Glass Fiber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

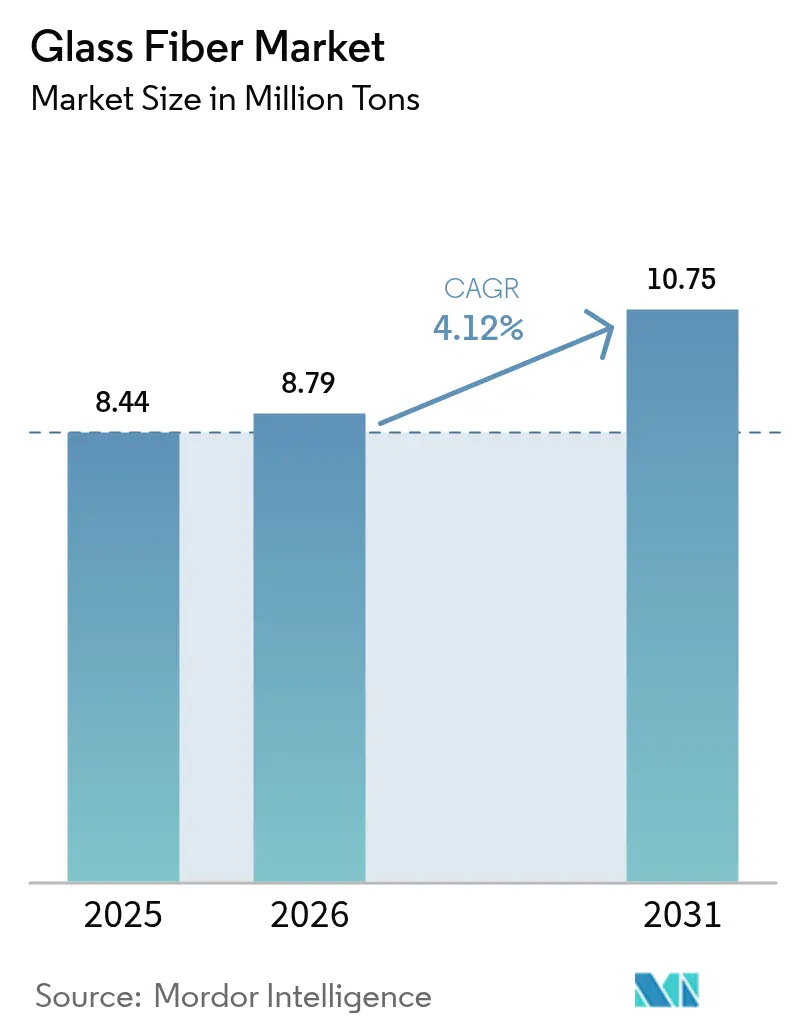

| Market Volume (2026) | 8.79 Million tons |

| Market Volume (2031) | 10.75 Million tons |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

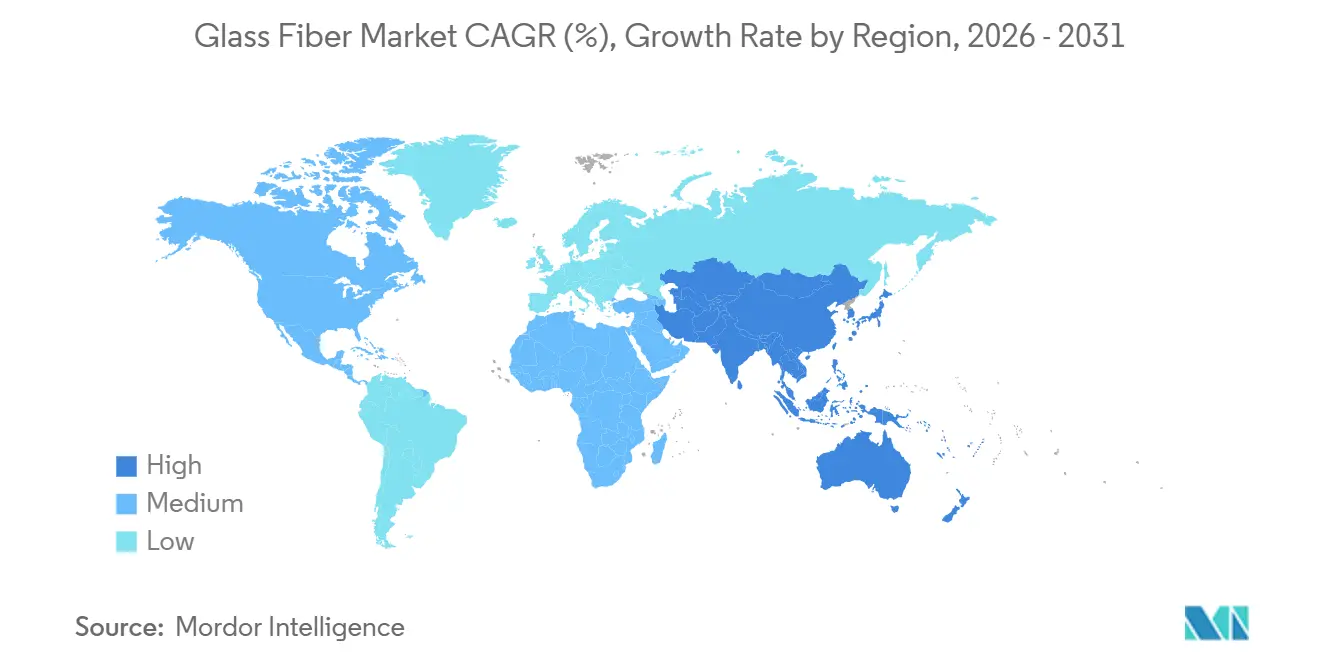

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Glass Fiber Market Analysis by Mordor Intelligence

The Glass Fiber Market size is expected to grow from 8.44 million tons in 2025 to 8.79 million tons in 2026 and is forecast to reach 10.75 million tons by 2031 at a 4.12% CAGR over 2026-2031. Demand is expanding in tandem with infrastructure spending across Asia-Pacific, the rapid scale-up of offshore wind projects, and accelerating electric-vehicle (EV) output that favors lightweight composite parts. In parallel, European and North American retrofit energy codes are lifting insulation volumes, while hydrogen pipeline projects introduce higher-value E-CR grades. Raw-material price swings and carbon-fiber cost deflation temper margins, yet the broad performance-to-cost advantage of glass fiber over metals or rival reinforcements underpins healthy capacity utilization. Competitive intensity remains moderate because the ten largest producers command less than one-third of global furnace capacity, which leaves headroom for regional specialists to capture niche opportunities.

Key Report Takeaways

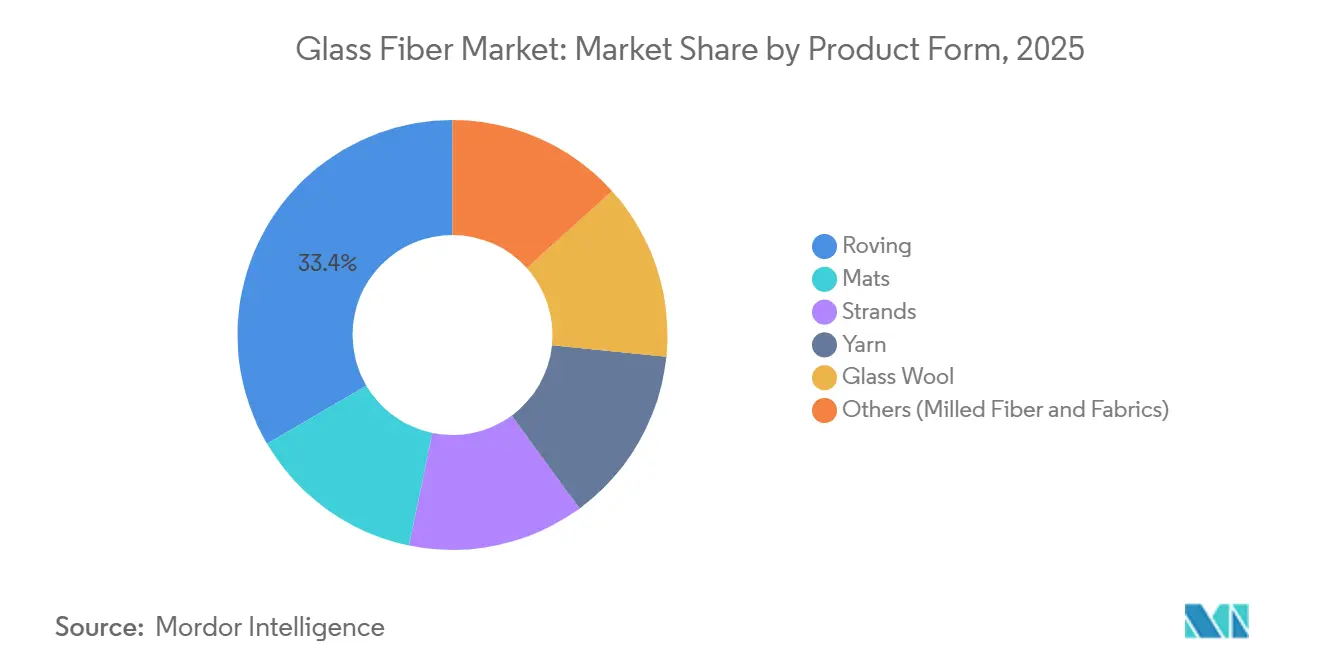

- By product form, roving led with 33.45% of the glass fiber market share in 2025, and is anticipated to expand at a 4.41% CAGR through 2031, the fastest among product categories.

- By fiber type, E-Glass accounted for 48.91% of the glass fiber market size in 2025 and is advancing at a 4.32% CAGR to 2031.

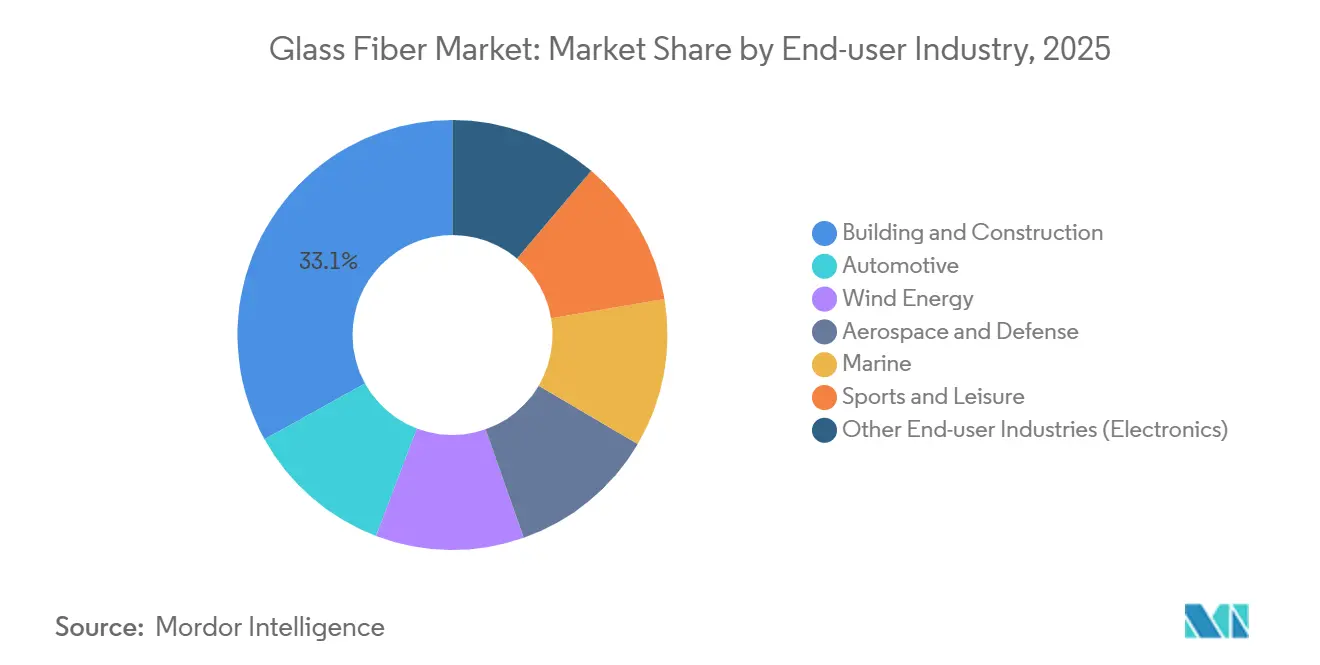

- By end-user industry, the construction industry accounted for the largest share of 33.07% in 2025. The aerospace and defense is projected to register a 5.55% CAGR between 2026 and 2031, outpacing construction and automotive.

- By geography, Asia-Pacific held 49.81% of the 2025 volume and will remain the fastest-growing region at a 4.57% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glass Fiber Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic construction boom in Asia bolsters demand for glass-wool insulation | +0.9% | India, Vietnam, Indonesia | Medium term (2–4 years) |

| EV lightweighting accelerates adoption of chopped-strand composites | +0.7% | China, United States, Germany | Medium term (2–4 years) |

| Mega-scale wind-turbine blades expand roving consumption | +0.8% | Europe, North America, Asia-Pacific | Long term (≥4 years) |

| EU and North-American retrofit energy codes mandate additional insulation | +0.6% | Europe, United States, Canada | Short term (≤2 years) |

| Hydrogen pipeline projects specify E-CR glass for chemical resistance | +0.5% | Europe, North America, Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Post-Pandemic Construction Boom in Asia Bolsters Demand for Glass-Wool Insulation

India allocated USD 120 billion to infrastructure in fiscal 2025, and nearly half of that spending went into residential projects where glass-wool batts are now required by the 2024 Energy Conservation Building Code[1]Ministry of Power, Government of India, “Energy Conservation Building Code 2024,” powermin.gov.in. Vietnam’s construction sector advanced 9.1% in 2025, with foreign-invested factories specifying clean-room insulation that relies on low-density glass wool. Indonesia earmarked IDR 410 trillion (USD 27 billion) for 2025 infrastructure, using glass-wool products that cut cooling loads by up to 35% in tropical housing. Malaysia and Thailand show parallel trends as data-center and cold-chain investors adopt higher R-value batts to meet ASHRAE 90.1 targets. Collectively, these programs keep Asia the anchor of glass fiber market growth.

EV Lightweighting Accelerates Adoption of Chopped-Strand Composites

Global battery-electric vehicle production hit 14.2 million units in 2025, a 19% jump over 2024 that propelled composite demand[2]International Energy Agency, “Global EV Outlook 2026,” iea.org. Tesla’s Model Y uses chopped-strand mat structures to trim body-in-white mass by 23%, translating into an 18 km range extension per charge. BYD, Volkswagen, and General Motors each validated glass-fiber-reinforced thermoplastics for battery trays, together saving more than USD 300 per vehicle against aluminum alternatives. As automakers push toward cost-parity EVs, volume contracts for chopped strands underpin a steady mid-single-digit rise in the glass fiber market.

Mega-Scale Wind-Turbine Blades Expand Roving Consumption

Offshore turbines rated 15–18 MW entered service in 2025, and each 120-plus-meter blade contains roughly 35 tons of unidirectional roving. Vestas’s V236-15 MW unit, Hollandse Kust West, and GE Vernova’s Haliade-X all specify European-sourced rovings to satisfy domestic-content rules under the EU Net-Zero Industry Act. China’s Goldwind deployed 18 MW machines that drive similar fiber intensities, lifting Asia’s share of global roving contracts. New blade factories in France, India, and the United States are signing multi-year offtake deals, locking in floor volumes for the glass fiber market through the next decade.

EU and North-American Retrofit Energy Codes Mandate Additional Insulation

The revised 2024 EU Energy Performance of Buildings Directive obliges member states to upgrade 3% of public buildings annually to class C, and most projects specify glass-wool cavity fills because of low installed cost and mature supply chains. Germany committed EUR 14 billion in 2025 subsidies that lifted attic-insulation installs by 420,000 homes, while France’s MaPrimeRénov’ financed 700,000 retrofits that favor glass wool for 35–40% heat-loss cuts. North America shows a parallel push: Canada’s Greener Homes Grant covered 180,000 projects in 2025, and the U.S. Weatherization Assistance Program reached 450,000 low-income homes, together absorbing more than 500 kilotons of glass wool. Tightening rules fast-track repeat orders, adding resilience to the glass fiber market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carbon-fiber price erosion narrows glass-fiber’s cost advantage | -0.5% | North America, Europe, Japan | Medium term (2–4 years) |

| Rock-wool producers target <100 kg/m³ HVAC niche | -0.2% | Europe, North America | Short term (≤2 years) |

| Volatile soda-ash and energy costs crimp Chinese furnace margins | -0.2% | Asia-Pacific, China | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Carbon-Fiber Price Erosion Narrows Glass-Fiber’s Cost Advantage

Toray, Mitsubishi Chemical, and SGL Carbon added a combined 9,500 tons of carbon-fiber nameplate capacity during 2025, pushing average prices down to USD 16.30 per kilogram. Automotive compounds now see a cost gap of only 2× versus glass-fiber polypropylene, compared with 2.4× in 2023. Sporting goods OEMs are piloting lower-cost shafts that could siphon mid-tier volumes away from E-Glass. Absent countermeasures, this trend trims the glass fiber market growth trajectory.

Rock-Wool Producers Target Less Than 100 kg/m³ HVAC Niche

Rockwool International launched a 90 kg/m³ board that hits R-4.2 per inch and carries Euroclass A1 fire certification, immediately winning share in German high-rise retrofits. Paroc and Knauf added similar offerings in 2025, and Owens Corning’s Thermafiber line gained a 12% share in North American data centers, sectors where combustibility ratings trump initial cost. These moves cap near-term growth for glass-wool batts in commercial HVAC retrofits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Roving Sustains Leadership on Wind and EV Momentum

Roving contributed 33.45% to 2025 volume and is on track for 4.41% CAGR through 2031, outpacing the broader glass fiber market because each 15 MW offshore turbine consumes 35 tons of unidirectional material. Mats follow, anchored in automotive underbody panels and marine laminates produced in low-cost Chinese and Turkish yards. Glass wool receives a tailwind from retrofit mandates across Europe and North America. Strands, yarns, and the “others” cluster supply printed-circuit boards, filtration textiles, and specialty adhesives, but direct-roving pultrusion is cannibalizing intermediate formats.

Roving’s installed base benefits from process improvements that cut cycle time in automotive compression molding to four minutes, half that of chopped-strand mats. Glass-wool producers are lowering binder content to 3%, improving R-value, and meeting VOC limits in California. Milled fiber remains a rheology modifier in sealants, whereas woven fabrics secure aerospace tooling demand. All told, diversified applications shield the glass fiber industry against single-segment swings.

By Fiber Type: E-Glass Dominates While E-CR Gains in Hydrogen Pipelines

E-Glass held 48.91% of volume in 2025 and is expanding at a CAGR of 4.32% through 2031, reinforced by a tensile strength of 3,400 MPa at a cost of USD 2.10 per kg. E-CR Glass, prized for alkali resistance, is scaling at double-digit rates within hydrogen-pipeline linings worth USD 150 million in 2025. S-Glass, commanding USD 23.40 per kg, captures high-performance aerospace niches. C-Glass is declining as E-CR delivers similar chemical durability at a lower total cost.

High-modulus E-Glass variants exceeding 90 GPa now allow blade designers to shave spar-cap thickness by 8–10%, preserving structural safety as rotor diameters crest 240 m. AR-Glass and D-Glass fill concrete reinforcement and low-dielectric roles, respectively. The diversified palette ensures that any substitution threat is segment-specific, leaving the broader glass fiber market intact.

By End-User Industry: Construction Leads, Aerospace Rises Fastest

Construction consumed 33.07% of 2025 tonnage owing to attic and cavity-wall insulation installs subsidized in Germany, France, and Canada. The consumption by the aerospace and defense industry is growing at a higher CAGR of 5.55% through 2031. Automotive ranked second as EV output hit 14.2 million units, each battery-tray switch from steel to polypropylene composites stripping out up to 25 kg of mass. Wind energy uses between 8–10 kg per installed megawatt, a ratio that scales with the offshore boom. Aerospace and defense grew 5.55% annually, driven by U.S. rotorcraft and European UAV programs that specify S-Glass radomes.

Marine, sports, and electronics provide steady mid-single-digit growth. Recreational boating registrations climbed 6% in 2025, lifting hull laminate demand. Carbon-fiber encroachment in premium sporting goods mainly affects the top segment, leaving cost-sensitive mid-tiers anchored to E-Glass. Printed-circuit board volumes ride 5G base-station deployments and hyperscale data-center expansions, both of which keep strand consumption buoyant.

Geography Analysis

Asia-Pacific dominated the glass fiber market with 49.81% of 2025 volume and is slated for a 4.57% CAGR to 2031. India alone absorbed 1.8 million tons, up 19% year-on-year, as developers met strengthened thermal codes. China produced 5.2 million tons but exported 38%, reflecting persistent overcapacity and aggressive outbound logistics. Vietnam’s 1.2 GW of 2025 wind builds needed 9,600 tons of roving, while Indonesia’s EV-motorcycle boom raised composite consumption in two-wheel battery enclosures.

North America accounted for a significant market share in 2025. The U.S. installed 12 GW of wind capacity under Inflation Reduction Act incentives, translating into 96,000 tons of roving demand. Canada’s Greener Homes Grant installed 180,000 retrofit kits dominated by glass wool, and Mexico produced 3.8 million vehicles using composites in 28% of units.

Europe accounted for significant glass fiber consumption in 2025, with Germany, France, and the U.K. making up 58%. Germany’s 420,000 home retrofits drew heavily on glass-wool batts, whereas France added 2.1 GW of wind that required 16,800 tons of roving. The U.K. saw automotive softness but aerospace upside as Airbus raised A320neo wing set output. South America and the Middle East-Africa together are witnessing the rising demand driven by Brazil’s 2.3 million-unit auto fleet and Saudi Arabia’s hydrogen pipelines that consume 12,000 tons of E-CR glass.

Competitive Landscape

The glass fiber market is moderately consolidated. China Jushi operates 2.1 million tons of capacity and commissioned a 600,000-ton Egyptian plant in September 2024 that trims freight cost to Europe and the Middle East by 15%. Owens Corning added 100,000 tons of U.S. roving output in 2024 to serve offshore wind farms planned for the Atlantic seaboard. Saint-Gobain’s Vetrotex division piloted an 85% fiber-recovery recycling line that tackles the looming blade-end-of-life issue.

Nippon Electric Glass is advancing ultra-thin strands under 5 µm for 224 Gbps circuit boards in AI accelerators, positioning for data-center mega-trends. Johns Manville locked in a decade-long natural-gas contract at USD 3.20 per MMBtu that shields U.S. furnaces from energy volatility. Emerging disruptors, notably Continuous Composites, are commercializing continuous-fiber 3D printing that could localize tool fabrication and reduce fiber waste. The sector’s innovation emphasis centers on energy efficiency, closed-loop recycling, and high-modulus chemistries, reinforcing competitive moats amid moderate concentration.

Glass Fiber Industry Leaders

-

Johns Manville

-

China Jushi Co., Ltd.

-

Saint-Gobain

-

Nippon Electric Glass Co., Ltd.

-

Taishan Fiberglass Inc.(CTG)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Nippon Electric Glass debuted sub-5 µm E-Glass strands for high-speed PCB laminates in AI servers.

- September 2024: China Jushi inaugurated a 600,000-ton line in Ain Sokhna, Egypt, aimed at European and Middle Eastern customers.

Global Glass Fiber Market Report Scope

Glass fiber, or fiberglass, is made of fine glass strands and is widely used for its strength, lightweight, and corrosion resistance. It is integral to industries like construction, automotive, aerospace, marine, electronics, and telecommunications, serving applications such as insulation, composites, reinforcements, and optical fibers.

The glass fiber market is segmented by product form, fiber type, end-user industry, and geography. By product form, the market is segmented into roving, mats, strands, yarn, glass wool, and others (milled fiber and fabrics). By fiber type, the market is segmented into E-glass, S-glass, E-CR glass, C-glass, and others. By end-user industry, the market is segmented into building and construction, automotive, wind energy, aerospace and defense, marine, sports and leisure, and other end-user industries (electronics). The report also covers the market size and forecasts for the glass fiber market in 27 countries across major regions. For each segment, the market sizing and forecast have been done on the basis of volume (tons).

| Roving |

| Mats |

| Strands |

| Yarn |

| Glass Wool |

| Others (Milled Fiber and Fabrics) |

| E-Glass |

| S-Glass |

| E-CR Glass |

| C-Glass |

| Others |

| Building and Construction |

| Automotive |

| Wind Energy |

| Aerospace and Defense |

| Marine |

| Sports and Leisure |

| Other End-user Industries (Electronics) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Vietnam | |

| Malaysia | |

| Thailand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Turkey | |

| Nordics | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Product Form | Roving | |

| Mats | ||

| Strands | ||

| Yarn | ||

| Glass Wool | ||

| Others (Milled Fiber and Fabrics) | ||

| By Fiber Type | E-Glass | |

| S-Glass | ||

| E-CR Glass | ||

| C-Glass | ||

| Others | ||

| By End-user Industry | Building and Construction | |

| Automotive | ||

| Wind Energy | ||

| Aerospace and Defense | ||

| Marine | ||

| Sports and Leisure | ||

| Other End-user Industries (Electronics) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Vietnam | ||

| Malaysia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Turkey | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the glass fiber market be by 2031?

It is forecast to reach 10.75 million tons by 2031, growing at a 4.12% CAGR over 2026–2031.

Which segment holds the highest glass fiber market share today?

Roving leads with 33.45% of 2025 global volume, supported by wind-turbine blade demand.

What is driving glass fiber adoption in electric vehicles?

Automakers use chopped-strand and roving composites to cut battery-enclosure mass by 20–25%, extending driving range without extra cells.

Why is E-CR glass gaining momentum?

Hydrogen pipelines require alkali-resistant reinforcement, and E-CR glass prevents stress-corrosion cracking at 100 bar operating pressure.

Which region is expanding fastest in the glass fiber market?

Asia-Pacific is growing at a 4.57% CAGR, fueled by construction booms in India, Vietnam, and Indonesia.

Are sustainability initiatives changing supply dynamics?

Yes, blade-recycling pilots, energy-efficient furnaces, and bio-based sizing agents are becoming supplier selection criteria for OEMs.

Page last updated on: