Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

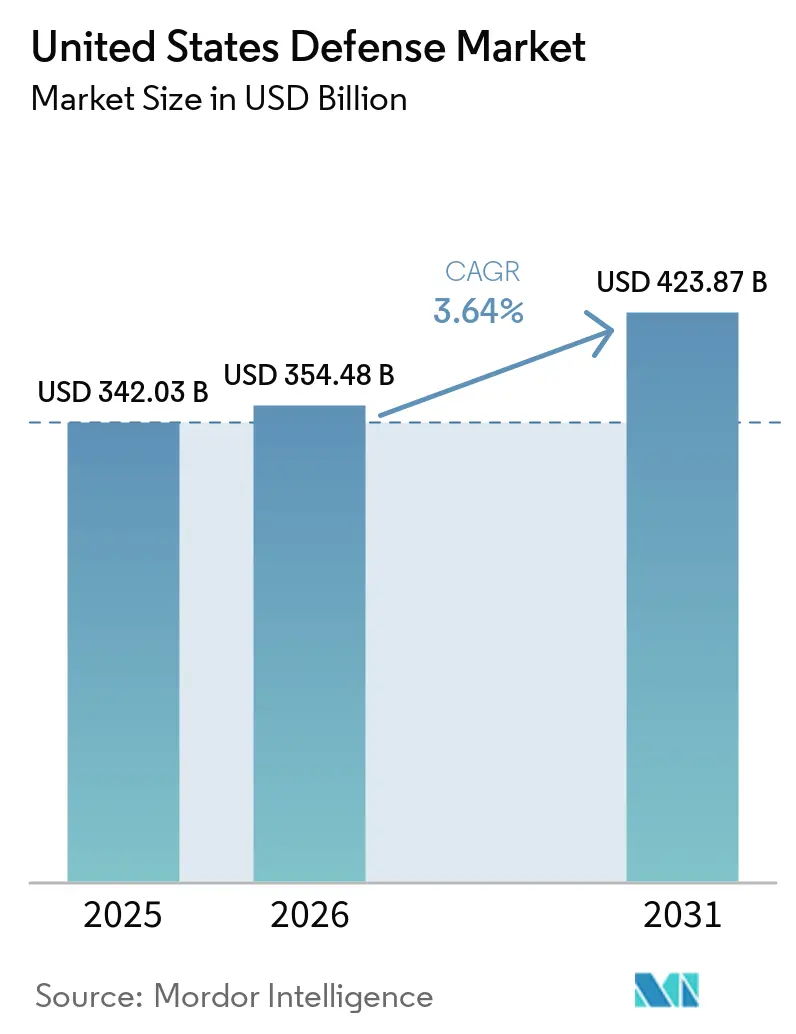

| Base Year Market Size (2025) | USD 342.03 Billion |

| Market Size (2026) | USD 354.48 Billion |

| Market Size (2031) | USD 423.87 Billion |

| Growth Rate (2026 - 2031) | 3.64% CAGR |

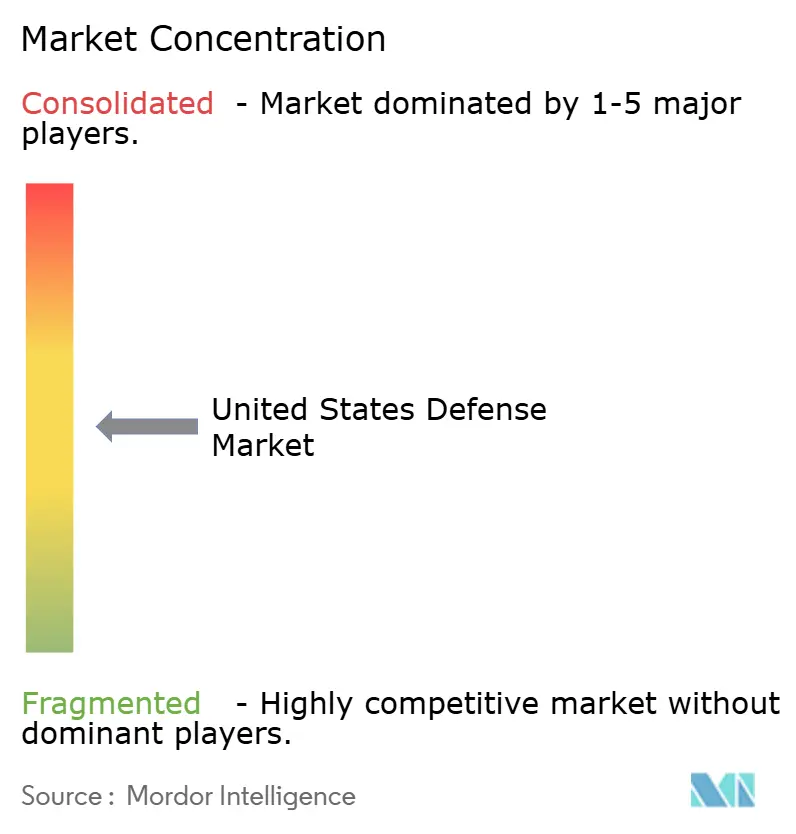

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Defense Market Analysis by Mordor Intelligence

The United States defense market size stood at USD 354.48 billion in 2026 and is projected to reach USD 423.87 billion by 2031, registering a 3.64% CAGR over the forecast period. The growth pace accompanies a structural shift from platform-centric procurement toward networked, software-defined systems that compress decision cycles in contested environments. Great-power competition with China is prioritizing long-range precision fires, proliferating low-Earth-orbit (LEO) constellations, and autonomous collaborative combat aircraft that extend the reach of crewed platforms without proportional cost escalation. Venture-backed entrants, such as Anduril Industries, demonstrate that digital engineering and modular, upgradeable architectures can deliver lethal capabilities at commercial refresh rates. At the same time, traditional primes pivot toward open-systems integration to defend their incumbency. Amid these shifts, continuing-resolution ceilings, depot labor shortages, and export-control compliance burdens temper near-term outlays yet ultimately reinforce the imperative for resilient supply chains and rapid fielding pathways.

Key Report Takeaways

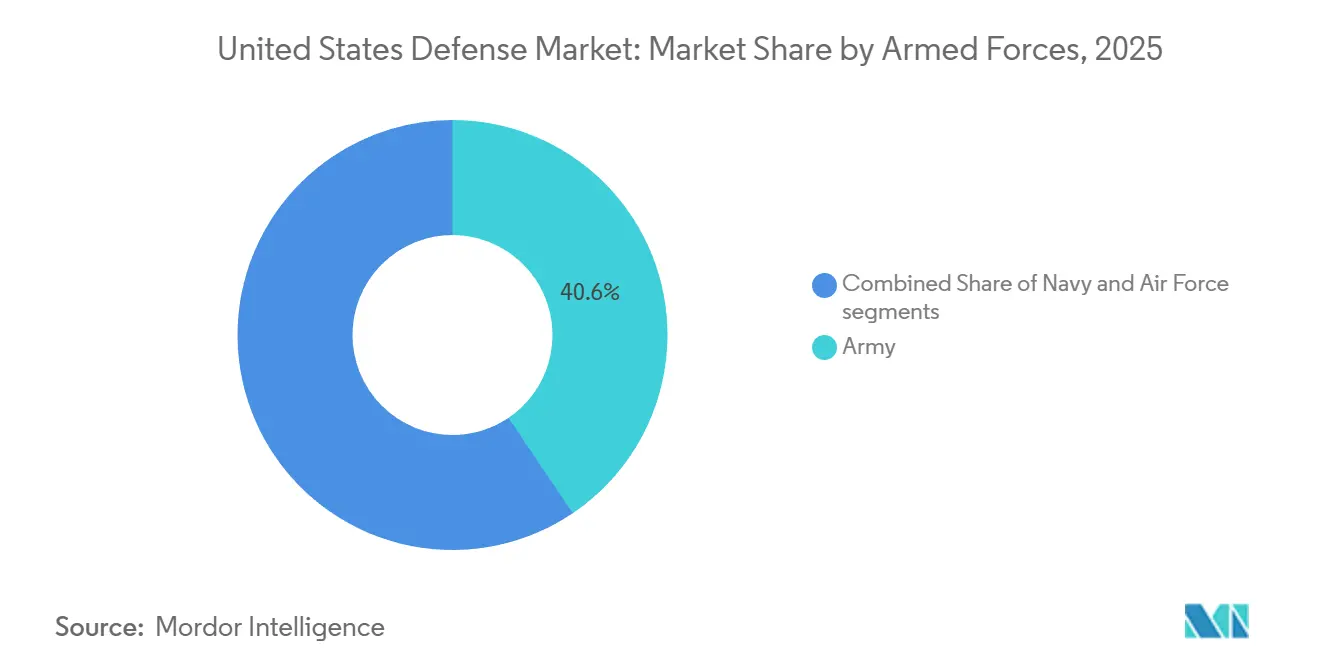

- By 2025, the armed forces, specifically the army, held 40.55% of the United States defense market share, while the air force is forecasted to expand at a 4.98% CAGR through 2031.

- By type, C4ISR and electronic warfare (EW) led with a 31.25% revenue share in 2025; space and cyber systems are projected to grow at a 6.12% CAGR through 2031.

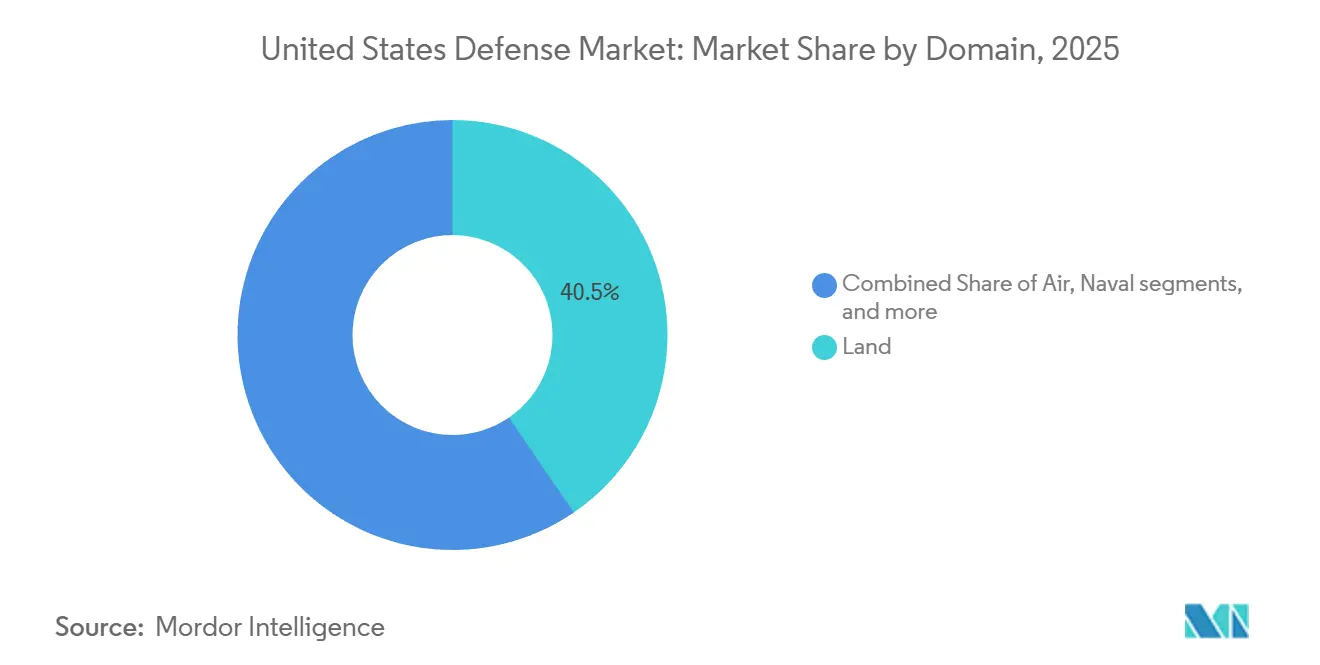

- By domain, land operations accounted for 40.45% of the United States defense market in 2025, while space operations are projected to grow at a 6.98% CAGR through 2031.

- By type, C4ISR and electronic warfare led with a 31.25% revenue share in 2025; space and cyber systems are projected to grow at a 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated replacement and modernization of legacy Cold War–era platforms | +1.20% | Continental US depots, forward-deployed units in Indo-Pacific and Europe | Medium term (2-4 years) |

| Great-power competition re-prioritizing multi-domain dominance | +1.50% | Indo-Pacific theater receives disproportionate allocation | Long term (≥4 years) |

| Rapid fielding pathways under FY24 National Defense Authorization Act | +0.80% | National, early use by SOCOM and combatant commanders | Short term (≤2 years) |

| Digital-engineering mandates compressing design-to-deployment cycle | +0.70% | National, led by PEO Advanced Aircraft and Army Futures Command | Medium term (2-4 years) |

| Commercial-space cost curves enabling proliferated LEO constellations | +0.90% | Global, Space Force prioritizes resilient architectures | Medium term (2-4 years) |

| Silicon Valley venture funding for dual-use start-ups | +0.60% | Southern California, Boston, Austin tech hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Accelerated Replacement and Modernization of Legacy Cold War-Era Platforms

Aging air, sea, and ground fleets averaging three to four decades in service drive escalating sustainment costs that crowd out new procurement across the US Defense Industry. The KC-135 tanker and DDG-51 destroyer classes illustrate how deferred recapitalization strains readiness and budgets. Northrop Grumman’s USD 1.381 billion award in February 2025 to expand the Integrated Battle Command System (IBCS) software underscores how allied interoperability accelerates US modernization timelines. Sustained demand for recapitalization underpins steady procurement volumes, even as unit costs rise and production rates lag behind retirement schedules.

Great-Power Competition Re-Prioritizing Multi-Domain Dominance

China’s anti-access/area-denial posture across the First Island Chain has rendered short-range legacy platforms increasingly vulnerable, compelling the Department of Defense (DoD) to field penetrating counter-air and stand-in forces. In 2024, the US Secretary of Defense issued a warning that China poses a “present threat,” underscoring the urgency of systems capable of withstanding contested electromagnetic environments.[1]Erin B. Logan, “Report to Congress on Air Force NGAD Fighter,” USNI.ORG The Air Force’s F-47 Next Generation Air Dominance (NGAD) fighter, awarded to Boeing in March 2025, exemplifies this pivot with a greater than 1,000-nautical-mile combat radius and enhanced stealth.

Rapid Fielding Pathways Under FY24 National Defense Authorization Act

The FY24 NDAA authorizes up to USD 100 million annually per Service for emergent-technology activities that can be operational within 24 months, allowing commanders to bypass traditional milestone gates. Special Operations Command has already awarded counter-UAS and AI-enabled ISR contracts within 15 days of need statements, demonstrating venture-speed procurement unseen in legacy programs.[2]GovRegs Editors, “Procedures for Urgent Acquisition,” GOVREGS.COM However, uneven adoption across the armed forces creates a bifurcated acquisition landscape where niche capabilities accelerate while major platforms remain tethered to multi-year cycles.

Digital-Engineering Mandates Compressing Design-to-Deployment Cycle

Digital twins and model-based systems engineering are shrinking design timelines by up to 40%, accelerating innovation across the US Defense Industry. The NGAD demonstrator reportedly flew within one year of digital design freeze, validating virtual-prototype methodologies. Parallel adaptive-cycle engine developments from GE and Pratt & Whitney illustrate how digital engineering preserves industrial base competition while accelerating maturation; however, translating virtual models to production exposes data standard and cybersecurity gaps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continuing-resolution budget ceilings | -0.90% | Nationwide, cascading supplier impacts | Short term (≤2 years) |

| MRO labor shortages in naval and air depots | -0.60% | Public shipyards and Air Logistics Complexes | Medium term (2-4 years) |

| Inflation pass-through clauses delaying contract awards | -0.40% | Fixed-price development contracts nationwide | Short term (≤2 years) |

| ITAR/EAR compliance burdens for emerging tech vendors | -0.30% | National, allied co-development programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Continuing-Resolution Budget Ceilings

Eight of the past ten fiscal years opened under continuing resolutions that freeze funding at prior-year levels and bar new-start programs. The FY2025 operating plan’s USD 557.10 million transfer from F-47 development to a distinct collaborative-combat-aircraft line illustrates how legislative uncertainty fragments funding and inflates unit costs.[3]U.S. Congress, “10 U.S.C. § 3601 Urgent Acquisition Procedures,” CONGRESS.GOV Suppliers face cash-flow squeezes that erode surge capacity, perpetuating a cycle in which instability begets inefficiency and congressional skepticism.

MRO Labor Shortages in Naval and Air Depots

Public shipyards and air logistics complexes report vacancy rates exceeding 20% for welders, electricians, and avionics technicians, creating persistent workforce challenges across the US Defense Industry. Maintenance availabilities for surface combatants and submarines now overrun schedules by 30–40%, reducing fleet readiness and forcing commanders to accept risk in deployment calendars. Apprenticeship pipelines require three to five years to produce journeyman-level mechanics, meaning shortages will constrain readiness throughout the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Armed Forces: Air Force Growth Outpaces Army Share

The Army captured 40.55% of the United States defense market in 2025, reflecting its extensive ground-vehicle, aviation, and soldier-systems portfolios. The Air Force, however, is projected to expand at a 4.98% CAGR through 2031, the fastest among the armed forces, propelled by sixth-generation fighter development, adaptive-cycle propulsion, and integration of loyal-wingman variants. The Navy’s Columbia-class submarines and DDG-51 Flight III destroyers sustain maritime share, though shipyard labor shortages temper near-term deliveries.

The Air Force’s March 2025 NGAD contract to Boeing for more than 185 F-47 fighters anchors its expansion strategy, while the May 2025 designation of Anduril’s YFQ-44A collaborative combat aircraft underscores its commitment to human-machine teaming. By contrast, the Army’s modernization priorities, including the Next-Generation Combat Vehicle (NGCV) and Extended Range Cannon Artillery (ERCA), face budget trade-offs between new procurement and the sustainment of legacy fleets, which moderates growth.

By Type: C4ISR Leadership Meets Space-Cyber Surge

C4ISR and EW dominated the market, accounting for a 31.25% revenue share of the United States defense market in 2025, driven by investments in joint all-domain command and control (JADC2) and next-generation radar programs. Space and cyber systems, though smaller, are forecasted to grow at a 6.12% CAGR, reflecting demand for resilient missile-warning architectures and AI-enabled cyber defense. Weapons and ammunition benefit from stockpile-replenishment mandates linked to Ukraine drawdowns and contingency planning in the Indo-Pacific.

BAE Systems’ USD 1.20 billion MEO missile-warning award exemplifies momentum in the space segment. Cyber growth is led by US Cyber Command’s machine-speed threat-response initiatives. The shift from hardware-centric platforms to software-defined architectures enables over-the-air upgrades that compress lifecycle costs and enhance continuous modernization.

By Domain: Land Primacy Yields to Space Expansion

Land operations retained 40.45% of the 2025 spending in the United States defense market. Yet, space is the fastest-expanding domain, with a 6.98% CAGR through 2031, driven by the Space Force’s proliferated-constellation strategy. Air domain outlays remain robust due to the modernization of fighters, tankers, and bombers, although uncertainty over the NGAD timeline injects risk. Naval investments concentrate on Columbia-class submarines and carrier aviation, yet shipyard backlogs delay deliveries.

Space’s ascent is illustrated by BAE’s missile-warning constellation and the Space Development Agency’s Tranche 1 Transport Layer. Land’s slower growth results from Army program cancellations and the maturation of its modernization portfolio. The cyber-electromagnetic spectrum domain, although small, grows quickly as electronic-warfare and spectrum-management tools gain budget priority.

By Procurement Nature: Indigenous Production Sustains Leadership

Indigenous production accounted for 69.54% of 2025 spending and is projected to rise at a 5.29% CAGR. Defense Production Act authorities and onshoring mandates for critical minerals and semiconductors reinforce domestic sourcing. Anduril’s planned Ohio factory to mass-produce autonomous systems exemplifies venture-funded onshoring. Foreign procurement grows more slowly, constrained by ITAR restrictions and allied budget pressures.

The FY24 NDAA’s USD 200 million aggregate ceiling for urgent acquisitions favors domestic suppliers capable of fixed-price rapid prototyping. Congressional scrutiny of China-linked supply chains and rare-earth dependencies further tilts the market toward vertically integrated US producers, complicating entry for foreign vendors even from treaty allies.

Geography Analysis

Procurement spans all 50 states, yet theater priorities shape spending. Indo-Pacific allocations emphasize long-range fires, ISR, and mobility assets to counter China. The Air Force’s Bamboo Eagle-Resolute Force Pacific exercise in summer 2025 deployed 300 aircraft and 2,000 personnel across dispersed bases, demonstrating Agile Combat Employment concepts that boost demand for expeditionary support systems. European investments prioritize NATO interoperability, as highlighted by Northrop Grumman’s USD 347.60 million contract share for Poland’s air defense integration.

Domestic depot networks in Norfolk, Portsmouth, Pearl Harbor, Tinker AFB, Hill AFB, and Warner Robins experience skilled-trade vacancies exceeding 20%, which lengthen maintenance timelines. The Austin-based Army Futures Command anchors digital-engineering collaboration with commercial tech hubs, while Space Force operations are clustered in Colorado Springs, Los Angeles, and Huntsville. High-cost-of-living areas, such as Southern California and the Boston corridor, concentrate aerospace talent yet struggle with workforce retention, prompting subcontractor consolidation.

Competitive Landscape

The five traditional primes, namely Lockheed Martin Corporation, RTX Corporation, The Boeing Company, General Dynamics Corporation, and Northrop Grumman Corporation, collectively secured significant prime-contract value in 2025, reflecting moderate concentration. Lockheed Martin’s F-35, THAAD, and Sikorsky portfolios deliver domain diversification, whereas RTX integrates missiles, radars, and engines following the merger. Boeing’s KC-46 delays and commercial aviation turmoil constrain defense growth, while Northrop Grumman capitalizes on strategic systems programs and General Dynamics on shipbuilding and armored vehicles.

Venture-backed disruptors erode the share of incumbents in autonomous systems and software-defined platforms. Anduril’s USD 6.26 billion in cumulative funding and a USD 30.5 billion valuation enable investment in Arsenal, a factory that targets tens of thousands of autonomous systems annually.[4]Julie Bort, “Anduril Raises $2.5B at $30.5B Valuation,” TECHCRUNCH.COM The Air Force’s selection of Anduril’s YFQ-44A collaborative combat aircraft validates start-ups’ ability to penetrate high-end fighter niches. White-space opportunities center on AI-enabled mission planning, counter-UAS, and secure cloud architectures, yet ITAR compliance and security-clearance pipelines remain barriers for newcomers.

Intellectual property strategies diverge with Anduril’s more than 350 patents on image noise reduction and modular vehicle management, illustrating how dual-use entrants build defensible technology positions.[5]PitchBook Analysts, “Anduril Industries 2025 Company Profile,” PITCHBOOK.COM Traditional primes respond with open-systems initiatives and venture-investment arms to absorb external innovation. The competitive dynamic is increasingly hinged on software agility, supply-chain resilience, and the capacity to scale production rapidly.

United States Defense Industry Leaders

Lockheed Martin Corporation

The Boeing Company

General Dynamics Corporation

RTX Corporation

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The US DoD and Lockheed Martin finalized an agreement to more than triple the production of PAC-3 Missile Segment Enhancement units over seven years.

- October 2025: General Dynamics Mission Systems announced that it was awarded a USD 28.30 million contract by the US Army to deliver critical C5ISR/EW Modular Open Suite of Standards (CMOSS) Mounted Form Factor (CMFF) prototype systems.

- September 2025: The Navy awarded contracts for the development of Collaborative Combat Aircraft (CCA) drones to leading defense contractors, including Anduril, Lockheed Martin, General Atomics, Boeing, and Northrop Grumman.

United States Defense Market Report Scope

The United States defense market study analyzes historical, current, and projected budget allocation and spending patterns. The market encompasses a range of activities, products, and services that support national defense and security requirements. The country's defense strategy focuses on protecting against external and internal threats while safeguarding strategic interests.

The study examines procurement and modernization plans for the UK armed forces. It also covers investments in satellite development and deployment, as well as the research and development of advanced technologies, including directed energy weapons (DEWs), hypersonic missiles, unmanned systems, advanced composites, and advanced manufacturing technologies such as 3D printing.

The United States defense market is segmented by armed forces, type, domain, and procurement nature. By armed forces, the market is segmented into the air force, the army, the navy, and the space force. By type, the market is segmented into personnel training and protection, C4ISR and electronic warfare, vehicles, weapons and ammunition, unmanned systems, and space and cyber systems. By domain, the market is segmented into land, air, naval, space, and cyber and electromagnetic spectrum. By procurement nature, the market is segmented into indigenous production and foreign procurement. The report offers the market size and forecasts in value (USD) for all the above segments.

By Armed Forces

| Air Force |

| Army |

| Navy |

| Space Force |

By Type

| Personnel Training and Protection |

| C4ISR and Electronic Warfare (EW) |

| Vehicles |

| Weapons and Ammunition |

| Unmanned Systems |

| Space and Cyber Systems |

By Domain

| Land |

| Air |

| Naval |

| Space |

| Cyber and Electromagnetic Spectrum |

By Procurement Nature

| Indigenous Production |

| Foreign Procurement |

| By Armed Forces | Air Force |

| Army | |

| Navy | |

| Space Force | |

| By Type | Personnel Training and Protection |

| C4ISR and Electronic Warfare (EW) | |

| Vehicles | |

| Weapons and Ammunition | |

| Unmanned Systems | |

| Space and Cyber Systems | |

| By Domain | Land |

| Air | |

| Naval | |

| Space | |

| Cyber and Electromagnetic Spectrum | |

| By Procurement Nature | Indigenous Production |

| Foreign Procurement |

Key Questions Answered in the Report

What was the United States defense outlay in 2026 and what CAGR is projected through 2031?

Spending reached USD 354.48 billion in 2026 and is projected to increase at a 3.64% CAGR through 2031.

Which armed service is forecast to record the fastest budget growth by 2031?

The Air Force segment is expected to expand at a 4.98% CAGR, fueled by sixth-generation fighter and collaborative combat aircraft programs.

Which capability area is projected to advance most rapidly over the next five years?

Space and cyber systems spending is set to rise at a 6.12% CAGR as the Pentagon fields proliferated LEO missile-warning constellations and AI-enabled cyber defenses.

What portion of 2025 procurement originated from domestic suppliers?

Indigenous production accounted for 69.54% of 2025 outlays and is forecast to grow at a 5.29% CAGR.

How is spending on the space domain expected to evolve by 2031?

Space allocations are growing at a 6.98% CAGR, the highest among domains, driven by resilient missile-warning and tracking programs.

What capital trend is enabling venture-backed companies to compete with traditional primes?

Large late-stage venture rounds; exemplified by Anduril’s USD 2.5 billion Series G in 2025; are funding scalable autonomous-system production and accelerating tech insertion.

How do continuing resolutions influence defense contract timelines?

Funding freezes under continuing resolutions delay new-start programs, defer contract awards, and add 5–10% to unit costs due to production inefficiencies.

Page last updated on: