India Engineering Research And Development (ER&D) Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

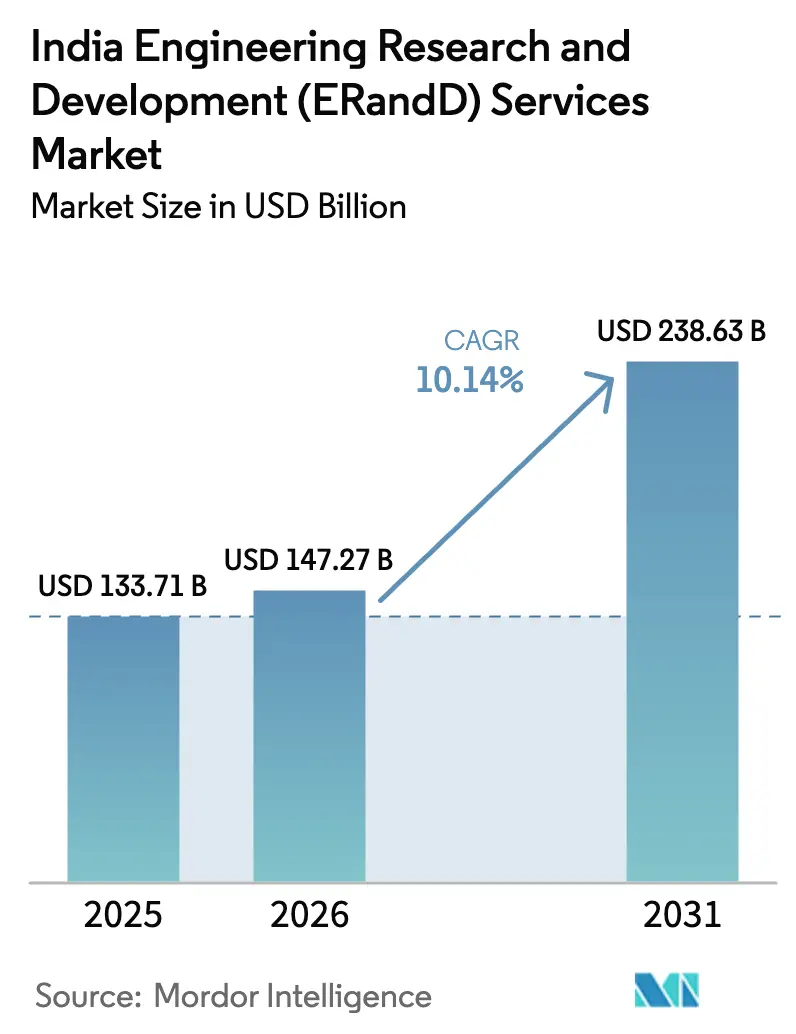

| Base Year Market Size (2025) | USD 133.71 Billion |

| Market Size (2026) | USD 147.27 Billion |

| Market Size (2031) | USD 238.63 Billion |

| Growth Rate (2026 - 2031) | 10.14% CAGR |

| Market Concentration | Low |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Engineering Research And Development (ER&D) Services Market Analysis by Mordor Intelligence

The India engineering research and development (ER&D) services market size was valued at USD 133.71 billion in 2025 and estimated to grow from USD 147.27 billion in 2026 to reach USD 238.63 billion by 2031, at a CAGR of 10.14% during the forecast period (2026-2031). Rising semiconductor self-reliance targets, the shift of global capability centres (GCCs) from cost to product ownership, and expanding digital-engineering demand from electric-vehicle (EV) programs are amplifying growth. Government production-linked incentives worth USD 24 billion for chipmaking, the world’s third-largest such package, are accelerating investments across design, validation, and assembly value-chain activities. Indian providers are simultaneously scaling AI-enabled design automation and digital-twin toolchains that compress development cycles for global original-equipment manufacturers (OEMs). Intensifying competition between diversified IT majors and focused engineering firms is spurring M&A, niche lab build-outs, and deep domain hiring, while policy support for defense offsets creates fresh aero-R&D mandates.

Key Report Takeaways

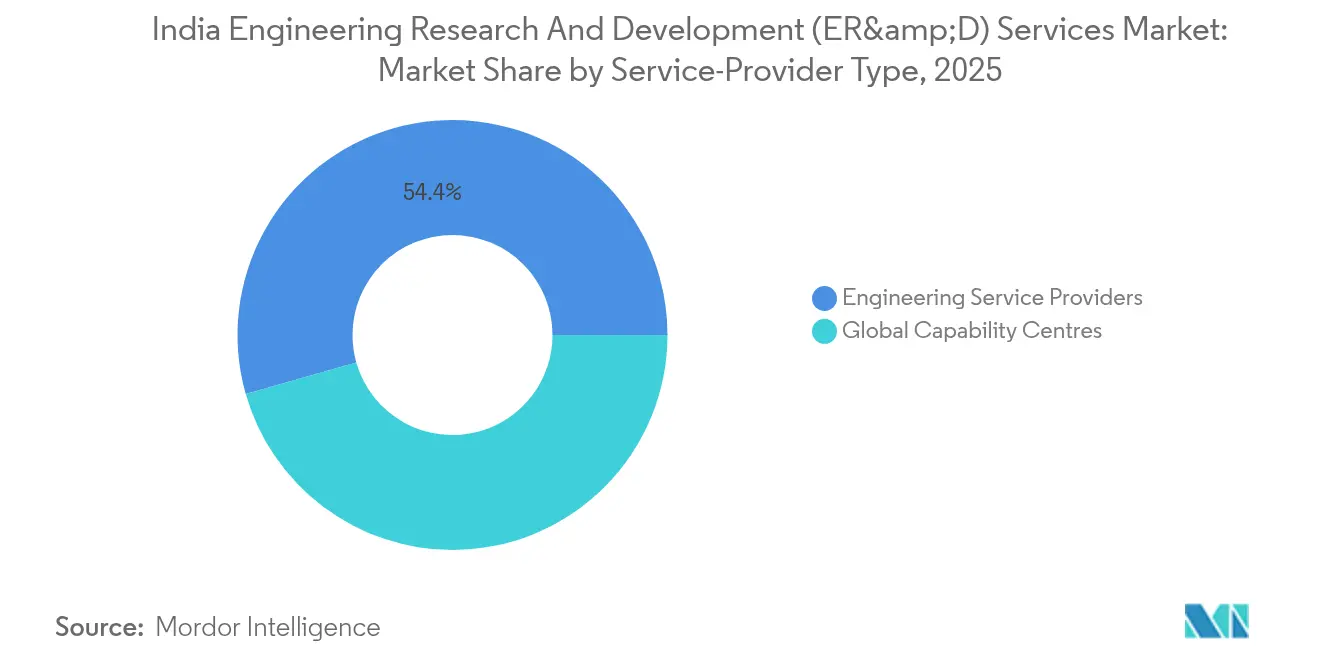

- By service-provider type, engineering service providers held 54.42% of the India engineering research and development (ER&D) services market share in 2025; GCCs are advancing at a 12.62% CAGR through 2031.

- By industry vertical, automotive led with 28.10% revenue share of the India engineering research and development (ER&D) services market in 2025, while semiconductor and electronics is projected to expand at a 12.85% CAGR to 2031.

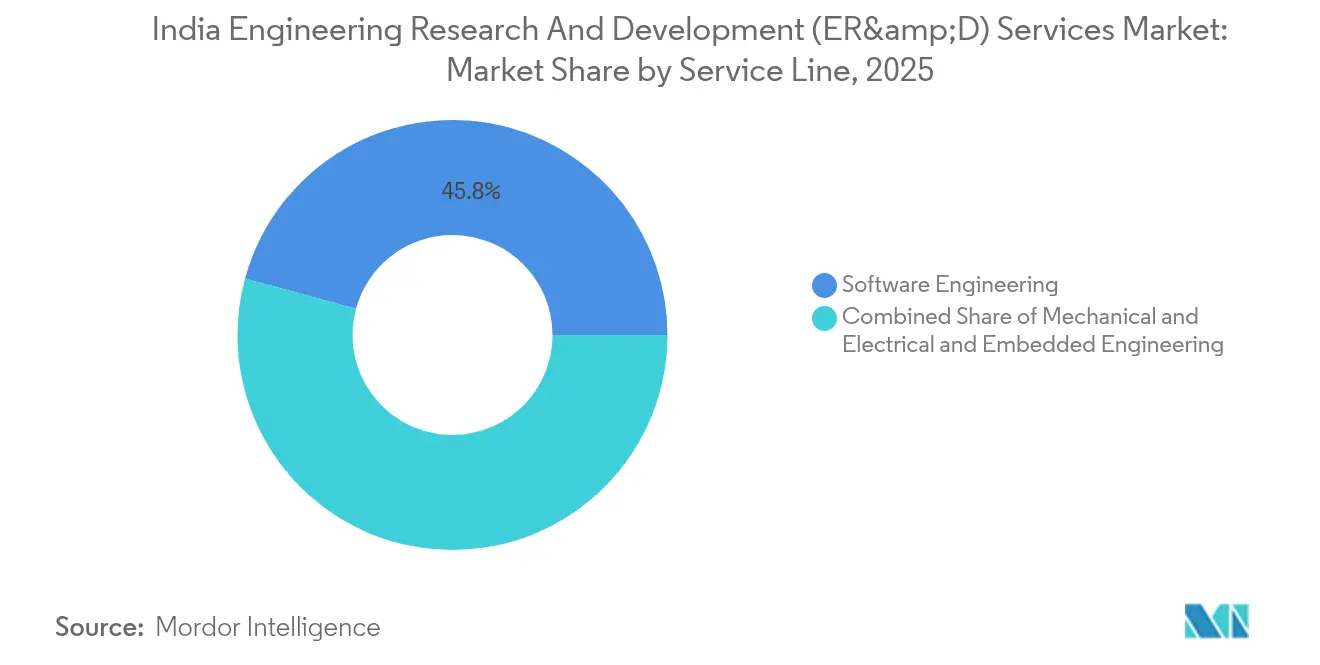

- By service line, software engineering accounted for 45.76% of the India engineering research and development (ER&D) services market size in 2025; embedded engineering shows the fastest 13.05% CAGR for 2026-2031.

- By the engineering phase, maintenance and sustenance commanded 12.31% CAGR between 2026-2031, the highest among all lifecycle phases of the India engineering research and development (ER&D) services market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Engineering Research And Development (ER&D) Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acceleration of global digital-engineering outsourcing | 2.10% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Cost advantage vs. on-shore ERandD centers | 1.80% | Global, particularly North America and Western Europe | Long term (≥ 4 years) |

| Rapid growth of domestic EV and mobility RandD | 1.50% | India-focused with spillover to ASEAN markets | Short term (≤ 2 years) |

| GCC expansion into product and platform ownership | 1.40% | India with global delivery model | Medium term (2-4 years) |

| Defence offset policy driving aero-RandD localisation | 0.90% | India-centric with export potential | Long term (≥ 4 years) |

| Semiconductor incentive scheme fuelling chip-design hubs | 1.20% | India with global semiconductor value chain integration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acceleration of global digital-engineering outsourcing

Global OEMs now embed software content that is poised to exceed 40% of vehicle value by 2030, prompting increased offshore model-based development, AUTOSAR integration, and AI-assisted design to India engineering research and development (ER&D) services market providers.[1]Embitel Technologies, “Customer Success Stories,” embitel.com Embitel Technologies extended into end-to-end ASIC programs while OMRON and Cognizant illustrated IT-OT convergence by co-building predictive manufacturing stacks, underscoring a dissolving boundary between mechanical, embedded, and cloud engineering.[2]Manufacturing Today India, “OMRON and Cognizant partner for IT-OT integration,” manufacturingtodayindia.com The India engineering research and development (ER&D) services market thereby captures a growing share of integrated product mandates that formerly required multiple vendors.

Cost advantage vs. onshore ER&D centers

Indian delivery can lower total engineering spend by 40-60% compared with Western sites, a gap widened by the shift-left approach at the Tata Elxsi and NI Mobility Innovation Centre that moves validation to earlier design stages.[3]Tata Elxsi, “Mobility Innovation Centre Launch,” tataelxsi.com Sumitomo Corporation’s JV with Tech Mahindra channels Japan’s crash-simulation workloads to a 6,000-engineer Indian pool, balancing Japanese quality with Indian efficiency.[4]Sumitomo Corporation, “Engineer Shortage JV Announcement,” sumitomocorp.com With global automotive ER&D outlays predicted to surpass USD 460 billion by 2030, this structural edge sustains the India engineering research and development (ER&D) services market’s scale runway.

Rapid growth of domestic EV and mobility R&D

Tesla’s alignment with Micron and Tata Electronics for legacy-node EV chips highlights India’s pivot from import dependence to indigenous design ecosystems that feed both domestic and export EV platforms. BMW-Tata Technologies and Mahindra-Qualcomm alliances deepen local power-electronics know-how, while RRP Semiconductor’s ASIC IP acquisition projects a USD 100 million automotive chip opportunity within two years. These dynamics reinforce the India engineering research and development (ER&D) services market as a competitive alternative to China-centric supply chains.

GCC expansion into product and platform ownership

Global capability centres are redeploying Indian teams from cost-optimized execution to full product road-map control. Caterpillar’s Bengaluru engineering center logged 450 patent filings, evidencing how GCCs deliver autonomous machine platforms that influence global profit pools. The India engineering research and development (ER&D) services market thus evolves toward higher-value innovation rather than transactional outsourcing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent attrition and wage inflation | -1.60% | India-wide with acute impact in Tier-1 cities | Short term (≤ 2 years) |

| Data-security and IP concerns among foreign OEMs | -1.20% | Global clients with India operations | Medium term (2-4 years) |

| Patchy Tier-2 city infrastructure for complex testing | -0.80% | India Tier-2 cities with expansion ambitions | Long term (≥ 4 years) |

| Client hesitancy over Gen-AI explainability in regulated verticals | -0.70% | Global, particularly in automotive and aerospace | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent attrition and wage inflation

Specialized ER&D skills remain scarce even as overall IT churn moderates, pushing providers to absorb higher salary bands and margin pressure. The semiconductor segment alone needs 85,000 additional engineers by 2032, demanding rapid skilling programs by IESA and AICTE. Tessolve’s USD 45.7 million buyout of Dream Chip Technologies tapped European talent to diversify resource pools, underlining how the India engineering research and development (ER&D) services market must pursue global hiring to sustain delivery.

Data-security and IP concerns among foreign OEMs

OEMs outsourcing autonomous-driving algorithms or ASIC road maps weigh India cost gains against IP risk. Cognizant mitigated this by operating a Gentherm-only Hyderabad center certified to ISO 27001 that ring-fences thermal-management software IP. Strengthening cyber-governance remains essential for long-cycle projects in the India engineering research and development (ER&D) services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service-Provider Type: GCCs recalibrate innovation mandates

The India engineering research and development (ER&D) services market size attributed to engineering service providers amounted to USD 72.78 billion in 2025, equal to 54.42% market share. GCCs generated the remainder yet are projected to compound at 12.62% through 2031, outpacing ESPs whose growth moderates to single digits. ESPs advance by blending domain reach with inorganic capability buys, illustrated by LTTS clinching a EUR 50 million multi-year engagement on micro-mobility platforms. GCCs such as Caterpillar’s 3,200-engineer unit prove Indian centers can steward patentable core IP. Consequently, clients are re-balancing portfolios to harness GCC strategic tightness and ESP execution breadth, a hybrid that redefines commercial models across the India engineering research and development (ER&D) services market.

In the medium term, ESPs will retain large-scale testing, prototyping, and compliance documentation where process maturity trumps invention. GCCs, backed by parent-company capex, will pilot autonomous machines, silicon photonics, and software-defined vehicles from India. As both archetypes embed AI-native toolchains, competitive boundaries blur, raising the likelihood of joint ventures between prime ESPs and captive GCC labs to accelerate platform acceleration.

By Industry Vertical: Semiconductor acceleration disrupts automotive primacy

The India engineering research and development (ER&D) services market share for automotive remained dominant at 28.10% in 2025, backed by ADAS calibration and e-powertrain programs. However, semiconductor and electronics are forecast to add USD 27 billion incremental value and log the fastest 12.85% CAGR through 2031. Domestic chip design incentives and partnerships, such as NXP’s USD 1 billion expansion, ignite design-for-manufacture flows that crisscross consumer, industrial, and mobility applications.

While industrial, transportation, construction, and heavy machinery (ITCHM) verticals exploit infrastructure mega-projects and Industry 4.0 retrofits, services-led verticals like BFSI and healthcare lean on secure software platforms and myriad IoT-enabled medical devices. Cross-learning rises automotive ADAS imaging IP now re-targets smart-city surveillance ASICs, and EV battery-management algorithms feed industrial robotics voltage control. Such adjacencies multiply addressable opportunities for the India engineering research and development (ER&D) services market beyond siloed vertical definitions.

By Service Line: Embedded momentum complements software scale

Software engineering represented 45.76% of the India engineering research and development (ER&D) services market size in 2025, anchored by model-based development, DevSecOps, and cloud-native control software. Embedded engineering is projected to outperform, expanding at a 13.05% CAGR on IoT proliferation and autonomy requirements. Ten-microcontroller ECUs are collapsing into single-domain controllers, demanding high-density board design, silicon validation, and firmware integration—capabilities Indian labs now field. Mechanical and electrical engineering persist yet increasingly integrate digital twins that cut mean-time-to-prototype by 30%, reinforcing the service-line convergence narrative pivotal to the India engineering research and development (ER&D) services market.

Growth also springs from new safety and cybersecurity mandates: ISO 21434-aligned penetration testing, ASPICE level 3 assessments, and functional-safety audits expand wallet share for embedded experts. Providers cross-train talent on MISRA-C, Rust, and model-checking to future-proof skills against rising quality thresholds.

By Engineering Phase: Lifecycle services move upstream into sustenance

Development and prototyping held a 39.95% share in 2025 as enterprises prioritized speed-to-concept. Yet maintenance and sustenance climb fastest, posting a 12.31% CAGR, because OEMs increasingly retain India teams for over-the-air (OTA) software update engineering and multi-generation platform cost-down exercises. The India engineering research and development (ER&D) services market thus tilts toward annuity-style engagements that merge DevOps with field-data analytics.

Testing and validation gains from stricter homologation regimes: Euro NCAP 2030 protocols and Bharat NCAP star ratings drive demand for simulation-rich validation that halves physical-crash dependency. Concept and design stages benefit from virtual-reality ideation studios and generative AI that outputs first-pass CAD in hours, not weeks, yet these efficiencies loop into maintenance contracts as providers track digital-twin field data to improve future iterations.

Geography Analysis

The India engineering research and development (ER&D) services market remains concentrated in Tier-1 hubs, yet regional specialization deepens. Bengaluru anchors automotive, aerospace, and semiconductor co-design owing to critical-mass OEM presence and the Tata Elxsi-NI mobility lab that offers hardware-in-loop benches and EV drivetrain dynos. Chennai and Pune complement with metal-cutting and drivetrain competencies linked to proximate manufacturing plants. Hyderabad’s surge in chip design, catalysed by Renesas and NXP expansions, signals an emerging silicon corridor that benefits from the state’s fab-cluster policy. Delhi NCR hosts avionics and cybersecurity GCCs servicing global airlines and defense primes, leveraging proximity to policymakers. Gujarat stakes a claim in assembly-test-mark-pack (ATMP) via the Dholera fab site, while Assam’s electronics PLI zone pilots cluster incentives for consumer components. Tier-2 cities such as Coimbatore provide value engineering and documentation tasks but require upgraded 10-gigabit networks and climatic chambers to host full-scale validation. Balanced regional growth is therefore contingent on targeted infrastructure outlays that enlarge the India engineering research and development (ER&D) services market without diluting quality benchmarks.

Competitive Landscape

Competition in the India engineering research and development (ER&D) services market is moderate-to-high. TCS, HCL, and Infosys leverage multi-vertical scale and enterprise relationships to win bundled engineering-plus-IT deals. Pure-play firms LTTS, Cyient, and Tata Elxsi counter with domain focus—LTTS recently secured a next-generation micro-mobility platform, Cyient reinforced aerospace wire-harness design, and Tata Elxsi embedded ADAS IP in EV prototypes. Strategic M&A underpins capability gaps: Tessolve’s acquisition of Dream Chip accelerated European imaging ASIC expertise, while KPIT bought PathPartner assets to broaden camera perception stacks.

Digital twin, AI-driven simulation, and cloud native PLM define table stakes. Providers invest in Gen-AI assistants for code review and BOM optimization, yet regulated clients temper adoption pending explainability assurances. First movers who operationalize AI responsibly stand to capture wallet share. White-space opportunities in quantum-safe cryptography, green hydrogen plant design, and sustainable materials research remain under-addressed, inviting niche entrants. The market’s evolution, therefore, hinges on continuous capability refresh as providers race to secure and expand positions across the India engineering research and development (ER&D) services market.

India Engineering Research And Development (ER&D) Services Industry Leaders

HCL

Infosys

L&T Technology Services

Tata Technologies

Wipro

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: RRP Semiconductor entered the fabless domain via an ASIC IP transfer targeting automotive silicon, opening a USD 25-100 million revenue window.

- February 2025: TCS assumed control of General Motors’ India engineering center, integrating 1,300 employees across propulsion and vehicle controls.

- November 2024: Tessolve agreed to acquire Dream Chip Technologies for EUR 42.5 million, adding ADAS imaging labs and European delivery hubs.

- July 2024: Tata Elxsi and Emerson launched the Bengaluru Mobility Innovation Centre, focusing on autonomous and EV R&D.

India Engineering Research And Development (ER&D) Services Market Report Scope

ER&D Services encompass a range of offerings tailored to enterprises, focusing on the design and development of various products, from devices and equipment to platforms and applications. These services pave the way for the eventual sale of the product, whether through software development or traditional manufacturing. The ER&D spectrum typically includes software, embedded, and mechanical engineering services, delineating the diverse expertise involved.

The Indian engineering research and development (ER&D) services market is segmented by service provider type (global capability centers (GCCs), engineering service providers (ESPs)), by industry vertical (automotive, industrial and transportation, construction, and heavy machinery (TCHM), hi-tech-led verticals (software and internet, semiconductor, telecom, etc.), services-led verticals (BFSI), healthcare, etc.) by service line (mechanical and electrical engineering services, embedded, engineering services, software engineering services), by geography (tier 1 cities, tier 2 cities, rest of India). The market sizes and forecasts are provided in terms of value (USD) for the above segment.

| Hardware |

| Software |

| Services |

| Cellular IoT (2G/4G/5G) |

| LPWAN (NB-IoT, LoRa, Sigfox) |

| Short-Range (Wi-Fi/Bluetooth/Zigbee) |

| Satellite-based IoT |

| Smart Cities |

| Industrial IoT |

| Consumer IoT |

| Automotive IoT |

| Healthcare IoT |

| Others |

| Manufacturing |

| Transportation and Logistics |

| Energy and Utilities |

| Agriculture |

| Retail and Smart Buildings |

| By Component | Hardware |

| Software | |

| Services | |

| By Connectivity Technology | Cellular IoT (2G/4G/5G) |

| LPWAN (NB-IoT, LoRa, Sigfox) | |

| Short-Range (Wi-Fi/Bluetooth/Zigbee) | |

| Satellite-based IoT | |

| By Application | Smart Cities |

| Industrial IoT | |

| Consumer IoT | |

| Automotive IoT | |

| Healthcare IoT | |

| Others | |

| By End-User Industry | Manufacturing |

| Transportation and Logistics | |

| Energy and Utilities | |

| Agriculture | |

| Retail and Smart Buildings |

Key Questions Answered in the Report

What is the current value of India engineering research and development (ER&D) services and how fast is it expanding?

The segment stands at USD 147.27 billion in 2026 and is forecast to grow at a 10.14% CAGR to reach USD 238.63 billion by 2031.

Which service-provider category is showing the strongest momentum?

Global capability centres (GCCs) are advancing at a 12.62% CAGR, outpacing engineering service providers that currently hold the larger share.

How large is the semiconductor and electronics opportunity in India's ER&D landscape?

Semiconductor and electronics programs are projected to post a 12.85% CAGR through 2031, adding roughly USD 27 billion in incremental value.

What operational headwinds are executives watching most closely?

Persistent talent attrition and wage inflation could shave 1.6 percentage points off forecast growth unless firms bolster retention and global hiring.

How do government incentives support domestic chip-design capacity?

A USD 24 billion production-linked incentive scheme funds fabless subsidies and advanced-node assembly lines, drawing commitments such as NXPs USD 1 billion R&D expansion.

What strategic moves distinguish leading ER&D providers?

Leaders are pairing AI-driven design automation with acquisitions examples include TCS absorbing GMs India engineering unit and Tessolve buying Germanys Dream Chip Technologiesto scale high-value mandates.

Page last updated on: