Digital Transformation In Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

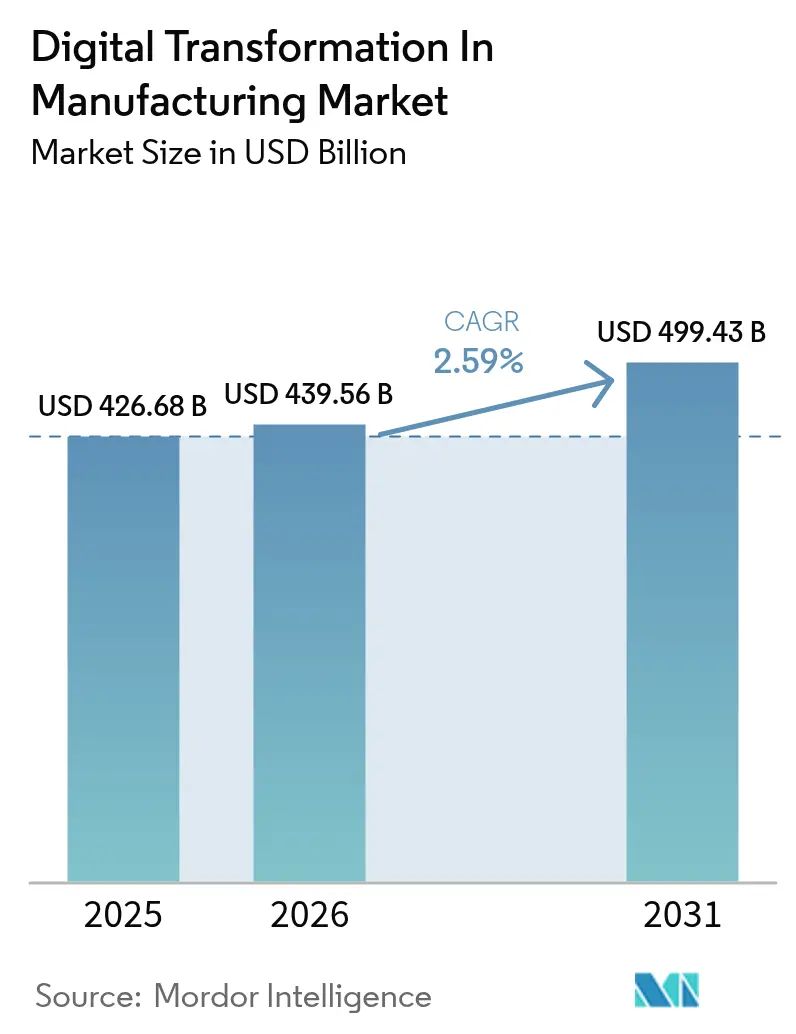

| Market Size (2026) | USD 439.56 Billion |

| Market Size (2031) | USD 499.43 Billion |

| Growth Rate (2026 - 2031) | 2.59% CAGR |

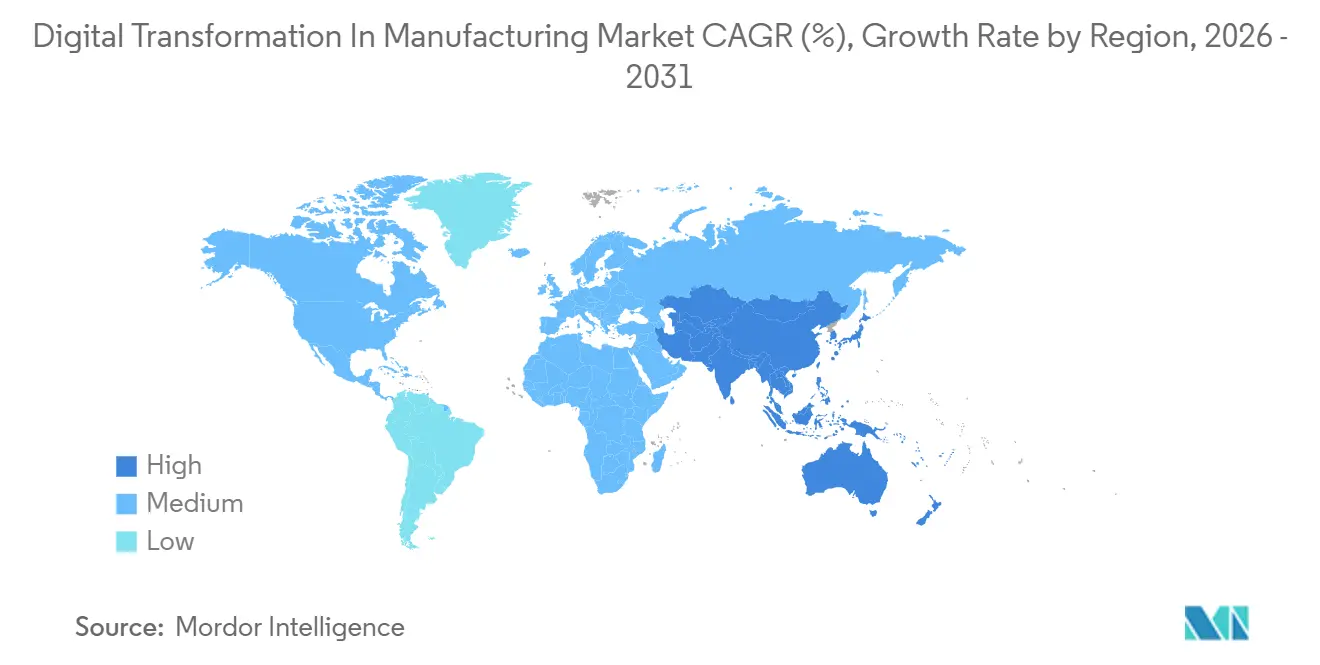

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

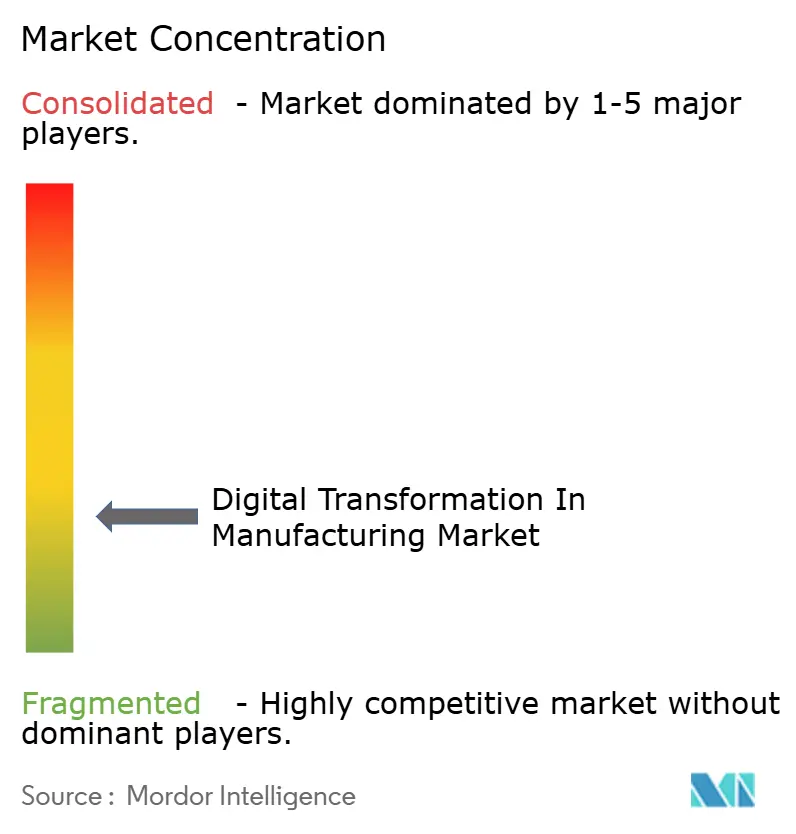

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Transformation In Manufacturing Market Analysis by Mordor Intelligence

The digital transformation in manufacturing market size is projected to be USD 426.68 billion in 2025, USD 439.56 billion in 2026, and reach USD 499.43 billion by 2031, growing at a CAGR of 2.59% from 2026 to 2031. Growth is moderating because factories are moving from quick, connectivity-only retrofits toward complex greenfield facilities that embed simulation, artificial intelligence and private 5G from day one. Vendors with vertically integrated hardware and software portfolios now differentiate through low-code configurability rather than proprietary protocols, which helps manufacturers shorten implementation cycles and curb vendor lock-in. Public-private incentives that tie disbursements to tangible productivity targets are accelerating first-time adoption among small and medium enterprises, while data-sovereignty rules in Europe and China are forcing large multinationals to engineer multi-cloud architectures. Finally, persistent cybersecurity risk tied to aging programmable logic controllers is pushing board-level budgets toward zero-trust architectures and continuous remediation programs.

Key Report Takeaways

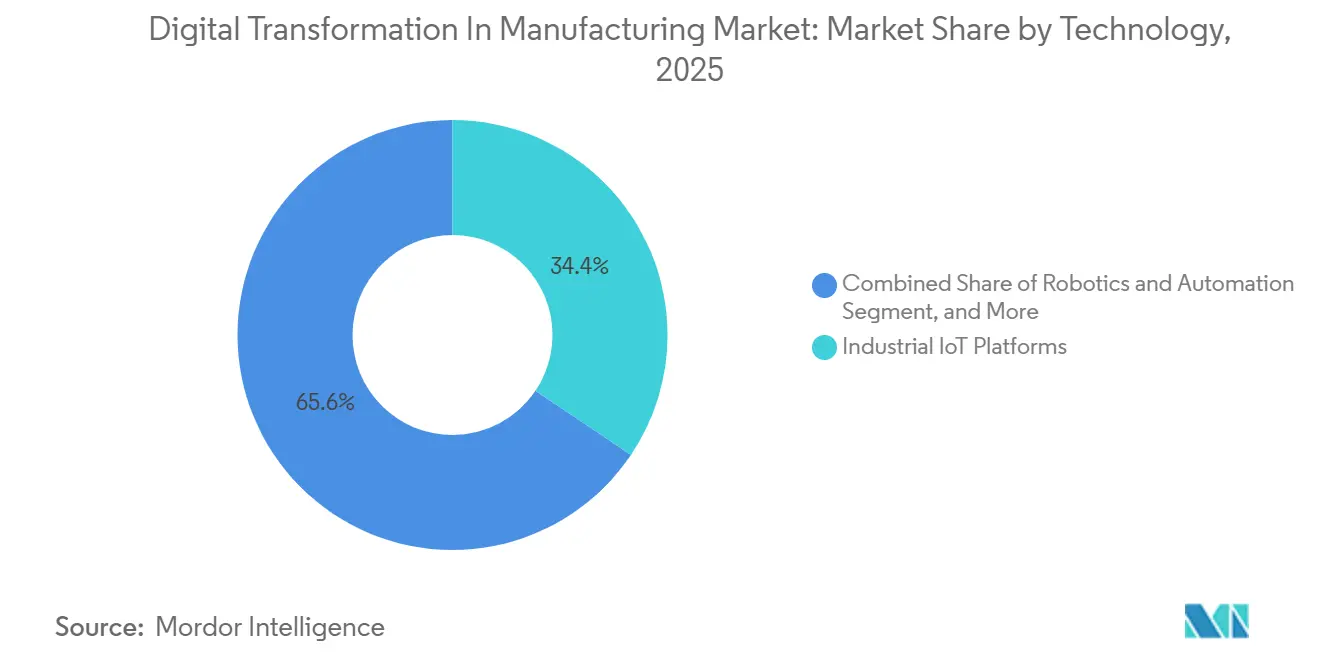

- By technology type, industrial IoT platforms led with 34.42% of the digital transformation in manufacturing market share in 2025. Digital twin and simulation tools are projected to expand at a 3.47% CAGR to 2031.

- By deployment mode, on-premises held 56.91% share of the digital transformation in manufacturing market size in 2025. Hybrid and edge configurations are forecast to grow at a 4.82% CAGR over 2026-2031.

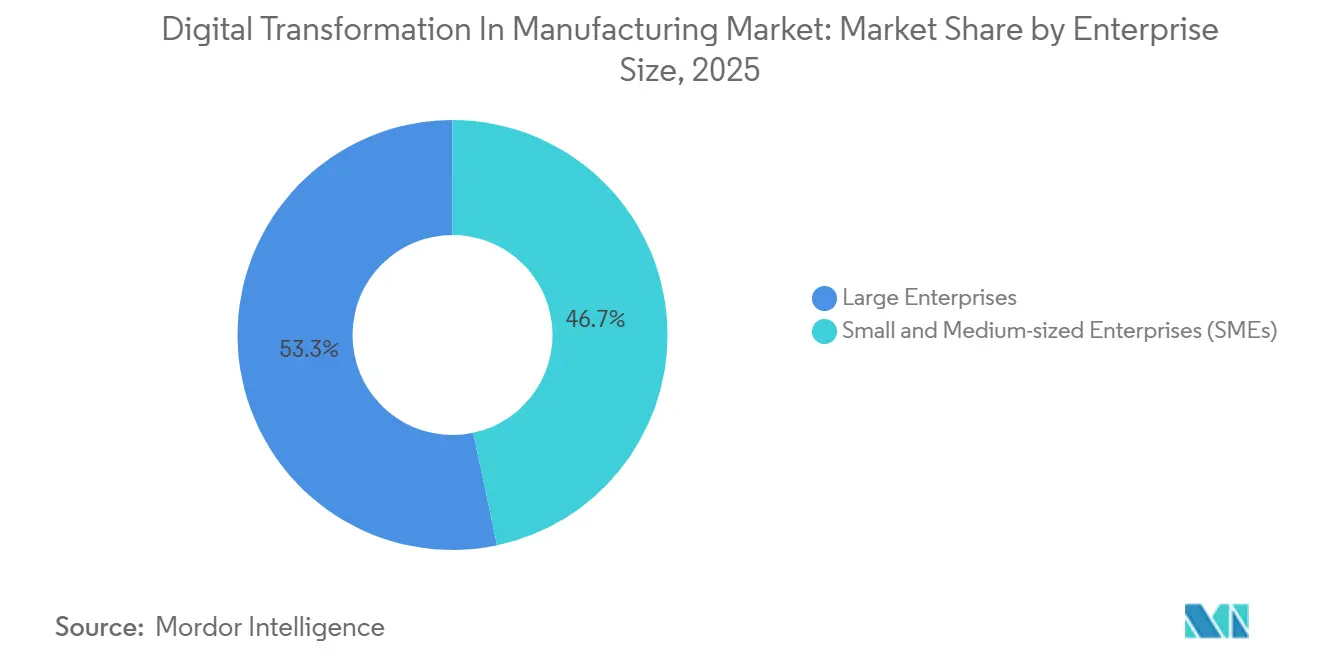

- By enterprise size, large enterprises commanded 53.32% of 2025 spending, while small and medium enterprises are pacing ahead at a 3.31% CAGR through 2031.

- By end-user industry, automotive captured 28.83% revenue share in 2025, and electronics and semiconductors are advancing at 3.63% CAGR to 2031.

- By geography, North America accounted for 38.41% of 2025 revenue, whereas Asia-Pacific is the fastest growing region with a 3.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Transformation In Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Industrial IoT Platforms | +0.8% | Global hubs in North America, Europe and Asia-Pacific | Medium term (2-4 years) |

| Rapid Shift to Cloud-Native MES and SaaS | +0.6% | North America and Europe lead, Asia-Pacific accelerating | Short term (≤ 2 years) |

| Government Incentives for Industry 4.0 | +0.5% | China, India, South Korea, Germany, France, United States, Canada | Medium term (2-4 years) |

| Availability of Private 5G Networks | +0.4% | Early in North America and Europe, scaling in Asia-Pacific | Long term (≥ 4 years) |

| Surge in Digital Product Passports | +0.3% | Europe driven, spillover to exporters in North America and Asia-Pacific | Short term (≤ 2 years) |

| Quantum-Inspired Optimization Integration | +0.2% | Semiconductor and aerospace clusters in United States, Taiwan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Industrial IoT Platforms

Industrial IoT platforms now embed predictive maintenance and in-line quality analytics directly in production cells, cutting unplanned downtime for automotive and aerospace producers by up to 40%.[1]BMW Group, “BMW Digital Factory Integration,” bmwgroup.com Automakers that unify robots, automated guided vehicles and test benches under one digital thread have shortened model changeovers from weeks to days, which frees capacity for personalized trim packages. Private 5G removes the latency that once forced controllers to stay hard-wired, making IoT the de facto nervous system of next-generation plants.[2]Hyundai-Samsung Private 5G Case, samsung.com Early adopters report yield gains that compound every quarter because anomaly-detection algorithms continuously retrain on streaming sensor data. Delayed adopters risk permanent cost disadvantages as digital work-instructions and self-healing lines become standard procurement requirements.

Rapid Shift to Cloud-Native MES and SaaS Solutions

Subscription MES platforms replace cap-ex heavy historians and supervisory systems, allowing multi-site planners to rebalance production with a browser instead of weeks of ERP reconfiguration.[3]SAP SE, “S/4HANA Cloud for Manufacturing,” sap.com More than one thousand plants moved core execution to the cloud during 2025, attracted by pay-as-you-go pricing that falls well below the half-million-dollar perpetual licenses of legacy suites. Virtualized controllers hosted on local outposts let safety-critical loops stay on-premises, while dashboards, machine learning training and supplier portals scale elastically off-premises. The model lowers barriers for small and medium enterprises that previously lacked data centers or DevOps teams, leveling the playing field across the digital transformation in manufacturing market.

Government Incentives for Industry 4.0 Adoption

Targeted subsidies and tax credits tie financial support to proof of Industry 4.0 deployment, channeling billions of USD into sensors, edge gateways and cloud connectors. Asian programs emphasize production-volume expansion, European funds reward compliance with Gaia-X data-sovereignty standards, and North American legislation focuses on reshoring critical supply chains. While objectives differ, every program forces vendors to deliver measurable overall-equipment-effectiveness improvements within eighteen months, stimulating demand for plug-and-play analytics and open APIs. Divergent regional requirements, however, compel global manufacturers to operate multiple technology stacks, complicating maintenance and talent allocation.

Availability of Private 5G Networks for Ultra-Reliable Low-Latency Control

Factory-wide private 5G replaces kilometers of Ethernet, supporting flexible lines that can rearrange in hours rather than weeks. Deployments show installation savings exceeding USD 3 million per large site and latency below ten milliseconds for coordinated fleets of mobile robots. Tight time-sensitive networking profiles ensure collision avoidance commands execute even during traffic bursts, making cable-less layouts viable for heavy payload handling. The network’s determinism also unlocks augmented reality and edge AI on moving platforms, widening the addressable use cases within the digital transformation in manufacturing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills Shortage in OT-IT Convergence | -0.5% | Global, acute in North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Escalating Cybersecurity Vulnerabilities | -0.4% | Brownfield sites in North America, Europe and Asia-Pacific | Short term (≤ 2 years) |

| Proprietary Data-Sovereignty Clauses | -0.2% | Europe, China, spillover to multinationals | Long term (≥ 4 years) |

| Hidden Carbon Footprint of HPC Clusters | -0.1% | Global, regulation strongest in Europe and California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skills Shortage in OT-IT Convergence

Manufacturers lack engineers who can code Python and also troubleshoot ladder logic, stretching project timelines by up to two years. Training academies graduate hundreds yet demand runs into thousands, making talent the scarcest resource in the digital transformation in manufacturing industry. The deficit widens competitive gaps because large enterprises fund internal boot camps, while mid-tiers must wait for vendor professional services, adding direct cost and lost opportunity. Automation suppliers respond with low-code interfaces, but complex edge analytics still requires domain specialists, so human capital remains the bottleneck.

Escalating Cybersecurity Vulnerabilities Across Brown-Field Assets

Legacy controllers installed before modern authentication standards now sit on converged networks, exposing unpatched Modbus and EtherNet/IP stacks to ransomware.[4]Honeywell International Inc., “Industrial Cybersecurity Report,” honeywell.com Incident volumes jumped nearly fifty percent year-over-year, forcing plants to consider costly network segmentation or full controller replacement. Automated patch-management tools exist yet adoption lags amid fears that downtime will disrupt delivery schedules. Regulatory frameworks such as IEC 62443 convert what was once optional into a license-to-operate obligation, redirecting discretionary budgets from analytics innovation toward basic cyber hygiene.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: IoT Platforms Provide the Foundation While Digital Twins Gain Velocity

Industrial IoT platforms captured 34.42% of the digital transformation in manufacturing market share in 2025, underscoring their position as the first layer of connectivity that links shop-floor sensors, controllers and enterprise applications. This portion of the digital transformation in manufacturing market size channels real-time machine data into unified data lakes, allowing predictive maintenance algorithms to cut unplanned downtime by double-digit percentages. IoT adoption is now broad enough that incremental value shifts toward higher-order applications, and that shift explains why digital twin and simulation tools are scaling at a 3.47% CAGR through 2031. Manufacturers use virtual replicas to stress-test assembly sequences, validate ergonomics and pre-train machine-learning models before hardware is on the floor, shrinking program launches from months to weeks.

Spending on robotics, additive manufacturing and augmented reality remains meaningful but grows more slowly, because most early movers prefer to extract additional yield from existing cells rather than install more hardware. Cybersecurity, once an afterthought, now appears on capital budgets as a distinct line item because every new device widens the threat surface. Edge processors packed into vision systems keep terabytes of images local, slashing bandwidth fees and enabling sub-second inspection feedback loops that human eyes cannot match. Over the forecast window, technology choices will be driven less by feature counts and more by how seamlessly each layer plugs into open APIs, so that future upgrades can happen without re-engineering the entire stack.

By Deployment Mode: Hybrid Architectures Turn Latency into a Manageable Variable

On-premises installations held 56.91% of spending in 2025, reflecting a long-standing preference for tight control over safety-critical loops and intellectual property. That dominance is eroding as hybrid and edge configurations record the fastest 4.82% CAGR, removing the binary choice between plant-floor responsiveness and cloud scalability. Production teams now place deterministic motion control on micro-data-centers a few meters from the line, while training deep-learning models in hyperscale regions overnight. This split architecture trims image-transfer bandwidth by roughly 80% and lets manufacturers stay compliant with data-sovereignty clauses without forgoing analytics firepower.

Pure cloud models still appeal for supplier collaboration, energy dashboards and sustainability reporting, where millisecond latency is not mission-critical. The lesson for buyers is that deployment is becoming an ongoing workload-balancing exercise rather than a one-time infrastructure bet. Vendors that automate this orchestration create tangible cost and performance advantages, because plant personnel no longer need to manage IP addresses or spin up virtual machines on Friday night shifts. As private 5G and containerized control software mature, the digital transformation in manufacturing market will treat connectivity and compute location as levers that can be pulled and reset whenever takt times, regulatory demands or product mixes change.

By Enterprise Size: SaaS Lowers the Barrier for Small and Mid-Sized Firms

Large corporations captured 53.32% of 2025 outlays thanks to multi-site footprints and the capacity to fund custom analytics teams. However, cloud-native subscriptions priced in the low five figures now allow plants with fewer than 500 employees to retire clipboards and paper travelers. These SaaS packages bundle sensors, dashboards and pre-trained defect-detection models, so supervisors can digitize work instructions over a weekend without coding. The result is a 3.31% CAGR for small and medium enterprises, outpacing the expansion rate of their larger peers.

Democratization is also visible in robotic process automation that offloads repetitive paperwork for a fraction of a full-time salary. As skill gaps persist, low-code interfaces remove the need for Python or ladder-logic fluency, letting operators adjust dashboards in real time instead of filing IT tickets. Volume discounts and professional-services clout still tilt procurement advantages toward conglomerates, yet the playing field is flatter than just two years ago. In the next cycle, customer audits that mandate digital traceability will transform these once-optional upgrades into table stakes for every tier of the supply base.

By End-User Industry: Automotive Still Commands Spend, Semiconductors Set the Pace

Automotive makers generated 28.83% of 2025 revenue by synchronizing battery modules, power-electronics and final assembly under unified execution layers. Tight takt times force plants to harness live torque data and vision analytics, converting every station into an IIoT node that feeds enterprise resource-planning systems with second-by-second status. Meanwhile, electronics and semiconductor fabs post the quickest 3.63% CAGR because quantum-inspired schedulers are now essential for handling the combinatorial complexity of sub-3-nanometer wafer steps. Those schedulers reallocate lots on the fly, lifting overall equipment effectiveness without staff increases.

Aerospace lines deploy blockchain-anchored records so inspectors can verify part genealogy in minutes, satisfying stringent regulator demands. Pharmaceutical packaging retrofits barcode verifiers to each blister and vial, closing gaps before tougher serialization deadlines take effect. Food and beverage plants wire cold-storage doors with temperature probes that trigger alerts when compressors drift from specification, preventing spoilage and protecting slim margins. Across all verticals, buyers show a willingness to fund upgrades when the payback period lands inside two fiscal years, and that threshold now applies to advanced analytics just as much as to traditional automation.

Geography Analysis

Asia-Pacific posts the highest 3.54% annual growth as Beijing and New Delhi channel USD 57 billion of incentives into domestic IoT and analytics providers. Chinese subsidies mandate local stack procurement, fostering parallel ecosystems around Huawei and Alibaba Cloud and reshaping competitive dynamics of the digital transformation in manufacturing market. Indian disbursements reward ISO 9001 certification tied to sensor-based quality, pulling small component makers onto data platforms. Japan and South Korea focus on robotics and front-end semiconductor automation, while Southeast Asian electronics hubs demand end-to-end digital traceability to win European orders.

North America retains 38.41% of 2025 sales thanks to early electric-vehicle and aerospace adopters and the presence of the three largest hyperscale clouds. U.S. gigafactories already coordinate thousands of autonomous mobile robots over private 5G, and federal energy-efficiency grants steer plants toward edge AI that trims electricity peaks. Canada pilots digital twins for battery assembly, and Mexico attracts near-shored suppliers that need real-time visibility to guarantee two-hour delivery windows.

Europe sits between rapid adoption and regulatory friction. The Digital Product Passport rule, enforceable in 2027, forces battery and textile producers to embed immutable serialization, accelerating migration to blockchain-ready clouds yet splintering analytics across data-sovereign zones. Germany’s EUR 140 million (USD 158 million) Manufacturing-X vouchers subsidize half of small enterprise platform costs, France funds aerospace inspection automation, and the United Kingdom offers twenty-five percent tax relief on robotics. South America concentrates spending in Brazil and Argentina across automotive and food chains, while the Middle East funds greenfield smart factories through sovereign wealth channels. Africa’s pilots remain small but rising power-stability investments may unlock broader programs later in the decade.

Competitive Landscape

The digital transformation in manufacturing market remains moderately fragmented, with the ten largest vendors together holding about 45% of 2026 revenue. Siemens and Schneider Electric stand out for end-to-end portfolios that bundle PLCs, edge appliances and cloud analytics, enabling single-contract rollouts that appeal to risk-averse multinationals. Microsoft, AWS and Google push the opposite strategy by commoditizing ingestion, storage and machine-learning platforms, leaving domain-specific value to ecosystems of independent software vendors. Start-ups such as Tulip Interfaces and UiPath exploit this openness by offering no-code tools that operators can deploy without waiting for an integrator, eroding traditional professional-services revenue streams.

Strategic moves in 2025 illustrate the race to own higher-margin software layers. Siemens pledged USD 450 million to infuse quantum-inspired scheduling into its Xcelerator platform, positioning itself for next-generation semiconductor fabs that cannot hit yield targets with classical algorithms. Rockwell Automation folded Plex Systems into FactoryTalk, creating a cloud-edge suite that shortens implementation timelines for tier-1 auto suppliers juggling just-in-sequence windows. ABB bought a majority stake in a German edge-AI specialist, embedding path-planning intelligence directly in robot drives so customers can slash commissioning time without installing additional servers.

Interoperability rather than raw feature counts now decides many deals, because manufacturers fear tech-stack lock-in that could become costly when regulations change. Vendors answer by joining working groups and publishing open APIs, even as they file patents on optimization methods and energy-efficiency heuristics. Compliance credentials also sway purchasing decisions; suppliers that arrive with IEC 62443 or ISO 9001 audit letters in hand shorten sales cycles by months. This shifting battlefield favors companies that can balance openness, cybersecurity assurances and rapid innovation, suggesting that partnership ecosystems will weigh as heavily as product roadmaps when market share is contested over the next five years.

Digital Transformation In Manufacturing Industry Leaders

Cisco Systems Inc.

Microsoft Corporation

Intel Corporation

IBM Corporation

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Siemens announced a USD 450 million expansion of its Xcelerator platform to include quantum-inspired scheduling that cuts semiconductor cycle time by up to fifteen percent.

- December 2025: Rockwell Automation completed Plex Systems integration, signing eighty-seven new automotive tier-1 customers for its unified cloud-edge execution suite.

- November 2025: Schneider Electric released EcoStruxure Automation Expert 2.0, virtualizing controllers and trimming commissioning by forty percent across European food plants.

- October 2025: Microsoft and BMW extended Azure IoT and HoloLens 2 to thirty-one factories, reducing mean-time-to-repair by thirty-eight percent.

Global Digital Transformation In Manufacturing Market Report Scope

The digital transformation market in manufacturing is defined based on the revenues generated from the technologies such as robotics, IoT, 3D printing and additive manufacturing, cybersecurity, and artificial intelligence, used globally. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the market's growth in terms of drivers and restraints.

The Digital Transformation in Manufacturing Market Report is Segmented by Technology Type (Industrial IoT Platforms, Robotics and Automation, Additive Manufacturing and 3D Printing, Digital Twin and Simulation, Cyber-Security Solutions, Cloud MES, AI and Advanced Analytics, AR and VR, Edge Computing Infrastructure, Other Technology Types), Deployment Mode (On-Premises, Cloud, Hybrid and Edge), Enterprise Size (Large Enterprises, SMEs), End-User Industry (Automotive, Aerospace and Defense, Electronics and Semiconductors, Chemicals and Materials, Food and Beverage, Pharmaceuticals and Medical Devices, Heavy Machinery and Industrial Equipment, Consumer Goods, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Industrial IoT Platforms |

| Robotics and Automation |

| Additive Manufacturing and 3D Printing |

| Digital Twin and Simulation |

| Cyber-Security Solutions |

| Cloud Manufacturing Execution Systems |

| Artificial Intelligence and Advanced Analytics |

| Augmented and Virtual Reality |

| Edge Computing Infrastructure |

| Other Technology Types |

| On-Premises |

| Cloud |

| Hybrid and Edge |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Automotive |

| Aerospace and Defense |

| Electronics and Semiconductors |

| Chemicals and Materials |

| Food and Beverage |

| Pharmaceuticals and Medical Devices |

| Heavy Machinery and Industrial Equipment |

| Consumer Goods |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South East Asia | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Technology Type | Industrial IoT Platforms | |

| Robotics and Automation | ||

| Additive Manufacturing and 3D Printing | ||

| Digital Twin and Simulation | ||

| Cyber-Security Solutions | ||

| Cloud Manufacturing Execution Systems | ||

| Artificial Intelligence and Advanced Analytics | ||

| Augmented and Virtual Reality | ||

| Edge Computing Infrastructure | ||

| Other Technology Types | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid and Edge | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-User Industry | Automotive | |

| Aerospace and Defense | ||

| Electronics and Semiconductors | ||

| Chemicals and Materials | ||

| Food and Beverage | ||

| Pharmaceuticals and Medical Devices | ||

| Heavy Machinery and Industrial Equipment | ||

| Consumer Goods | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South East Asia | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the digital transformation in manufacturing market in 2026?

The market is valued at USD 499.88 billion in 2026 and is forecast to grow rapidly through 2031.

What is the expected CAGR for digital transformation initiatives in manufacturing?

A 13.61% CAGR is projected for the 2026-2031 period.

Which technology segment currently holds the largest share?

Industrial IoT platforms lead with 34.41% share in 2025.

Which region is growing the fastest?

Asia Pacific is set to expand at a 14.16% CAGR through 2031.

What segment shows the quickest growth among end-user industries?

Electronics and semiconductors are advancing at a 13.82% CAGR.

How fragmented is the competitive landscape?

The market scores 5 on a 1-10 concentration scale, reflecting moderate fragmentation.

Page last updated on: