Vietnam Food Additives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vietnam Food Additives Market Analysis by Mordor Intelligence

Vietnam food additives market size reached USD 1.15 billion in 2026 and is forecast to attain USD 1.38 billion by 2031, advancing at a 4.92% CAGR during 2026-2031. Growth looks moderate on the surface, yet the country’s 7.4% expansion in food processing revenue in 2024, coupled with urbanization, clean-label reformulation, and steady foreign investment, signals deeper structural momentum behind demand for preservatives, emulsifiers, and flavor systems. Multinational ingredient houses are scaling local presence to serve a beverage category exceeding 4.6 billion litres and a bakery segment worth more than USD 4 billion, both of which are preparing for the 10% sugar-sweetened-beverage (SSB) tax slated for 2026. Manufacturers are tightening formulations to meet front-of-pack labeling rules, while domestic processors confront cold-chain gaps that still require functional synthetics to safeguard shelf life in Vietnam’s tropical climate. The resulting push-and-pull between cost control, regulatory pressure, and premiumization keeps overall additive volumes rising even as per-kilogram dosages trend lower.

Key Report Takeaways

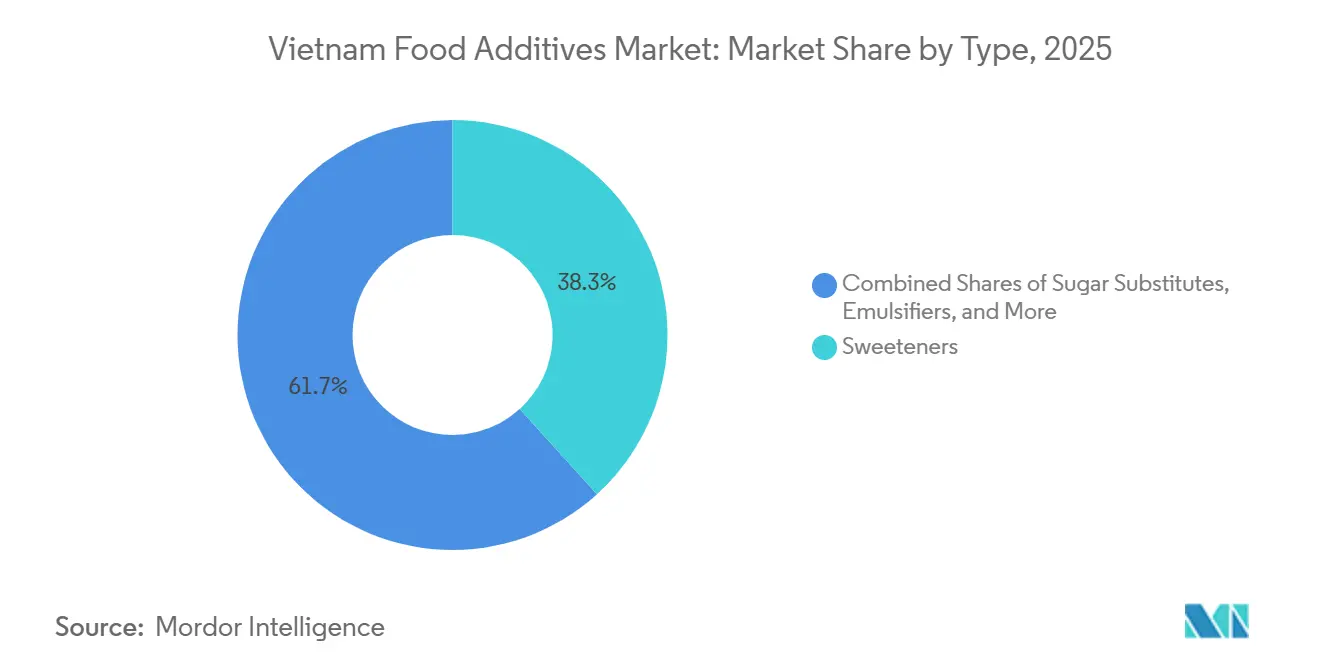

- By product type, sweeteners led with 38.28% revenue share in 2025; sugar substitutes are forecast to expand at a 6.12% CAGR to 2031.

- By source, synthetic additives accounted for 52.15% of the Vietnam food additives market share in 2025, whereas natural variants will register the highest projected CAGR at 5.52% during 2026-2031.

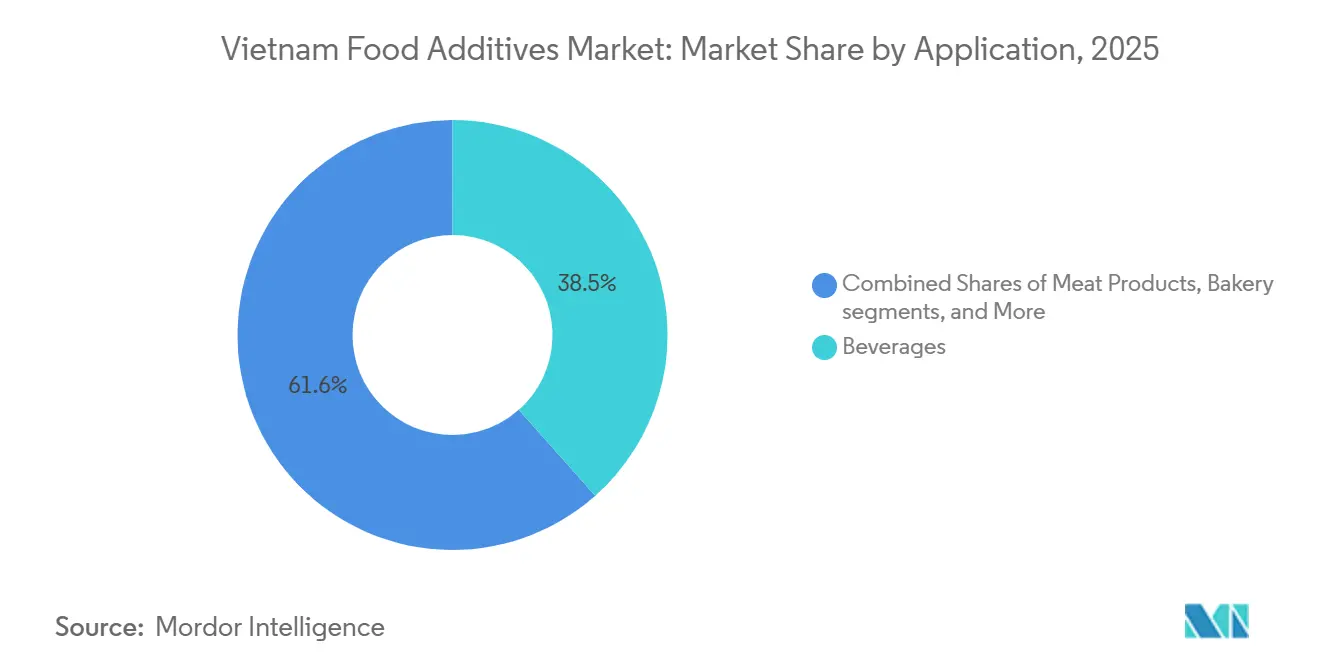

- By application, beverages captured 38.45% of the Vietnam food additives market size in 2025 and meat & meat products will be the fastest-growing use case at a 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Food Additives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for processed and convenience foods | +1.2% | Ho Chi Minh City, Hanoi, Binh Duong industrial belt | Medium term (2-4 years) |

| Evolving dietary preferences toward ready-to-eat formats | +0.9% | Urban centers nationwide | Short term (≤ 2 years) |

| Rising bakery, beverage, and dairy output requiring emulsifiers, colors, flavors | +1.1% | Beverage growth strongest in south, dairy in north | Medium term (2-4 years) |

| Government incentives for food-processing FDI | +0.8% | Key zones in Bac Ninh, Hai Phong, Dong Nai | Long term (≥ 4 years) |

| Investments in food-tech and R&D for functional, natural additives | +0.5% | R&D clusters in Hanoi and Ho Chi Minh City | Long term (≥ 4 years) |

| Technological advances in additive processing | +0.4% | Led by multinational subsidiaries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Processed and Convenience Foods

In 2024, Vietnam's food processing sector generated over VND 720 trillion (approximately USD 30 billion), reflecting a year-on-year growth of 10.92%. However, 85% of the country's agricultural exports remain raw or minimally processed, highlighting the early stage of domestic value addition, according to the Vietnam Ministry of Industry and Trade. Urbanization is a key driver in this scenario. The urban population is expected to increase from 37% in 2024 to 44% by 2030, reducing meal-preparation times and boosting demand for frozen meals, instant noodles, and shelf-stable sauces that rely on preservatives such as sorbates and benzoates, as noted by the Asian Development Bank[1]Source: Asian Development Bank. "Vietnam Urbanization and Economic Development Report." adb.org.. Additionally, packaged snacks and sweets are gaining traction as working-age consumers adopt Western snacking habits. Bakery products are projected to grow at a 7.5% CAGR through 2029, while confectionery products are expected to grow at a 7% CAGR through 2028. A less apparent issue is the cold-chain gap. Approximately 70% of food-processing enterprises still use outdated equipment, leading manufacturers to depend heavily on chemical preservatives to offset inadequate refrigeration during distribution. This reliance paradoxically sustains demand for synthetic additives, even as consumers increasingly prefer clean-label products, as noted by the Vietnam Food Association. The ASEAN Food & Beverage Alliance reports that 96% of regional food and beverage businesses have either undertaken or plan to undertake product reformulation. However, 80% of Asian consumers are willing to accept reformulated products only if the taste remains unchanged. This consumer demand is driving ingredient suppliers to create masking agents and flavor enhancers to address the sensory challenges posed by reduced sugar or sodium.

Evolving Consumer Dietary Preferences and Lifestyles Boost Usage in Ready-to-Eat Products

In 2024, 78% of Vietnamese shoppers intend to prioritize purchasing healthier products. Despite this shift in consumer preferences, per-capita consumption of processed meat remains low at just 0.4 kilograms, highlighting the continued prevalence of wet markets, particularly in areas outside major urban centers. Among urban millennials, there is a growing preference for portion-controlled, protein-rich chilled meals. This change in dietary habits has driven an increased use of emulsifiers and stabilizers to preserve the texture of these products. The "healthy indulgence" trend is also gaining traction, as seen in the rising demand for sugar-free energy drinks and fortified ready-to-drink teas. These beverages rely heavily on acidulants and high-intensity sweeteners to deliver appealing flavors while ensuring sugar levels remain below the SSB-tax threshold. Early formulation data reveal a significant upward trend, with the use of acesulfame-K and sucralose across Southeast Asia increasing by approximately 25% annually, reflecting the region's growing focus on healthier product formulations.

Rising Demand for Bakery, Beverages, and Dairy Products Requiring Emulsifiers, Colors, and Flavors

Despite the growth, per-capita bread consumption remains at 10.1 kilograms, which is below regional standards. This gap highlights significant opportunities for the adoption of enzymes that can extend shelf life and improve bread softness. In the beverage industry, new regulations introduced by the Ministry of Health in 2023 are driving the phase-out of certain azo dyes. This regulatory shift creates a competitive advantage for suppliers whose inventories have already been approved by JECFA. Additionally, the persistent dairy deficit, with annual imports exceeding USD 1.2 billion, continues to drive demand for stabilizers such as carrageenan and pectin, particularly in fortified liquid milk products. At the same time, functional dairy product lines are increasingly incorporating cultures and vitamin premixes to meet protein and probiotic content requirements, catering to evolving consumer preferences.

Government Initiatives Supporting Food Processing Industry Growth

In 2024, Vietnam's processing and manufacturing sectors secured foreign direct investment (FDI) worth USD 25.58 billion, representing 66.9 percent of the country's total FDI. Major contributors to this investment included Singapore, South Korea, China, Hong Kong, and Japan, according to the Vietnam Ministry of Planning and Investment. To support these sectors, the Vietnamese government has introduced attractive incentives, including tax holidays of up to four years and land-lease discounts in specific food-processing zones. Prominent zones such as Bac Ninh, Hai Phong, Dong Nai, and Binh Duong have drawn significant investments, including Cargill's cumulative USD 200 million across four feed and ingredient facilities, which collectively employ over 1,000 individuals. Cargill Incorporated has established a strong presence in these zones. Additionally, Decree 15/2018/ND-CP, issued by the Vietnam Ministry of Health, aimed to simplify the approval process for food additives. While the decree reduced the approval time for single-ingredient permitted additives from six months to 30 days, it retained strict requirements for mixed additives and novel uses, necessitating full registration. This has created a two-tier system that benefits established multinationals while posing challenges for local innovators. On the trade front, the EU-Vietnam Free Trade Agreement (EVFTA), effective since 2020, eliminated tariffs on 99 percent of goods over a ten-year period. However, Vietnamese exporters have faced challenges in meeting stringent EU food-safety standards. Compliance requirements, particularly regarding traceability and maximum residue limits, have driven exporters to upgrade their processing lines. Many have adopted internationally recognized certifications such as HACCP and ISO 22000. These efforts not only ensured compliance but also increased demand for functional additives, which are essential for compensating for shorter thermal processing times, as noted by the European Commission[2]Source: European Commission. "EU-Vietnam Free Trade Agreement Implementation." ec.europa.eu..

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory frameworks limit new additive introductions | -0.6% | National, with stricter enforcement in export-oriented facilities | Medium term (2-4 years) |

| Fluctuating raw material prices and transportation costs | -0.5% | National, palm oil and dairy powder imports most volatile | Short term (≤ 2 years) |

| Increasing consumer skepticism about artificial and synthetic additives | -0.4% | Urban centers (Ho Chi Minh City, Hanoi, Da Nang) | Medium term (2-4 years) |

| Supply chain disruptions impacting ingredient availability and pricing | -0.3% | National, port congestion in Hai Phong and Ho Chi Minh City | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Frameworks Limit New Additive Introductions

Vietnam's alignment with CODEX GSFA, as outlined in Circular 17/2023, has introduced significant regulatory challenges for suppliers. Compounds that are not included in the JECFA or FEMA lists now require the submission of a detailed toxicological dossier, with associated costs ranging from USD 50,000 to 100,000. This requirement creates a substantial financial barrier, particularly for smaller suppliers. Moreover, mixed formulations or products falling under novel food categories are subject to audits, which can take up to 12 months to complete, further delaying the time-to-market for these products. Looking ahead, Circular 29/2023, effective from January 2026, will mandate the use of color-coded nutrition labels. These labels will prominently display sugar and sodium content, increasing transparency for consumers and placing additional pressure on manufacturers to reformulate their products to meet healthier standards. Adding to the complexity, the upcoming 10% tax on sugar-sweetened beverages (SSBs) will require manufacturers to navigate stringent compliance measures. Sweetener blends must not only pass safety evaluations but also ensure that total sugar content remains below 5 grams per 100 milliliters, further intensifying the reformulation and compliance challenges faced by the industry.

Fluctuating Raw-Material Prices and Transportation Costs

During 2023-2024, palm-oil prices experienced significant volatility, ranging from USD 800 to USD 1,100 per tonne. This fluctuation was primarily caused by Indonesian export restrictions and the adverse effects of El Niño on crop yields. These price changes have notably increased the production costs of mono- and diglyceride emulsifiers. In 2024, dairy-powder spot rates stabilized at approximately USD 3,200 per tonne. However, even a 10% shift in these prices could add an estimated USD 150 million to Vietnam’s overall ingredient expenditure. Freight rates have remained elevated, standing 30-40% higher than 2019 levels due to persistent container shortages. Additionally, port congestion at key locations such as Hai Phong and Cat Lai has significantly extended lead times for temperature-sensitive inputs, including ascorbic acid, to 8-10 weeks. Processors, already grappling with limited cold storage capacity, continue to rely on chemical preservatives as a risk mitigation strategy. This reliance has, in turn, slowed the adoption of more expensive natural alternatives in the short term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sweeteners Dominate as Tax Threat Accelerates Substitution

Sweeteners commanded 38.28% of the Vietnam food additives market in 2025 on the back of 4.658 billion litres of soft-drink output. The Vietnam food additives market size for sugar substitutes is projected to outpace all other product groups at a 6.12% CAGR to 2031 as producers pre-empt the 10% SSB tax by reformulating below the 5 g/100 ml threshold. Within synthetic sweeteners, acesulfame-K and sucralose are favored for heat stability at ambient distribution temperatures, while natural stevia adoption lags because flavor masking remains costly.

Beyond sweeteners, preservatives retain relevance for sauces and processed meats even as “no artificial preservatives” claims proliferate. Emulsifiers such as lecithin and mono-glycerides protect texture in premium breads and dairy drinks, while enzymes offer a clean-label workaround by replacing chemical oxidizers in dough conditioning. Hydrocolloids—carrageenan, xanthan, pectin—arm beverage and dairy formulators against protein precipitation, though Vietnam still imports most volumes. Global flavor and color specialists supply high-intensity concentrates through Thai or Malaysian hubs, yet emerging local companies are chipping away in value segments like instant noodles.

By Source: Synthetic Leads but Natural Gains as Premium Gap Narrows

Synthetic inputs delivered 52.15% revenue in 2025 thanks to 30-50% unit-cost advantages and robust performance under Vietnam’s high-temperature supply chain. Natural counterparts, however, will grow faster at 5.52% CAGR to 2031, reflecting rising urban incomes and regulatory nudges such as colorant phase-outs. The Vietnam food additives market share for synthetic variants is likely to erode slowly as blended “nature-identical” solutions bridge price and performance.

Consumer surveys show 74% express high concern over ultra-processed foods, yet 47% still rank price as the primary purchase driver, keeping synthetic and hybrid systems entrenched in mass-market offerings. Natural sweeteners and preservatives face raw-material volatility and longer lead times, but upcoming domestic seaweed refining and synthetic-biology stevia sourcing could shorten supply lines and shrink cost premiums, accelerating the shift.

By Application: Beverages Retain Lead While Meat Processing Captures Growth

Beverages absorbed 38.45% of additive spending in 2025 and remain the largest outlet as the sector expands toward 7.45 billion litres by 2033. Carbonated drinks are flattening, yet ready-to-drink tea and sugar-free energy drinks are rising, each leveraging flavor enhancers and high-intensity sweeteners to maintain mouthfeel while complying with impending taxes. Acidulant and stabilizer demand is also growing in functional bottled water and collagen tea lines.

Meat and meat products represent the fastest lane, advancing at 7.05% CAGR through 2031 on the back of foreign entrants such as JBS and local champions scaling chilled, portion-controlled proteins. Although labels trumpet “no additives,” processors still depend on nitrites and phosphates to secure safety and color in cured lines. Bakery, dairy, and sauce segments continue to post mid-single-digit gains, collectively balancing the portfolio of the Vietnam food additives market.

Geography Analysis

In Vietnam's southern industrial corridor, which spans from Ho Chi Minh City through Binh Duong and Dong Nai, Cargill operates a 200,000-tonne-per-year animal-feed facility in Dong Nai, while Ajinomoto manages its MSG and seasonings factory in Bien Hoa. Meanwhile, the northern manufacturing belt, covering Hanoi, Bac Ninh, and Hai Phong, houses Cargill's 10,000-tonne-per-year feed-ingredients plant and a larger 200,000-tonne-per-year facility in Bac Ninh. This northern region benefits significantly from its proximity to China's raw-material supply chains and the Hai Phong deep-water port, which handles 70 percent of northern Vietnam's containerized imports, as reported by the Vietnam Ministry of Transport. In 2024, foreign direct investment in processing and manufacturing reached USD 25.58 billion, representing 66.9 percent of total FDI.

The Mekong Delta, recognized as Vietnam's agricultural heartland, provides essential raw materials such as cassava for starch-based sweeteners and sugarcane for sugar production. However, the region lacks large-scale additive-manufacturing facilities, forcing processors to rely on emulsifiers and preservatives sourced from Ho Chi Minh City or international suppliers, as noted by the Vietnam Sugar and Sugarcane Association. Central Vietnam, anchored by Da Nang, is emerging as a secondary hub for food processing due to its lower labor costs and the incentives offered by the Chu Lai Open Economic Zone. Urbanization in Vietnam is accelerating, rising from 37 percent in 2024 to a projected 44 percent by 2030, which is attracting food-processing investments to urban areas.

Vietnam imports approximately USD 9.8 billion worth of food products annually, reflecting a 15 percent year-on-year growth in 2023. Dairy, meat, and various ingredients account for a significant portion of these imports. On the other hand, food exports reached USD 53.2 billion, marking a 21.3 percent increase, with coffee, rice, seafood, and processed fruits leading the export categories, as reported by the Vietnam General Statistics Office. Additionally, freight costs remain 30 to 40 percent higher than 2019 levels, compressing margins for importers and making local production a more viable option where feasible. The Ministry of Health's Circular 17/2023, effective November 2023, aligns Vietnam's permitted-additive list with CODEX Alimentarius. This alignment simplifies the approval process for multinational companies but increases compliance costs for smaller local firms. Furthermore, Circular 29/2023 mandates front-of-pack nutritional labeling starting January 2026, which will make sugar and sodium content more visible to consumers and accelerate reformulation cycles among manufacturers[3]Source: Vietnam Ministry of Health, “Circular 29/2023 on Nutritional Labeling,” moh.gov.vn.

Competitive Landscape

The Vietnamese food additives market remains fragmented. Global suppliers, including Cargill, Ajinomoto, DSM-Firmenich, Kerry, Givaudan, ADM, and Tate and Lyle, operate through representative offices or regional production hubs and leverage pre-approved CODEX-aligned portfolios to fast-track registrations. Vietnamese firms such as TTC AgriS, Quang Ngai Sugar, and LASUCO dominate sugar-derived sweeteners but have limited reach in high-margin specialty ingredients.

Strategies subdivide into cost leadership for commodity MSG and benzoates, differentiation via natural enzyme or taste-masking systems, and vertical integration that hedges raw-material swings. Cargill’s four-facility footprint covering feed, lecithin, and starches is emblematic. Emerging players like Viet Huong Flavor and Fragrance JSC carve out a share in instant-noodle and confectionery flavoring by offering localized profiles at 15-20% lower prices than multinationals.

Regulatory dynamics amplify competitive gaps. Circular 17/2023’s dossier requirements lock out undercapitalized entrants, while the SSB tax propels demand for turnkey sweetener-replacement platforms that only a handful of suppliers can deliver quickly. Technology investments, from encapsulation for heat-sensitive flavors to synthetic-biology stevia, are set to reshape cost curves and may trigger consolidation once early movers demonstrate scalable economics.

Vietnam Food Additives Industry Leaders

-

TTC AgriS

-

The KCP Limited

-

LASUCO

-

Quang Ngai Sugar Joint Stock Company

-

Viet Huong Flavor and Fragrance JSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Meyer Vietnam Co., Ltd. launched the Master 4.0 intelligent color sorting machine, developed by Meyer Optoelectronic, to the international market. This cutting-edge sorting solution is designed to enhance the capabilities of global food processing enterprises.

- July 2024: Quang Ngai Sugar Joint Stock Company approved an investment exceeding VND 2 trillion to strengthen its An Khe sugar processing and biomass power plants. Specifically, VND 1.169 trillion is allocated to boost the processing capacity of the An Khe plant in Gia Lai to 25,000 tons daily. This expansion is intended to bolster the sugarcane supply, support deep processing initiatives, and maintain the company's leadership in Vietnam’s sugar sector.

- June 2024: Morinaga Nutritional Foods Vietnam JSC, a subsidiary of Japan's Morinaga Milk Industry Co., Ltd, launched its newest product: the Morinaga Zero Fat Drink Yogurt. This yogurt variant is enhanced with several additives, including food gelatin, stabilizers (1422, 471), and preservatives (202).

Vietnam Food Additives Market Report Scope

Food additives are substances added to food during its processing/manufacturing to maintain or improve its safety, freshness, taste, texture, shelf life, or appearance.

The Vietnam food additives market is segmented by product type into preservatives, sweeteners, sugar substitutes, emulsifiers, anti-caking agents, enzymes, hydrocolloids, food flavors and enhancers, food colorants, and acidulants. By source, the market is segmented into natural and synthetic. By application, the market is segmented into bakery and confectionery, dairy and desserts, beverages, meat and meat products, soups, sauces, and dressings, and other applications. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Preservatives |

| Sweeteners |

| Sugar Substitutes |

| Emulsifiers |

| Anti-Caking Agents |

| Enzymes |

| Hydrocolloids |

| Food Flavors and Enhancers |

| Food Colorants |

| Acidulants |

| Natural |

| Synthetic |

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Soups, Sauces, and Dressings |

| Other Applications |

| By Product Type | Preservatives |

| Sweeteners | |

| Sugar Substitutes | |

| Emulsifiers | |

| Anti-Caking Agents | |

| Enzymes | |

| Hydrocolloids | |

| Food Flavors and Enhancers | |

| Food Colorants | |

| Acidulants | |

| By Source | Natural |

| Synthetic | |

| By Application | Bakery and Confectionery |

| Dairy and Desserts | |

| Beverages | |

| Meat and Meat Products | |

| Soups, Sauces, and Dressings | |

| Other Applications |

Key Questions Answered in the Report

How fast is the Vietnam food additives market expected to grow through 2031?

It is projected to register a 4.92% CAGR, reaching USD 1.38 billion by 2031.

Which product group holds the largest revenue share?

Sweeteners led with 38.28% share in 2025, driven by beverage and bakery applications.

What segment will grow quickest over the next five years?

Meat and meat products additives are forecast to rise at a 7.05% CAGR, outpacing all other applications.

Are natural additives likely to overtake synthetics in Vietnam?

Natural variants will grow faster at 5.52% CAGR, yet synthetics will keep the majority share until unit-cost gaps narrow further.

Page last updated on: