation technologies and carrier systems. DSM-Firmenich’s USD 100 million investment over 2 to 3 years to expand manufacturing plants and laboratories in India may include capacity for liquid enzyme formulations, anticipating infrastructure improvements. The slower growth of the powder segment reflects saturation in traditional bakery applications, while liquid enzymes are capturing demand in dairy, beverages, and plant-based proteins, where precise dosing and rapid activity onset justify the cold-chain premium.

By Source: Microbial Enzymes Lead on Regulatory Acceptance and Scale Economics

In 2025, microbial-sourced enzymes dominated the market, accounting for 71.50% of total revenue. This dominance is driven by the FSSAI's endorsement of genetically modified microorganism-derived enzymes as processing aids, along with fermentation-scale economies and the technical versatility of bacterial and fungal strains in producing amylases, proteases, and lipases. While plant-derived enzymes hold a smaller market share, they are growing at 6.98% annually through 2031, fueled by clean-label mandates and consumer scrutiny over GMM origins. This creates opportunities for suppliers of enzymes like papain, bromelain, and ficin, extracted from papaya, pineapple, and fig. Microbial enzymes dominate due to fermentation-based production, which ensures consistent quality, high titers, and cost advantages over plant extraction, particularly for high-volume applications like bakery amylases and dairy proteases. The FSSAI's October 2022 notification on GMM-derived enzymes, clarifying labeling requirements and safety assessments, has reduced regulatory uncertainties and encouraged investments in fermentation capacity.

Animal-sourced enzymes, primarily rennet for cheese making, are losing market share as microbial and plant-based alternatives gain acceptance among vegetarian consumers and processors seeking halal and kosher certifications. India's vegetarian population and religious dietary restrictions drive demand for non-animal enzymes, a trend leveraged by companies like Novonesis and Kerry through microbial rennet and plant-based coagulants. The BioE3 policy, targeting a USD 300 billion bioeconomy by 2030, is expected to accelerate research and development in microbial enzyme engineering, though commercial-scale production remains nascent and concentrated among players like Advanced Enzymes Technologies and Infinita Biotech, as noted by the Department of Biotechnology. Plant-derived enzyme growth is further supported by Amano Enzyme's focus on non-GMO microbial enzymes and classical fermentation, catering to processors wary of GMO-derived products.

By Application: Bakery Scale Meets Dairy Momentum

In 2025, bakery and confectionery applications accounted for 46.10% of the demand, underscoring the organized bakery sector's dependence on enzyme improvers. These enzymes play a pivotal role in dough conditioning, extending shelf life, and replacing emulsifiers. However, the dairy and dessert segment is set to outpace all other end-uses, boasting a projected CAGR of 7.15% through 2031. This growth is fueled by GCMMF's substantial investment of Rs 11,500 crore and a forecasted milk production in India of 216.5 million metric tons by 2025. Bakery enzymes, especially amylases and hemicellulases, tackle challenges like crumb firming, staling, and inconsistencies in volume due to varying flour quality. This makes them essential for industrial bread and bun manufacturers aiming for an extended shelf life. Innovations in mature bakery applications are evident, with Kerry's Biobake Fresh Rich, introduced in June 2024 for high-sugar baked goods, and Puratos' Intens Freshness, which prolongs softness for up to 14 days.

The growth in dairy and desserts is largely attributed to enzyme applications in cheese making, yogurt texturing, lactose hydrolysis, and the modification of whey proteins. GCMMF's expansion in capacity is driving a structural demand for microbial lipases and proteases. In a notable move, Novonesis sold its lactase business to Kerry for EUR 145.4 million in November 2024, highlighting the strategic importance of the lactose-free dairy segment. This segment is witnessing an expansion, particularly as urban consumers increasingly prioritize digestive health. While beverages like juice clarification and craft beer brewing represent a smaller segment, they are on the rise, especially with the anticipated growth of microbreweries. Meat products, soups, sauces, and dressings are still considered niche applications. Their growth is limited by India's predominantly vegetarian population and a cautious adoption of enzymes in traditional condiment production. However, there's a notable uptick in the use of protease-based meat tenderizers within quick-service restaurant supply chains.

Geography Analysis

India's food enzymes market is concentrated in Maharashtra, Gujarat, and Tamil Nadu due to their food processing clusters, dairy cooperatives, and bakery chains. Maharashtra, contributing 15%-18% of India's food processing output, drives amylase and lipase consumption through its bakery and dairy hubs. Gujarat, with a 12%-15% share, benefits from GCMMF's Rs 11,500 crore investment and mega food parks, sustaining demand for dairy enzymes and beverage aids. Tamil Nadu, contributing 10%-12%, combines bakery clusters with growing plant-based protein manufacturers, boosting protease and transglutaminase applications. Uttar Pradesh, despite being the largest milk producer, faces limited enzyme adoption due to fragmented infrastructure and cold-chain gaps.

Punjab and Karnataka are emerging hubs, driven by government incentives and innovation. Punjab's food processing policy attracts bakery and dairy investments, while Bengaluru's innovation cluster supports precision-fermentation startups under the BioE3 policy targeting a USD 300 billion bioeconomy by 2030. Bengaluru's craft beer market, with 85 brewpubs and a 25%-50% summer sales surge in 2024, offers niche enzyme opportunities despite regulatory and taxation challenges. Tier-2 and Tier-3 cities in Uttar Pradesh, Bihar, Madhya Pradesh, and Odisha hold potential but face low enzyme penetration due to cold-chain gaps and reliance on cheaper chemical alternatives. India's cold storage facilities, concentrated in six states, leave Tier-2 and Tier-3 cities with only 15%-20% of infrastructure, risking enzyme spoilage, as per the National Centre for Cold-chain Development.

Regional disparities in regulatory compliance and technical literacy affect enzyme adoption. Maharashtra and Gujarat, with active FSSAI offices, show higher awareness, while less-developed states lack technical support. The National Centre for Cold-chain Development's October 2024 quality certification program aims to improve logistics, though benefits may take until 2026. DSM-Firmenich's USD 100 million investment in manufacturing and laboratories aims to position India among the top three global markets within five years, reflecting optimism in infrastructure improvements and regional growth.

Competitive Landscape

In the Indian food enzymes market, global leaders such as Novonesis (a EUR 3.7 billion biosolutions entity formed in February 2024 from the merger of Novozymes and Chr. Hansen) and DSM-Firmenich dominate through their expertise in technical services, regulatory affairs, and fermentation intellectual property. Domestic players like Advanced Enzymes Technologies and Maps Enzymes leverage cost efficiencies and regional distribution networks to cater to Tier-2 and Tier-3 processors. A strategic divide is evident, with multinationals focusing on portfolio expansion, precision-fermentation research and development, and mergers and acquisitions to consolidate applications in bakery, dairy, and plant-based proteins. In contrast, Indian biotech firms prioritize cost-effective microbial enzymes and localized technical support to penetrate small and medium enterprises. Untapped opportunities exist in areas such as precision-fermented lipases for plant-based cheese, enzyme blends for craft brewing, and cold-chain-stable liquid formulations for automated dairy lines, where neither global majors nor domestic players have established dominance. Emerging disruptors like Infinita Biotech and Lumis Biotech are targeting niche applications in detergent and food enzymes, though their scale remains limited compared to incumbents.

Technology adoption is reshaping competitive dynamics, with enzyme suppliers investing in fermentation-platform technologies, enzyme engineering, and bioprocess optimization to reduce production costs and expand application scope. Kerry's May 2025 acquisitions of c-LEcta (Germany) and Enmex (Mexico) highlight this trend, as the company integrates enzyme discovery, bioprocess development, and regional production capabilities. This model could extend to India if regulatory and infrastructure conditions improve. Amano Enzyme is actively developing intellectual property, with patent filings for maltotriose-producing amylases, protein glutaminases for plant-based beverages, and cyclodextrin-producing enzymes for flavor modification. These innovations target India's rice processing, plant-based dairy, and clean-label segments. Similarly, Puratos' June 2024 partnership with Bota Bio aims to accelerate enzyme discovery using digital tools, lab automation, and bioinformatics, positioning the company to respond swiftly to clean-label and sustainability trends.

Regulatory changes are also influencing market dynamics. FSSAI's October 2024 amendments to import regulations and contaminant limits favor well-capitalized suppliers with in-house testing infrastructure and regulatory affairs teams, raising entry barriers for new players and niche biotechs. These changes create a competitive advantage for established players with robust resources, further consolidating the market. As the industry evolves, the interplay of technology adoption, strategic acquisitions, and regulatory frameworks will continue to shape the competitive landscape of India's food enzymes market.

India Food Enzymes Industry Leaders

Koninklijke DSM N.V.

Novozymes A/S

Advanced Enzyme Technologies Limited

Lumis Biotech Pvt. Ltd.

International Flavors & Fragrances

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: DSM-Firmenich announced a USD 100 million (Rs 835 crore) investment over 2 to 3 years to establish new manufacturing plants, debottleneck existing facilities, and expand laboratories in India, targeting India as a top-3 global market within 5 years. The investment builds on USD 500 million deployed over the past decade and reflects confidence in India's food processing trajectory and enzyme demand growth.

- August 2024: The Indian government launched the BioE3 (Biotechnology for Economy, Environment, and Employment) policy, targeting a USD 300 billion bioeconomy by 2030 and emphasizing precision fermentation, biomanufacturing, and enzyme production. The policy includes funding for Smart Proteins and fermentation science, creating opportunities for enzyme suppliers to access grants and partnerships for developing precision-fermented enzymes.

- August 2024: AB Enzymes and APC Group signed an exclusive distribution agreement for pulp and paper enzymes covering China, India, Southeast Asia, and the Middle East. While the agreement focuses on pulp and paper, it signals AB Enzymes' intent to expand regional distribution infrastructure that could support food enzyme sales in India.

India Food Enzymes Market Report Scope

Food enzymes are protein molecules that are safe for ingestion and are utilized by the food industry throughout food production to increase the food's safety, quality, and process effectiveness. The India food enzymes market is classified according to type and application. Based on product type, the market is segmented into carbohydrases, proteases, lipases, and other types. By application, the market is segmented into bakery, confectionery, dairy, and frozen desserts; meat, poultry, and seafood products; beverages; and other applications. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

Type

| Carbohydrase | Amylases |

| Pectinases | |

| Cellulases | |

| Others | |

| Protease | |

| Lipase | |

| Other Enzymes |

Form

| Powder |

| Liquid |

Source

| Plant |

| Microbial |

| Animal |

Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Soups, Sauces, and Dressings |

| Other Applications |

| Type | Carbohydrase | Amylases |

| Pectinases | ||

| Cellulases | ||

| Others | ||

| Protease | ||

| Lipase | ||

| Other Enzymes | ||

| Form | Powder | |

| Liquid | ||

| Source | Plant | |

| Microbial | ||

| Animal | ||

| Application | Bakery and Confectionery | |

| Dairy and Desserts | ||

| Beverages | ||

| Meat and Meat Products | ||

| Soups, Sauces, and Dressings | ||

| Other Applications |

Key Questions Answered in the Report

How large is the India food enzymes market in 2026?

The market stands at USD 225.15 million in 2026 and is forecast to grow at a 7.11% CAGR over 2026-2031.

Which enzyme type dominates demand?

Carbohydrase enzymes lead with 48.10% of 2025 revenue due to broad use in bakery and beverage processing.

What is driving the shift toward liquid enzyme formats?

Automation in large dairy and beverage plants favors liquid concentrates because they disperse faster and allow precise dosing.

Why are microbial enzymes preferred over animal-based alternatives?

Microbial sources align with vegetarian diets, offer cost-efficient fermentation, and meet halal and kosher certification.

What regulatory hurdles exist for new enzyme entrants?

FSSAI requires a five-day laboratory clearance for imports and a pre-approval path for novel processing aids, increasing compliance costs.

Page last updated on: