Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

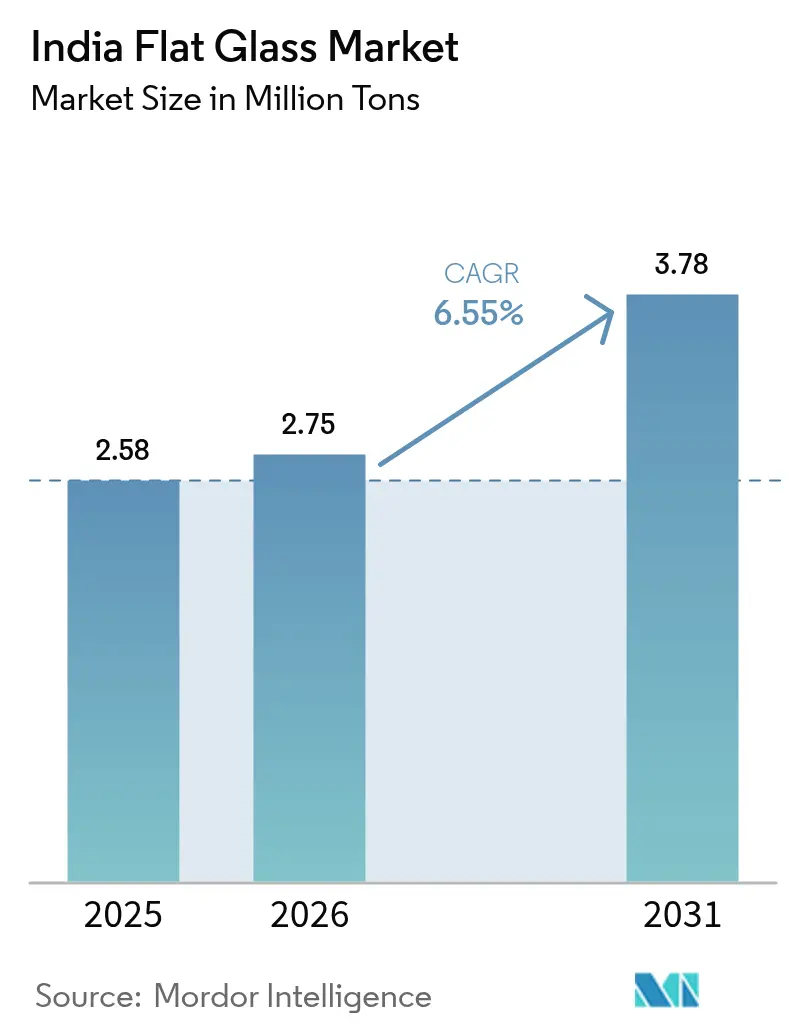

| Base Year Market Size (2025) | 2.58 Million tons |

| Market Volume (2026) | 2.75 Million tons |

| Market Volume (2031) | 3.78 Million tons |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

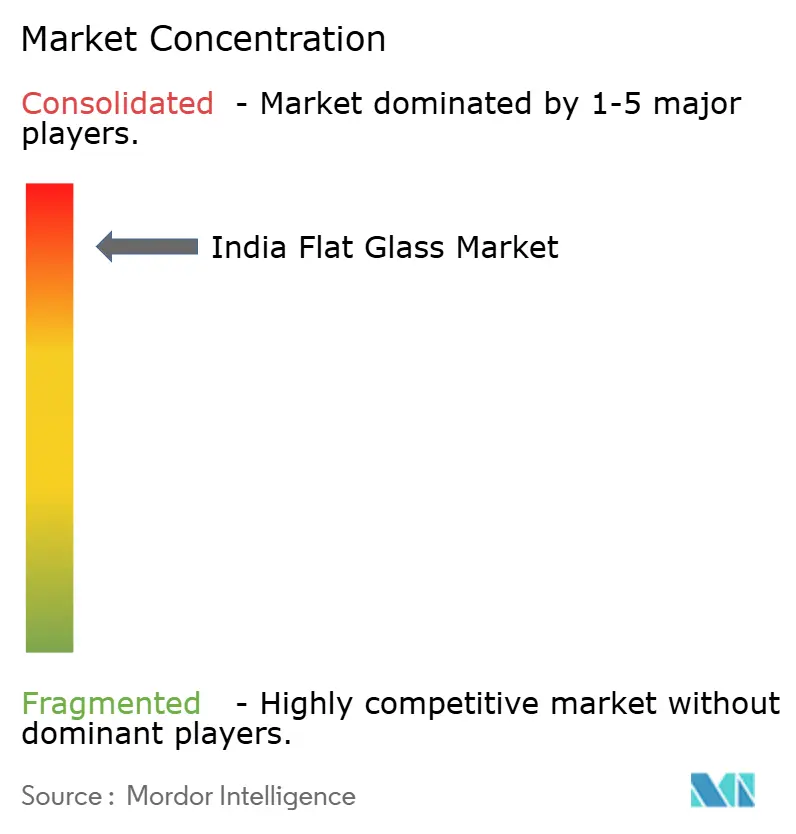

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Flat Glass Market Analysis by Mordor Intelligence

The India Flat Glass Market size is expected to grow from 2.58 million tons in 2025 to 2.75 million tons in 2026 and is forecast to reach 3.78 million tons by 2031 at 6.55% CAGR over 2026-2031. Urbanization, large-scale infrastructure projects, and government incentives aimed at renewable energy deployment collectively underpin this volume-driven expansion of the India flat glass market. Developers of commercial real estate in tier-1 and tier-2 cities increasingly specify energy-efficient facade systems to comply with evolving building codes, while global automotive OEMs continue to scale up output from India-based plants, keeping glazing demand on an upward trajectory. Domestic manufacturers are adding new float lines and processed-glass capacities to correct a supply-demand gap that left the India flat glass market reliant on USD 236 million of net imports in 2022. At the same time, high natural-gas costs and volatility in soda-ash supply keep pressure on margins, forcing industry players to adopt fuel-mix optimization and forward-buying strategies. The interplay of rising demand and input-cost stress is accelerating the shift toward high-value processed glass, which commands stronger pricing power and has become the strategic focus for most large plants.

Key Report Takeaways

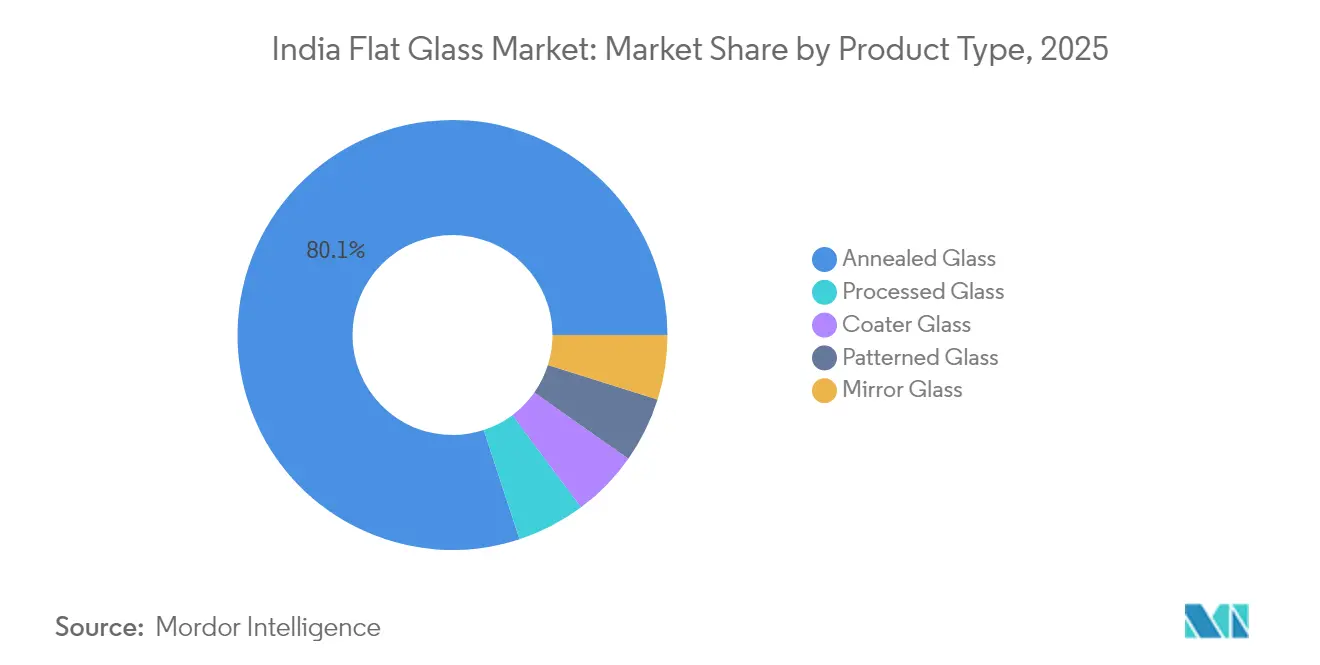

- By product type, annealed glass led with an 80.05% India flat glass market share in 2025, whereas processed glass is forecast to register the fastest 7.05% CAGR through 2031.

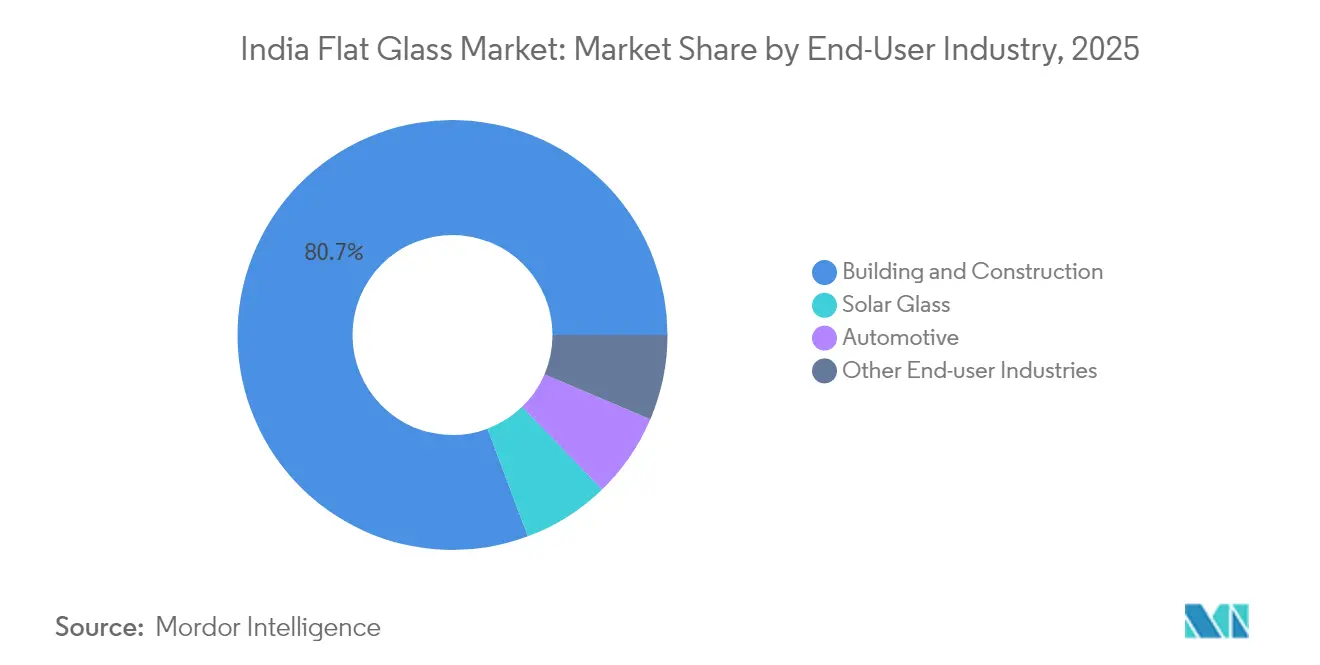

- By end-user industry, building and construction captured 80.70% of the India flat glass market size in 2025, while solar glass is advancing at an 8.55% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Flat Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban infrastructure boom and Smart Cities push | +1.80% | Mumbai, Chennai, Bengaluru, Hyderabad | Medium term (2-4 years) |

| Automotive glazing demand from rising vehicle production | +1.20% | Gujarat, Tamil Nadu, Maharashtra automotive corridors | Short term (≤ 2 years) |

| National solar-PV targets spurring solar glass capacity | +2.10% | Gujarat, Rajasthan, Tamil Nadu | Long term (≥ 4 years) |

| Data-centre construction driving high-performance facade glass | +0.90% | Mumbai, Chennai, Bengaluru, Hyderabad | Medium term (2-4 years) |

| PLI schemes for electronics propelling speciality display glass | +0.70% | Tamil Nadu, Karnataka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban Infrastructure Boom & Smart Cities Push

India’s Smart Cities Mission has approved 8,016 projects worth INR 1.64 trillion, which is translating into large procurement lots for low-emissivity, solar-control, and laminated facades that reduce HVAC load in public and private buildings. Policy mandates for green ratings have expanded specification depth, compelling architects to select glazing solutions with certified U-values and visible-light-transmittance benchmarks. Domestic contractors now tender facade packages earlier in project cycles, giving glass processors longer visibility of order pipelines and supporting capacity planning. As smaller municipalities replicate smart-city guidelines to draw investment, demand for certified glass spreads beyond major metros. International consortium partners from Europe and Japan transfer cutting-edge facade engineering know-how, nudging local processors toward triple-silver coatings and warm-edge spacer technologies that once were confined to premium offices. This diffusion of best practice heightens competitive pressure on legacy float-line operators to upgrade to magnetron sputtering or outsource coating to specialist toll coaters.

National Solar-PV Targets Spurring Solar Glass Capacity

India targets 500 GW of non-fossil power by 2030, of which solar constitutes the largest share, generating durable offtake for anti-reflective patterned glass used in photovoltaic modules. Anti-dumping duties on Chinese imports shield domestic players during scale-up, allowing them to pass through soda-ash cost spikes. Technological upgrades such as dual-textured rolling and online pyrolytic coating boost light transmission above 93%, enabling module efficiencies that rival imported glass. Manufacturers also integrate tin-bath waste-heat recovery to shave fuel costs and lower Scope 1 emissions. Export prospects brighten as Indian modules penetrate U.S. and European markets that require traceable, low-carbon glass inputs. Consequently, the India flat glass market gains a high-growth specialty branch that buffers against cyclicality in construction demand.

Data-Centre Construction Driving High-Performance Facade Glass

Hyperscale providers plan roughly 500 MW of new server capacity in Mumbai, Chennai, Bengaluru, and Hyderabad through 2029, each facility mandating facades that optimize daylight while holding stringent thermal transmittance and electromagnetic shielding thresholds[1]International Finance Corporation, “Strengthening Sustainability in the Glass Industry,” ifc.org . Curtain-wall contractors order double-silver low-E, low-iron units paired with argon-filled cavities to cut cooling loads that consume up to 60% of data-center energy. Blast-resistant laminated configurations are also specified to protect critical assets. Indian processors respond by installing jumbo-size tempering furnaces and autoclaves that accommodate 3.3 m × 6 m lites, aligning with global hyperscale specifications. Smart-glass solutions integrating electro-chromic coatings move from pilot to commercial scale in a few data centers, signaling an emerging demand pocket. As operators pursue net-zero certifications, facade glass suppliers leverage Environmental Product Declarations to differentiate bids, embedding sustainability metrics into competitive dialogues.

PLI Schemes for Electronics Propelling Specialty Display Glass

Government incentives worth INR 38,000 crore under the electronics PLI program spur investment in mobile, laptop, and display plants located primarily in Tamil Nadu and Karnataka manufacturing clusters. Thin-rolled alkali-aluminosilicate substrates are critical to these value chains, prompting flat-glass producers to install down-draw fusion and overflow fusion lines historically absent in India. Tight dimensional tolerances and surface-defect thresholds under 5 microns drive adoption of automated optical inspection and Class-100 cleanrooms. As integrated display fabs reach commercial throughput, local glass suppliers capture import substitution demand and mitigate currency exposure for downstream device makers. Over the long term, the specialization channel enriches the product mix of the India flat glass industry, raising average realization per ton and insulating revenue streams from construction cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of soda ash and natural gas | -1.40% | National, with higher impact on Gujarat, Maharashtra production centers | Short term (≤ 2 years) |

| Stringent emission norms elevating compliance costs | -0.80% | National, particularly affecting older manufacturing facilities | Medium term (2-4 years) |

| High inbound freight for heavy float glass across regions | -1.10% | National, with higher impact on inland states like Madhya Pradesh, Rajasthan, Uttar Pradesh distant from production hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Soda Ash & Natural Gas

India imported more than 10 million tons of soda ash in FY 2024 to supplement domestic output of 2.5 million tons, exposing glassmakers to global price swings linked to energy costs and shipping disruptions. A 62% jump in domestic natural-gas prices in 2021 raised furnace-fuel costs, eroding EBITDA margins, especially for legacy float lines with specific-energy consumption above 5 GJ per ton. Manufacturers respond by forward-contracting soda-ash deliveries and blending petcoke or furnace oil when policy allows, though each alternative requires burner and emission-control retrofits. Spot gas volatility also complicates new-capacity project budgeting, prompting some investors to delay final investment decisions. The corresponding working-capital strain increases borrowing needs at a time when interest rates are elevated, pressuring free cash flows and slowing greenfield expansions that would otherwise help resolve domestic supply deficits.

Stringent Emission Norms Elevating Compliance Costs

India’s progressive alignment with global best-available-technology guidelines for glass furnaces requires the installation of baghouse filters, continuous emission monitoring, and low-NOx burners[2]E3S Web of Conferences, “Potentials of Gas Emission Reduction (GHG) by the Glass Sheet Industry through Energy Conservation,” e3s-conferences.org . Plants built before 2010 often lack adequate space or structural provisions for such retrofits, making compliance capital-intensive. Regulatory deadlines spaced over 2025-2028 compel staggered shutdowns for upgrades, temporarily reducing effective capacity and tightening supply. Smaller regional players face the highest risk of shutdown due to limited access to low-cost finance, accelerating industry consolidation. Larger operators embed investments in electric-boosting and oxy-fuel technologies, which can reduce energy intensity by 20% but carry a multi-year payback. While the long-term outcome is cleaner production, near-term capex commitments compress return profiles and may slow the cadence of incremental capacity additions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Value-Added Glass Outpaces Basic Annealed

Annealed Glass retained an 80.05% India flat glass market share in 2025, anchored by its ubiquitous use in residential windows and cost-sensitive commercial builds. The segment’s scale benefits stem from established float-line infrastructure and minimal downstream processing. Yet Processed Glass is set to log a 7.05% CAGR through 2031, ensuring that its slice of the India flat glass market size widens meaningfully over the forecast horizon. Growth stems from the convergence of energy codes, architectural aesthetics, and vehicle-safety norms that require tempering, lamination, or functional coatings. The wider adoption of double-glazed units and solar-control coatings in premium offices drives coated-glass offtake, while mirrored and patterned variants cater to interior applications and decorative facades.

The shift carries strategic implications for margin profiles. Processed-glass realization often doubles the ex-factory price of annealed equivalents, enabling faster return on incremental capex for downstream lines. Several domestic producers now route as much as 45% of float output to their own tempering or lamination facilities, capturing integrated value. The India flat glass industry also observes increased licensing of sputter-coating technology from European firms, unlocking local production of low-E coatings once fully imported. Annealed-glass volumes are expected to persist in mass housing, yet their share gradually declines as code-compliant fenestration becomes mainstream in both new construction and retrofit markets.

By End-User Industry: Solar Glass Emerges as Fastest-Growing Segment

Building and Construction accounted for 80.70% the India flat glass market size in 2025, supported by government spending on metro rail, airports, and commercial towers. Steady urban migration drives residential demand, while corporate space absorption rebounds in major metros, reinforcing baseline growth. Automotive applications provide a stable second pillar, with vehicle production gains feeding demand for safety and solar-control glazing across sedans, SUVs, and trucks. Solar Glass stands out within the renewable space with an 8.55% CAGR through 2031, outpacing all other end-user segments. Protectionist tariffs on imported modules and PLI incentives spur integrated manufacturing, channeling predictable orders to domestic solar-glass makers.

Other industrial users embrace specialty glass in electronics enclosures, appliance doors, and greenhouse agriculture, but their combined volumes remain relatively small. Even so, these niches offer superior margins due to tight tolerance requirements and chemical strengthening processes. As India’s electronics ecosystem matures under Make-in-India, demand for display and cover glass supplies additional impetus to the processed-glass category, reinforcing the broader product-mix upgrade observed within the India flat glass market.

Geography Analysis

The India flat glass market exhibits a pronounced west-to-south corridor in manufacturing capacity, anchored by Gujarat, Maharashtra, and Tamil Nadu. Gujarat hosts multiple float lines leveraging local silica-sand deposits and petrochemical feedstock clusters, supplying construction and automotive customers across western and northern demand centers. Maharashtra complements with downstream processing facilities that cater to the neighboring automotive hubs of Pune and Aurangabad. Tamil Nadu supports integrated complexes near Chennai that feed OEM car plants, electronics parks, and the expanding solar-glass ecosystem.

Northern states like Rajasthan and Uttar Pradesh offer long-term capacity options as Smart-City projects and industrial corridors raise local consumption. The India flat glass market size for northern India remains underserved relative to demand, which has prompted feasibility studies for new float lines closer to Delhi-NCR gateways. Coastal locations with port access, such as Mundra and Ennore, retain strategic relevance, enabling the import of soda ash and the export of processed units to Middle-East and ASEAN customers.

Although India remained a net importer of float glass worth USD 236 million in 2022, several greenfield projects now under construction could shift the balance toward self-sufficiency by 2028. Logistics economics also favor regional clustering, given that finished glass is weighty and prone to breakage, translating into freight costs that can reach 8% of invoice value over distances exceeding 1,000 km. Consequently, manufacturers often locate dispatch warehouses adjacent to primary highways to shrink last-mile risk. Looking ahead, the geographic dispersion of Smart-City developments, covering 100 urban centers, ensures that demand growth will spill beyond traditional metros, fostering the rise of tier-2 consumption nodes that call for agile distribution networks.

Competitive Landscape

The India flat glass market is highly consolidated. Global majors Saint-Gobain, Guardian Industries Holdings, and Şişecam lead premium architectural and automotive niches through scale float lines, sputter-coating facilities, and robust R&D pipelines. Domestic leader Asahi India Glass (AIS) leverages entrenched OEM relationships to dominate passenger-vehicle glazing, while Borosil Renewables has carved out a stronghold in solar-glass manufacturing and is now pursuing international acquisitions to triple capacity. Gold Plus, Hindustan National Glass, and several mid-sized processors target region-specific construction markets with competitively priced annealed and tempered offerings.

Strategic moves emphasize vertical integration and energy efficiency. Borosil Renewables channels INR 950 crore into a Gujarat expansion that lifts solar-glass output by 600 TPD, reducing reliance on imports and supporting domestic module producers. Saint-Gobain inks a 25-year green-power purchase deal with Sembcorp to decarbonize its massive Sriperumbudur complex, trimming operating costs while meeting customer sustainability criteria. Gold Plus inaugurates a Karnataka float line with an eye on solar-glass diversification, capitalizing on proximity to southern photovoltaic clusters. Many operators adopt waste-heat-recovery boilers and electric-boosting elements to offset gas volatility, with capex partially financed through green bonds tied to emission-reduction milestones.

Innovation acts as another competitive lever. Guardian installs an online CVD coating unit to introduce tri-silver low-E products produced domestically, reducing lead times for high-performance facade projects. Şişecam pilots oxy-fuel combustion at one of its western India lines, cutting NOx emissions and securing regulatory goodwill. Smaller processors differentiate via quick-turn customization services for interior fit-out contractors. The industry also witnesses heightened collaboration with façade consultants and automotive designers early in project cycles, embedding proprietary glass solutions into specifications and creating lock-in effects that defend share against late-stage substitutes.

India Flat Glass Industry Leaders

Saint-Gobain

Asahi India Glass Limited.

Borosil Renewables

Gold Plus Group

Guardian Industries Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Gold Plus Group has announced the successful commissioning of its manufacturing facility in Karnataka. This development reinforces Gold Plus's market position while diversifying its product portfolio by entering the solar glass segment. The expansion is set to bolster the flat glass market, boosting supply capabilities and addressing the surging demand for solar glass.

- May 2025: Borosil Renewables Ltd has initiated a significant expansion project in Gujarat, with an INR 950-crore (~USD 111.08 million) investment to increase its solar glass production capacity by 600 tons per day (TPD). The company expects this enhanced capacity to become operational by the third quarter of the 2026-27 financial year.

India Flat Glass Market Report Scope

Flat glass, often referred to as sheet or plate glass, is frequently used to create solar panels, windows, mirrors, and doors. Sand, silica, limestone, and soda ash are melted to create the liquid, which is then cooled to create the product of the required thickness. The India flat glass market is segmented by product type and end-user industry. By product type, the market is segmented into annealed glass (including tinted glass), coater glass, reflective glass, processed glass, and mirrors. By end-user industries, the market is segmented into building and construction, automotive, solar glass, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

By Product Type

| Annealed Glass |

| Coater Glass |

| Processed Glass |

| Mirror Glass |

| Patterned Glass |

By End-user Industry

| Building and Construction |

| Automotive |

| Solar Glass |

| Other End-user Industries |

| By Product Type | Annealed Glass |

| Coater Glass | |

| Processed Glass | |

| Mirror Glass | |

| Patterned Glass | |

| By End-user Industry | Building and Construction |

| Automotive | |

| Solar Glass | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current volume of the India flat glass market?

The India flat glass market size was 2.75 million tons in 2026 and is on track to reach 3.78 million tons by 2031.

Which segment shows the fastest growth within flat glass demand in India?

Solar glass is projected to expand at an 8.55% CAGR through 2031, making it the fastest-growing end-user segment in the country.

How dependent is India on flat glass imports?

India recorded USD 236 million in net float-glass imports in 2022, though new domestic capacity under construction may close this gap by 2028.

What major factor is pressuring glass manufacturing costs?

Volatile prices for soda ash and natural gas accelerate input-cost swings, directly affecting furnace operations and end-product pricing.

Which states dominate flat glass production in India?

Gujarat, Maharashtra, and Tamil Nadu host the majority of float and processed-glass capacity because of resource access and proximity to key end-use industries.

Page last updated on: