India Data Center Physical Security Market Size and Share

Market Overview

| Study Period | 2020 - 2032 |

|---|---|

| Forecast Data Period | 2026 - 2032 |

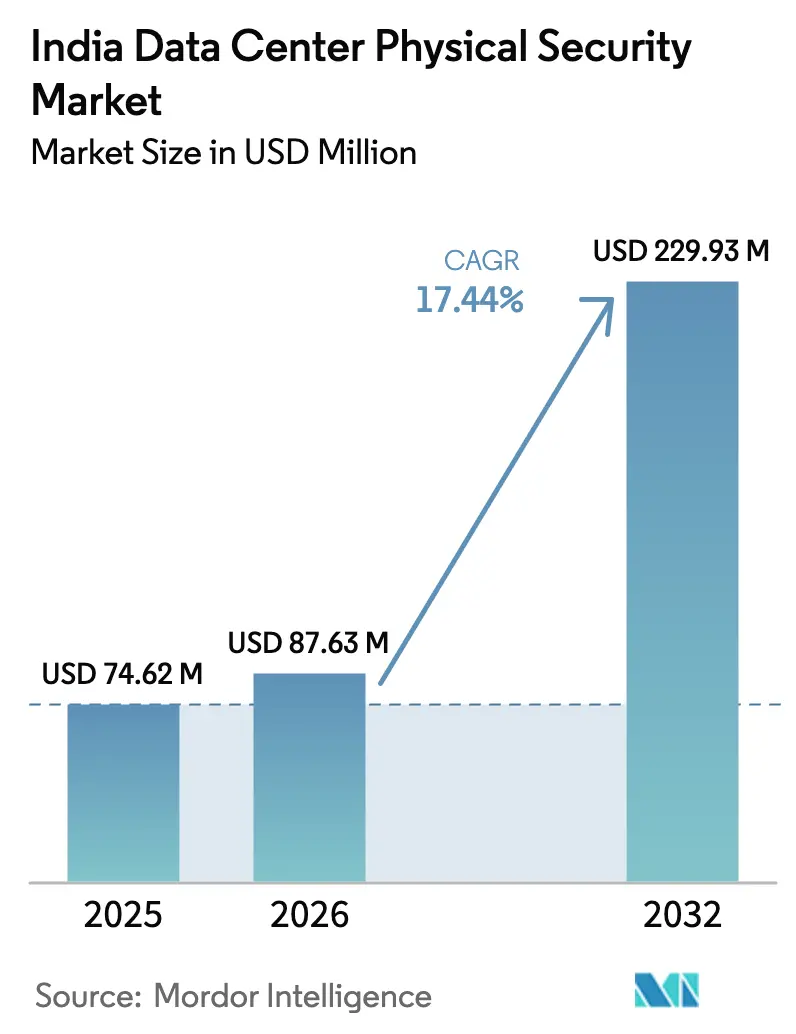

| Base Year Market Size (2025) | USD 74.62 Million |

| Market Size (2026) | USD 87.63 Million |

| Market Size (2032) | USD 229.93 Million |

| Growth Rate (2026 - 2032) | 17.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Data Center Physical Security Market Analysis by Mordor Intelligence

India data center physical security market size in 2026 is estimated at USD 87.63 million, growing from 2025 value of USD 74.62 million with 2032 projections showing USD 229.93 million, growing at 17.44% CAGR over 2026-2032. Expansion reflects the nation’s rapid digitalization, stricter data-localization rules, and the surge in hyperscale as well as edge facilities that require robust on-premises protection. Operators are prioritizing AI-enabled video analytics, biometric access control, and converged cyber-physical platforms to satisfy compliance under the Digital Personal Data Protection Act and upcoming CCTV safety norms. At the same time, incentives such as lower insurance premiums for certified sites are easing budget concerns for mid-tier builds. The India data center physical security market is also benefiting from local manufacturing of cameras and controllers, which helps reduce import duties and accelerates deployment.

Key Report Takeaways

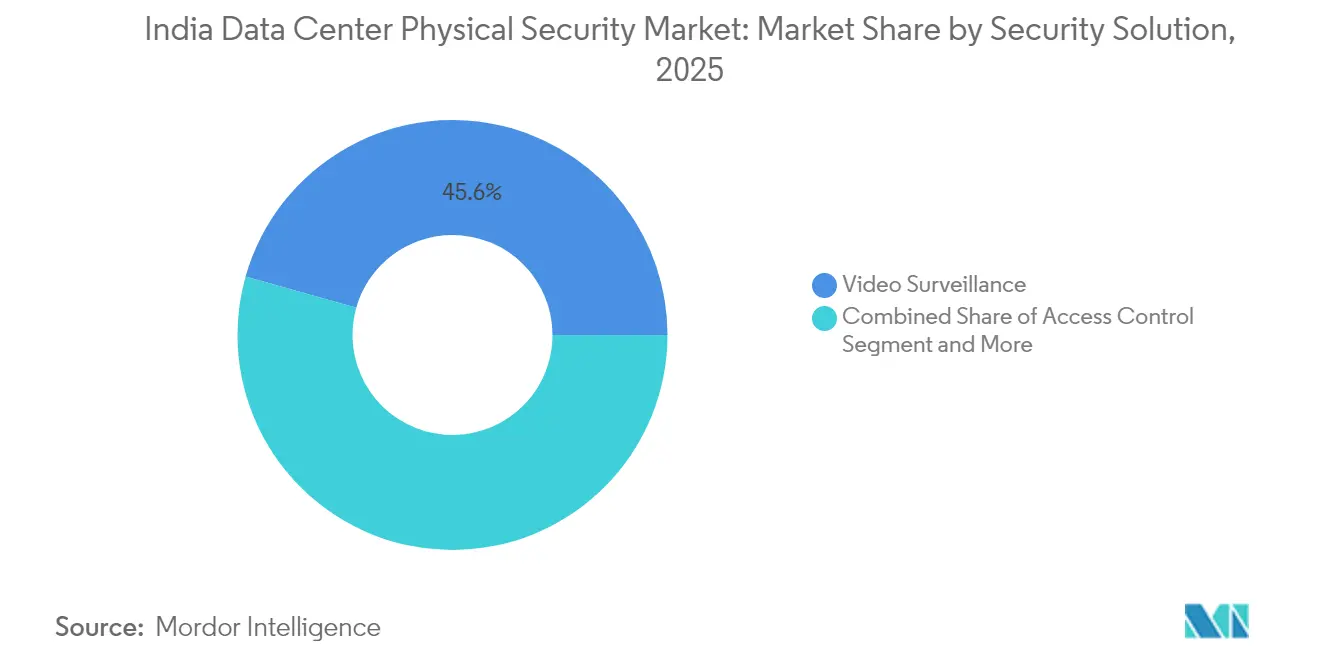

- By security solution, video surveillance led with 45.62% of the India data center physical security market share in 2025; intrusion detection and perimeter security is projected to post a 17.72% CAGR through 2032.

- By service, managed services posted the quickest growth at an 18.11% CAGR between 2025 and 2032 in the India data center physical security market.

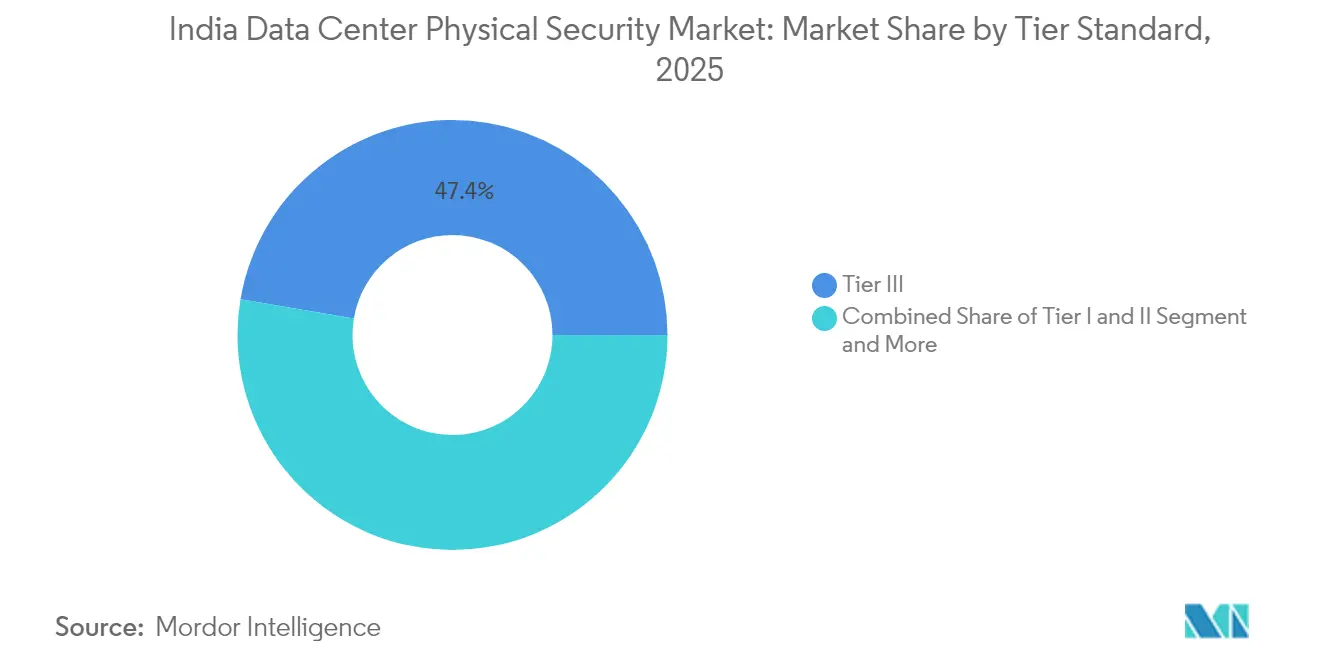

- By tier standard, Tier III facilities captured 47.35% of 2025 revenue in the India data center physical security market; edge and micro sites are forecast to rise at a 17.46% CAGR to 2032.

- By data center size, hyperscale campuses commanded 50.28% of the 2025 India data center physical security market size, while edge-scale hyperscale deployments are expected to increase at a 17.78% CAGR to 2032.

- By end-user industry, IT and telecommunications contributed 38.42% of 2025 demand in the India data center physical security market; e-commerce and retail is the fastest-expanding user group at 17.63% CAGR to 2032.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India participates in a competitive field that extends beyond its own borders. The market landscape in the global data center physical security industry outlined by Mordor Intelligence covers that wider structure.

India Data Center Physical Security Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in data traffic and cloud adoption | +1.8% | National with Mumbai and Chennai leading | Medium term (2-4 years) |

| Rising cyber and physical breach incidents | +1.2% | National, concentrated in financial hubs | Short term (≤ 2 years) |

| Expansion of hyperscale and colocation sites | +1.5% | Tier-1 cities expanding to Tier-2/3 | Long term (≥ 4 years) |

| Digital-India and data-localization mandates | +1.3% | National implementation | Medium term (2-4 years) |

| Edge DC growth in Tier-2/3 cities | +0.9% | Tier-2/3 cities nationwide | Long term (≥ 4 years) |

| Insurance-linked incentives | +0.3% | National with state-specific variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Data Traffic and Cloud Adoption

India’s data demand now outpaces available server capacity, pushing operators to build new sites secured by layered surveillance and biometric gates. Cloud providers that plan multi-billion-dollar campuses are specifying integrated AI video analytics to filter vast camera feeds in real time, while high-density racks require environmental sensors tied to the same command platform.[1]Bharti Airtel, “Nxtra by Airtel Becomes First Data Centre in India to Deploy AI for Enhanced Operational Excellence,” airtel. in These investments lift the India data center physical security market by broadening the addressable base from hyperscale players to smaller regional hosts.

Rising Cyber and Physical Breach Incidents

High-profile events such as the Star Health customer data leak sparked urgent reviews of physical access policies, steering enterprises toward zero-trust site designs that authenticate every entry and exit.[2]Press Information Bureau, “Government Taking Measures to Protect Critical Infrastructure and Private Data Against Cyber Attacks,” pib.gov.in Healthcare, financial services, and government users now insist on continuous surveillance, multi-factor authentication, and tamper-proof audit trails before awarding colocation contracts. The resulting uplift in demand reinforces steady growth in the India data center physical security market.

Expansion of Hyperscale and Colocation Facilities

Planned 3 GW campuses and multi-city colocation rollouts require standardized but scalable security blueprints. Operators procure perimeter radars, mantrap vestibules, and centralized security-information management systems that handle thousands of badge events per second.[3]EdgeConneX, “AdaniConneX Hyderabad Site Gets Five-Star Grading,” edgeconnex.com As projects spread to Tier-2 locations, suppliers with modular, prefabricated guard pods gain traction within the India data center physical security market.

Digital-India and Data-Localization Mandates

Regulations mandating domestic data processing mean more on-shore data halls that must prove compliance with physical-security clauses on controlled entry, 24 × 7 CCTV, and tamper-evident storage. Mandatory annual audits under the RBI and upcoming Digital India Act have made certification coverage a purchasing criterion, expanding the India data center physical security market into audit support and documentation software.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High CAPEX for advanced security systems | –0.8% | National, more acute in Tier-2/3 cities | Short term (≤ 2 years) |

| Grey-market low-cost surveillance products | –0.5% | National, price-sensitive segments | Medium term (2-4 years) |

| Shortage of skilled security engineers | –0.6% | National, especially in emerging hubs | Long term (≥ 4 years) |

| Import duties on advanced hardware | –0.4% | National, impacts foreign technology flows | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Advanced Security Systems

Deploying AI cameras, biometric turnstiles, and redundant monitoring rooms can add 8–12% to total build cost. Smaller operators weigh these outlays against tight budgets, which slows penetration in the lower end of the India data center physical security market. Managed security subscriptions that convert upfront expense into monthly fees are emerging but remain niche.

Grey-Market Low-Cost Surveillance Products

Uncertified imports or knock-off cameras tempt budget-conscious buyers, yet they fail compliance tests. Upcoming mandates that enforce Bureau of Indian Standards certification from April 2025 aim to curb such products, but in the interim they pressure recognized vendors’ margins within the India data center physical security market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Security Solution: Video Surveillance Remains the Cornerstone

The segment opened 2025 with a 45.62% India data center physical security market share, confirming its role as the first layer of defense. AI-enabled analytics now flag dwell-time anomalies and piggy-backing in real time, which reduces operator fatigue and speeds incident response. Intrusion detection and perimeter security posted the top growth at a 17.72% CAGR as operators extend protection beyond compound walls. Integrated command software aligns cameras, motion sensors, and biometric logs to one pane of glass, trimming false positives and ensuring compliance evidence. Secondary solutions such as mantraps and anti-ram bollards complete the multi-layer stack.

Edge operators adopt lower-power cameras paired with cloud AI to offset bandwidth limits. Hyperscale sites deploy thermal imaging to spot heat signatures in low-light perimeters, aided by radar for blind-spot coverage. As analytics migrate to on-device chips, the India data center physical security market anticipates lower total cost of ownership and faster forensic search.

By Service: Managed Services Accelerate Adoption

Integration and maintenance remain core, yet managed services recorded an 18.11% CAGR through 2032. Enterprises outsource 24 × 7 monitoring, firmware updates, and incident triage to specialist security operations centers that aggregate hundreds of sites. Consulting firms map regulatory needs, select hardware, and validate resilience during power or network failure drills. Providers bundle uptime, intrusion response times, and audit documentation into outcome-based contracts, shifting risk away from asset owners.

Cloud dashboards offer multi-tenant views, letting colocation customers monitor their own cages while facility teams retain holistic oversight. Because certified staff are scarce, operators value service partners who guarantee technician availability in remote cities. These dynamics expand recurring revenue streams inside the India data center physical security market

By Tier Standard: Tier III Balances Risk and Cost

Tier III facilities held 47.35% of 2025 revenue in the India data center physical security market. They install redundant access paths and dual power feeds but avoid Tier IV cost escalation. Security investments focus on dual-factor entry doors, 90-day video retention, and zoned alarms that allow concurrent maintenance without exposing live halls.

Edge and micro nodes, often Tier II, grow at 17.46% CAGR. Limited staffing prompts heavier reliance on autonomous drones and smart locks that auto-revoke credentials on contract completion. Vendors provide plug-and-play security kits that factory-test cable routing, camera calibration, and biometric firmware before shipment.

By Data Center Type: Hyperscale Shapes Standards

Hyperscale campuses captured 50.28% of 2025 spending within the India data center physical security market size, underpinned by cloud majors that require uniform safeguards across multi-building parks. They deploy redundant fiber loops for camera backhaul, on-premises AI inference clusters, and biometric mustering during fire drills.

Edge-scale hyperscale nodes rise at 17.78% CAGR as operators bring compute closer to users while maintaining centralized policy control. Compact designs integrate access-control panels, battery backup, and environmental sensors in a single rack, enabling truck-roll deployment in new cities. These innovations spill over to enterprise and colocation builds, lifting overall technical maturity.

By End-User Industry: IT and Telecom Dictates Volume

IT and telecom owned 38.42% of 2025 demand and continues to scale as carriers like Nxtra extend footprints to 65 cities. Compliance with global cloud benchmarks drives adoption of mantrap vestibules and AI camera analytics that reconcile access logs with server-room badge use.

E-commerce and retail expand at 17.63% CAGR, propelled by omnichannel platforms that store consumer data locally to meet upcoming privacy rules. BFSI maintains high per-rack spend with vault-grade cages, seismic bracing, and continuous guard patrols. Healthcare facilities reinforce audit transparency after ransomware incidents, adopting real-time location services for staff and visitor tracking.

Geography Analysis

Mumbai, Chennai, and Delhi-NCR host about 60% of national capacity, making them focal points for suppliers in the India data center physical security market. Mumbai’s financial concentration drives investments in biometric portals and AI cameras that meet stringent audit trails for banking clients. Chennai, with multiple submarine cables, uses flood-resistant barriers and elevated camera mounts to counter cyclone risk. Delhi-NCR sites emphasize anti-drone defenses near critical government assets.

Bangalore attracts technology firms yet faces power stability challenges, so operators integrate UPS-backed camera loops and generator-powered access control. Hyderabad and Pune offer cost advantages, illustrated by AdaniConneX earning a five-star safety rating at its Hyderabad campus. Tier-2 cities like Nagpur, Raipur, and Chandigarh provide incentives under Data Centre Economic Zones, prompting vendors to design modular guardhouses that ship pre-wired.

Government projects, such as the National Informatics Centre build in Guwahati, extend demand into the northeast, requiring ruggedized hardware against humidity. Uniform certification frameworks ensure sites in newer regions still align with national insurance and compliance benchmarks, spreading the India data center physical security market across the entire country.

Mordor Intelligence provides coverage of the global data center physical security market across other key regional markets, including South America, Europe, and Middle East, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Singapore, Thailand, Brazil, Spain, Saudi Arabia, and Philippines incorporating local coverage and market participation, as required.

Competitive Landscape

The market is moderately concentrated. Global providers such as Honeywell, Schneider Electric, and Johnson Controls lead end-to-end solution bids for hyperscale campuses, leveraging integrated building-management platforms. Domestic manufacturers like CP Plus strengthen position through Make-in-India certified cameras that bypass import duties and appeal to government buyers.

AI capability is the main differentiator. Honeywell’s locally produced 50 Series cameras ship with on-device facial analytics that meet data-sovereignty rules. Axis offers cloud-connect APIs so operators can integrate physical and cyber alerts on one dashboard. System integrators compete on outcome-based contracts that guarantee maximum response times and audit readiness.

Recent security breaches raised the bar for compliance evidence, prompting hyperscale clients to favor vendors with independent certifications and proven incident histories. This shift consolidates spending among about 15 players, yet smaller projects still source cost-sensitive gear from regional brands, keeping overall fragmentation intact.

India Data Center Physical Security Industry Leaders

Axis Communications AB

ABB Ltd

Bosch Sicherheitssysteme GmbH

Honeywell International Inc.

Johnson Controls.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Sify Technologies committed USD 5 billion for AI-ready data-center expansion, including advanced surveillance and biometric upgrades.

- February 2025: Reliance Industries broke ground on a 3 GW green-energy campus in Jamnagar, specifying multi-layered physical security.

- March 2025: The Government of India reinforced national cyber-preparedness measures that require parallel physical safeguards.

- April 2025: Enforcement of Bureau of Indian Standards rules on CCTV hardware came into effect.

India Data Center Physical Security Market Report Scope

The data center physical security market refers to the industry focused on providing products and services to safeguard the physical infrastructure and assets of data centers. This includes measures to protect data centers from unauthorized access to premises, hardware theft, vandalism, sabotage, terrorist acts, and other physical threats. Key components of data center physical security may include video surveillance and monitoring, access control systems, physical barriers, biometric authentication, and environmental controls designed to ensure the safety and integrity of the data center environment.

The Indian data center physical security market is segmented by solution type, service type, and end users. By type, the market is segmented into video surveillance and access control solutions. By service type, the market is segmented into consulting services and professional services. By end users, the market is segmented into IT and telecommunication, BFSI, government, media and entertainment, and other end users. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Video Surveillance |

| Access Control |

| Intrusion Detection and Perimeter Security |

| Other Solutions (Mantraps, Fences, Monitoring) |

| Consulting |

| Integration and Deployment |

| Maintenance and Support |

| Managed Services |

| Tier I and II |

| Tier III |

| Tier IV |

| Hyperscale/Self-Built |

| Colocation |

| Enterprise (On-Premise) |

| IT and Telecommunication |

| BFSI |

| Government and Public Sector |

| Healthcare and Life Sciences |

| E-commerce and Retail |

| Other End Users |

| By Security Solution | Video Surveillance |

| Access Control | |

| Intrusion Detection and Perimeter Security | |

| Other Solutions (Mantraps, Fences, Monitoring) | |

| By Service | Consulting |

| Integration and Deployment | |

| Maintenance and Support | |

| Managed Services | |

| By Tier Standard | Tier I and II |

| Tier III | |

| Tier IV | |

| By Data Center Type | Hyperscale/Self-Built |

| Colocation | |

| Enterprise (On-Premise) | |

| By End-User Industry | IT and Telecommunication |

| BFSI | |

| Government and Public Sector | |

| Healthcare and Life Sciences | |

| E-commerce and Retail | |

| Other End Users |

Key Questions Answered in the Report

What is the 2026 value of the India data center physical security market?

The market is valued at USD 87.63 million in 2026.

How fast is the market expected to grow through 2032?

It is forecast to register a 17.44% CAGR, reaching USD 229.93 million by 2032.

Which security solution holds the largest share today?

Video surveillance leads with 45.62% of 2025 revenue.

Which end-user segment demands the most physical security?

IT & telecommunications accounts for 38.42% of current demand.

Why are Tier III facilities prominent in India?

They balance uptime needs with cost and capture 47.35% of 2025 spending on physical security.

Page last updated on: