Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

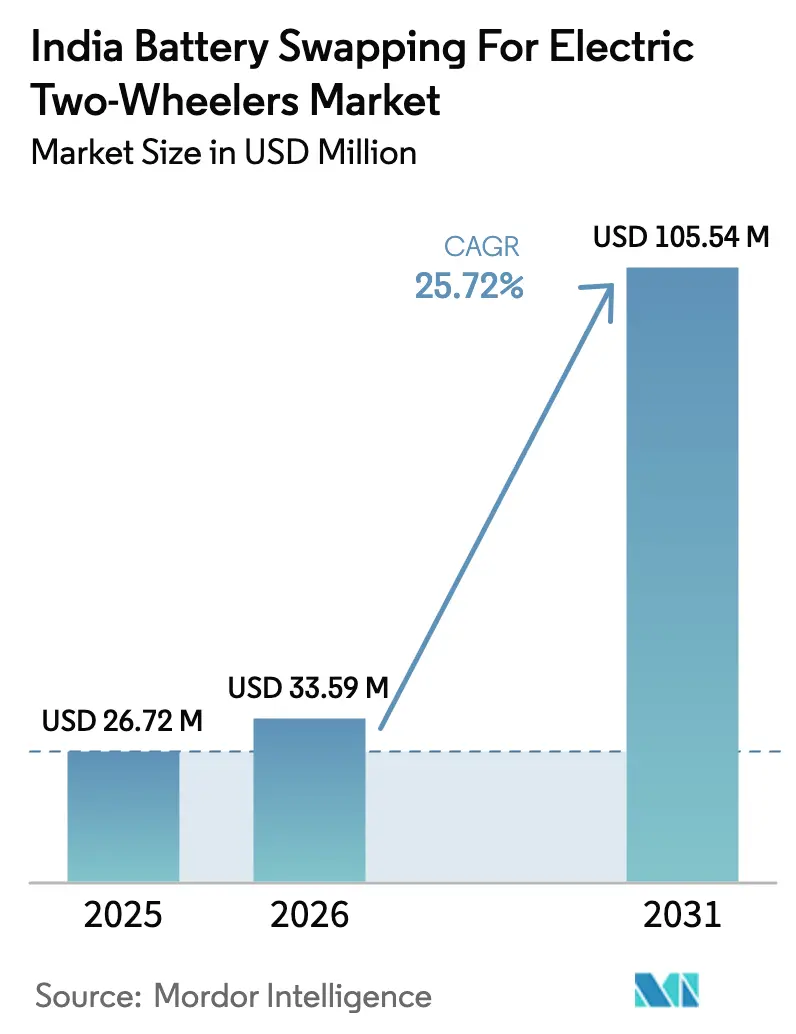

| Base Year Market Size (2025) | USD 26.72 Million |

| Market Size (2026) | USD 33.59 Million |

| Market Size (2031) | USD 105.54 Million |

| Growth Rate (2026 - 2031) | 25.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Battery Swapping For Electric Two-Wheelers Market Analysis by Mordor Intelligence

The India battery swapping for electric two-wheelers market size was valued at USD 26.72 million in 2025 and estimated to grow from USD 33.59 million in 2026 to reach USD 105.54 million by 2031, at a CAGR of 25.72% during the forecast period (2026-2031). Rapid sales growth in electric two-wheelers, federal and state-level purchase incentives, and a maturing venture-capital pipeline are reinforcing confidence that swapping infrastructure will underpin India’s broader electrification roadmap. The transition from FAME-II to the PM E-DRIVE scheme sustains direct purchase subsidies while earmarking funds for interoperable packs and Internet-of-Things (IoT) battery monitoring, ensuring that subsidies translate into real-world utilization. Private capital from oil-marketing companies (OMCs) and global investors is speeding up station deployment, and the introduction of Bureau of Indian Standards (BIS) safety norms is unlocking institutional lending. Mobile kiosk formats now complement fixed cabinets, raising network density without equivalent real-estate costs. Fragmented pack designs, tax ambiguity, and import-dependent cell supply remain headwinds, yet domestic cell manufacturing under the Production-Linked Incentive (PLI) program is set to soften these risks.

Key Report Takeaways

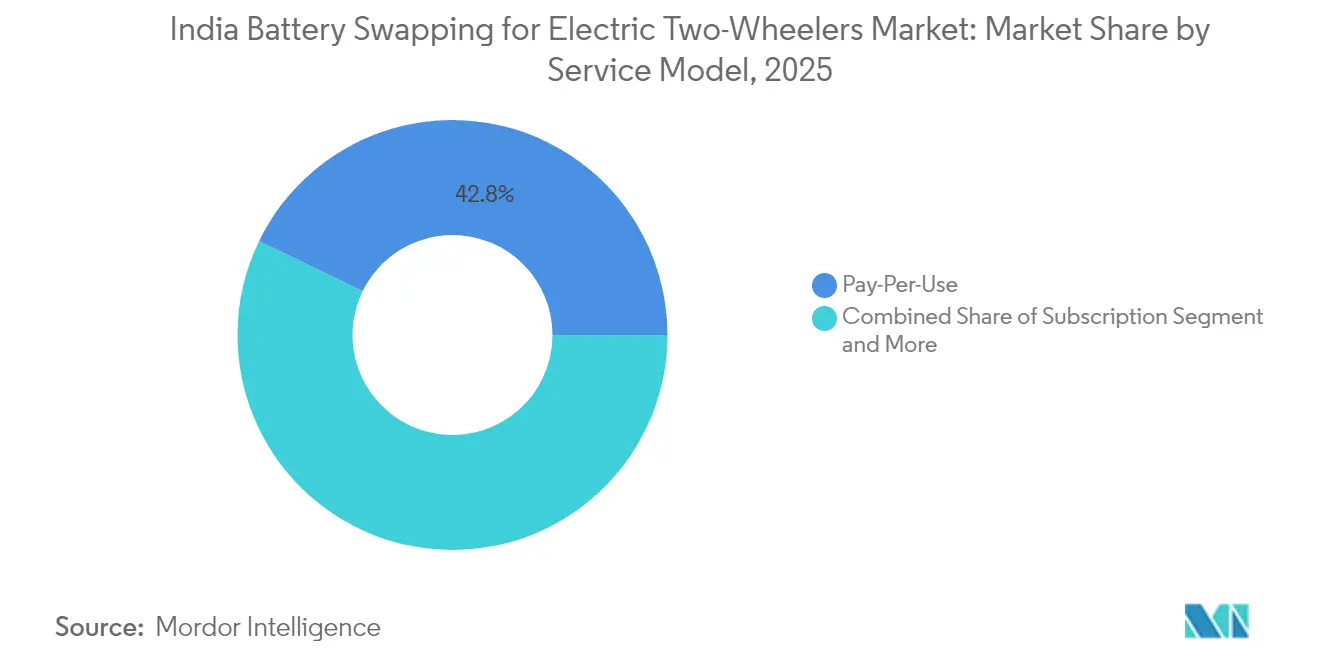

- By service model, the Pay-Per-Use option held 42.80% of the Indian battery swapping for electric two-wheelers market share in 2025, while subscription plans are projected to expand at a 27.36% CAGR through 2031.

- By battery chemistry, lithium-ion NMC/NCA commanded 62.40% of the Indian battery swapping for electric two-wheelers market size in 2025; lithium-iron-phosphate (LFP) variants are advancing at a 27.70% CAGR to 2031.

- By vehicle category, electric scooters captured 68.65% of the Indian battery swapping for electric two-wheelers market share in 2025, and electric motorcycles are forecast to post the fastest 28.10% CAGR through 2031.

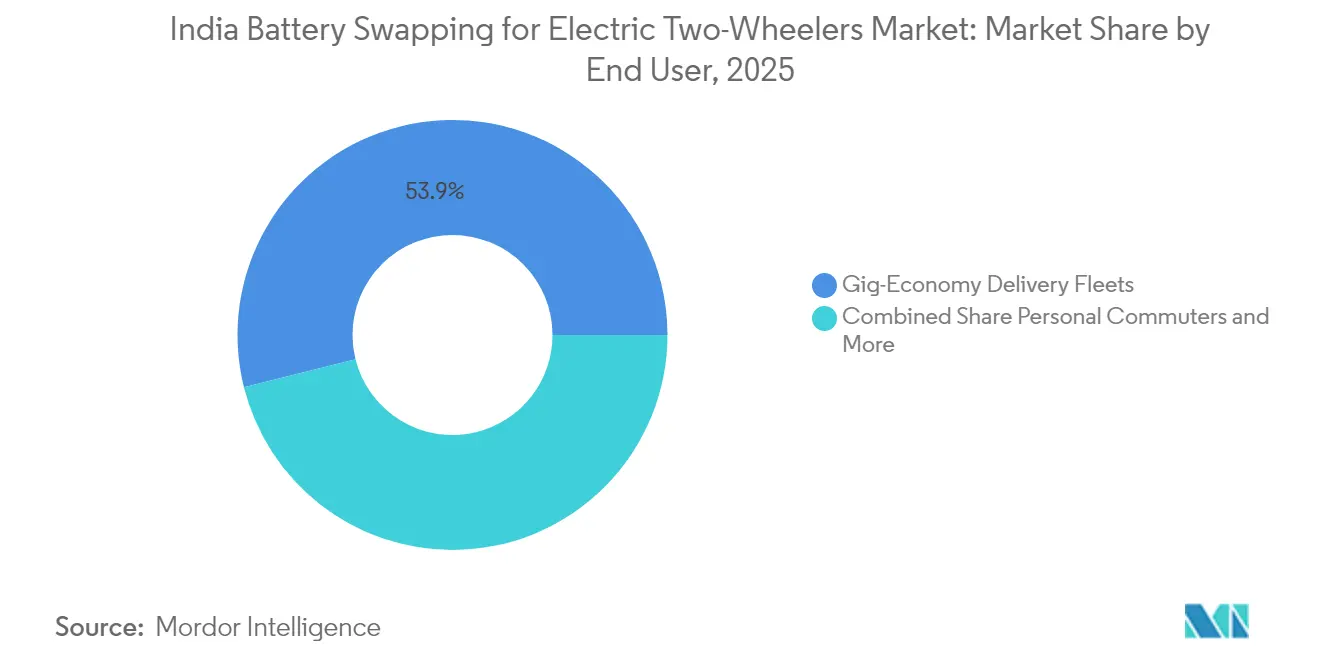

- By end user, gig-economy fleets accounted for a 53.90% share of the Indian battery swapping for electric two-wheelers market size in 2025 and are progressing at a 26.55% CAGR to 2031.

- By battery capacity, 2.1-3.0 kWh packs dominated with 62.95% of the Indian battery swapping for electric two-wheelers market share in 2025, whereas the 3.1-5.0 kWh band is projected to expand at a 26.40% CAGR through 2031.

- By swap station type, fixed cabinets led with 75.90% of the Indian battery swapping for electric two-wheelers market share in 2025; mobile kiosks are growing at a 27.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Battery Swapping For Electric Two-Wheelers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gig-Economy Downtime Demand | +6.3% | Metro delivery hubs | Short term (≤ 2 years) |

| VC and OMC Investments | +5.1% | Urban centers to Tier-II cities | Medium term (2-4 years) |

| FAME-II E2W Sales Growth | +4.2% | National; Maharashtra, Karnataka, Tamil Nadu | Short term (≤ 2 years) |

| Li-Ion Cost Decline | +3.9% | Tamil Nadu, Gujarat | Long term (≥ 4 years) |

| Battery Swapping Policy | +3.8% | National metro clusters | Medium term (2-4 years) |

| BIS Safety Standards | +2.7% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in E-Two-Wheeler Sales Via FAME-II Incentives

PM e-DRIVE was approved on June 26, 2025, with an outlay of ₹10,900 crore for 2024-25 to 2028-29 to support demand incentives for EVs. With the phasing out of previous subsidy schemes, manufacturers are channeling their efforts into innovation and operational efficiency to maintain price competitiveness. Adoption is rising, especially in states like Maharashtra, Karnataka, and Tamil Nadu, which offer extra incentives. This has led to a broader user base, many turning to battery-swapping infrastructure for its convenience and cost benefits.

Declining Li-Ion Costs and Localization of Pack Assembly

India is witnessing a pivotal shift in its battery ecosystem, with domestic production lines poised to commence operations. This transition aims to curtail import dependence, alleviate foreign exchange strains, and trim overall expenses. Lithium iron phosphate (LFP) is gaining traction among battery chemistries, especially for high-usage applications like swapping, due to its extended lifespan and cost-effectiveness compared to other options.

Domestic manufacturing fosters nimble supply chains, facilitating just-in-time deliveries and diminishing the necessity for extensive inventory. Moreover, standardized battery housings for robotic handling enhance operational efficiency. As these efficiencies accumulate, subscription costs are anticipated to decrease, broadening the accessibility of electric mobility and amplifying market reach.

Draft Battery Swapping Policy Enabling Interoperability

NITI Aayog’s draft framework specifies connector design, communications, and pack dimensions, removing the most significant barrier—platform fragmentation—by forcing OEM alignment[1]“Draft Battery Swapping Policy,”, NITI Aayog, niti.gov.in. BIS fire-safety testing complements the technical mandate, while clear liability definitions build lender confidence. Early rollouts in Delhi and Bengaluru serve as proof points, and phased geographic expansion is expected to trigger demand in Tier-II cities. Standardization curbs capex per station because operators carry fewer SKUs, and riders can choose any network, mirroring the convenience of gasoline refueling.

BIS Safety Standards Unlocking Financing and Insurance

BIS certification enforces thermal-runaway tests, ingress protection, and live data logging, reducing fire claims that once spooked insurers[2]“Safety Standards for Swappable Batteries,”, Bureau of Indian Standards, bis.gov.in. Standardized risk scores now allow underwriters to price premiums competitively, and lenders treat batteries as recoverable collateral, unlocking working-capital lines. IoT telemetry captures cycle counts, depth-of-discharge, and temperature anomalies, enabling predictive maintenance that sharply reduces catastrophic failures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fire Safety Concerns | -4.2% | Nationwide | Short term (≤ 2 years) |

| Fragmented Battery Formats | -3.4% | Nationwide | Medium term (2-4 years) |

| Import-Dependent Cell Supply | -2.8% | Nationwide | Long term (≥ 4 years) |

| GST Uncertainty on BaaS | -2.1% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fire-Safety Incidents Dent Consumer Confidence

Safety concerns loom large over the electric two-wheeler market, especially when incidents gain traction on social media. Even when fires stem from unauthorized aftermarket conversions, the public often generalizes the risk across the entire category.

While regulatory standards like BIS norms provide a framework for safer products, merely adhering to these standards isn't enough to rebuild consumer trust. To reassure price-sensitive buyers and maintain momentum in the shift to electric mobility, it's crucial to ensure consistent safety performance, conduct transparent investigations, and communicate incidents clearly.

Import-Dependent Cell Supply Exposed to Geo-Political Risk

India's battery supply chain, heavily dependent on Chinese imports, faces significant geopolitical and currency-related risks. Disruptions, be they trade tensions or currency fluctuations, can swiftly escalate costs or limit availability. This scenario compels operators to maintain larger inventories as a safeguard, tying up working capital and complicating financial planning—especially for the rapidly evolving electric mobility sector.

Although government-backed initiatives promise a surge in domestic production capacity in the coming years, the current landscape remains precarious. Until local manufacturing achieves scale, the sector will grapple with supply-chain volatility, jeopardizing cost stability and operational agility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Model: Subscription Plans Capture Fleet Wallet Share

Subscription plans increased their footprint even though the Pay-Per-Use option retained 42.80% of 2025 revenue. Commercial fleets value fixed monthly outlays and off-balance-sheet treatment, helping the subscription segment log a forecast 27.36% CAGR. Hero MotoCorp’s July 2025 VIDA VX2 launch separates chassis and battery financing, showcasing OEM agility in serving gig-economy clients.

Subscription contracts convert capex into opex, mitigating the 30-40% battery cost that often stalls purchases. Tiered plans from Battery Smart align pricing with daily-kilometer bands, ensuring fleets avoid overpaying during slack demand. Predictable revenue streams lower lenders’ risk, reducing interest burdens. Individual commuters still lean toward Pay-Per-Use to avoid fixed commitments, while fleet-leasing hybrids fill mid-tenure niches.

By Battery Chemistry: LFP Gains Traction on Cost and Safety

Lithium-ion NMC/NCA held 62.40% share in 2025, yet LFP’s 27.70% CAGR suggests the safety-value trade-off tilts in its favor. LFP’s 3,000–5,000 cycle life pairs naturally with high-throughput swapping, and inherent thermal stability curbs fire risks, a vital reputation safeguard.

OEM moves validate the shift: Ola Electric’s Gen 3 platform pivots to LFP, while domestic cell lines favor iron-phosphate chemistry due to raw-material availability. The India battery swapping for electric two-wheelers market size tied to LFP packs is forecast to close the gap with NMC by 2031 as vertical integration compresses pack costs. Lead-acid persists only in low-speed, sub-25 km/h vehicles, a niche eroding fast as lithium prices fall.

By Vehicle Category: Motorcycles Deliver the Next Wave

Scooters still ruled 68.65% of 2025 volumes, but motorcycles are sprinting at 28.10% CAGR thanks to Ola’s Roadster and upmarket entries from TVS and Hero. Higher payload and range make motorcycles attractive to inter-city couriers and ride-hail fleets, preparing the segment to narrow the share gap by decade’s end.

The India battery swapping for electric two-wheelers market share attributed to scooters remains robust in metro commuting, yet motorcycles are expected to dominate incremental growth. Mopeds continue to serve price-sensitive buyers exempt from licensing, but technology trickle-down and cheaper packs will erode this low-speed moat.

By End User: Gig-Economy Fleets Anchor Early Scale

Gig-platform fleets constituted 53.90% of 2025 demand, and ride-sharing subscriptions are rising at a 26.55% CAGR. Aggregated kilometers stabilize station loads, improving payback periods. Personal commuters lag due to station density and higher per-kilometer swap costs versus cheap home charging, but network expansion may unlock latent demand.

Platform-level procurement drives pack standardization as fleet operators pressure OEMs for interchangeable modules. The Indian battery swapping for electric two-wheelers market size linked to the gig economy will stay dominant until personal usage overtakes commercial kilometers in the latter half of the decade.

By Battery Capacity: Extended-Range Packs Scale Up

Packs between 2.1 kWh and 3.0 kWh held 62.95% share in 2025; 3.1–5.0 kWh variants are scaling at a 26.40% CAGR as riders seek longer routes without mid-shift swapping. Honda’s 1.5 kWh module for the Activa e: illustrates low-capacity standardization, while Ola’s dual-pack S1 Z covers 75–146 km ranges with modular add-ons.

Higher energy density and falling dollars per kWh reduce weight penalties, making bigger packs feasible without sacrificing handling. Extended-range packs let operators tier pricing by range bands when tied to subscription models, broadening consumer choice.

By Swap Station Type: Mobile Kiosks Bridge Accessibility Gaps

Fixed cabinets comprised 75.90% of active stations in 2025, but mobile kiosks are racing ahead at a 27.30% CAGR. These trailer-based or containerized units sidestep high street rents and expedite permits, crucial for dense markets like Delhi, where real estate costs stifle fixed deployment.

Mobile formats allow operators to pilot new catchments, relocating under-performing assets with minimal sunk cost. The Indian battery swapping for electric two-wheelers market size tied to mobile kiosks is modest today, yet pivotal for Tier-III towns that cannot sustain permanent infrastructure initially. As labor costs rise, automated robotic systems are emerging in premium hubs, while retail-integrated “battery ATMs” exploit existing foot traffic.

Geography Analysis

Maharashtra recorded 211,880 electric two-wheeler registrations in FY 2025, representing 18% of national volume, cementing its lead through additive state subsidies and a mature automotive cluster . Karnataka followed with 148,254 units, benefiting from Bengaluru’s tech ecosystem and Ather’s home-based effect. Tamil Nadu hosted 118,836 units and anchors the south-India manufacturing corridor, including Ola’s Gigafactory and TVS Motor.

India's EV adoption shows regional disparities, with Uttar Pradesh leading in total EV sales but lagging in electric two-wheeler uptake. This signals growth potential as battery-swapping infrastructure expands. Gujarat faces a slowdown, indicating early saturation and the need for renewed incentives. High real estate costs in Delhi hinder fixed swapping stations, but mobile kiosks offer a flexible solution. Localized strategies and infrastructure are crucial to unlocking India's electric two-wheeler market.

Regional deployment mirrors policy agility. Honda Power Pack Energy India is staging 500 swap stations across Bengaluru, Delhi, and Mumbai by March 2026 via partnerships with HPCL, metro rail operators, and Adani Electricity. Progressive states streamline land allotment and provide tariff rebates, shaving upfront costs. Demonstration success in these corridors galvanizes investor confidence to seed stations in secondary cities such as Coimbatore and Jaipur.

Competitive Landscape

Early station operators carved a share via speed-to-market, but scale now hinges on capital depth and strategic alliances. Battery Smart surpassed 1,000 stations in 2024 across 30 cities after attracting Tiger Global and responsAbility debt, holding nearly 15% of operational cabinets. Sun Mobility, partnered with Indian Oil Corporation, leverages national pump networks to roll out multi-format stations, while RACEnergy dominates in the three-wheeler niche.

OEM integration is a rising moat. Ola Electric’s vertical stack combines cell production, battery management systems, and vehicle hardware, lowering the bill of materials and tightening feedback loops. Honda’s dedicated subsidiary injects global quality benchmarks and retail muscle, raising the competitive bar. Smaller independents are responding with interoperability coalitions and co-branded packs to avoid isolation in a standardizing ecosystem.

M&A chatter is increasing as infrastructure intensity demands larger balance sheets. Sun Mobility has signaled its intent to acquire regional players to achieve sub-1 km urban station radii. Battery Smart is exploring franchise models to accelerate market entry in Tier-II towns, promising financiers minimum-guarantee returns. Overall, competitive dynamics are moving from land-grab to network-effect monetization, where customer lock-in derives from densest coverage and lowest swap downtime.

India Battery Swapping For Electric Two-Wheelers Industry Leaders

Ola Electric Mobility Ltd.

SUN Mobility

RACE Energy Limited

Upgrid Solutions Private Limited (Battery Smart)

Gogoro

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hero MotoCorp introduced a Battery-as-a-Service subscription for its VIDA VX2, offering nationwide fast-charging, access to over 500 service outlets, and a convenient solution for electric vehicle users to enhance their charging experience. This initiative aims to address range anxiety and improve the adoption of electric mobility across the country.

- November 2024: Honda Power Pack Energy India secured INR 2.2 billion to expand its two-wheeler battery swapping infrastructure, enhance operational capabilities, and support the growing demand for electric mobility solutions in India.

India Battery Swapping For Electric Two-Wheelers Market Report Scope

In battery swapping, EV owners visit the swapping stations and swap out their exhausted batteries for charged ones. It reduces drivers' range anxiety and aids in resolving the issue of installing charging stations. In addition, leasing batteries can help EV owners avoid the expense of outright battery purchases. It takes the least amount of time and infrastructure to charge at a battery station, a process that could take several hours. The Indian battery swapping for electric two-wheeler market is segmented by service type into the pay-per-use and subscription models. By battery type, the market is segmented as lead-acid and lithium-ion. The market size and forecast for each segment have been calculated based on value (USD billion).

By Service Model

| Pay-Per-Use |

| Subscription |

| Fleet Leasing (Long-Term) |

By Battery Chemistry

| Lithium-ion (NMC/NCA) |

| Lithium-ion (LFP) |

| Lead-acid |

By Vehicle Category

| Electric Scooters |

| Electric Motorcycles |

| Electric Mopeds |

By End User

| Personal Commuters |

| Gig-Economy Delivery Fleets |

| Ride-Sharing / Subscription Platforms |

By Battery Capacity (kWh)

| Up to 2.0 |

| 2.1-3.0 |

| 3.1-5.0 |

| Above 5.0 |

By Swap Station Type

| Fixed Cabinet |

| Mobile Kiosk |

| Fully-Automated Robotic |

| Retail-Outlet Integrated (Battery ATM) |

| By Service Model | Pay-Per-Use |

| Subscription | |

| Fleet Leasing (Long-Term) | |

| By Battery Chemistry | Lithium-ion (NMC/NCA) |

| Lithium-ion (LFP) | |

| Lead-acid | |

| By Vehicle Category | Electric Scooters |

| Electric Motorcycles | |

| Electric Mopeds | |

| By End User | Personal Commuters |

| Gig-Economy Delivery Fleets | |

| Ride-Sharing / Subscription Platforms | |

| By Battery Capacity (kWh) | Up to 2.0 |

| 2.1-3.0 | |

| 3.1-5.0 | |

| Above 5.0 | |

| By Swap Station Type | Fixed Cabinet |

| Mobile Kiosk | |

| Fully-Automated Robotic | |

| Retail-Outlet Integrated (Battery ATM) |

Key Questions Answered in the Report

How big is India’s battery-swapping opportunity for electric two-wheelers in 2026?

The India battery swapping for electric two-wheelers market size stands at USD 33.59 million in 2026.

What CAGR is projected for battery-swapping between 2026 and 2031?

The market is expected to grow at a 25.72% CAGR over the forecast period.

Which service model is growing fastest?

Subscription plans are expanding at 27.36% CAGR as fleets favor predictable monthly costs.

Why are LFP batteries gaining share?

LFP chemistry offers 20-30% lower costs and stronger safety credentials, supporting a 27.70% CAGR through 2031.

Which Indian state leads two-wheeler electrification?

Maharashtra leads with 211,880 units in FY 2025, accounting for 18% of national sales.

Who are the major players in swapping infrastructure?

Battery Smart, Sun Mobility, RACEnergy, Ola Electric, and Honda Power Pack Energy India are the most active operators.

Page last updated on: