Market Overview

| Study Period | 2020 - 2031 |

|---|---|

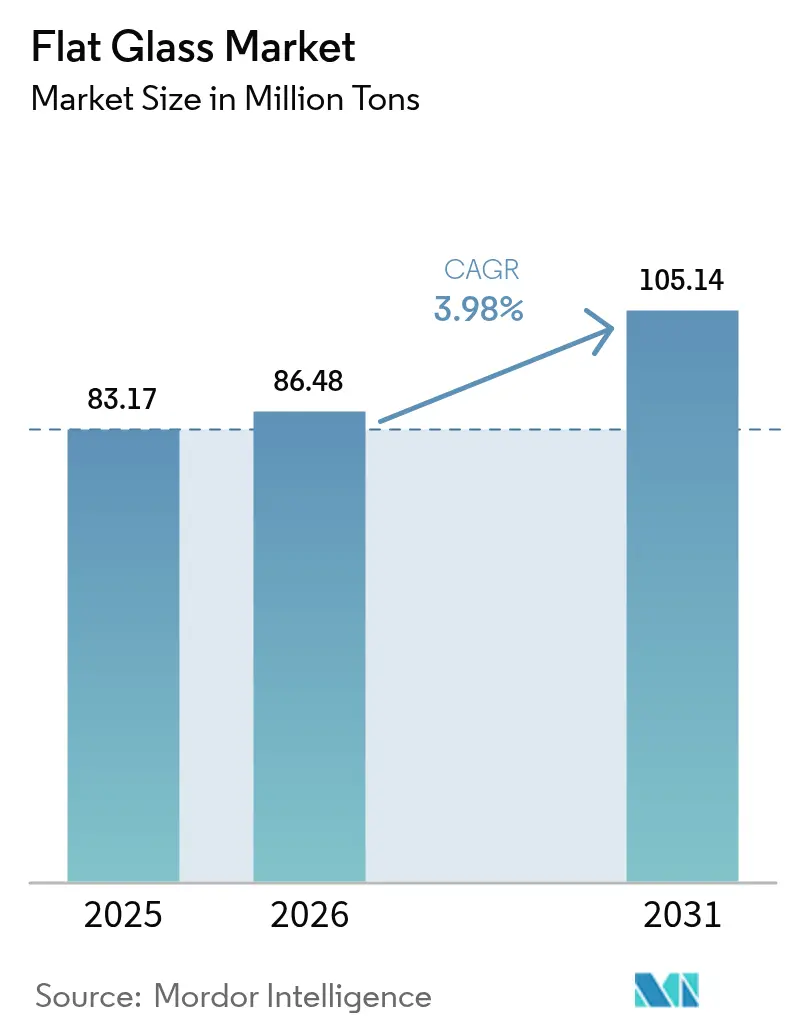

| Market Volume (2026) | 86.48 Million tons |

| Market Volume (2031) | 105.14 Million tons |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

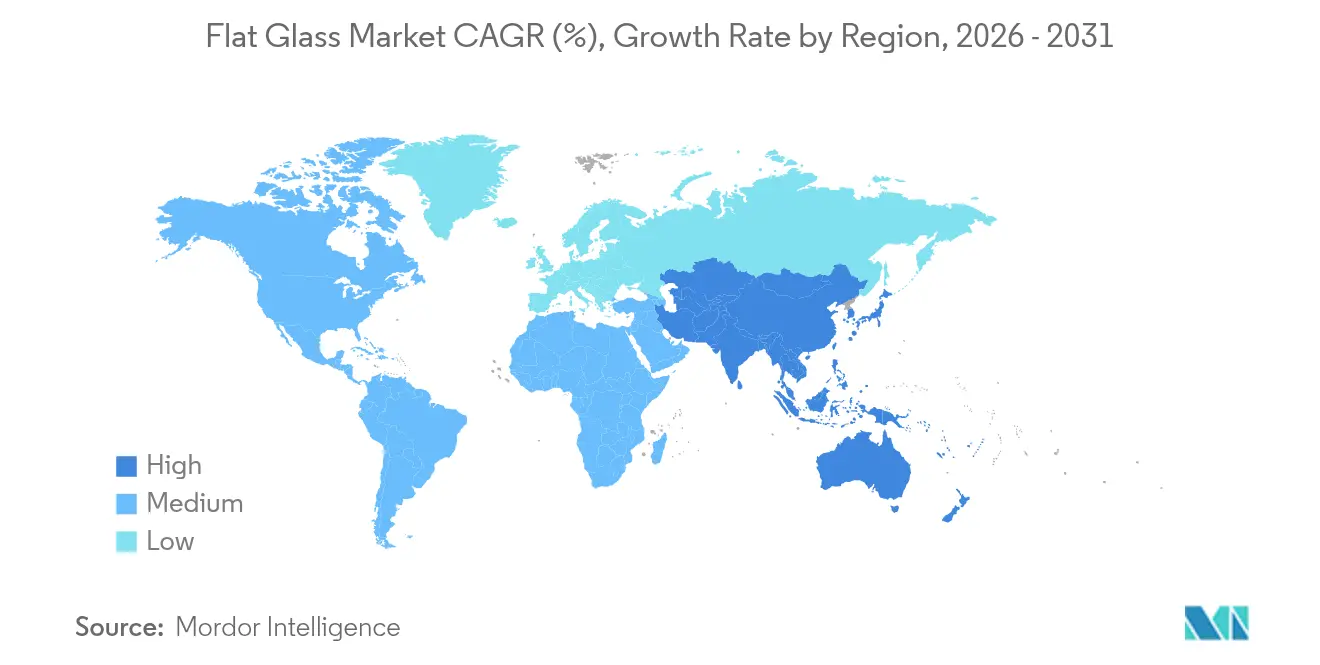

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flat Glass Market Analysis by Mordor Intelligence

The Flat Glass market size is expected to grow from 83.17 Million tons in 2025 to 86.48 Million tons in 2026 and is forecast to reach 105.14 Million tons by 2031 at 3.98% CAGR over 2026-2031. Demand resilience stems from stricter construction energy codes, rapid photovoltaic build-outs, and automotive lightweighting that favors advanced glazing. Manufacturers are shifting toward low-carbon melting, green hydrogen trials, and oxy-electric hybrid furnaces to secure price premiums in sustainability-conscious tenders. Solar module glass, antimicrobial coatings for healthcare facilities, and ultra-thin triple units for high-rise retrofits are expanding the revenue mix. Asia-Pacific anchors both production and consumption, while North America and Europe invest in furnace electrification to counter energy-price swings and looming carbon tariffs.

Key Report Takeaways

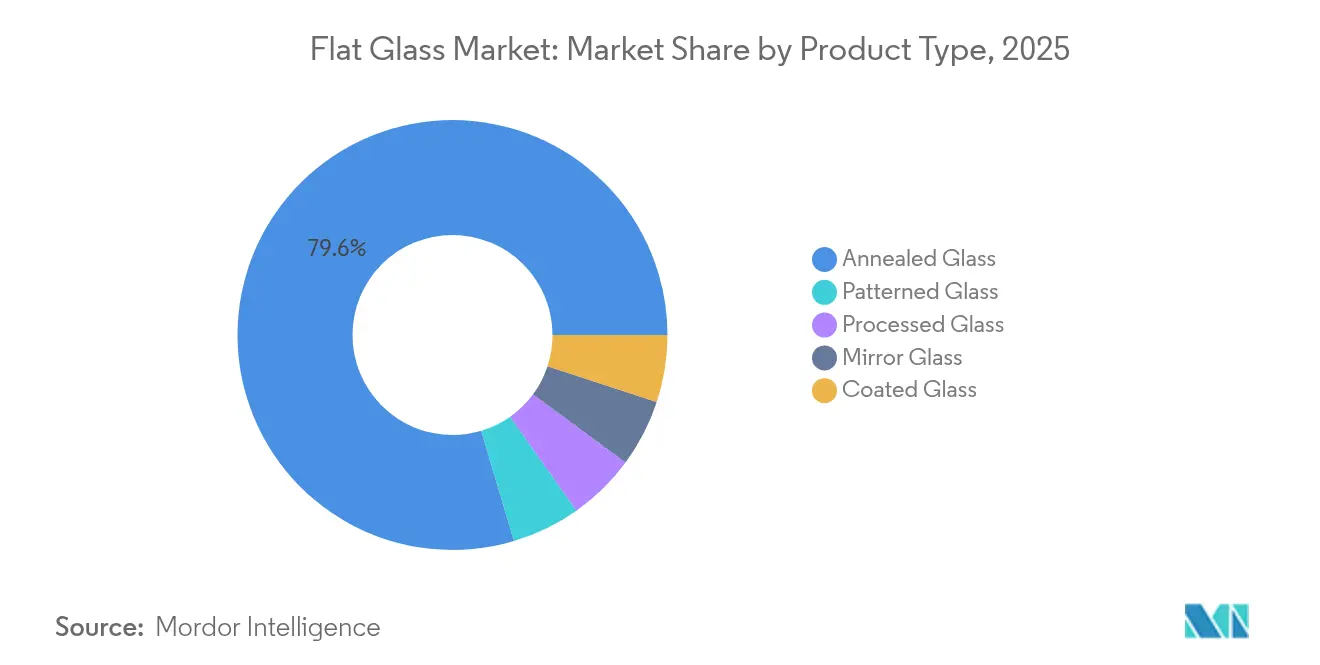

- By product type, annealed glass led with 79.62% of the flat glass market share in 2025, whereas processed glass is projected to grow at a 4.65% CAGR to 2031.

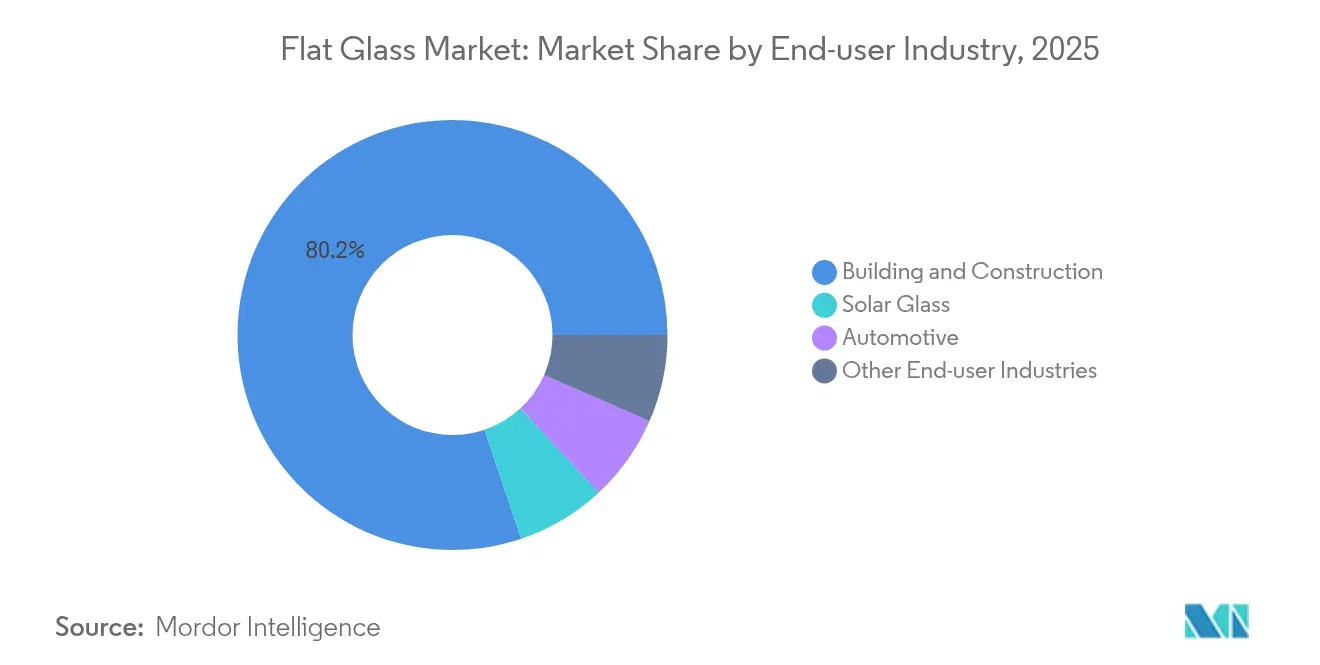

- By end-user industry, building and construction accounted for 80.18% of the flat glass market size in 2025; solar glass is advancing at a 6.45% CAGR through 2031.

- By geography, Asia-Pacific commanded 63.88% revenue in 2025, while also topping the growth table with a 4.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flat Glass Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction spending rebound | +1.2% | APAC and North America | Medium term (2-4 years) |

| EV glazing and lightweighting | +0.8% | China, Europe, North America | Medium term (2-4 years) |

| Solar-grade glass capacity surge | +1.0% | APAC core, spill-over to Europe and North America | Long term (≥ 4 years) |

| Energy-efficient building codes | +0.7% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Antimicrobial glass uptake | +0.3% | Developed markets worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Investments in Commercial and Residential Construction

Global construction outlays are forecast to climb, aided by lower borrowing costs and an uptick in developer sentiment. Multifamily starts accelerate in response to single-family affordability gaps, channeling sustained demand for curtain wall and window systems that integrate Low-E and triple-glazed units. Developers specify higher-performance glass to secure LEED credits, driving volume growth for sputter-coated and argon-filled insulating products. The flat glass market, therefore, benefits directly from code-driven window-to-wall ratios that favor advanced glazing solutions.

Rising Automotive Glazing Requirements for EV Safety and Lightweighting

Electric vehicle platforms intensify structural glazing needs while mandating lighter glass to offset battery mass. Fuyao committed CNY 9.1 billion (USD 1.26 billion) in 2024 for two new plants aimed at new-energy vehicle demand. Thin laminated windshields, panoramic roofs, and heads-up display-ready windscreens expand processed glass penetration. Embedded sensor packages elevate value per car, creating a lucrative growth pocket inside the broader flat glass market. Aerodynamic gains from slimmer profiles further align with range optimization, cementing glass as a critical lightweight substrate over the forecast horizon.

Rapid Capacity Additions for Solar PV Module Glass

Global PV deployments surpassed 1.6 TWdc by end-2023, and regional makers are retrofitting float lines for low-iron solar sheets[1]David Feldman, “Solar Industry Update,” U.S. Department of Energy, energy.gov. NSG and Vitro invested USD 180 million to upgrade furnaces for transparent conductive oxide coatings, while the segment already represents 5% of floated output. With solar installations projected to exceed 240 GW annually by 2030, the flat glass market gains a durable, high-margin outlet for specialized ultra-clear products.

Energy-Efficient Building Codes Boosting Low-E and Triple Glazing Demand

The 2024 International Energy Conservation Code trims allowable fenestration air leakage to 0.35 cfm/ft² and tightens U-factor bands in temperate zones. ASHRAE 90.1-2019 lowered U-values a further 17% for some assemblies, fueling triple-pane adoption. Glaston’s 0.5 mm center-glass IGU delivers 20% better thermal performance at lower frame loads. Vacuum insulating units now achieve 0.5 W/m²·K but remain premium-priced. Each revision embeds higher-value coated glass into project specifications, enlarging the addressable flat glass market.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of polymer, acrylic and polycarbonate substitutes | -0.5% | Global, with higher impact in automotive applications | Medium term (2-4 years) |

| Volatile soda-ash and natural-gas input costs | -0.8% | Global, with acute impact in Europe and North America | Short term (≤ 2 years) |

| EU Carbon Border Adjustment Mechanism compliance costs | -0.3% | Europe and exporters to EU markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Polymer, Acrylic and Polycarbonate Substitutes

Automakers trial polycarbonate side windows and panoramic roofs that weigh up to 50% less than comparable glass panels. Optical clarity and UV stability have improved, yet scratch resistance and thermal tolerance still lag glass. Stringent windshield regulations keep polycarbonate use niche, confining substitution risk mostly to non-load-bearing glazing. Glass recycling advantages and tighter end-of-life circularity goals further insulate flat glass market volumes.

Volatile Soda-Ash and Natural-Gas Input Costs

Soda ash spot prices fell amid oversupply, but the input remains prone to price swings that compress margins. WE Soda’s USD 1.425 billion deal for Genesis Alkali consolidated 9.5 million tons of natural trona capacity, potentially stabilizing supply yet concentrating purchasing power. European producers face added strain from natural-gas volatility, spurring trials with biofuel and electric melting. O-I Glass completed a 100% biofuel furnace run in 2025, proving an alternative path to de-risk energy costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Processed Glass Drives Innovation

Processed glass generated the fastest 4.65% CAGR between 2026 and 2031, outpacing the broader flat glass market. Laminated and tempered variants supply automotive windscreens, curtain walls, and security facades where impact resistance is critical. Annealed output still dominated in 2025 with 79.62% of volume because it serves as the base substrate for downstream upgrades. The segment’s cost edge keeps it central to commodity construction, yet its share is set to moderate as codes and safety norms elevate demand for value-added treatments.

Coated, reflective, and Low-E sheets advance in parallel due to mandatory thermal standards. AGC Glass Europe’s 5.5 kg CO₂ eq/m² Low-Carbon Glass exemplifies product differentiation that commands premium bids. Tinted glass usage in EVs supports cabin cooling and battery efficiency. Mirror and patterned glass remain niche but attractive for interior and privacy applications. Altogether, specialization raises average selling prices, widening the processed share in the flat glass market size over the forecast horizon.

By End-user Industry: Solar Glass Accelerates Growth

Building and construction remained the anchor at 80.18% of demand in 2025, yet solar glass is on track for a 6.45% CAGR through 2031, the fastest among all end-users. Utility-scale and rooftop installations require ultra-clear, low-iron sheets with anti-reflective layers, prompting float line conversions worldwide. AGC’s tie-up with recycling firm ROSI will channel retired PV cover glass back into new float batches, reinforcing circular supply.

Commercial retrofits, housing densification, and mixed-use projects bolster architectural glazing volumes, especially where Low-E and triple units meet stricter codes. Automotive demand allies with EV adoption, using heads-up display-compatible windscreens and thinner laminates to trim mass. Appliance, furniture, and antimicrobial hospital partitions add steady baseline consumption. These dynamics diversify revenue streams and cushion the flat glass market against cyclical shocks in any single sector.

Geography Analysis

The Asia-Pacific region secured 63.88% of 2025 shipments and is expanding at a 4.63% CAGR, the highest among regions. India is scaling new float lines while testing green hydrogen furnaces under a 20-year offtake pact between Asahi India Glass and INOX Air Products.

Europe focuses on decarbonization leadership. Saint-Gobain and AGC started trials of a hybrid furnace that cuts CO₂ by 75% through 50% electrification and oxy-fuel combustion, supported by the EU Innovation Fund. Carbon Border Adjustment Mechanism fees, effective 2026 incentivize local sourcing, potentially boosting intra-regional sales. North American producers, led by Vitro’s USD 180 million modernization and O-I’s UK investment, upgrade lines to withstand gas-price volatility and ESG scrutiny.

South America, the Middle East, and Africa post rising urbanization but face infrastructure deficits and competition from Asian imports. Green-field float projects remain selective, though regional builders prefer local panes to avoid freight surcharges, supporting gradual volume growth. Altogether, geographic shifts keep Asia unchallenged in volume share while other regions chase value-added specialties within the flat glass market.

Competitive Landscape

The global flat glass market is moderately fragmented. AGC, Saint-Gobain, Guardian Industries, and Fuyao leverage multi-continent furnace networks and in-house coating technologies to deliver differentiated portfolios. Fuyao’s automotive focus secures global contracts, while Guardian’s vacuum insulating unit patents position it for premium retrofit demand. Saint-Gobain and AGC co-develop hybrid furnaces that could slash energy consumption, sharpening their sustainability brand. New entrants target niche segments like antimicrobial coatings and ultra-thin vacuum insulating glazing. Barriers include capital intensity and multiyear permitting cycles, but collaboration models with equipment suppliers shorten ramp-ups.

Flat Glass Industry Leaders

AGC Inc.

Saint-Gobain

Guardian Industries

Nippon Sheet Glass Co. Ltd

Xinyi Glass Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Saint-Gobain and AGC began pilot runs on a hybrid flat glass line that targets 75% CO₂ cuts via 50% electrification and oxy-gas combustion.

- October 2024: AGC Glass Europe partnered with ROSI to recycle PV cover sheets into new flat glass, advancing circular economy goals.

Global Flat Glass Market Report Scope

Flat glass is a type of glass initially produced in plane form. It is commonly used for windows, glass doors, transparent walls, and windscreens. Flat glass is sometimes bent after the plane sheet is produced for modern architectural and automotive applications.

The flat glass market is segmented by product type, end-user industry, and geography. The market is segmented by product type into annealed glass, coated glass, processed glass, mirror glass, and patterned glass. By end-user industry, the market is segmented into building and construction, automotive, solar glass, and other end-user industries. The report also covers the market sizes and forecasts for the flat glass market in 15 countries across major regions. For each segment, the market sizing and forecasts are done based on volume (tons).

By Product Type

| Annealed Glass | Clear Glass |

| Tinted Glass | |

| Coated Glass | Reflective Glass |

| Low-E Glass | |

| Processed Glass | Laminated Glass |

| Tempered Glass | |

| Mirror Glass | |

| Patterned Glass |

By End-user Industry

| Building and Construction |

| Automotive |

| Solar Glass |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Annealed Glass | Clear Glass |

| Tinted Glass | ||

| Coated Glass | Reflective Glass | |

| Low-E Glass | ||

| Processed Glass | Laminated Glass | |

| Tempered Glass | ||

| Mirror Glass | ||

| Patterned Glass | ||

| By End-user Industry | Building and Construction | |

| Automotive | ||

| Solar Glass | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the flat glass market in volume terms?

The flat glass market size reached 86.48 million tons in 2026 and is forecast to hit 105.14 million tons by 2031.

Which region leads global demand for flat glass?

Asia-Pacific led with 63.88% of 2025 shipments and is also the fastest-growing region at a 4.63% CAGR.

Which flat glass segment is expanding the fastest?

Solar glass is projected to grow at a 6.45% CAGR through 2031, outpacing all other end-user segments.

How are sustainability targets influencing flat glass production?

Producers are piloting hybrid oxy-electric furnaces, green hydrogen firing, and recycled cullet programs to cut CO? emissions by up to 75%.

Who are the major players in the flat glass market?

AGC, Saint-Gobain, Guardian Industries, and Fuyao Group lead the market, backed by global furnace networks and advanced coating technologies.

What are the main raw-material risks for glassmakers?

Volatile soda-ash prices and fluctuating natural-gas costs can erode margins, prompting firms to secure trona supply and trial alternative fuels.

Page last updated on: