Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.76 Billion |

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.66 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Faucet Market Analysis by Mordor Intelligence

India faucets market size in 2026 is estimated at USD 1.89 billion, growing from 2025 value of USD 1.76 billion with 2031 projections showing USD 2.66 billion, growing at 7.12% CAGR over 2026-2031. Urbanization, government housing schemes, and shifting consumer preferences toward premium fixtures explain most of this rise. Smart Cities Mission spending funnels institutional orders directly to large manufacturers, smoothing demand cycles and encouraging capacity investments. Rising disposable income supports upgrades from basic taps to designer models, while digital retail channels lower discovery costs and broaden reach. Organized brands gain visibility through e-commerce, yet unorganized suppliers still compete on price in rural and semi-urban zones.

Key Report Takeaways

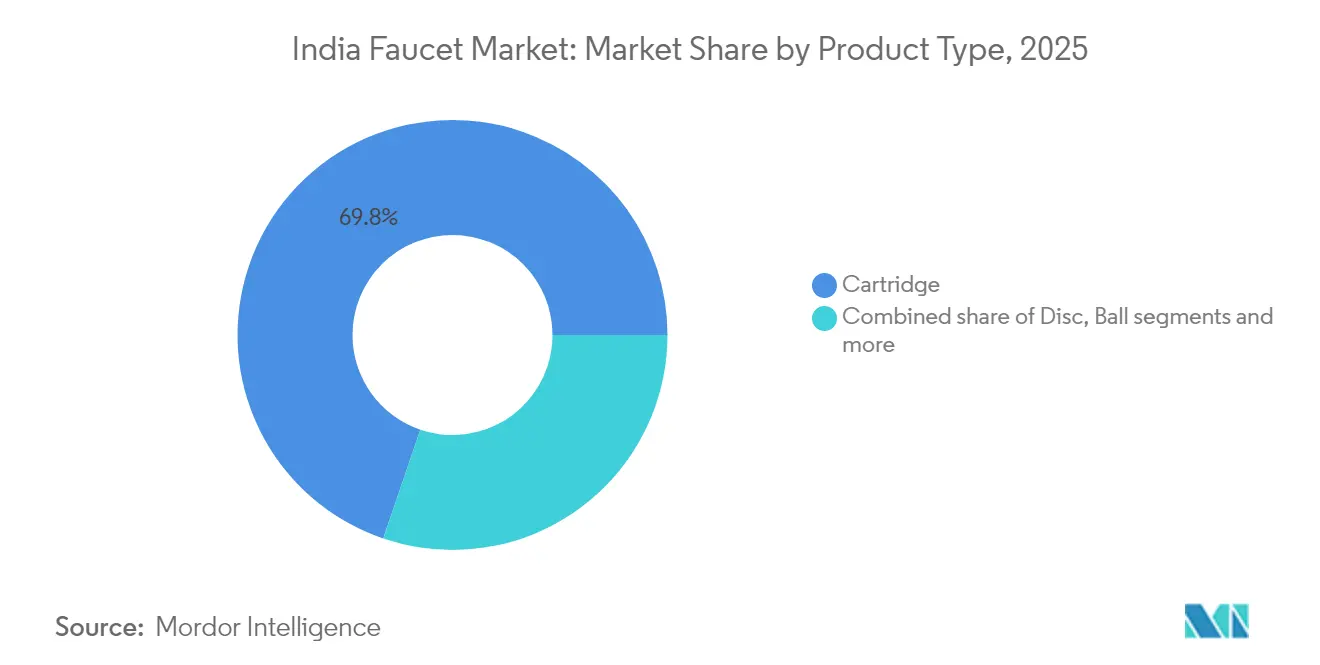

- Cartridge faucets commanded 69.78% of the India faucets market share in 2025, while ceramic disc models are expected to grow at a 7.18% CAGR through 2031.

- Brass units accounted for 48.71% of revenue in 2025; stainless-steel pieces are forecast to expand at a 7.45% CAGR over the same period.

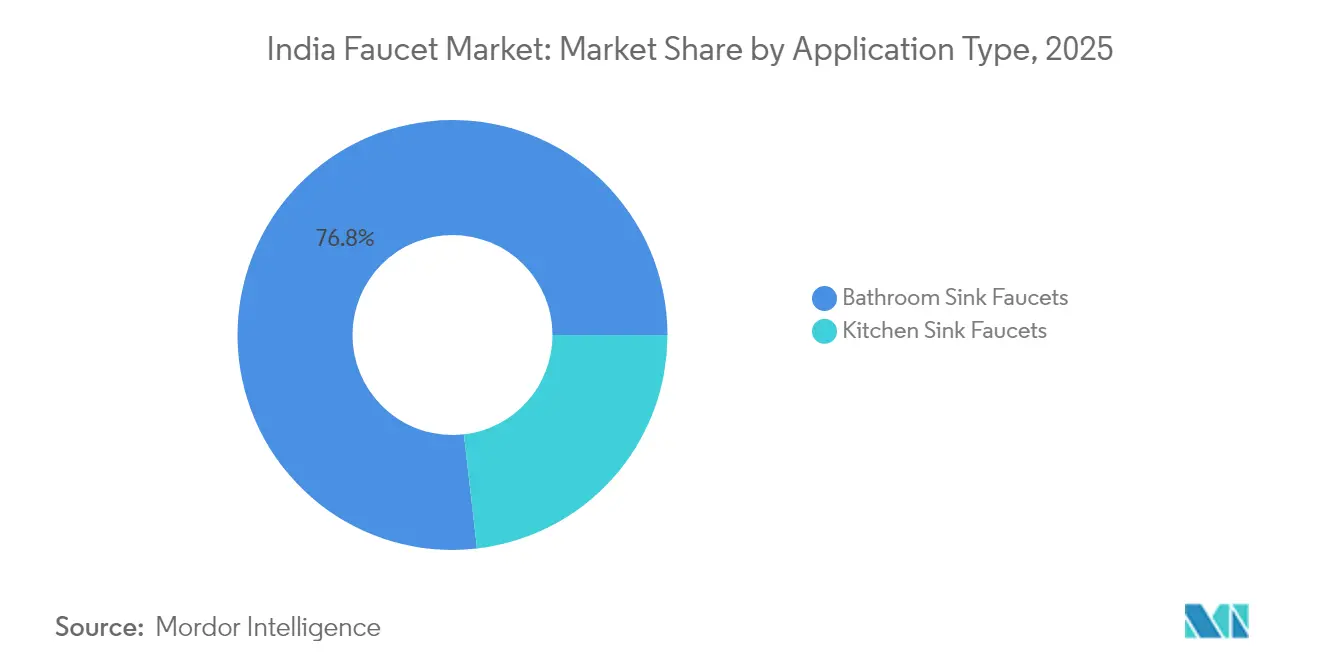

- Bathroom sink installations contributed 76.82% of 2025 revenue, yet kitchen sink faucets are projected to advance at a 7.52% CAGR to 2031.

- Residential buyers generated 67.65% of 2025 turnover, whereas commercial end-users are set to rise at 7.60% CAGR during the outlook period.

- South India captured 34.12% of the India faucets market in 2025; North India is positioned for an 8.21% CAGR to 2031.

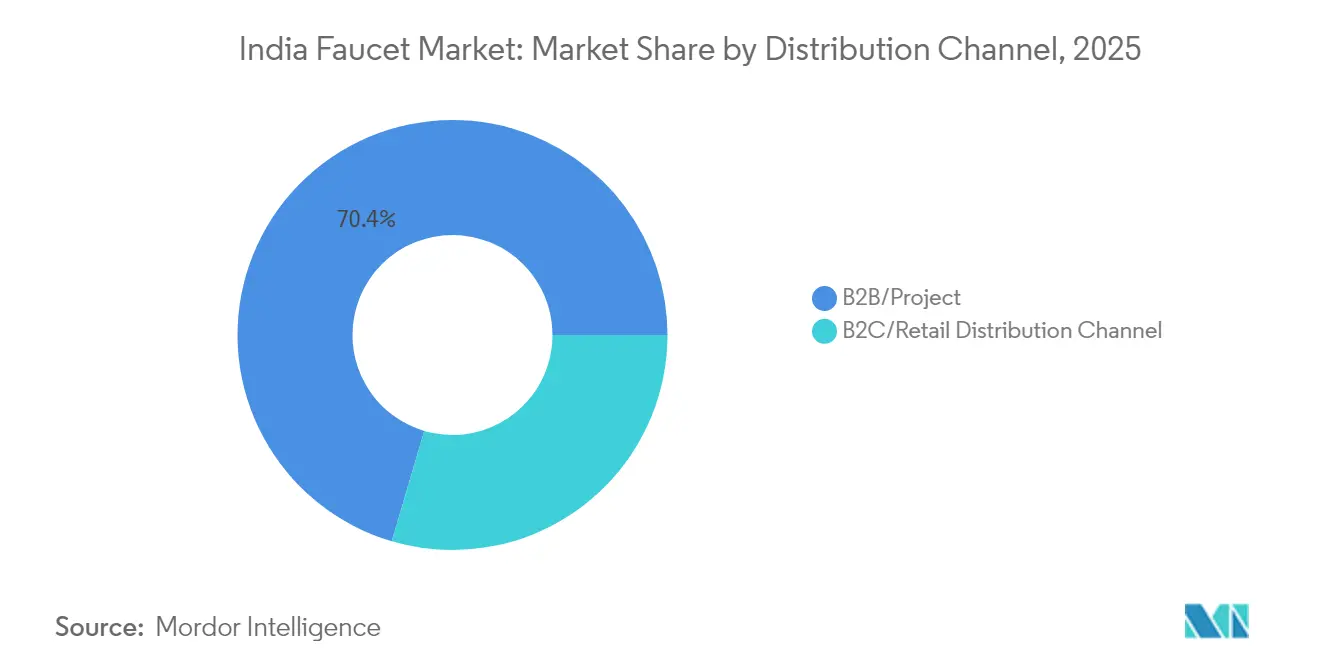

- B2B/project channels held 70.44% revenue share in 2025; B2C/retail channels are likely to post a 7.36% CAGR on the back of e-commerce penetration.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Faucet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urban housing projects & Smart Cities Mission | +1.2% | National, with early gains in Delhi NCR, Pune, Chennai | Medium term (2-4 years) |

| Rising hotel-hospital capex in Tier-2/3 cities | +0.8% | Central & Western India core, spill-over to Eastern regions | Medium term (2-4 years) |

| E-commerce accelerating branded faucet penetration | +0.9% | National, with higher impact in metros and Tier-1 cities | Short term (≤ 2 years) |

| Water-scarcity push for low-flow & WaterSense-style products | +0.7% | Western & Southern India, expanding to Northern states | Long term (≥ 4 years) |

| IoT-enabled "smart" kitchens & bathrooms adoption | +0.5% | Metro cities and premium housing segments nationally | Long term (≥ 4 years) |

| GST-credit advantage shifting share to organised players | +0.6% | National, with stronger impact in tax-compliant regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban Housing Projects & Smart Cities Mission

Government programs reshape faucet demand through scale procurement that locks in standard specifications. The Smart Cities Mission earmarked INR 5,961 crore for smart water systems, triggering bulk orders for sensor-ready fixtures. PMAY-U approvals covering 12.2 million units stabilize long-run volumes and favor firms with reliable supply chains. Institutional buyers insist on water-efficient models, speeding mainstream adoption of aerators and flow restrictors. Predictable tender cycles allow factories to plan tooling upgrades and reduce per-unit costs. Compliance requirements also edge out informal makers that lack certification infrastructure.

Rising Hotel-Hospital Capex in Tier-2/3 Cities

Secondary cities witness brisk hotel construction as leisure and business travel disperse beyond metros. Developers specify sturdy, stylish faucets that endure high footfall yet match premium décor. Parallel healthcare spending adds demand for touchless units that enhance infection control. Stainless steel gains traction for its durable finish and low-maintenance profile in intensive-use settings. Regional OEMs with quick service networks win contracts by cutting downtime for maintenance calls. The combined pipeline lifts commercial sales faster than housing replacements through 2030.

E-commerce Accelerating Branded Faucet Penetration

Digital marketplaces, with their transparent pricing, vivid imagery, and doorstep delivery, empower brands to bypass dealer mark-ups. These platforms provide consumers with a seamless shopping experience, offering a wide range of options and competitive pricing. In India, online sales in the faucets market are surging at an annual rate of 9.12%, outpacing offline growth. This growth is driven by increasing internet penetration, rising smartphone usage, and the convenience of e-commerce platforms. Even for premium SKUs, consumer reviews, especially when paired with on-site installation services, bolster trust and encourage purchases. Additionally, brands leverage clickstream data to fine-tune designs and predict color trends, all with reduced lead times, enabling them to stay ahead of market demands. Omnichannel strategies, including showroom pickups for online orders, are not only slashing last-mile costs but also expanding coverage, ensuring a more comprehensive reach to diverse consumer segments.

Water-Scarcity Push for Low-Flow & WaterSense-Style Products

TERI studies show aerators can trim water use by 55%, resonating with households facing tiered tariff hikes[1]The Energy and Resources Institute, “Water Savings through Aerators,” TERI, teriin.org. In Maharashtra and Karnataka, city utilities are incentivizing faucet replacements through rebate schemes, which refund a portion of the replacement costs. These initiatives aim to encourage the adoption of water-efficient fixtures among consumers. The Bureau of Indian Standards (BIS) is in the process of formulating a voluntary star-label program, akin to the U.S. WaterSense initiative, signaling a potential move towards obligatory efficiency regulations. This program is expected to provide consumers with clear information about water-efficient products, fostering informed decision-making. In regions susceptible to drought, builders are proactively installing low-flow taps, not only to comply with anticipated regulations but also to sidestep future retrofit costs. This approach helps them align with evolving water conservation norms while minimizing long-term expenses. Meanwhile, corporate campuses are increasingly opting for flow-controlled models as part of their strategy to achieve Environmental, Social, and Governance (ESG) water targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unorganised/grey market price competition | -1.1% | National, with higher impact in rural and semi-urban areas | Short term (≤ 2 years) |

| Volatile copper & zinc alloy input prices | -0.8% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Fragmented plumbing channel beyond metros | -0.6% | Tier-2/3 cities and rural markets | Medium term (2-4 years) |

| Delay in BIS water-efficiency labelling roll-out | -0.4% | National, with stronger impact on premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Unorganised/Grey Market Price Competition

Micro-scale workshops, which avoid paying GST, offer products priced approximately 18% lower than branded SKUs. This pricing strategy appeals to cost-conscious buyers, particularly in non-metro regions. Local plumbers often recommend these taps because they earn higher profit margins compared to the commissions they receive from selling branded products. Additionally, the shorter delivery distances associated with these workshops reduce freight costs and enable same-day restocking, making them a convenient option. However, the inconsistent quality of alloy grades used in these taps results in higher failure rates, which gradually diminishes buyer confidence. The government's initiative to implement e-invoicing is expected to reduce these price differences after 2026.

Volatile Copper & Zinc Alloy Input Prices

Copper breached INR 905/kg in 2024 and remains choppy, inflating brass faucet costs. Smaller firms lack hedging desks and absorb shocks in margin erosion or abrupt list-price hikes[2]Livemint Desk, “Copper Price Trend in India,” Livemint, livemint.com. Zinc swings compound risk when makers juggle multi-metal portfolios. Frequent repricing irritates channel partners who print catalogues annually, nudging them toward steel-based collections. Meanwhile, tier-one producers find some relief through long-term supply contracts and scrap-recycling efforts, which help mitigate cost pressures and ensure a more sustainable supply chain. These strategies also position them better to navigate the challenges posed by volatile raw material markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cartridge Dominance Faces Disc Innovation

Cartridge assemblies held 69.78% of the India faucets market share in 2025 on the back of familiarity, easy replaceability, and broad price coverage from entry to mid-premium. Yet disc mechanisms posted the quickest momentum at a 7.18% CAGR, adding roughly 4 percentage points to the overall India faucets market by 2031. Consumers in metros value ceramic discs for mineral-build-up resistance and feather-touch operation, ideal for hard-water zones in Delhi NCR. Manufacturers integrate dual-ceramic seals that last up to 500,000 cycles, halving lifetime maintenance versus conventional cartridges. Price compression from Chinese imports and localized disc production in Tamil Nadu narrow the upfront cost gap. Retailers now market disc faucets as “install-and-forget” options, fostering higher ticket sizes.

At the same time ball and compression faucets retain a foothold in rental housing and heritage renovations, respectively. Local authorities restoring colonial structures in Kolkata specify compression types to match historical authenticity, keeping this sub-segment alive. However, rising GST scrutiny and evolving consumer education tilt incremental volumes toward disc and cartridge hybrids that merge field-service simplicity with ceramic sealing. The India faucets market continues to favor modular valves where handles can interchange across designs, pushing OEMs to standardize spindle dimensions for cartridge and disc formats alike.

By Material: Stainless Steel Challenges Brass Leadership

Brass covered 48.71% of the India faucets market in 2025 due to its machinability, corrosion tolerance, and perceived premium finish. Nonetheless, stainless-steel SKUs are forecast to outpace the broader India faucets market, gaining 7.45% CAGR as urban homeowners gravitate to a contemporary brushed aesthetic. The alloy’s lead-free nature aligns with potable-water directives, strengthening its institutional pull in school and hospital contracts. Stainless items also resist fingerprint smudges, vital for high-traffic food-service restrooms.

Brass remains entrenched in luxury villas where heritage gold-tone plating and intricate knurling rule design briefs. OEMs counter stainless momentum by offering low-lead brass blends certified under IS 1264:2021, retaining upscale luster while meeting health norms. Chrome-plated zinc caters to budget refurbishments, though scratch susceptibility limits its commercial usage. PTMT polymer enjoys tax incentives under the government’s plastics processing cluster scheme, carving cost-driven demand in semi-urban self-build homes. Across all materials, recyclability considerations grow salient, pressuring producers to adopt take-back programs and closed-loop smelting for scrap brass.

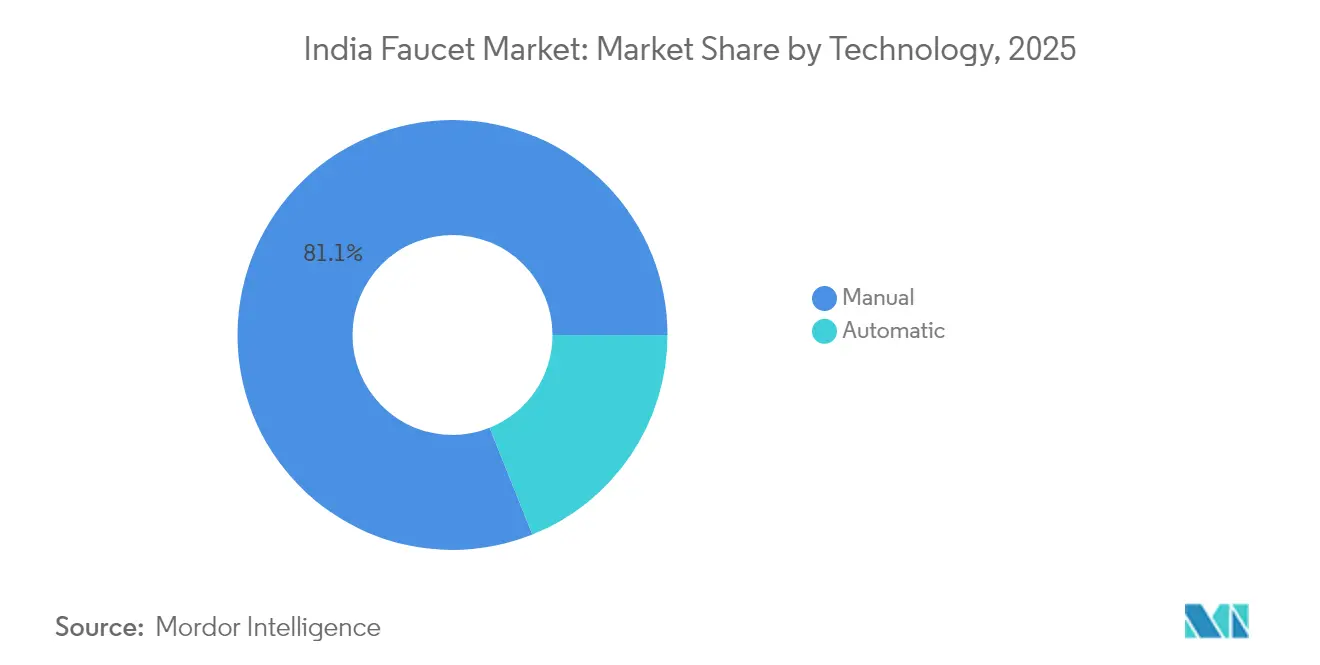

By Technology: Automatic Systems Gain Traction

Manual valves dominated 81.06% of 2025 shipments as price sensitivity defines the mass segment. Yet the automatic cohort is registering an 8.04% CAGR, twice the broader India faucets market pace, aided by falling infrared sensor costs and battery lives now exceeding 300,000 activations. Hotels in Jaipur report water-use cuts of 28% after migrating to touchless taps, translating to one-year payback that resonates with asset managers. Government guidelines for infection control in healthcare also stipulate hands-free operation in ICU suites, driving institutional tenders toward automatic options.

Integration features climb up the specification ladder: Bluetooth modules feed facility dashboards, and solar trickle charging eliminates scheduled battery swaps in office campuses. For residential buyers, inductive recharge cables simplify maintenance anxiety that previously curbed sensor uptake. Domestic brands strike licensing deals with Taiwanese chip makers, embedding AI-based occupancy algorithms that calibrate flow duration to usage patterns. These innovations keep automated formats on an upswing even as manual valves retain baseline volume, ensuring a steady technology mix within the India faucets market.

By Installation Type: Deck Mount Preferences Reflect Design Trends

In 2025, deck mounts captured a dominant 75.12% of the market demand, underscoring a trend towards under-counter basins and quartz countertops. Their design, featuring concealed plumbing, allows for easy access post-installation. This is particularly advantageous for franchise hotels that prioritize minimal downtime. The deck mount segment is witnessing a robust expansion, growing at a 7.28% CAGR. This growth aligns with the rising trend of modular kitchen installations, where sink cut-outs are now designed to accommodate pre-drilled faucet templates. Additionally, the increasing adoption of deck mounts is driven by their compatibility with modern kitchen designs, which emphasize functionality and aesthetics. Manufacturers are also focusing on offering customizable options to cater to diverse consumer preferences, further fueling the segment's growth.

In Mumbai's compact apartments, wall mounts continue to be the preferred choice, conserving valuable counter space. Architects, when designing co-living units, opt for wall-mounted solutions equipped with concealed stop-cocks, simplifying maintenance tasks. However, challenges arise when retrofitting; upgrading to wall mounts often involves chiseling tiles, which significantly increases labor costs. This has led renovation projects to favor deck adaptations as a more cost-effective alternative. To address these challenges, the India faucets market has seen OEMs introducing convertible rough-in kits. These kits enable dealers to stock a single body that can accommodate either deck or wall spouts, optimizing inventory management. Furthermore, the growing focus on urbanization and the rise in co-living spaces are expected to sustain the demand for wall-mounted faucets, particularly in metropolitan areas where space optimization is critical.

By Application Type: Kitchen Segment Accelerates Growth

In 2025, bathroom sink faucets accounted for 76.82% of the revenue, but their growth lagged behind that of kitchen faucets. Forecasts predict a 7.52% CAGR for kitchen faucets, driven by homemakers' preference for single-lever, pull-down sprayers that simplify meal preparation. Additionally, appliance showrooms are boosting sales by bundling faucets with quartz sinks, which has significantly increased attachment rates and enhanced consumer convenience.

Urban millennials, inspired by restaurant workflows, are increasingly opting for commercial-style spring-neck designs. These designs not only offer a professional aesthetic but also provide enhanced functionality, making them a popular choice in urban households. Taps that offer integrated filtration and boiling water can command prices up to three times that of standard kitchen units, reflecting the growing demand for premium and multi-functional products. The kitchen segment is emerging as a testing ground for IoT features, with innovations like voice-controlled dispense volumes that sync with recipe apps. These advancements cater to tech-savvy consumers seeking convenience and efficiency in their kitchens. As a result, these gains in the kitchen segment are compensating for stagnant growth in bathroom faucets, ensuring a steady revenue stream for suppliers in India's faucet market. Furthermore, the shift toward multi-functional and technologically advanced faucets highlights the evolving consumer preferences and the increasing importance of innovation in maintaining market competitiveness.

By End-User: Commercial Growth Outpaces Residential Base

In 2025, residential projects accounted for 67.65% of receipts, buoyed by ongoing metro-led apartment launches. This dominance highlights the sustained demand for residential developments, particularly in urban areas where infrastructure expansion continues to drive growth. However, the commercial sector is projected to achieve a 7.60% CAGR through 2031, driven by burgeoning hospitality pipelines in Tier-2 cities and expansive state healthcare rollouts. These factors underscore the increasing investment in commercial infrastructure, which is expected to contribute significantly to the overall market dynamics. Hotels are opting for high-polish stainless units, rigorously tested for 200,000 handle cycles, ensuring durability and compliance with stringent quality standards. Meanwhile, hospitals are turning to laminar-flow aerators to reduce aerosolization, addressing critical hygiene and safety requirements in healthcare facilities.

Government office complexes are adopting low-flow faucets, seamlessly integrated into building-management systems for precise water budget monitoring. This integration not only supports sustainability goals but also enhances operational efficiency by providing real-time data on water usage. In Hyderabad, corporate campuses are embedding usage data into their ESG dashboards, showing a clear preference for brands that provide API-ready devices. This trend reflects the growing emphasis on environmental, social, and governance (ESG) considerations in corporate decision-making. While residential projects form the bedrock of India's faucet market, a strategic shift towards premium commercial kits is not only enhancing the average revenue per unit but also providing a buffer against material cost fluctuations. This mix improvement is expected to strengthen the market's resilience and profitability over the forecast period.

By Distribution Channel: B2B Dominance Faces Retail Challenge

In 2025, B2B and project sales accounted for a significant 70.44% of turnover, driven largely by bulk purchases for housing societies and civic infrastructure projects. Developers are locking in multi-year rate contracts, which play a pivotal role in shaping factory utilization plans. These contracts provide manufacturers with predictable demand, enabling better resource allocation and operational efficiency. Furthermore, direct supply agreements have become essential, especially highlighted during the pandemic, as they mitigate risks associated with distributor stock-outs. By bypassing intermediaries, companies ensure a steady supply chain, which is critical for meeting project deadlines and maintaining customer trust.

On the other hand, the retail sector is poised for growth, with a projected CAGR of 7.36%, largely attributed to innovative omnichannel strategies. In Bengaluru, flagship stores are introducing augmented-reality configurators, allowing customers to visualize products in real-time, which enhances the shopping experience and reduces decision-making time. Additionally, e-commerce platforms are enhancing their offerings by bundling installation services at checkout, effectively tackling the final-mile challenge and improving customer satisfaction. Despite the digital shift, regional hardware shops continue to dominate, moving half of the rural volume, thanks to their strong community connections and localized expertise. These shops remain a critical distribution channel, especially in areas where digital penetration is limited.

Geography Analysis

South India captured 34.12% of 2025 revenue, reflecting the proximity of faucet foundries in Chennai and Bengaluru that slash logistics overheads and speed prototype iterations. The cluster benefits from mature component ecosystems for gaskets, ceramic discs, and electroplating, letting regional OEMs release design refreshes every eight months. Consumer willingness to pay for premium matte-black finishes outstrips national averages, underpinning sustained showroom upgrades.

North India is on track for the strongest expansion, recording an 8.21% CAGR through 2031 as Delhi NCR’s township corridors absorb smart-city subsidies. Early Phase-I smart projects in Lucknow and Varanasi include sensor-faucet specifications that ripple into adjacent Tier-3 districts as aspirational benchmarks. Manufacturing investments in Haryana’s Kundli industrial belt foster supply-side depth, cutting lead times to high-rise construction sites.

West India draws upon Maharashtra’s auto parts metallurgy expertise and Gujarat’s brassware export heritage, serving both domestic and Middle-East orders. Mumbai’s water tariffs rose 10% in 2025, propelling low-flow retrofits across gated communities. Meanwhile, East India lags but shows green shoots: the Kolkata-Asansol corridor’s logistic parks attract migrant workers whose rising incomes feed into bathroom renovation cycles. State subsidies for SME foundries in Odisha encourage localized production that can shave freight costs by 7%, potentially redefining competitive equations within the India faucets market.

Competitive Landscape

In 2025, the top five organized vendors in India's faucets market are projected to command a combined share of approximately 42%. Jaquar, with a turnover of INR 7,493 crore (USD 909 million) for FY 2024-25, achieved this milestone on an annual output of 45.9 million units, showcasing the potential of merging vertical integration with brand equity. The company's strong performance highlights the importance of operational efficiency and brand positioning in driving growth. Meanwhile, Hindware and Cera are automating their factories, successfully reducing yield losses to under 1.5% on their high-volume plating lines, in their pursuit of market leadership. These advancements in automation not only enhance production efficiency but also improve product quality, enabling these brands to cater to the growing demand for premium faucets in India.

Strategic acquisitions are broadening product offerings: Prince Pipes' acquisition of Aquel allows them to combine piping with brassware, and Somany Ceramics' purchase of Schablona India integrates tiles with sanitaryware. These strategies create comprehensive portfolios that resonate with project specifiers, who often prefer single-source procurement. Such acquisitions also enable companies to expand their market presence and strengthen their competitive positioning. The competition extends to sensor modules; collaborations with Korean chipsets empower local brands with exclusive firmware, steering clear of open-source risks. This focus on proprietary technology not only enhances product security but also provides a competitive edge in the rapidly evolving smart faucets segment.

Regional players like Kerala-based Johnson Faucets thrive by servicing grey-market plumbers with 24-hour part delivery. Their ability to cater to niche markets with quick turnaround times has helped them maintain a strong foothold despite the challenges posed by larger organized players. GST compliance gaps are narrowing but still provide a haven for these smaller outfits in cash-heavy micro-markets. However, increasing enforcement and the adoption of e-invoicing are expected to pressure informal players, potentially driving market consolidation. To stay competitive, brands are leveraging influencer marketing through architecture-award tie-ins, signaling design leadership that appeals to premium buyers. This approach aligns with the ongoing premiumization of the India faucets market, where consumers are increasingly prioritizing aesthetics and functionality in their purchasing decisions.

India Faucet Industry Leaders

Jaquar Group

Hindware Home Innovation

Cera Sanitaryware

Kohler India

Grohe India (LIXIL)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cera Sanitaryware introduced the ‘Polipluz’ bathware collection to widen its domestic lineup.

- September 2024: HomeLane acquired Design Café via share-swap and raised INR 225 crore from Hero Enterprise and WestBridge Capital.

- March 2024: Apollo Pipes bought a 53.57% stake in Kisan Mouldings for INR 118.40 crore, enhancing PVC pipe reach in western and central India.

- February 2024: The Jaquar Group IPA Neerathon, held on February 4, 2024, at Major Dhyan Chand National Stadium, witnessed the outstanding participation of 1600+ sports enthusiasts, army personnel, corporate leaders, and first-time runners.

India Faucet Market Report Scope

A faucet is a device usually used for controlling the flow of liquid from a pipe. The most common type of faucet used is the different types of tap used in commercial as well as residential spaces. Rising technological innovations are leading to faucets equipped with sensors making automatic flow of water when in use.

The study gives a brief description of the Indian faucet market and includes details on types of faucets, investments by the manufacturers, and technological, product innovation by the manufacturers.

India's faucet market is segmented by product type, by technology, by installation, by material used, by application, by end-user, and by distribution channel. By product type, the market is segmented into ball, disc, cartridge, and compression. By technology, the market is segmented into manual and automatic. By installation, the market is segmented into deck mount and wall mount. By material, the market is segmented into chrome, stainless steel, brass, Polytetra Methylene Terephthalate (PTMT) Plastic, and other materials. By application, the market is segmented into kitchen faucets, bathroom faucets, and other applications. By end user, the market is segmented into residential and commercial. By distribution channel, the market is segmented into B2C/retail, multi-brand stores, exclusive stores, online, and B2B/Project (architect, interior designers, contractors, etc.).

The report also covers the market sizes and forecast for the Indian faucet market in value (USD) for all the above segments.

By Product Type

| Ball |

| Disc |

| Cartridge |

| Compression |

By Material

| Chrome |

| Stainless Steel |

| Brass |

| Polytetra Methylene Terephthalate (PTMT) Plastic |

| Other Materials |

By Technology

| Manual |

| Automatic |

By Installation Type

| Deck Mount |

| Wall Mount |

By Application Type

| Kitchen Sink Faucets |

| Bathroom Sink Faucets |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Local Hardware Stores | |

| B2B/Project |

By Region

| North India |

| South India |

| West India |

| East India |

| By Product Type | Ball | |

| Disc | ||

| Cartridge | ||

| Compression | ||

| By Material | Chrome | |

| Stainless Steel | ||

| Brass | ||

| Polytetra Methylene Terephthalate (PTMT) Plastic | ||

| Other Materials | ||

| By Technology | Manual | |

| Automatic | ||

| By Installation Type | Deck Mount | |

| Wall Mount | ||

| By Application Type | Kitchen Sink Faucets | |

| Bathroom Sink Faucets | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Local Hardware Stores | ||

| B2B/Project | ||

| By Region | North India | |

| South India | ||

| West India | ||

| East India | ||

Key Questions Answered in the Report

What is the current value of the India faucets market?

The India faucets market size stands at USD 1.89 billion in 2026 and is projected to grow steadily through 2031.

How fast will automatic sensor faucets grow?

Automatic variants are forecast to expand at an 8.04% CAGR thanks to falling sensor costs and hygiene regulations in commercial facilities.

Which region is the most lucrative for faucet vendors?

South India leads with 34.12% revenue share due to its manufacturing clusters and higher home-improvement spending.

Which product type dominates sales?

Cartridge faucets hold the biggest slice of 2025 revenue, capturing 69.78% of the India faucets market share.

How is e-commerce reshaping faucet distribution?

Online platforms enable direct brand access, transparent pricing, and bundled installation services, driving a 7.36% CAGR in retail-channel sales through 2031.

What raw-material risks affect faucet manufacturers?

Volatile copper and zinc prices squeeze brass faucet margins, encouraging some producers to pivot toward stainless-steel alternatives.

Page last updated on: