Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.34 Billion |

| Market Size (2026) | USD 3.49 Billion |

| Market Size (2031) | USD 4.34 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

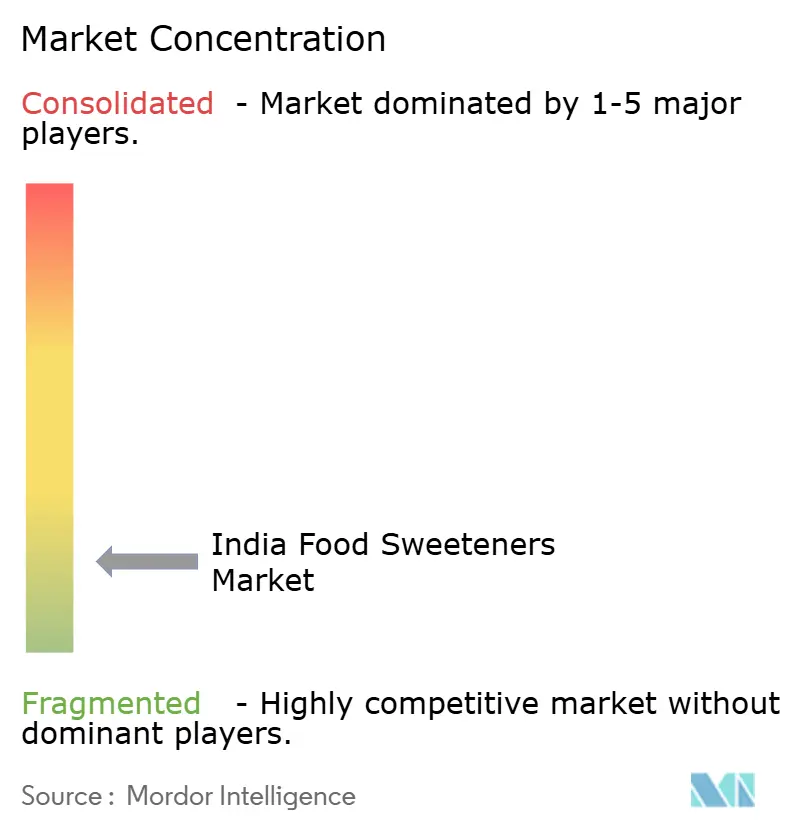

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Food Sweeteners Market Analysis by Mordor Intelligence

The India food sweeteners market size was valued at USD 3.34 billion in 2025 and estimated to grow from USD 3.49 billion in 2026 to reach USD 4.34 billion by 2031, at a CAGR of 4.49% during the forecast period (2026-2031). Demand is tilting toward low-calorie options, yet bulk sweeteners still anchor volume, allowing incumbents to defend price-sensitive channels even as new entrants scale fermentation capacity. Government ethanol blending mandates are tightening sugarcane availability, forcing manufacturers to diversify feedstocks and invest in biotechnology pipelines. Meanwhile, labeling reforms and faster ingredient approvals are lowering go-to-market friction for high-intensity alternatives, driving reformulation across beverages, bakery, and dairy. Competitive intensity remains pronounced because entry barriers are low, research and development costs are falling, and regional players continue to leverage proximity to agricultural basins and urban consumption hubs.

Key Report Takeaways

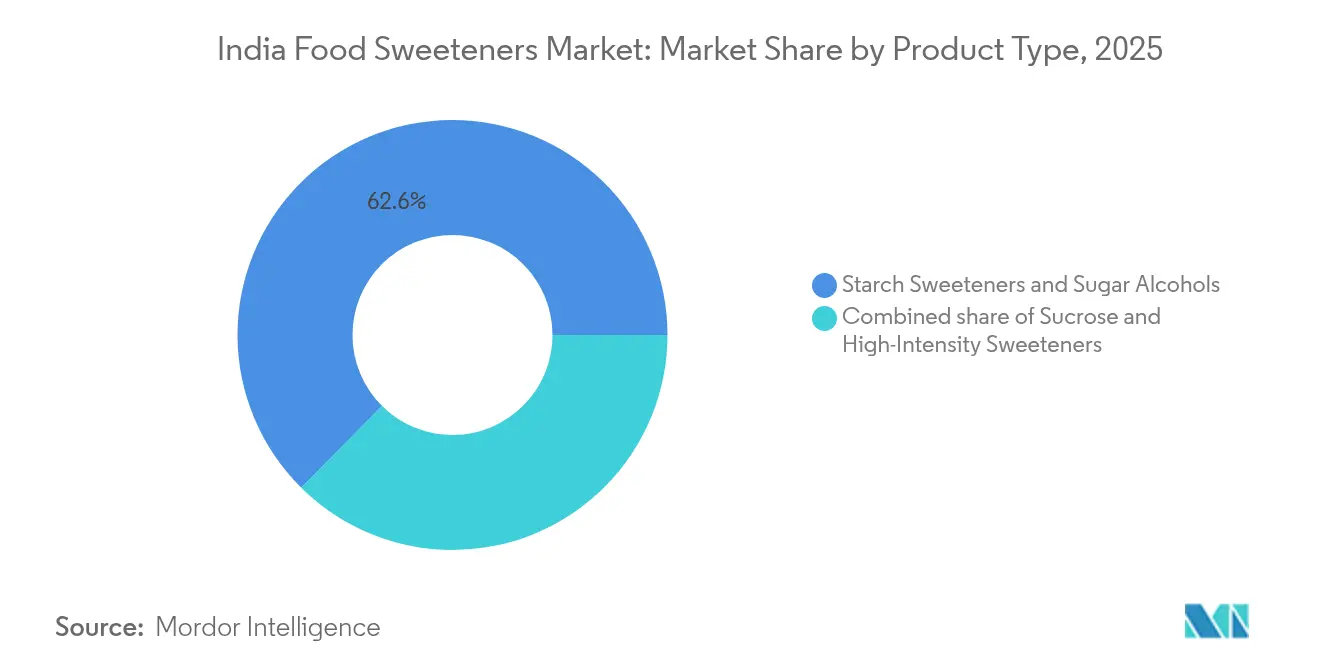

- By product type, starch sweeteners and sugar alcohols commanded 62.58% of the Indian sweeteners market share in 2025, while high-intensity sweeteners are forecast to grow at a 5.33% CAGR through 2031.

- By source, plant-based ingredients held 44.74% revenue share in 2025; fermentation-derived sweeteners are projected to expand at a 4.92% CAGR between 2026 and 2031.

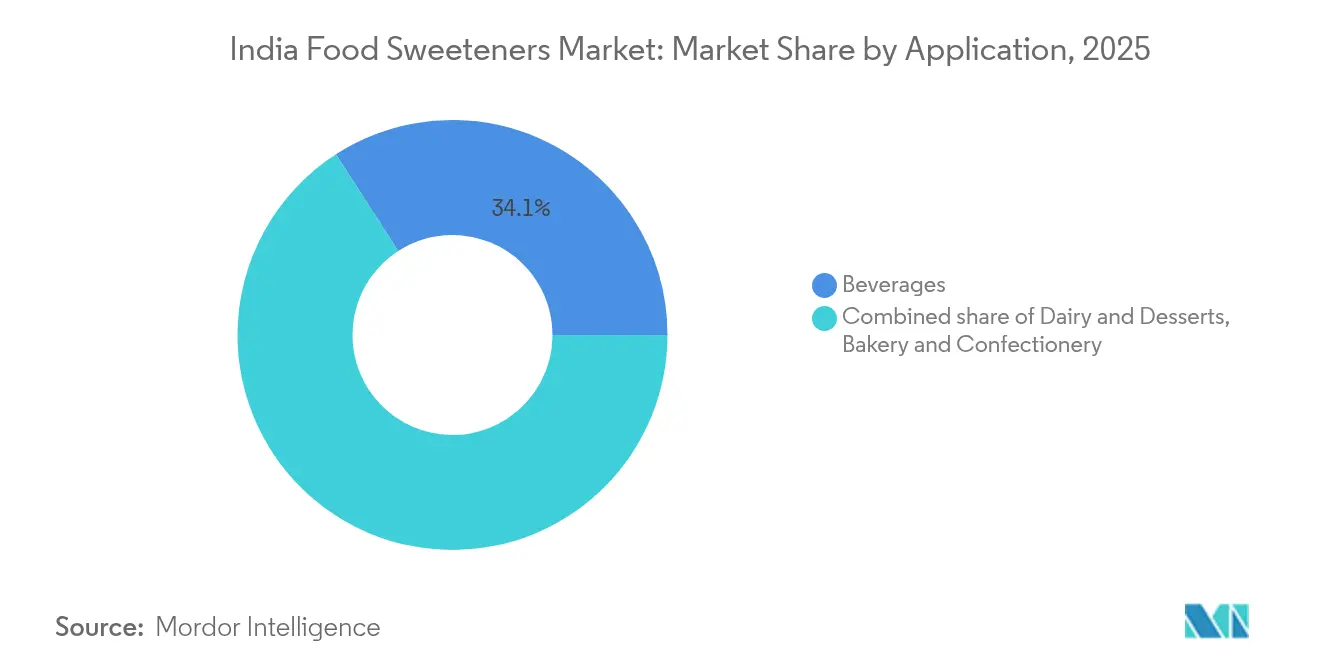

- By application, beverages accounted for 34.12% of the India sweeteners market size in 2025, while bakery and confectionery are advancing at a 5.44% CAGR to 2031.

- By geography, North India led with 40.85% revenue share in 2025; East India records the highest projected CAGR at 4.27% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Food Sweeteners Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes and obesity spur demand for low-/no-calorie sweeteners | 0.8% | National, urban-centric | Medium term (2-4 years) |

| Expansion of processed food and beverage manufacturing | 0.7% | North and West India, urban hubs | Short term (≤ 2 years) |

| Rising demand for clean-label formulations | 0.5% | National, metros and Tier 1 cities | Medium term (2-4 years) |

| Technological advancements in extraction and processing | 0.5% | Industrial clusters, pan-India | Long term (≥ 4 years) |

| Strong regulatory support for the use of Natural Sweeteners | 0.4% | National, with early gains in metros | Short term (≤ 2 years) |

| Fermentation-derived rare-sugar start-ups scaling in India | 0.3% | South and West India, biotech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of processed food and beverage manufacturing

The government's Production Linked Incentive Scheme (PLISFPI), along with complementary initiatives, has played a transformative role in accelerating the growth of the food processing market, achieving a remarkable 15.2% CAGR. These initiatives have focused on building modern infrastructure and strengthening export capabilities, positioning the sector for sustained growth. Between 2014–15 and 2022–23, the share of processed food exports in total agricultural exports witnessed a significant rise, increasing from 13.7% to 25.6%. This expansion in food processing has fueled a growing demand for sweeteners, particularly in the ready-to-eat and beverage segments, which continue to be major contributors to this trend. The increasing consumer preference for convenience foods and beverages, coupled with the rising disposable incomes and urbanization, has further amplified the demand for sweeteners. Moreover, state-level policies and fiscal incentives have been pivotal in attracting private investments, driving industrial development, and generating employment opportunities. These measures collectively underscore the sector's potential for long-term growth and its critical role in the broader economic landscape, Invest India, 2024[1]Invest India, "Food Processing", www.investindia.gov.in.

Rising demand for clean-label formulations

As consumers increasingly prioritize transparency and natural ingredients, a pronounced demand for clean labels emerges, especially in metropolitan and Tier 1 cities. Here, shoppers meticulously examine ingredient lists, showing a clear preference for plant-based or minimally processed sweeteners. This shift in consumer behavior is driving significant changes in the food and beverage industry. Regulatory bodies, notably the FSSAI, are playing a pivotal role. They've revamped labelling and display standards, pushing for clearer nutritional information. This move not only bolsters consumer trust but also hastens reformulation initiatives among manufacturers. Companies are responding by innovating their product offerings, leveraging this trend to differentiate their products and tap into premium market segments. This alignment with consumer preferences and regulatory requirements is expected to shape the competitive landscape in the coming years, according to the Food Compliance International, 2024.

Technological advancements in extraction and processing

Bioconversion and patented preservation techniques have boosted yields, leading to the commercialization of novel sweeteners like allulose and stevia Reb M. In India, both biotech startups and established sugar mills are investing in advanced processing lines to boost production efficiency and product quality. These investments are aimed at meeting the increasing demand for innovative sweeteners that align with consumer preferences for healthier options. Meanwhile, multinationals are leveraging proprietary formulation tools to enhance mouthfeel, solubility, and sensory profiles in their products. These tools enable companies to fine-tune their offerings, ensuring they meet both functional and sensory expectations of consumers. These innovations are increasingly safeguarded by patents, highlighting the sector's pivot towards an IP-centric growth model. This emphasis on intellectual property is spurring innovation, allowing companies to carve out a niche in a competitive market while meeting the rising demand for healthier, sustainable sweetener alternatives. Additionally, the focus on IP protection is fostering collaborations between research institutions and industry players, further accelerating advancements in the sweetener market.

Strong regulatory support for the use of natural sweeteners

Owing to the FSSAI's nod to allulose and stevia, and its efforts to align with global food additive benchmarks, the door has swung open for fresh product launches and a surge in foreign investments. These approvals have encouraged manufacturers to explore innovative formulations, catering to the growing demand for healthier and low-calorie alternatives. But the FSSAI's reach isn't limited to just greenlighting ingredients. With revamped labelling mandates and stringent food safety norms, they're not only influencing how consumers view products but also quickening the industry's innovation tempo. Updated labelling requirements ensure greater transparency, enabling consumers to make informed choices, while stricter safety standards push companies to adopt higher-quality practices. Today, the regulatory path charted by the sector stands as a pivotal factor in carving out competitive edges, particularly as compliance becomes a cornerstone of product development. Companies that proactively adapt to these evolving regulations are likely to gain a significant advantage in the market.

Restraints Impact Analysis*

| Rstraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow adoption of natural sweeteners in traditional recipes | -0.5% | Rural, Tier 2/3 cities | Long term (≥ 4 years) |

| Growing health consciousness among wider population | -0.4% | National, urban and rural | Medium term (2-4 years) |

| Growing preference for calorie reduction | -0.3% | Urban, health-focused segments | Short term (≤ 2 years) |

| Rising type 2 diabetes linked to high sugar consumption | -0.2% | National, high-prevalence states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Slow adoption of natural sweeteners in traditional recipes

India's culinary heritage, steeped in tradition, often favors sucrose and jaggery for their familiar taste. Even with regulatory nods and health campaigns championing natural sweeteners, their adoption in these age-old recipes has been sluggish. Cultural habits and a lack of awareness beyond urban locales pose hurdles, stalling broader market growth. The preference for traditional sweeteners is deeply ingrained, as they are not only integral to the flavor profile of many dishes but also hold cultural and emotional significance. While manufacturers dabble in hybrid formulations and ramp up educational efforts, the advancements remain modest. These efforts include introducing products that blend traditional and natural sweeteners to ease the transition for consumers and conducting targeted campaigns to raise awareness about the health benefits of natural alternatives. However, overcoming the structural challenges tied to cultural inertia and limited outreach in rural areas will require sustained and innovative strategies.

Growing health consciousness among wider population

Health-conscious consumers are increasingly seeking low-calorie and clean-label sweeteners. However, this trend has also heightened scrutiny on artificial ingredients and fostered skepticism towards emerging sweetener technologies. As a result, adoption rates for some product categories have lagged, pushing manufacturers to prioritize consumer education and adopt transparent labeling practices. To address these challenges, companies are investing in research and development to create innovative sweetener solutions that align with consumer preferences while meeting regulatory standards. Regulatory bodies are taking note: the FSSAI has rolled out updated labeling standards to bolster consumer trust, but their effectiveness hinges on widespread compliance across the industry. These standards aim to ensure that consumers have access to clear and accurate product information, ultimately fostering greater confidence in the market, according to the Food Compliance International, 2024[2]Food Compliance International, "FSSAI notified re-operationalisation of food labelling and display standards", www.foodcomplianceinternational.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: High-Intensity Sweeteners Accelerate Reformulation

India's sweeteners market is witnessing a notable shift, with high-intensity sweeteners projected to lead the growth at a 5.33% CAGR from 2026 to 2031. This trend is largely attributed to expanding regulatory approvals for ingredients like stevia and allulose, steering the market away from traditional bulk sweeteners. While starch sweeteners and sugar alcohols currently dominate the market, holding a 62.58% share in 2025, they continue to be favored for their cost-effectiveness in mass-market processed foods and beverages. Recent patent advancements, including the stabilization of allulose syrup and innovations in stevia Reb M, have enhanced taste profiles and solubility. This progress positions high-intensity sweeteners as formidable contenders in both mainstream and premium market segments.

The transition is further bolstered by the FSSAI's regulatory influence and its alignment with global additive standards, especially as beverage and bakery manufacturers adapt to shifting consumer preferences, as noted by Tate & Lyle PLC in 2024. Meanwhile, other product segments such as dextrose, HFCS, maltodextrin, and sugar alcohols like xylitol and sorbitol continue to cater to specific functional and cost requirements, especially in confectionery and dairy sectors. Yet, as health-driven innovations and reformulations gain momentum, the market share of these segments is anticipated to stabilize.

By Source: Fermentation-Based Sweeteners Reshape Supply Chains

Fermentation-based sweeteners are poised to outpace both plant-derived and artificial counterparts, with a projected growth rate of 4.92% CAGR from 2026 to 2031. This momentum is largely attributed to breakthroughs in microbial engineering, facilitating the cost-effective and environmentally-friendly production of rare and next-generation sugars. These advancements have made it possible to scale production while addressing sustainability concerns, a critical factor driving adoption across various industries, including food and beverages, pharmaceuticals, and personal care. While plant-based sweeteners command the largest market share at 44.74% in 2025, owing to a consumer tilt towards natural ingredients, artificial sweeteners, though still favored for budget-sensitive uses, grapple with challenges from the clean-label movement and heightened regulatory oversight. The demand for plant-based sweeteners is further supported by their perceived health benefits and their alignment with the growing trend of clean eating.

Local biotech startups and collaborations between academia and industry, especially in South and West India, are bolstering the fermentation-derived production landscape. These initiatives not only diminish reliance on imports but also spur swift product innovation. The involvement of academic institutions has been instrumental in advancing research and development, while startups bring agility and innovation to the market. As supply chains evolve and regulatory approvals broaden, this trend is anticipated to gain even more momentum. Additionally, government incentives and funding for biotech research are expected to further accelerate the adoption of fermentation-based sweeteners, creating a robust ecosystem for growth in the coming years.

By Application: Bakery and Confectionery Lead Growth, Beverages Dominate Demand

In response to a growing consumer demand for healthier, lower-calorie options, the bakery and confectionery sectors are set to witness a 5.44% CAGR growth from 2026 to 2031. This growth reflects the sector's ongoing reformulation efforts to align with shifting consumer preferences. Beverages, commanding a 34.12% share in 2025, continue to dominate, bolstered by a surge in ready-to-drink, functional, and sugar-free product launches. These innovations cater to the increasing demand for convenience and health-conscious choices.

Significant segments like dairy, sauces, dressings, and spreads are also evolving, adapting to shifting regulatory landscapes and consumer preferences. These segments are focusing on product reformulation and innovation to meet the dual objectives of compliance and consumer satisfaction. One notable trend is the use of multi-sweetener blends, which optimize taste, mouthfeel, and calorie content. This advancement, driven by proprietary formulation tools and extraction technology, is especially pertinent in the beverage sector, where challenges like solubility and stability are paramount. The integration of these blends not only enhances product quality but also addresses the growing demand for reduced-calorie beverages without compromising on flavor or texture.

Geography Analysis

In 2025, North India commands a dominant 40.85% share of the country's sweeteners market, thanks to its leadership in sugarcane farming and processed food production. This region's success is bolstered by a strong agricultural framework and its proximity to major urban centers. However, recent government initiatives, like the Ethanol Blended Petrol Programme, are reshaping supply chains. By channeling sugarcane towards biofuel, these policies are tightening the raw material supply for sweetener production, according to the Department of Food and Public Distribution, 2023.

East India is set to outpace others with a projected growth rate of 4.27% CAGR from 2026 to 2031. This surge is attributed to increasing urbanization, heightened investments in food processing, and proactive state measures to draw in private investments. As the urban-rural spending divide narrows and per capita calorie consumption rises, there's a noticeable tilt towards processed foods and beverages in dietary choices. Government initiatives and infrastructure enhancements further bolster the region's growth trajectory, according to the Ministry of Statistics and Programme Implementation, 2025.

While West and South India command smaller market shares, they're carving out a niche as innovation hotspots. These regions are particularly buzzing with fermentation-based sweetener startups and biotechnology enterprises. By harnessing collaborations between academia and industry, alongside state-backed incentives, they're making strides in specialty sweeteners and cutting-edge processing. Moreover, with Maharashtra and Karnataka topping the charts in sugar consumption per capita among rural demographics, there's a clear indication of both market promise and the urgency for public health measures.

Regulatory Landscape

Food sweeteners in India fall under the oversight of the Food Safety and Standards Authority of India (FSSAI), mainly through the Food Safety and Standards (Food Products Standards and Food Additives) Regulations, 2011. These rules set permitted sweetening agents and their conditions of use across food categories. In 2026, FSSAI continued to operationalize approvals for novel and non-specified ingredients using its published application-status tracker (status as of 3 June 2026), which gives manufacturers and importers more clarity on dossier requirements and authorization timelines.

Trade and compliance actions are also affecting category economics for high-intensity sweeteners. In March 2026, the Directorate General of Trade Remedies (DGTR) initiated an anti-circumvention investigation into alleged rerouting of Chinese-origin saccharin via Thailand to bypass countervailing duties, raising near-term risk for import-dependent supply chains. Separately, FSSAI issued multiple draft notifications in 2026 that replace older packaging and labelling references with the Labelling and Display Regulations, 2020 and Packaging Regulations, 2018. This reinforces the shift toward tighter label substantiation and harmonized additive references for reformulated, reduced-sugar products.

Value Chain Analysis

India's food sweeteners value chain starts with feedstocks such as sugarcane and grains (notably maize). Supply is supported by domestic milling and refining ecosystems concentrated in major sugar belts, including Uttar Pradesh and Maharashtra, along with derivative-processing clusters such as Gujarat, Maharashtra, and Tamil Nadu. Bulk sweeteners and starch-derived ingredients typically move through direct mill-to-industry contracts and regional wholesalers, while high-intensity sweeteners and polyols rely more on specialized ingredient distributors that bundle documentation, application support, and compliance services for food and beverage customers.

A key friction point is the structural reliance on imports for several high-intensity sweeteners, even as domestic production anchors most nutritive sweeteners and sugar derivatives. This import exposure increases sensitivity to trade actions, including the DGTR saccharin probe, and to FSSAI documentation requirements for additives and non-specified ingredients. As onboarding cycles lengthen, procurement is increasingly tied to supplier capability in regulatory dossiers, quality systems, and formulation support, particularly for beverage, bakery, and dairy reformulation programs that use multi-sweetener blends.

Competitive Landscape

India's sweeteners market showcases a fragmented landscape. This landscape is painted with the presence of multinational behemoths, regional stalwarts, and an emerging wave of fermentation-centric startups. The strategic chessboard is witnessing shifts: industry veterans like Tate & Lyle and Ingredion are pivoting towards specialty ingredients, innovation anchored in intellectual property, and product lines tethered to sustainability. These companies are focusing on developing solutions that cater to evolving consumer preferences, such as reduced sugar content and natural alternatives, while also addressing environmental concerns. In parallel, local enterprises are not just scaling their production but are also venturing into bioplastics and ethanol, diversifying their portfolios to remain competitive in a dynamic market.

Emerging white-space opportunities beckon in the realms of clean-label, plant-based, and fermentation-sourced sweeteners. Companies are harnessing proprietary technologies and forging academic alliances to carve out distinct market positions. The demand for clean-label products is driven by increasing consumer awareness of health and wellness, pushing firms to innovate and offer transparent ingredient lists. Biotechnology startups are the new disruptors, slashing production costs and accelerating product development. A surge in patent filings especially for extraction and solubility technologies like stevia Reb M and allulose syrup underscores a sector-wide shift towards innovation and the safeguarding of intellectual property, as highlighted by the USPTO in 2024. These advancements are enabling the development of sweeteners that not only meet taste and texture expectations but also align with regulatory and sustainability goals.

The regulatory landscape, particularly through ingredient approvals and labelling mandates, wields significant influence. The FSSAI's evolving standards not only shape competitive strategies but also play a pivotal role in cultivating consumer trust. Firms that swiftly navigate these regulatory waters and champion transparent supply chains stand poised to seize the growth opportunities of tomorrow. Companies that proactively engage with regulatory bodies and invest in compliance mechanisms are better equipped to mitigate risks and capitalize on emerging trends. Additionally, the emphasis on traceability and ethical sourcing is becoming a critical factor in building long-term consumer loyalty and market differentiation.

India Food Sweeteners Industry Leaders

-

Cargill Incorporated

-

Archer Daniels Midland Company

-

International Flavors & Fragrances Inc.

-

Kerry Group plc.

-

Tate & Lyle PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Ongoing product reformulation and ingredient modernization are creating whitespace for high-intensity and next-generation sweeteners that reduce sugar while meeting clean-label and compliance expectations. FSSAI's continued processing of non-specified food and ingredient applications (status published as of 3 June 2026) provides a clearer pathway for companies looking to commercialize newer sweeteners and specialty solutions. At the same time, the broader push to align product standards with the Labelling and Display Regulations, 2020 increases the premium on transparent claims and standardized additive references for national launches.

On the supply side, investment and process upgrades across the sugar and ingredients ecosystem are expanding adjacent capabilities that can support sweetener supply chains, co-products, and industrial flexibility. For instance, Shri Dutt India Private Limited commissioned a rapid expansion of its Kandla, Gujarat sugar refinery capacity from 1,000 TPD to 2,500 TPD (reported in January 2026), showing how debottlenecking can raise throughput within existing footprints. Indian sugar groups are also allocating capital toward higher-value diversification, including Balrampur Chini Mills announcements in April 2026 covering an 80,000-tonnes-per-year lactogypsum processing plant at Kumbhi, Uttar Pradesh and progress on a PLA biopolymer facility. These moves point to broader shifts toward integrated, value-added platforms that can improve ingredient-grade quality practices and logistics for food sweetener customers.

Recent Industry Developments

- May 2026: Ingredion Incorporated announced a strategic partnership with Sanstar Limited, including a minority equity stake and a joint venture to manufacture specialty pharmaceutical and food ingredient products in India. The move strengthens Ingredion's local manufacturing access for higher-value ingredients used in reformulation, including reduced-sugar applications, while shortening supply chains and compliance lead times for Indian customers.

- May 2026: Cargill Incorporated completed the divestiture of its corn wet milling facility in Davangere, Karnataka to Riddhi Siddhi Gluco Biols Limited. The transaction changes domestic capacity ownership for starch-based derivatives and sweetener intermediates, while indicating portfolio prioritization toward higher-margin ingredient solutions and partnerships in India.

- April 2024: Ingredion Incorporated introduced the PURECIRCLE Clean Taste Solubility Solution (CTSS), a plant-derived, clean-label stevia solution positioned for improved solubility and taste performance. The launch supports beverage and dairy formulators working on sugar reduction with fewer sensory trade-offs, reinforcing competitive intensity in stevia-based high-intensity sweeteners.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the India food sweetener market is defined as the value of sweetening ingredients sold for use in food and beverage manufacturing within India, covering both caloric sweeteners and high-intensity alternatives used to deliver sweetness in finished products.

Scope exclusions: This sizing excludes tabletop sweeteners sold mainly for at-home use, and it excludes non-food sweetening uses, such as pharmaceutical excipients, when they are not used in food formulations.

Segmentation Overview

-

Product Type

- Sucrose

-

Starch Sweeteners and Sugar Alcohols

- Dextrose

- High-Fructose Corn Syrup (HFCS)

- Maltodextrin

- Sorbitol

- Xylitol

- Other Starch Sweeteners and Sugar Alcohols

-

High-Intensity Sweeteners (HIS)

- Sucralose

- Aspartame

- Saccharin

- Cyclamate

- Ace-K

- Neotame

- Stevia

- Other High-Intensity Sweeteners

-

Source

- Plant-Based

- Artificial

- Fermentation-Drived

-

Application

- Bakery and Confectionery

- Dairy and Desserts

- Sauces Dressings and Spreads

- Beverages

- Other Applications

-

Geography

- North India

- West India

- East India

- South India

Data Sources, Market Sizing, and Validation

Desk Research

We start by mapping the demand pool using public, India-specific indicators that tend to remain stable year to year, and then we add product and pricing context from industry documentation. Typical inputs include official references like the Ministry of Agriculture and Farmers Welfare updates, the Department of Food and Public Distribution releases on sugar, APEDA trade data, and customs trade statistics, alongside FSSAI regulations and standards that influence which sweeteners are permitted in food.

To make the model workable, company annual reports, investor presentations, and reputable press sources are used to capture capacity changes, product mix, and how pricing is described for industrial customers. For cross-checking financial signals and product activity over time, we also use a paid subscription focused on company financials and intelligence, plus a separate paid subscription focused on news and financials, which helps when public disclosures are limited. The desk sources listed here are illustrative only, and additional documents were referenced during data collection, validation, and clarification.

Primary Interviews and Surveys

Next, we validate the desk-based assumptions through expert interviews and structured surveys with sweetener manufacturers, ingredient distributors, and food and beverage formulators, then we reconcile any mismatches before finalizing the model. Coverage is balanced across India so usage patterns across beverages, bakery, dairy, and confectionery are not inferred from a single region, and pricing discussions are tested across different buying volumes and contract cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | |

| Mid tier: 58% | Functional/Unit leaders: 29% | |

| Smaller Players: 15% | Managers: 59% |

Market-Sizing & Forecasting

Our sizing uses top-down demand reconstruction, where India-level consumption signals, sugar production and trade flows, and category-level food output are used to build a realistic sweetener demand pool, which is then converted into value using price bands aligned to industrial buying. After forming that view, we corroborate it using selective bottom-up approximations, including sampled price per kilogram ranges by sweetener type, distributor channel checks, and supplier revenue sanity checks. We then adjust when the same direction of mismatch appears across categories.

In practice, the model tracks a few recurring drivers that explain most year-to-year movement, including sugar production and diversion patterns, food and beverage output growth, reformulation intensity toward low-calorie options, import reliance for specific high-intensity sweeteners, and typical industrial pricing progression by sweetener class. Forecasting is completed using scenario analysis, since regulation, input cost swings, and substitution between sucrose and alternatives can shift the trajectory quickly. Scenario weights are aligned to expert expectations collected during interviews. Where visibility is limited, we use conservative penetration assumptions tied to application mix, and then we re-check implied consumption against known production and trade signals.

Data Validation & Update Cycle

Before sign-off, results are triangulated across multiple checks so that no single indicator determines the final value. Analysts compare market output against independent signals such as production trends, import intensity for specific sweeteners, and food category growth rates, then review variance flags in a second pass to confirm whether unusual jumps are explainable or need correction.

If major events occur, such as material policy changes, sudden price spikes, or large capacity announcements, the team re-contacts selected experts to confirm what changed and how quickly it is likely to flow into demand. Reports are refreshed annually, and prior to delivery an analyst performs a final review so clients get an updated view reflecting the latest available public data and validated assumptions.

Mordor Intelligence's India Food Sweetener Market Market Estimate Compared With Other Published Estimates

Published market values for India food sweeteners can differ because each study draws its boundary in a slightly different place and then uses a different set of demand signals to build the total. Variation also comes from the chosen base year, how prices are averaged (spot versus contract), and whether the model is built strictly around industrial usage or across a broader sweeteners basket.

Production and trade signals, together with application-level consumption checks from food and beverage output, are used as evidence to keep Mordor Intelligence's estimate tied to sweeteners used in food formulations within India. When other estimates include wider sweetener uses or assume a faster switch into high-intensity sweeteners without re-checking implied volumes, their totals can move away from what the demand pool can reasonably support.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.34 B (2025) | |

| Industry Research Publisher A | USD 3.30 B (2025) | Uses a broader framing of food sweeteners and a longer forecast window, and it can apply different pricing progression assumptions by sweetener class, which slightly shifts the base-year value. |

| Market Insights Portal B | USD 3.03 B (2025) | Often groups sweeteners at a high level (natural, artificial, sugar alcohols) without detailing industrial application mapping, which can undercount categories where sucrose and starch-derived sweeteners dominate value. |

Taken together, the spread is mainly explained by how narrowly the market is defined and how price and substitution are treated in the base year. By keeping the demand pool tied to observable food use signals and cross-checking value against production and trade realities, the final number remains traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current valuation of the India sweeteners market?

The market is valued at USD 3.49 billion in 2026 and is projected to reach USD 4.34 billion by 2031.

Which region dominates consumption?

North India leads with 40.85% revenue share due to its sugarcane base and dense food-processing network.

Which product category is growing fastest?

High-intensity sweeteners are expanding at a 5.33% CAGR as formulators adopt stevia and allulose.

Which application segment offers the highest growth outlook?

Bakery and confectionery products are forecast to grow at 5.44% CAGR through 2031 as brands launch healthier SKU lines.

Page last updated on: