Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

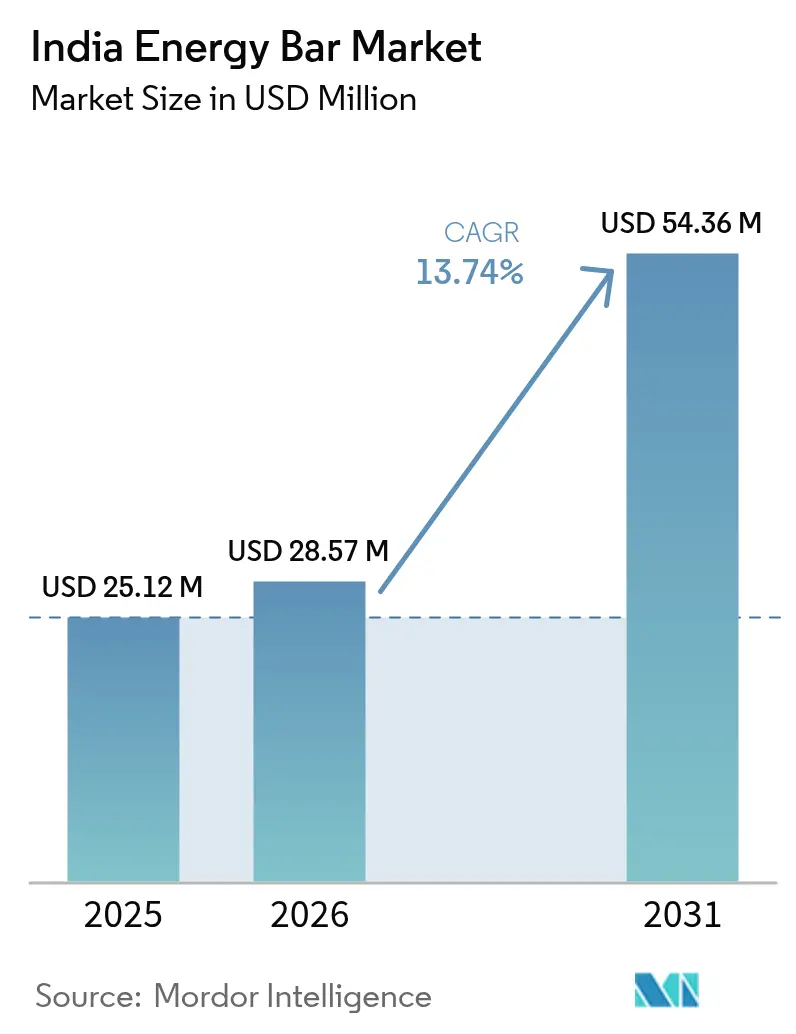

| Base Year Market Size (2025) | USD 25.12 Million |

| Market Size (2026) | USD 28.57 Million |

| Market Size (2031) | USD 54.36 Million |

| Growth Rate (2026 - 2031) | 13.74% CAGR |

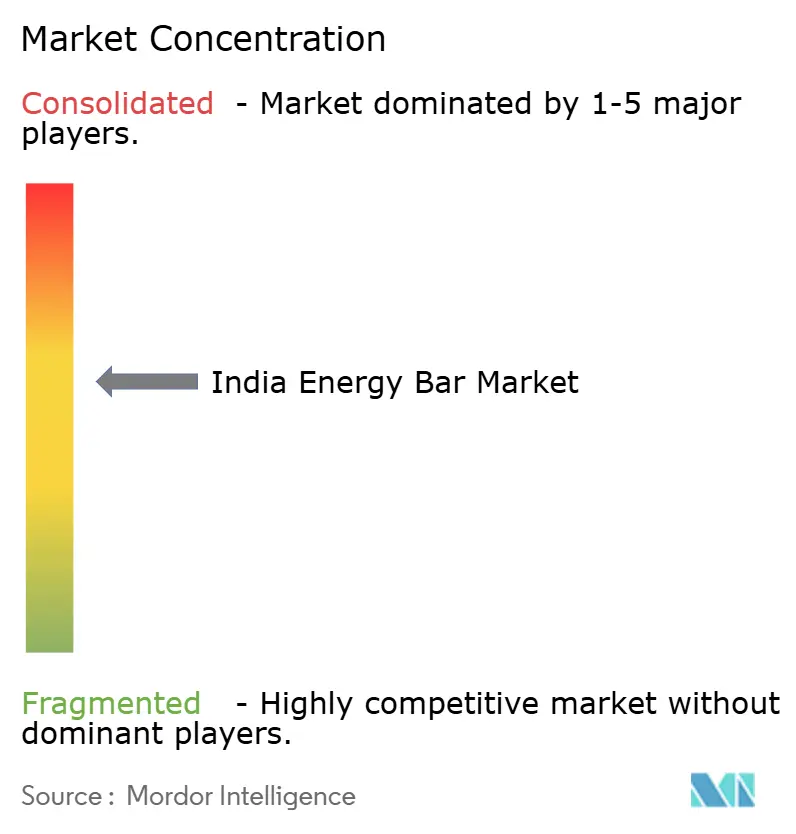

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Energy Bar Market Analysis by Mordor Intelligence

The Indian energy bar market size is expected to grow from USD 25.12 million in 2025 to USD 28.57 million in 2026 and is forecast to reach USD 54.36 million by 2031 at 13.74% CAGR over 2026-2031. The current India energy bar market size reflects rising health consciousness, fitness-driven lifestyles and expanding modern retail access. Protein-rich formulations dominate because consumers view them as convenient tools for bridging India’s chronic protein deficit. Moreover, growth accelerators include gym proliferation, government sports initiatives and omnichannel shopping habits that favor portable nutrition solutions. Product developers intensify flavor innovation and clean-label claims to capture millennials who research labels online before purchase. Meanwhile, strategic acquisitions by large FMCG firms confirm the category’s long-term potential and signal a shift from niche to mainstream positioning. However, energy bars in India are perceived to be high-priced in comparison with regular snack bars. This has provided an opportunity for Indian players such as Patanjali to come up with energy bars that are offered at a lower price.

Key Report Takeaways

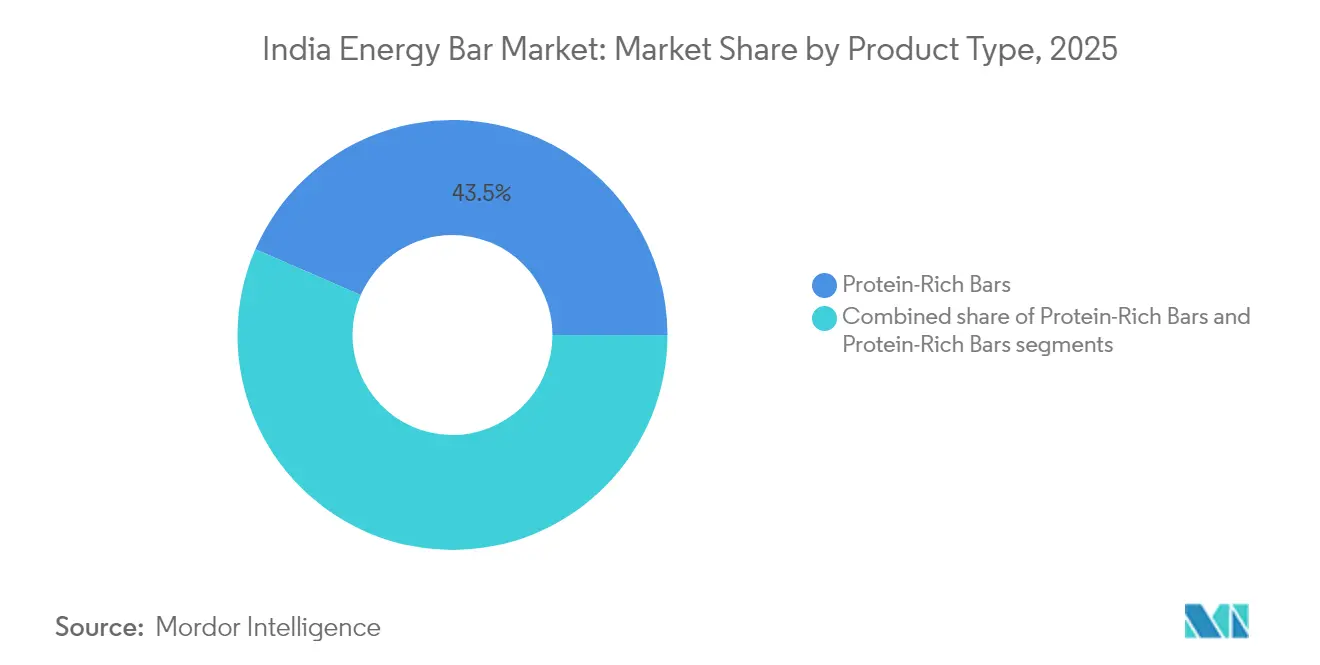

- By product type, protein-rich bars captured 43.47% of the Indian energy bar market share in 2025 and are projected to advance at a 14.98% CAGR through 2031.

- By consumer demographic, adults commanded 54.66% of the Indian energy bar market share in 2025, while sports and fitness enthusiasts are forecast to record the fastest 15.06% CAGR to 2031.

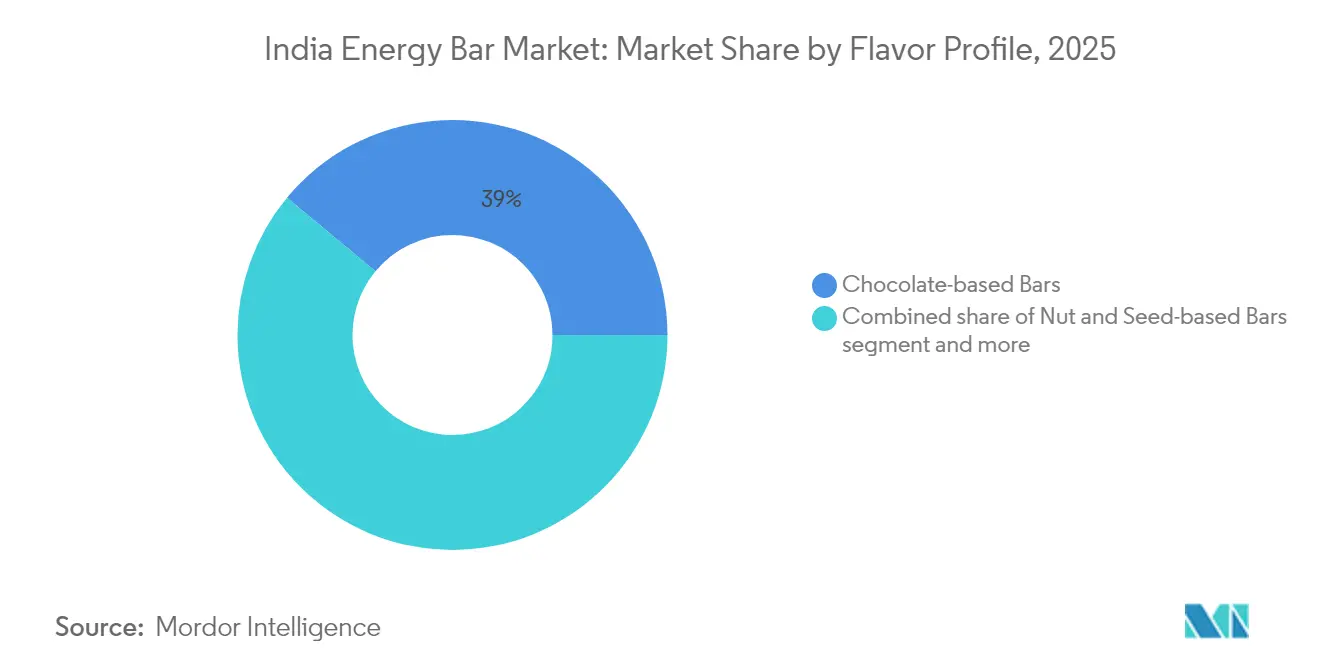

- By flavor profile, chocolate variants accounted for 38.98% of the Indian energy bar market share in 2025, and nut-and-seed bars are anticipated to post the quickest 14.61% CAGR up to 2031.

- By distribution channel, supermarkets/hypermarkets held 62.56% of the Indian energy bar market share in 2025; in contrast, online retail is expected to expand at a 15.32% CAGR during the forecast period.

- By region, the West led with 34.57% of the Indian energy bar market share in 2025, whereas the South is set to grow at a 14.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Energy Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Geographic Relevance |

|---|---|---|---|

| Rising health-conscious consumer base and demand for on-the-go nutrition | +3.2% | National, with early gains in West and South regions | Medium term (2-4 years) |

| Growth of fitness centers and gyms | +2.8% | Urban centers across West, North, and South regions | Medium term (2-4 years) |

| Rising sports and recreational participation | +2.1% | National, spill-over from government initiatives | Long term (≥ 4 years) |

| Innovation in flavors and nutrient composition | +1.9% | National, with premium segment focus in metros | Short term (≤ 2 years) |

| Demand for plant-based and clean-label trends | +2.4% | Urban markets, particularly South and West regions | Medium term (2-4 years) |

| Endorsement by influencers and fitness experts | +1.8% | Digital-native consumers across tier-1 and tier-2 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising health-conscious consumer base and demand for on-the-go nutrition

The rising health-consciousness among urban consumers is driving significant growth in the energy bar market. Urban adults, averaging 1,943 Kcal daily, face notable protein and micronutrient intake gaps, positioning energy bars as a practical supplement. This heightened nutritional awareness is underscored by Sodexo's findings: Indians, especially 60% of millennials aged 25-44, are leading the charge in adopting healthy eating habits, with a pronounced commitment to sustainable food choices in 2024 [1]Source: Sodexo, "India Strives for Planet-Friendly Food More Than the Developed Countries, says Sodexo’s Sustainable Food Barometer survey", sodexo.in . This trend isn't confined to metropolitan areas; tier-2 cities, contributing nearly half of India's online shoppers, signal a broader geographic embrace of health-conscious behaviors. The post-pandemic landscape has seen consumers increasingly willing to pay a premium for health-centric products, particularly those targeting weight management and stress relief. As busy lifestyles intertwine with heightened health awareness, the demand for convenient, nutritious snacks like energy bars remains robust. Brands such as YogaBar are seizing this momentum, offering protein-rich, clean-label bars designed for the urban fitness enthusiast. This alignment of shifting consumer lifestyles with a deepening health consciousness propels the Indian energy bar market, suggesting its growth is not merely a fleeting trend. Innovations in packaging and the surge of online sales further broaden access, propelling the market's expansion beyond traditional urban confines.

Growth of fitness centers and gyms

The expansion of fitness infrastructure serves as a key driver for energy bar consumption through direct distribution channels and increased adoption among fitness enthusiasts. The Sports Authority of India (SAI) manages 24 National Centres of Excellence and 69 training centers, supporting over 3,240 athletes with specialized nutrition programs in 2022-23, establishing a foundation for performance nutrition adoption [2]Source: Sports Authority of India, "Annual Report 2022-23", sportsauthorityofindia.gov.in. Besides, private fitness chains like Gold's Gym, Cure.fit, and Talwalkars continue to expand across urban areas, increasing the consumer base for energy bars. Corporate wellness programs have also integrated energy bars into their offerings, extending market reach to working professionals. The COVID-19 pandemic accelerated digital transformation in the fitness sector, resulting in hybrid models that combine physical facilities with online services. This evolution has expanded access to nutrition products beyond traditional gym members. Companies like The Whole Truth have capitalized on these expanded consumer touchpoints by offering protein and energy bars that appeal to both athletes and recreational fitness enthusiasts. Hence, the development of this fitness ecosystem, comprising government sports facilities, commercial gyms, corporate wellness programs, and hybrid delivery models, provides structural support for sustained market growth. This integration of fitness infrastructure and nutrition products aligns with changing consumer lifestyles in urban and semi-urban regions.

Rising sports and recreational participation

The Khelo India movement, along with various government initiatives, has significantly expanded the athlete base in India while embedding performance nutrition as a critical component across all age groups and skill levels. Also, the Sports Authority of India (SAI) has developed specialized training centers and personalized diet plans, designed by professional nutritionists, for athletes in disciplines such as athletics, boxing, and weightlifting, highlighting the importance of nutrition in enhancing performance. This institutional framework is influencing consumption patterns, with recreational athletes and fitness enthusiasts increasingly adopting professional training and nutrition practices. Besides, strategic partnerships between sports authorities and nutrition brands have strengthened credibility and widened distribution networks, bringing energy bars from niche athletic circles into mainstream consumer markets. Additionally, a favorable regulatory environment and government endorsements are addressing consumer skepticism about supplementation, positioning energy and nutrition bars as essential tools for performance rather than luxury products. Brands like YogaBar are leveraging this trusted environment to market protein and energy bars aligned with scientific nutrition principles. The integration of government-led sports infrastructure, nutrition education, and corporate collaborations is fostering a robust ecosystem that supports the growth of the energy bar market. As sports and recreational participation continue to rise nationwide, this comprehensive approach ensures sustained market expansion.

Innovation in flavors and nutrient composition

The energy bar market in India is undergoing a significant transformation, driven by the integration of diverse culinary traditions and advanced nutritional science. Manufacturers are leveraging the clean-label trend to develop unique products that command premium pricing and foster brand loyalty. A notable example is influencer Revant Himatsingka’s July 2025 launch of "Only What's Needed", which emphasizes transparent labeling and minimal ingredients, curated through public input to meet consumer expectations. Besides, flavor innovations have expanded beyond traditional chocolate and vanilla, incorporating regional tastes and millet-based formulations. These developments align with government nutrition initiatives and traditional Indian dietary habits. Nutrient compositions now focus on functional benefits, with brands incorporating prebiotics, probiotics, and targeted micronutrients to address specific health concerns, offering more than basic protein. Moreover, the regulatory framework supports such advancements, with FSSAI’s April 2022 nutraceutical guidelines outlining permissible botanical ingredients and functional food categories, enabling compliant product development. Brands like Sirimiri are capitalizing on these trends by combining traditional ingredients with modern nutritional science. This dynamic innovation cycle strengthens consumer trust and loyalty while driving market growth. By addressing local tastes and health needs, these products differentiate themselves in a competitive landscape, adhering to evolving regulatory standards. The combination of cultural relevance and scientific progress serves as a key differentiator in the expanding energy bar market in India.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price point versus traditional snacks | -2.1% | National, particularly impacting tier-2 and tier-3 cities | Medium term (2-4 years) |

| Negative perception of high sugar bars among health-conscious consumers | -1.4% | Urban markets with higher health awareness | Short term (≤ 2 years) |

| Limited consumer awareness in non-urban areas | -1.8% | Rural and semi-urban regions, particularly East and North | Long term (≥ 4 years) |

| Competition from other healthy snacks | -1.6% | National, with intensity varying by distribution channel | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High price point versus traditional snacks

Price sensitivity presents a significant challenge in the energy bar market. Traditional snacks, priced between INR 5-20, are considerably cheaper than energy bars, which range from INR 45 to INR 540. This 5-10 times price difference creates a substantial barrier to both trial and repeat purchases, particularly in price-sensitive tier-2 and tier-3 cities. While energy bars offer superior nutritional value, consumers in these regions often opt for cheaper local snacks that provide immediate satiation. As a result, retailers prioritize faster-moving, lower-priced items, reducing shelf space and visibility for higher-margin energy bars. Efforts by companies to lower costs through value engineering are constrained by the need to maintain nutritional integrity, as compromising product quality risks eroding consumer trust and brand value. Brands such as Healthkart and Sproutlife Foods, despite their popularity, must carefully balance premium pricing with delivering genuine nutritional benefits to appeal to urban fitness enthusiasts and the growing semi-urban consumer base. As the market expands beyond metro areas, the economic disparity in pricing remains a critical obstacle, requiring targeted strategies to ensure affordability without diluting core health attributes. This ongoing tension between premium pricing and the affordability of traditional snacks continues to shape distribution and marketing strategies in the rapidly growing energy bar segment.

Negative perception of high sugar bars among health-conscious consumers

Health-conscious consumers, who drive growth and premium pricing in the energy bar market in India, harbor concerns over high sugar content. Campaigns, such as Revant Himatsingka's "Label Padhega India," aim to educate these consumers. They reveal that many energy bars contain sugar levels comparable to confectionery items, challenging their positioning as health foods and fostering skepticism. This concern extends beyond added sugars to include natural sweeteners and sugar alcohols, which, despite their distinct nutritional profiles, are often associated with processed foods. The FSSAI enforces stringent labeling regulations, requiring clear disclosure of sugar content and substantiation of health claims [3]Source: Food Safety and Standards Authority of India (FSSAI), "FOOD SAFETY AND STANDARDS (LABELLING AND DISPLAY) REGULATIONS, 2020", fssai.gov.in . While this enhances transparency, it limits brands' ability to obscure high sugar formulations. As a result, manufacturers face a trade-off between optimizing taste, often dependent on sugars, and maintaining a strong health-focused image. Brands like YogaBar have responded by emphasizing clean-label ingredients with reduced sugar content to better align with consumer expectations. Heightened scrutiny from consumers, combined with regulatory pressures, challenges the energy bar market in India. Companies are now compelled to innovate, developing formulations that balance flavor and health benefits to sustain consumer trust and drive market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein-Rich Bars Drive Market Leadership

Protein-rich bars accounted for a dominant 43.47% market share in 2025 and are projected to grow at a robust 14.98% CAGR through 2031. This trend highlights a shift in consumer focus from indulgent snacking to functional nutrition. The widespread protein deficiency in Indian diets, often lacking adequate protein, drives sustained demand for convenient protein supplementation. Endorsements from fitness professionals and sports figures further enhance the appeal of the protein bar category. For instance, Axar Patel has both invested in and become the brand ambassador for FitFeast, a brand promoting protein-rich snacks to a broader audience beyond fitness enthusiasts.

Moreover, cereal and granola bars, traditionally dominant in the snacking segment, now face challenges as consumer preferences shift toward functional nutrition. Meanwhile, fruit and nut bars attract consumers seeking natural ingredients and familiar flavors. Competitive dynamics within product categories reveal a premiumization trend, with 20-30g protein bars commanding higher prices than 10g variants, reflecting consumer willingness to pay for enhanced functionality. Manufacturers are accelerating innovation cycles by incorporating plant-based proteins, clean-label ingredients, and specialized formulations targeting specific needs, such as meal replacement or post-workout recovery. This growth trajectory aligns with the expanding fitness culture and increasing awareness of protein's role in weight management, muscle building, and overall health maintenance.

By Consumer Demographic: Adults Lead While Sports Enthusiasts Accelerate

Adults account for a dominant 54.66% share of the market in 2025. Their established consumption patterns have seamlessly integrated energy bars into daily routines, serving as meal replacements, office snacks, and on-the-go nutrition. This dominance is supported by rising disposable incomes and heightened health awareness, enabling consumers to accept premium pricing for functional food products. The preference for convenience, combined with functionality, positions adults as the core customer base, ensuring consistent demand.

Sports and fitness enthusiasts represent the fastest-growing segment, with a robust CAGR of 15.06% projected through 2031. This growth is driven by the expansion of fitness infrastructure and a cultural shift toward active lifestyles. Also, government initiatives and celebrity endorsements have normalized performance nutrition, particularly among individuals who prioritize energy bars for performance enhancement and recovery. Additionally, children present an emerging opportunity, as parents increasingly seek healthier snacking alternatives to traditional confectionery and processed snacks. Brands like Mama Nourish are addressing this demand with kid-friendly products such as the Dryfruit Instant Energy LadduBar, which cater to nutritional needs while complying with FSSAI’s stringent guidelines on health claims and ingredient safety. These demographic insights highlight varied consumption patterns and product preferences, driving diverse growth trajectories in the market.

By Consumer Demographic: Adults Lead While Sports Enthusiasts Accelerate

Chocolate-based bars maintain a 38.98% market share in 2025, driven by their universal appeal and familiar taste, which reduces barriers to consumer trials. Nut and seed-based bars are the fastest-growing segment, with a 14.61% CAGR projected through 2031. The dominance of the chocolate segment highlights consumer preferences for familiar flavors, offering comfort and indulgence that bridge the gap between traditional confectionery and functional nutrition. However, the segment faces challenges from health-conscious consumers associating chocolate with high sugar content and processed ingredients, creating opportunities for premium dark chocolate formulations with reduced sugar profiles.

Nut and seed-based bars leverage increasing awareness of healthy fats, plant-based proteins, and natural ingredients, aligning with clean-label trends and traditional dietary preferences. Fruit-based bars attract consumers seeking natural sweetness and recognizable ingredients, while unique flavors provide differentiation opportunities for brands targeting specific regional preferences or functional benefits. The flavor innovation landscape reflects broader food industry trends toward authenticity, functionality, and cultural relevance, with successful products balancing taste appeal with nutritional benefits. The regulatory environment supports flavor innovation through FSSAI guidelines that permit natural flavoring agents while restricting artificial additives that could compromise health positioning.

By Distribution Channel: Supermarkets Lead While E-commerce Accelerates

Supermarkets/hypermarkets dominate the retail landscape in 2025, holding a commanding 62.56% market share. These traditional channels not only enhance product visibility but also offer consumers opportunities to trial products. Meanwhile, online retail stores are emerging as the fastest-growing channel, boasting a robust 15.32% CAGR projected through 2031. Supermarkets lead the pack, owing to ingrained consumer shopping habits, their ability to demonstrate products, and the impulse purchase opportunities they offer, all vital for the adoption of energy bars. By associating with well-known food retailers, these channels bolster their credibility, allowing consumers to compare products, scrutinize labels, and make informed choices. Yet, these channels grapple with margin pressures and limited shelf space, curbing their ability to proliferate SKUs and exercise promotional flexibility.

The rapid growth of e-commerce reflects the ongoing digital transformation, particularly in the online grocery sector. These online platforms foster direct-to-consumer ties, embrace subscription models, and employ targeted marketing strategies that resonate with health-conscious shoppers on the lookout for specific nutritional profiles or ingredients. Pharmacies and drug stores cater to niche segments, focusing on therapeutic or medical nutrition, while convenience and grocery stores capitalize on accessibility and spur-of-the-moment purchases. The shifting distribution landscape mirrors evolving consumer habits. Notably, tier-2 and tier-3 cities account for nearly half of all online shoppers, presenting a lucrative growth avenue for energy bar brands. As brands navigate the delicate balance between customer acquisition costs and market penetration, there's a pronounced shift towards omnichannel strategies. These approaches harmoniously blend online discovery and education with the tangible benefits of offline trials and convenience.

Geography Analysis

In 2025, the West region commands a dominant 34.57% market share, largely due to the robust fitness ecosystem in Maharashtra and Gujarat. Mumbai, often regarded as the fitness capital, hosts numerous gyms, wellness centers, and corporate health initiatives, creating natural consumption channels for energy bars. This region benefits from higher disposable incomes and cosmopolitan lifestyles, driving early adoption of global health trends. Consequently, energy bars are positioned as lifestyle essentials rather than niche supplements. The West's distribution strengths include established FMCG networks, extensive modern retail penetration, and a well-developed logistics infrastructure, ensuring efficient market coverage and product availability. However, the market faces challenges such as intense competition from established players and the need for premium positioning, which create entry barriers for new players in this mature segment.

The South region is emerging as a key growth driver, with a projected 14.31% CAGR through 2031. Growth in this region is supported by Karnataka's technology-driven employment base, Tamil Nadu's advanced food processing capabilities, and Andhra Pradesh's expanding urban centers, which collectively foster affluent, health-conscious consumer groups. Tamil Nadu's leadership in processed food exports provides supply chain advantages and manufacturing expertise, enabling local production and cost efficiencies for energy bar companies. The region's openness to dietary experimentation, coupled with strong educational institutions and heightened awareness of nutritional science, creates a conducive environment for product innovation and market expansion. Additionally, Southern states exhibit higher monthly per capita expenditure on food, indicating strong consumer capacity for premium nutrition products.

The North and East regions represent untapped opportunities, each characterized by distinct market dynamics that require tailored strategies and long-term investment. In the North, Delhi NCR's corporate concentration and Punjab's sports-oriented culture offer growth potential, but traditional dietary preferences and price sensitivity hinder the adoption of premium products. In contrast, the East faces affordability challenges due to the lowest monthly per capita expenditure nationally. This necessitates the development of value-engineered products and alternative distribution strategies focused on accessibility rather than premiumization. To succeed in these emerging markets, businesses must prioritize educational marketing, adapt products to local tastes, and collaborate with regional distributors who possess deep insights into cultural nuances and consumer behavior, which differ significantly from the more established Western and Southern markets.

Regulatory Landscape

Energy bars in India are regulated by the Food Safety and Standards Authority of India (FSSAI) under the broader food and nutraceutical framework, with many SKUs formulated and marketed within the Food Safety and Standards (Health Supplements, Nutraceuticals, Food for Special Dietary Use, Food for Special Medical Purpose, and Prebiotic and Probiotic Food) Regulations, 2022, where bars are an accepted delivery format. Products positioned as foods for special dietary use, such as meal-replacement style bars, must align with compositional provisions in these rules (including defined energy ranges per meal for partial replacements), while all mainstream retail packs must comply with the Food Safety and Standards (Labelling and Display) Regulations, 2020 for mandatory nutrition and claim disclosures.

In 2026, FSSAI activity signaled additional compliance work for packaged food brands: in February 2026, FSSAI issued draft amendments to the Food Products Standards and Food Additives Regulations, 2011 to update cross-references to the 2018 Packaging Regulations and the 2020 Labelling and Display Regulations across food categories, prompting label and artwork reviews for companies operating in adjacent packaged snack segments. On the input side, periodic customs valuation changes can influence landed costs for ingredients such as edible oils, with the Central Board of Direct Taxes and Customs (CBIC) revising tariff values via Notification No. 49/2026-CUSTOMS (N.T.) dated 29 May 2026, reinforced the need for importers to monitor duty-linked price movements in formulations and procurement.

Value Chain Analysis

The value chain begins with ingredient sourcing, where key inputs include cereals and millets (often domestically sourced), sweeteners and binders (including date-based ingredients and other natural binders), fats and oils, and functional additions such as whey protein isolates that are frequently imported. Manufacturing involves formulation, mixing, and forming using processes such as extrusion or cold pressing, followed by secondary steps such as coating, cutting, and packaging. Compliance and quality systems shape both formulation and labeling decisions because the category often sits under proprietary food or nutraceutical/functional positioning, requiring adherence to FSSAI rules, particularly the Labelling and Display Regulations, 2020 for nutrition and claim disclosures.

Downstream, brands distribute through modern trade (supermarkets/hypermarkets), pharmacies/drug stores for performance and functional positioning, and fast-growing e-commerce and quick-commerce platforms that support discovery, subscriptions, and targeted assortments. The April 2024 FSSAI advisory to e-commerce operators on avoiding misleading categorization of health and energy products tightened digital shelf governance, making correct online taxonomy and compliant product descriptions part of the commercialization workflow alongside offline retail execution. This structure favors players that can balance premium D2C economics with the shelf visibility of modern trade, while managing input cost volatility and packaging choices that support freshness, portability, and claims-led marketing.

Competitive Landscape

The competitive landscape of the Indian energy bar market is moderately consolidated yet highly dynamic, marked by the presence of both established players and emerging brands. Traditional FMCG companies, specialized nutrition brands, and D2C startups compete by prioritizing product innovation, distribution strategies, and distinct brand positioning. This fragmented yet competitive environment drives differentiation through clean-label offerings, transparency in ingredient sourcing, and engagement with younger, skeptical consumers seeking authenticity. For example, brands like YogaBar focus on clean-label and ingredient transparency to attract health-conscious buyers.

Strategic actions such as acquisitions are influencing market consolidation trends. A notable example is Zydus Wellness’s acquisition of Naturell for Rs 390 crore in October 2024, demonstrating how companies with strong distribution capabilities and financial resources are strengthening their market presence. Technology adoption further sets competitors apart, with players leveraging e-commerce, direct-to-consumer models, and digital marketing to engage a research-savvy consumer base that scrutinizes product efficacy and safety before purchase. These digital tools enable omnichannel distribution and influencer partnerships, which enhance brand credibility and trust, critical factors in a category where performance and health claims are pivotal.

Additionally, white-space opportunities remain in addressing regional flavor preferences, specialized nutritional formulations, and underserved demographic segments. Emerging disruptors emphasize community engagement and transparent marketing that resonates with younger consumers wary of conventional claims. The regulatory environment, led by FSSAI’s evolving guidelines, presents both challenges and opportunities for innovation. Companies with robust quality management systems are better positioned to benefit, particularly when making functional ingredient claims. This regulatory framework supports market growth by balancing compliance with creative product development tailored to evolving consumer demands in the Indian energy bar market.

India Energy Bar Industry Leaders

-

Naturell India Pvt Ltd

-

SproutLife Foods Private Limited (Yogabars)

-

Fitshit Health Solutions Pvt. Ltd (The Whole Truth)

-

General Mills Inc.

-

Mars Incorporated

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities concentrate around compliant innovation, affordability, and channel expansion into new consumption occasions. Protein-rich and clean-label positioning continues to reshape brand playbooks, but the most actionable whitespace is in formulations that address sugar scrutiny through transparent labeling and ingredient choices (for example, date and jaggery-based sweetness) while maintaining taste and texture. The ongoing shift of discovery and replenishment to online and quick-commerce creates room for trial packs, subscriptions, and targeted assortments for adults and sports and fitness enthusiasts, supported by the channel’s ability to surface functional attributes and enable rapid repeat purchases.

Manufacturing and ecosystem programs add additional headroom for brands to scale localized production and broaden distribution reach. The Ministry of Food Processing Industries PLI Scheme for the food processing sector (INR 10,900 crore outlay) explicitly prioritizes innovation and millet-based products, aligning with energy bars that incorporate indigenous grains and functional ingredients. Broader packaged-food capacity investments also strengthen the supplier and co-manufacturing ecosystem that energy bar brands tap for scale and procurement leverage, illustrated by Nestle India's March 2026 announcement of a new production line at its Sanand facility in Gujarat and PepsiCo India's stated multi-year foods manufacturing expansion plan announced in May 2026. These moves, combined with FSSAI's labeling enforcement focus, favor companies that can industrialize clean-label claims, standardize quality, and execute omnichannel distribution while keeping unit economics viable for price-sensitive consumers beyond core metro markets.

Recent Industry Developments

- April 2026: ITC Limited finalized acquisition of control over SproutLife Foods Private Limited (YogaBar), making it a subsidiary effective April 1, 2026 after securing the right to nominate a majority of directors on the board. The move brings a scaled FMCG distribution and sourcing platform behind a digital-first energy and protein bar brand. It also raises competitive pressure on independent brands as modern trade reach and brand building budgets become easier to deploy at national scale.

- February 2026: A USD 51 million Series D funding round closed for The Whole Truth brand under Fitshit Health Solutions Pvt. Ltd, with Sofina Ventures and Sauce.vc leading the round. The capital supports deeper investments in product development and operational scale-up across clean-label snacking, including bars. The new funding strengthens the brand's market reach through expanded distribution and increased marketing cadence, intensifying competition in the clean-label snacking space.

- October 2024: Zydus Wellness announced a definitive agreement to acquire 100% of Naturell (India) Private Limited, the maker of RiteBite Max Protein bars, for INR 390 crore. The acquisition links an established bar portfolio to Zydus Wellness's distribution and consumer health platform. It accelerates consolidation in performance-oriented snack formats and increases the prominence of large portfolio players in shelf space negotiations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers packaged energy bars sold in India through offline and online channels, where consumption is for convenient snacking and quick energy. Revenues are counted at the point where branded products are sold into the market, converted to USD for consistency.

Scope exclusions: Excludes homemade or unpackaged bars, and it also excludes wider snack-bar categories unless they are sold as energy bars.

Segmentation Overview

-

By Product Type

- Cereal/Granola Bars

- Protein-Rich Bars

- Fruit and Nut Bars

-

By Consumer Demographic

- Children/Kids

- Adults

- Sports and Fitness Enthusiasts

-

By Flavor Profile

- Chocolate-based Bars

- Fruit-based Bars

- Nut and Seed-based Bars

- Other Unique Flavors

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Pharmacies/Drug Stores

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

-

By Region

- East

- West

- North

- South

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the base structure of the model and to anchor assumptions that can be checked in public data. We review sources such as the Ministry of Commerce and Industry trade statistics, FSSAI updates and notifications, National Sample Survey (consumer spending context), and Reserve Bank of India macro series for inflation and currency trends. When available, we also read snack and packaged-food updates from industry bodies such as FICCI and ASSOCHAM, along with peer-reviewed nutrition and food-science journals to understand ingredient and labeling shifts.

To connect these signals to company performance, we add annual reports, filings, and investor presentations of relevant packaged-food companies, plus reputed press coverage for launches and pricing moves. Paid subscriptions are used in a limited way for company financials and intelligence, and for patent searches where formulation activity supports a trend view. The desk sources listed here are illustrative only, and many other public documents were also used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work is used to turn desk signals into practical inputs, especially for price bands, channel mix, and how frequently bars are bought for fitness, travel, or everyday snacking. We speak with a mix of brand-side managers, distribution and retail stakeholders, and category experts across major Indian regions so gaps in availability and discounting patterns can be corrected before the final numbers are locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | |

| Mid tier: 46% | Functional/Unit leaders: 37% | |

| Smaller Players: 21% | Managers: 50% |

Market-Sizing & Forecasting

For sizing, we use a top-down approach where the packaged snack and nutrition bar demand pool is reconstructed through channel presence and consumption frequency, and then narrowed to energy bars using category definitions used by retailers and brands. The totals are corroborated with selective bottom-up approximations, where sampled price points are multiplied by estimated volumes across key channels and then adjusted using interview checks.

A few practical inputs that shape the model include: average selling price by pack size, share of online retail versus modern trade and pharmacies, the rate of new product launches and reformulations (for example, whole grain, nuts, and seeds positioning), and the intensity of promotions that temporarily changes realized prices. We also track gym and fitness participation as a directional demand signal, along with inflation trends that affect consumer trade-down. When a channel has thin visibility, we fill the gap using proxy splits from similar packaged snack categories and then re-check the split with primary respondents.

Forecasts are built using scenario analysis with a simple demand driver set, and assumptions are aligned to what experts expect for channel expansion and price progression. Growth rates are then stress-tested against historical shifts in availability and affordability before the final series is published.

Data Validation & Update Cycle

Outputs are validated through triangulation across three layers, which are desk indicators, primary feedback, and internal consistency checks across years. If growth jumps or channel shares move too sharply, the inputs are re-reviewed and respondents are re-contacted to confirm whether the change is real or driven by temporary discounting or a one-time supply event.

Before sign-off, the model is reviewed by another analyst to confirm currency conversions, inflation handling, and the logic behind any step changes. Reports refresh annually, and interim updates are made when there are material events such as major regulatory updates, sharp input-cost movements, or a visible shift in channel structure. Right before delivery, we do a final pass so clients receive the most current view available.

Mordor Intelligence's India Energy Bar Market Estimate Compared With Other Published Estimates

Published market sizes for India energy bars can look far apart because each publisher uses a different product boundary, year definition, and pricing basis. Differences also come from how online discounting is treated, whether regional coverage is explicit, and how much primary validation is used to check the channel mix.

Functional snack bars like protein, fiber, and meal replacement bars sit outside Mordor Intelligence's scope here, which is one reason the value in this study does not track broader snack-bar totals seen in some publications. Other gaps usually come from mixing retail value with manufacturer revenue, using aggressive adoption assumptions for fitness-led demand, or applying a single ASP trend without checking pack-size shifts and promo intensity.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.12 M (2025) | |

| Retail Aggregator A | USD 3.91 M (2024) | Uses an earlier base year and tends to undercount offline contribution when modern trade and pharmacy sales are not fully captured, which pulls down the total for India. |

| Industry Publisher B | USD 13.00 M (2025) | Covers functional snack bars as a combined category and only partially isolates energy bars, so the number reflects a different product pool and a slower growth profile. |

Looking across the table, the spread is mainly explained by what is included as an energy bar, plus how channel coverage and realized pricing are built into the calculation. By keeping the inputs tied to clear channel splits, pack-level pricing, and repeatable validation steps, the final value is easier to trace and update year after year.

Key Questions Answered in the Report

How large is the India energy bar market in 2026?

The India energy bar market size stands at USD 28.57 million in 2026.

Which product type leads sales?

Protein-rich bars held 43.47% of India energy bar market share in 2025 and will stay dominant through 2031.

Which region shows the quickest expansion?

Southern states collectively post the fastest CAGR at 14.31% during 2026-2031.

How is e-commerce influencing sales?

Online retail is the fastest-growing channel at 15.32% CAGR, aided by subscription models and quick-commerce delivery.

Page last updated on: