India Decorative Laminates Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.32 Billion |

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.81 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Decorative Laminates Market Analysis by Mordor Intelligence

The India Decorative Laminates Market size was valued at USD 1.32 billion in 2025 and estimated to grow from USD 1.39 billion in 2026 to reach USD 1.81 billion by 2031, at a CAGR of 5.35% during the forecast period (2026-2031). Ongoing residential construction, rising modular furniture penetration, and regulatory moves toward ultra-low formaldehyde grades are driving steady volume growth while increasing input cost complexity. Particle board and medium-density fiberboard remain the core substrates; however, adhesive suppliers are capturing incremental value as manufacturers reformulate to meet the IS 12592:2023 emission limits. Digital printing is enabling mid-tier producers to offer premium aesthetics at lower minimum order sizes, thereby fragmenting design leadership. At the same time, sharp swings in phenolic and melamine resin prices are compressing margins and rewarding players with backward integration or long-term supply contracts. Competitive pressure remains intense because unorganized factories still dominate the volume, although capacity additions by organized leaders signal an accelerating formalization.

Key Report Takeaways

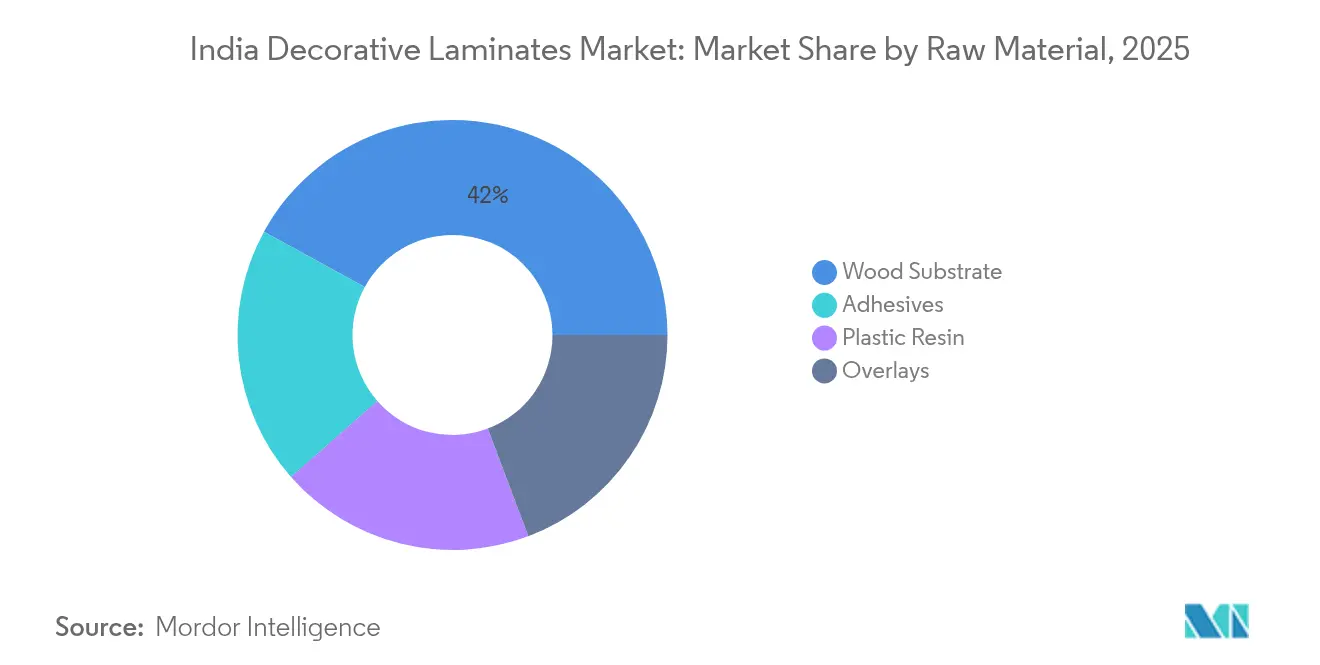

- By raw material, the Wood Substrate segment accounted for 42.02% of India decorative laminates market share in 2025. Adhesives are forecasted to grow at the fastest rate within raw materials, with a 6.05% CAGR through 2031.

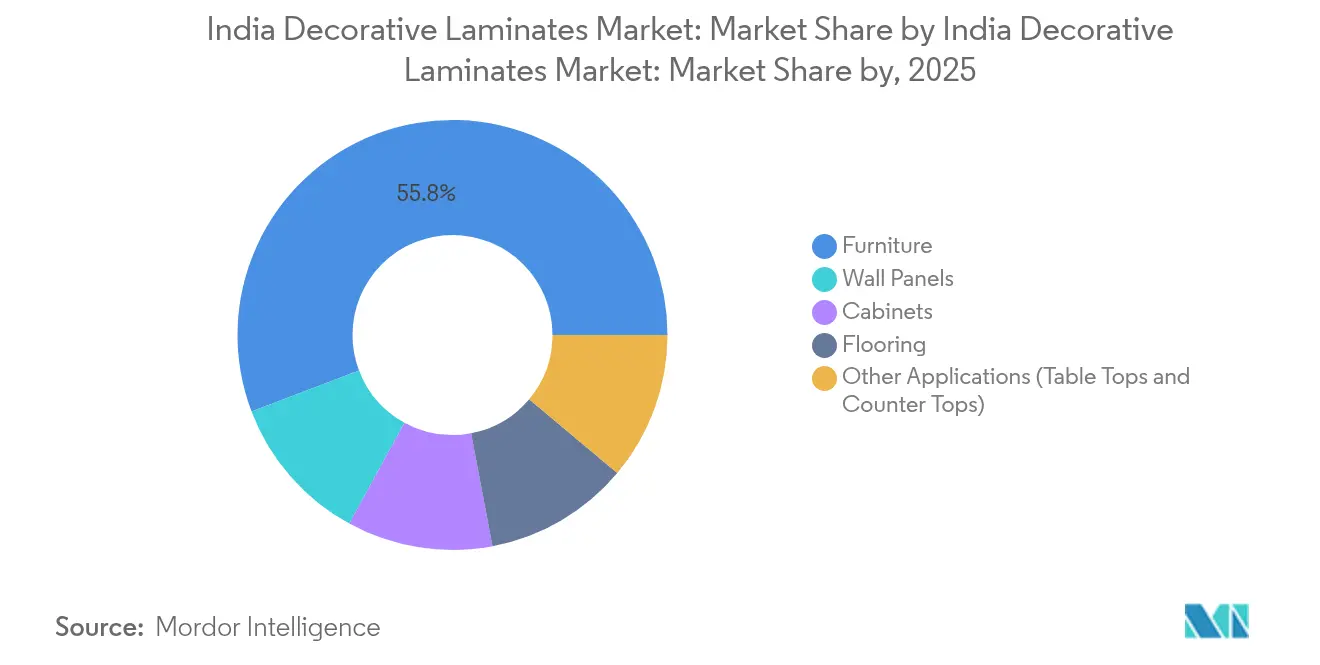

- By application, Furniture led with 55.78% revenue share of India decorative laminates market size in 2025. Wall panels are expected to post the highest growth rate at a 6.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on decorative laminates market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Decorative Laminates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of residential real-estate and affordable-housing schemes | +1.8% | Maharashtra, Gujarat, Karnataka, Tamil Nadu | Medium term (2-4 years) |

| Shift to modular furniture and organised retail channels | +1.5% | Mumbai, Delhi, Bengaluru, Pune, Ahmedabad | Short term (≤ 2 years) |

| Digital-printing tech enabling mass-premium custom decors | +0.9% | Early adoption in Gujarat and Maharashtra | Medium term (2-4 years) |

| Government incentives for low-VOC / E0 grade surfaces | +0.7% | National | Long term (≥ 4 years) |

| Export boom from India under “China-plus-one” sourcing | +0.6% | Gujarat, Andhra Pradesh, Punjab | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Residential Real-Estate and Affordable-Housing Schemes

India delivered 406,889 new homes in fiscal 2025, representing a 33% year-over-year increase, while the luxury category saw sales growth of 28-85% across major metros[1]India Brand Equity Foundation, “Real Estate Annual Update 2025,” ibef.org. This build-out feeds direct demand for laminates in kitchens, wardrobes, and wall panels. Developers favor pre-laminated particle board and MDF to shorten project cycles and control budgets, locking in high-volume purchases from organized distributors. Government programs such as Pradhan Mantri Awas Yojana enhance momentum in the sub-₹50 lakh bracket. As urbanization pushes India’s city population above 600 million by 2030, manufacturers that secure supply agreements with turnkey fit-out firms are positioned for sustained sheet-volume gains.

Shift to Modular Furniture and Organised Retail Channels

Factory-built modular units are replacing on-site carpentry, reshaping laminate specification and distribution. Large chains, including IKEA, Pepperfry, and Godrej Interio, are scaling into tier-2 cities, demanding certified laminates with uniform quality for flat-pack logistics. Dealer expansion models such as CenturyPly’s “Fix Day Fix Route” have added more than 500 outlets in a single fiscal year, cementing channel reach. Each urban modular kitchen consumes 15-25 sheets, and penetration has risen to an estimated 25% of new homes in metropolitan areas. Rising expectations around anti-fingerprint coatings and synchronized wood-grain textures are pushing unorganized mills to either upgrade or exit.

Digital-Printing Tech Enabling Mass-Premium Custom Decors

Investments in single-pass inkjet lines enable photo-realistic wood, stone, and fabric finishes without the need for expensive rotogravure cylinders, thereby cutting design lead times from months to days. Launches such as Greenlam’s Mikado collection and Merino’s Decowood underscore how mid-volume runs now command a premium. Capital outlays of INR (50-100) crore per press limit participation to well-capitalized firms, accelerating consolidation. Interior designers gain freedom to order short-run bespoke patterns, expanding the addressable pool for premium-priced sheets.

Government Incentives for Low-VOC / E0 Grade Surfaces

IS 12592:2023 sets an E0 cap of ≤0.5 mg/L formaldehyde, down from E1’s ≤1.5 mg/L threshold, and dovetails with Quality Control Orders due in 2024 and 2025[2]Bureau of Indian Standards, “IS 12592:2023 Formaldehyde Emission Standard,” bis.gov.in. Compliance drives adhesive reformulation costs up 8-12%, yet allows producers to charge 10-15% price premiums on IGBC LEED or GRIHA projects. Fiscal incentives worth ₹329 crore have been offered to Greenlam’s Andhra Pradesh plant, highlighting state-level support tied to environmental benchmarks. Early movers anticipate dominating institutional and export tenders that require low-VOC certification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying competition from PVC boards and engineered stone | -0.8% | Coastal and humid regions (Kerala, Goa, West Bengal) | Short term (≤ 2 years) |

| Volatility in phenolic/melamine resin prices | -0.6% | National | Short term (≤ 2 years) |

| Tightening formaldehyde-emission norms (IS 12592:2023) | -0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition from PVC Boards and Engineered Stone

Polyvinyl chloride boards and wood-plastic composites offer termite and moisture resistance, capturing a significant share of the kitchen and bath market in coastal states. Engineered quartz worktops, priced at INR (565-1,400) per sq ft versus laminates at about INR 150, are pulling premium consumers toward stone finishes, especially in metropolitan renovations. Laminate producers are countering with compact panels and fire-retardant grades, but these niches require customer education and higher production costs.

Volatility in Phenolic/Melamine Resin Prices

Phenol traded above INR 100 per kg in 2024 amid a 15,000-tonne domestic supply shortfall, resulting in a reliance on imports. Melamine experienced double-digit quarterly swings as global supply and demand shifted. Producers with captive resin lines or locked-in contracts typically realize a 5-8% cost advantage, while smaller firms often suffer margin shocks. Unpredictable raw material outlays complicate pricing strategies for the India decorative laminates market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Substrate Dominance Amid Adhesive Innovation

Wood substrate held a 42.02% India decorative laminates market share in 2025, anchored by the cost advantage of particle board and MDF. Domestic board makers can deliver at INR (25-35) per sq ft, reinforcing their grip on value-conscious projects. Adhesives, though a smaller revenue pool today, are forecast to post a 6.05% CAGR, supported by the mandated shift to formaldehyde-free chemistries. Multinationals such as Henkel and Pidilite have introduced soy- and lignin-based binders that enable manufacturers to hit E0 thresholds without compromising bond strength.

Continuous-press particle-board lines, like the one Greenlam is installing in Andhra Pradesh, produce denser panels with tighter tolerances, helping laminators reduce sanding loss and improve yield. In parallel, antimicrobial additive packages embedded in adhesive layers, exemplified by CenturyPly’s ViroKill, open premium price windows in healthcare and hospitality projects. As sustainability audits become mainstream, board and resin suppliers offering FSC or PEFC chain-of-custody documentation will unlock access to export orders and green-building projects, raising the strategic value of backward integration.

By Application: Furniture Leads, Wall Panels Surge

Furniture accounted for 55.78% India decorative laminates market size in 2025, riding the modular-kitchen boom that now touches roughly one-quarter of new urban homes. Ready-to-assemble cabinetry relies on laminates for shutters, carcass cladding, and slim worktops, keeping volume growth synchronized with housing deliveries. Organized fit-out specialists specify abrasion-class ratings and synchronized grain alignment, prompting greater design differentiation.

Wall panels are set to expand at 6.26% CAGR, the fastest among applications, as hospitality and office interiors pivot toward quick-install decorative cladding. Single-pass digital printing lets designers order bespoke textures that previously required imported veneer or fabric panels. Compact laminates with self-supporting thicknesses of 6-25 mm are penetrating high-traffic corridors and elevator lobbies, adding durability attributes that justify higher per-sheet pricing.

Geography Analysis

Western and southern states drive roughly two-thirds of India decorative laminates market demand. Maharashtra tops consumption, buoyed by Mumbai’s dominance in residential and commercial construction approvals; over 30 million sq ft of office space is slated to open across its IT parks and mixed-use complexes by 2027. Organized laminate showrooms cluster in Pune and Mumbai, where modular-kitchen retailers record their highest sales density.

Gujarat is emerging as a powerhouse in production and exports. The Morbi-Ahmedabad corridor attracted investments topping INR 2.83 lakh crore in fiscal 2023, while proximity to Kandla and Mundra ports lowers export logistics costs. Rushil Décor’s Gandhinagar complex exemplifies this orientation, having booked overseas contracts soon after its commissioning. Smart-city programs in Ahmedabad and Surat are stimulating demand for E0-grade surfaces in municipal and institutional buildings.

Southern hubs—Karnataka, Tamil Nadu, and Andhra Pradesh—are emerging as next-generation growth centers. Greenlam’s Naidupeta site will be South India’s largest high-pressure laminate plant, supported by state incentives covering about 30% of project capex. Bengaluru’s tech corridor is fueling corporate fit-out volumes, while Chennai and Hyderabad add housing starts that favor pre-laminated boards. Northern clusters in Punjab and the Delhi-NCR region continue to leverage long-standing manufacturing bases; CenturyPly’s expansion in Hoshiarpur strengthens supply into North and East markets.

Mordor Intelligence provides coverage of the decorative laminates market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The Indian Decorative Laminates Market is moderately concentrated. Greenlam, CenturyPly, and Merino headline the organized tier, each investing in capacity, digital printing, and low-VOC compliance. Technology and compliance are separating leaders from laggards. Continuous-press board lines, single-pass inkjet printers, silver-ion antimicrobial formulations, and in-house test labs confer both cost and pricing power. The march toward mandatory E0 certification is likely to hasten consolidation, as undercapitalized mills either upgrade at compressed margins or exit the Indian decorative laminates industry.

India Decorative Laminates Industry Leaders

Greenlam Industries Limited

Aica Laminates India Pvt. Ltd.

Merino India

CenturyPly

Stylam

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Rushil Décor Limited, a player in the Indian decorative laminate and MDF panel board industry, announced the commencement of trial run production under Phase 2 of its advanced Jumbo Size decorative Laminates manufacturing facility, located at Village Itla, District Gandhinagar, Gujarat.

- July 2025: Greenlam Industries announced an investment of INR 1,147 crore (USD 132.7 million) in Andhra Pradesh's Naidupeta to establish a high-pressure laminate and particleboard manufacturing facility. The facility will produce 7 million sheets of high-pressure decorative laminate.

India Decorative Laminates Market Report Scope

Decorative laminates are predominantly used as furniture surface materials or wall paneling. They are primarily known for their aesthetic appeal and availability in various textures, patterns, colors, and finishes. Due to their decorative and protective properties, they are often used for furniture designs such as shelves, cabinets, doors, and office cubicles.

The Indian decorative laminates market is segmented by raw material, application, end-user industry, and geography. By raw material, the market is segmented into plastic resin, overlays, adhesives, and wood substrate. By application type, the market is segmented into furniture, cabinets, flooring, wall panels, and other applications (table tops and countertops). By end-user industry, the market is segmented into residential, non-residential, and transportation. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Plastic Resin |

| Overlays |

| Adhesives |

| Wood Substrate |

| Furniture |

| Cabinets |

| Flooring |

| Wall Panels |

| Other Applications (Table Tops and Counter Tops) |

| By Raw Material | Plastic Resin |

| Overlays | |

| Adhesives | |

| Wood Substrate | |

| By Application | Furniture |

| Cabinets | |

| Flooring | |

| Wall Panels | |

| Other Applications (Table Tops and Counter Tops) |

Key Questions Answered in the Report

What is the current value of the India decorative laminates market?

The India decorative laminates market size stands at USD 1.39 billion in 2026 and is forecast to reach USD 1.81 billion by 2031.

Which raw-material segment dominates sales?

Wood substrates, primarily particle board and MDF, captured 42.02% India decorative laminates market share in 2025.

Which application segment is growing the fastest?

Wall panels are projected to expand at a 6.26% CAGR between 2026 and 2031.

How will IS 12592:2023 affect producers?

The E0 emission mandate raises production costs 8-12% but enables premium pricing on green-certified projects.

Which states host the largest laminate plants?

Major capacities are concentrated in Gujarat’s Gandhinagar corridor and Andhra Pradesh’s Naidupeta manufacturing hub.

Page last updated on: