India Cement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

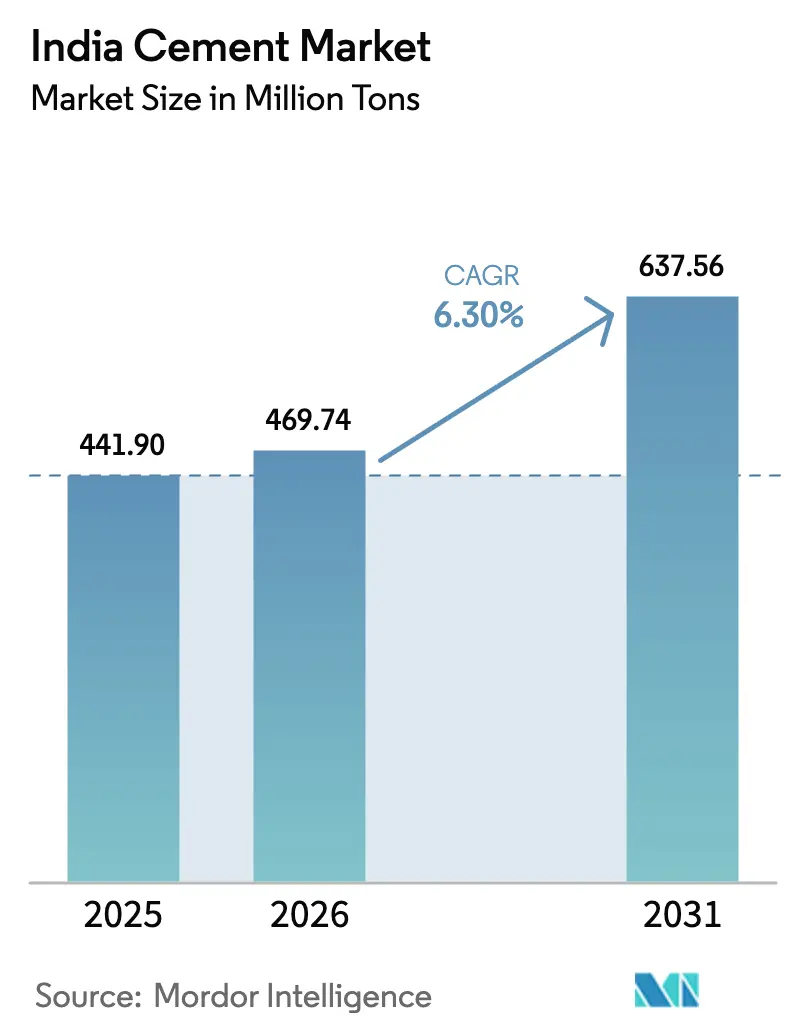

| Base Year Market Size (2025) | 441.90 Million Tons |

| Market Volume (2026) | 469.74 Million Tons |

| Market Volume (2031) | 637.56 Million Tons |

| Growth Rate (2026 - 2031) | 6.30% CAGR |

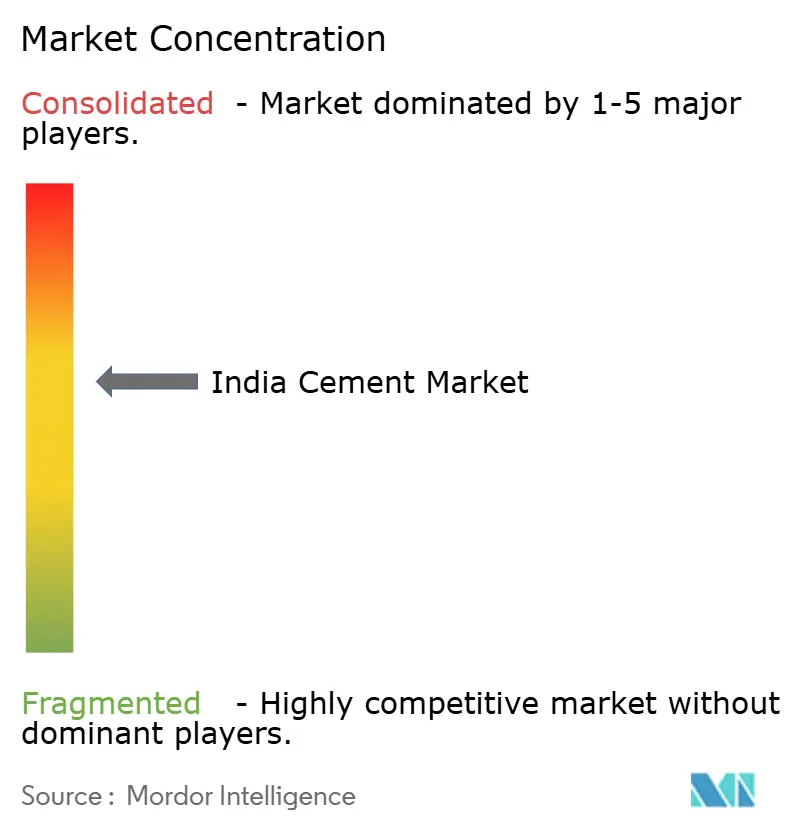

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Cement Market Analysis by Mordor Intelligence

The India Cement Market size is expected to grow from 441.90 Million Tons in 2025 to 469.74 Million Tons in 2026 and is forecast to reach 637.56 Million Tons by 2031 at 6.30% CAGR over 2026-2031. Demand continues to track public-sector infrastructure outlays, rising urban housing starts, and expanding data-center construction. Blended formulations dominate shipments as producers balance cost, carbon intensity, and Bureau of Indian Standards compliance. Fiber cement is scaling fastest on the back of commercial real-estate safety codes, while aggressive capacity additions are reshaping regional price dynamics. Consolidation among the top five manufacturers has lifted their combined India cement market share to roughly 60%, giving large, integrated players meaningful leverage in procurement and logistics.

Key Report Takeaways

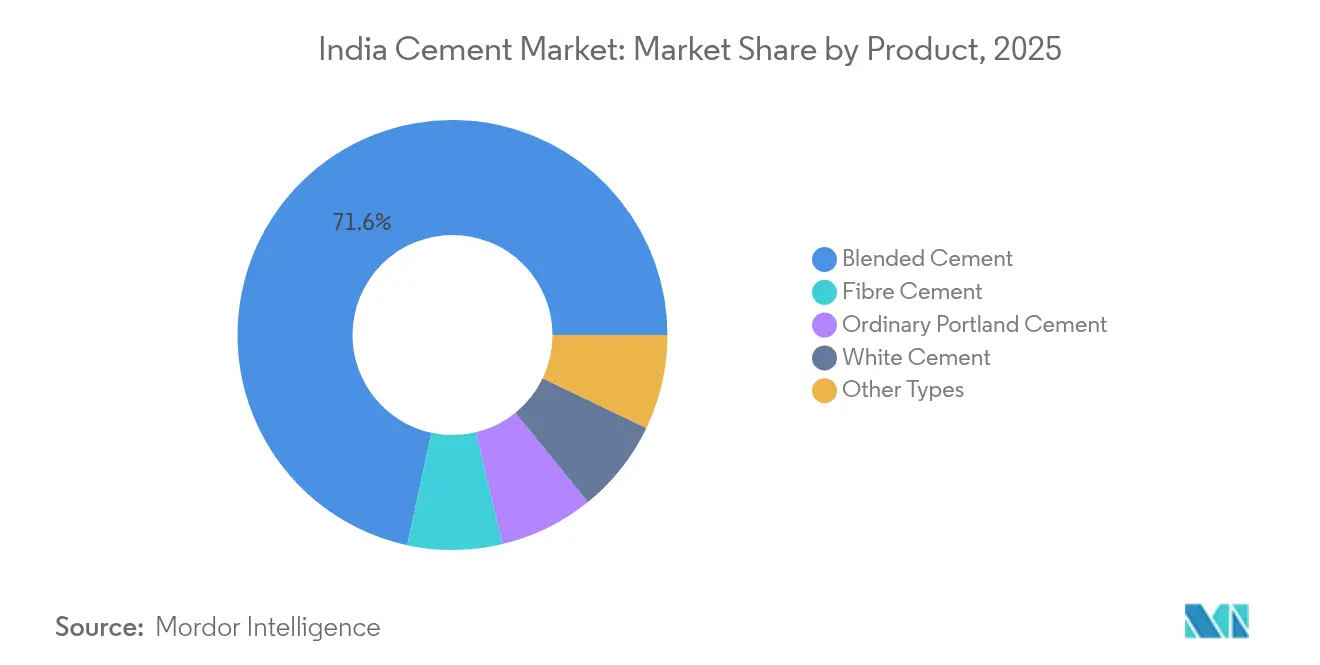

- By product, blended cement led with 71.62% revenue share of the India Cement market in 2025; fiber cement is projected to register a 6.62% CAGR to 2031.

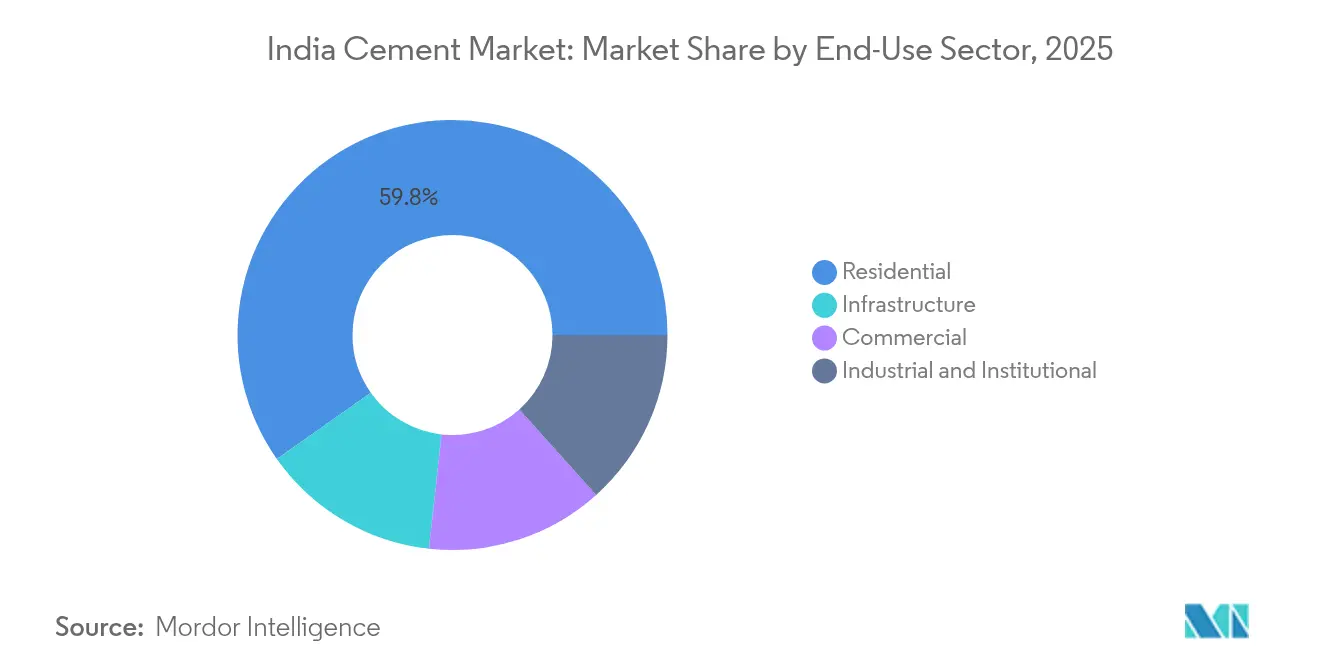

- By end-use sector, the residential segment accounted for 59.78% of the India Cement market size in 2025; commercial construction is advancing at a 6.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Cement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained Public‐sector Capex on Expressways and Rail Corridors | +1.5% | Nationwide; corridor states | Medium term (2-4 years) |

| PM-GatiShakti Hub-and-spoke Logistics Investments | +1.2% | Nationwide; industrial clusters | Long term (≥4 years) |

| Affordable-housing Push Under PMAY-Urban 2.0 | +0.8% | Tier-II/III urban centers | Medium term (2-4 years) |

| Demand for Low-carbon Blended Cements from Data-centre Builders | +0.6% | Mumbai, Chennai, Bengaluru, Hyderabad | Short term (≤2 years) |

| Green-hydrogen-ready Kilns Unlocking ESG Financing | +0.5% | Coastal production belts | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Sustained Public‐sector Capex on Expressways and Rail Corridors

Union Budget 2025-26 set government infrastructure spending at INR 11.21 lakh crore (USD 128.6 billion), including INR 2.65 lakh crore (USD 31.4 billion) for Railways[1]. Network expansion to 146,145 km and 33.8 km-per-day highway construction rates have aligned cement demand with project execution schedules in the india cement market. Bharatmala Phase I delivered 18,926 km by November 2024, while 35 upcoming multimodal logistics parks will concentrate on regional order books. The nearly complete Delhi–Mumbai Expressway and Western Dedicated Freight Corridor exemplify large, cement-intensive programs moving from announcement to concrete pours. Ongoing track-doubling and station-modernization works further lift ordinary Portland and slab-track cement off-take.

PM-GatiShakti Hub-and-spoke Logistics Investments

The National Master Plan integrates 44 federal ministries and 36 states, collapsing permit delays that historically fragmented demand. A vetted project pipeline worth INR 15.39 lakh crore (USD 176.4 billion) underpins forward capacity planning for the India cement market. Mode-shift savings of 30-50% when cargo moves from road to sea benefit coastal grinding units and unlock new inland demand nodes as river-port linkages mature. Industrial-corridor nodes such as the Delhi–Mumbai Industrial Corridor’s 11 hubs translate into a predictable, clustered need for performance-graded cement.

Affordable-housing Push Under PMAY-Urban 2.0

The upgraded scheme targets 1 crore new homes, representing an outlay of INR 10 lakh crore (USD 114.6 billion)[2]. With 88.32 lakh units already handed over under the prior phase, execution risk remains modest across the india cement market. Typical designs consume 0.6–0.8 tons of cement per square meter, offering bulk-procurement efficiencies to regional producers. Expansion into Tier-II/III cities such as Surat and Indore diversifies the demand base, and Smart Cities Mission tie-ins lift per-unit cement intensity through allied civic works.

Demand for Low-carbon Blended Cements from Data-centre Builders

Hyperscale capacity is set to add 500 MW across Mumbai, Chennai, Bengaluru, and Hyderabad by 2029. Data-center foundations rely on low-heat blended formulations to curb thermal cracking, creating a premium niche in the india cement market. High cement consumption per MW and compressed construction timelines translate into frequent, high-volume dispatches for local suppliers. Alignment with enterprise ESG targets enables pricing traction for 30–40% fly-ash blends.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Railway Wagon Shortages During Harvest Seasons | -0.90% | National, acute in agricultural states (Punjab, Haryana, UP, Bihar) | Short term (≤ 2 years) |

| Aggressive Capacity Additions Driving Price Wars in East and South | -0.70% | Eastern India (West Bengal, Odisha, Jharkhand) and Southern India (Tamil Nadu, Karnataka, Andhra Pradesh) | Medium term (2-4 years) |

| Rising Pet-coke Import Duty Volatility | -0.50% | National, concentrated impact on coastal cement plants | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Railway Wagon Shortages During Harvest Seasons

Competition between grain and clinker consignments intensifies every post-harvest quarter, squeezing wagon allocations and forcing cement producers onto more expensive road routes. Eastern dispatches face the sharpest disruption as rail priority shifts to food-grain movement, inflating delivered-cost structures and shortening viable supply radii from surplus to deficit markets in the india cement market. The mismatch grows as manufacturing hubs migrate inland while limestone-rich source states cluster along the coast.

Aggressive Capacity Additions Driving Price Wars in East and South

Southern nameplate capacity stands at 188 million tons annually, yet utilization lingers near 60–65%, encouraging undercutting among roughly 45 local brands. Eastern India shows similar imbalances as new kilns ramp faster than nearby demand within the india cement market. Persistent oversupply depresses regional pricing and margins, delaying reinvestment in modern kilns and sustainability retrofits across the India cement industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Blended Cement Holds Sway as Compliance Costs Fall

Blended grades captured 71.62% of the India Cement market in 2025 on the back of 15-20% lower cash costs versus ordinary Portland mixes and rising pressure to slash clinker factors. The segment’s dominance is further underwritten by abundant fly-ash from coal plants and explicit carbon-footprint rules in public tenders. Fiber cement, although niche, is on track for a 6.62% CAGR from 2026-2031, buoyed by non-combustible mandates in data centers and industrial sheds.

User adoption trends favor performance-based purchasing, with infrastructure bidders specifying durability metrics rather than generic grades. OPC 53 remains indispensable for bridges and high-rise cores where 28-day compressive strength above 53 MPa is non-negotiable, shaping technical preferences in the india cement market. White cement stays a premium architect’s choice, while marine-grade and rapid-setting formulas round out specialized demand pockets.

By End-Use Sector: Residential Leads; Commercial Builds Momentum

Housing retained a 59.78% share of the India Cement market size in 2025, underscoring the nation’s structural deficit in quality dwellings. Individual plot construction in rural districts and vertical apartment schemes in metros create a stable baseline of bag-cement consumption.

Commercial builds, however, clock the swiftest trajectory at a 6.55% CAGR through 2031. Retail malls, Grade-A offices, and hospitality projects in Tier-II corridors are adopting ready-mix solutions that embed value-added cement blends across the india cement market. Industrial and institutional segments gain from manufacturing-linked-incentive schemes and public health infrastructure roll-outs, while transport megaprojects safeguard a steady baseline of bulk orders for pavement-grade concrete.

Geography Analysis

Regional consumption aligns with economic heft, putting Maharashtra on top with roughly 12.04% of national volume. Mumbai’s vertical skyline and Pune’s auto clusters keep bag and bulk channels busy. Northern demand rides on National Capital Region arterial-road upgrades and dedicated freight corridors that consume high-strength slab track formulations.

Southern India hosts 188 million tons of installed kiln capacity but endures price volatility because utilization hovers near 60-65%. Proximity to ports and fly-ash supplies favors blended cement exports from coastal plants, yet fragmented ownership caps pricing power. Central India, rich in limestone, is a supply node feeding the deficit northern and western states via rail.

PM-GatiShakti corridor planning redraws demand maps; multimodal parks and industrial nodes stimulate concrete consumption in once-sleepy hinterlands. Coastal break-bulk terminals spur marine infrastructure pours, while PMGSY Phase IV links another 25,000 rural habitations, driving thin-lift pavement demand across the Indo-Gangetic plain.

Competitive Landscape

The Indian Cement market is moderately consolidated. UltraTech alone operates 150.7 million tons of capacity and targets 200 million tons by 2028. Adani’s announced purchases of Orient and Penna aim for 140 million tons, intensifying the race for coastal grinding footprints. Smaller firms are ceding ground or entering regional alliances as the capital intensity of waste-heat recovery systems and renewable-power PPAs widens the cost gap. Integration from limestone quarries to packaged-cement depots cushions margin swings for larger groups, hastening the attrition of stand-alone grinding players unable to fund kiln upgrades or alternative-fuel retrofits.

India Cement Industry Leaders

Adani Group

Dalmia Bharat Limited

Nuvoco Vistas Corp Ltd.

Shree Cement Limited

UltraTech Cement Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: JK Cement Ltd. announced a major greenfield expansion to increase the company’s production capacity by 7 million tonnes per annum (MTPA). The move aims to strengthen its position in India’s cement industry and meet the growing demand for construction materials nationwide.

- February 2025: Shree Cement launched Bangur Marble Cement under its master brand Bangur Cement in Ranchi, Jharkhand. This Portland Slag cement offers high brightness, superior strength, and crack resistance, making it ideal for exposed concrete structures and ensuring grand, imposing designs. The product will be further rolled out in Bihar, West Bengal, and other Indian states.

India Cement Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Blended Cement, Fiber Cement, Ordinary Portland Cement, White Cement are covered as segments by Product.| Ordinary Portland Cement |

| Blended Cement |

| White Cement |

| Fibre Cement |

| Other Types |

| Residential |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| By Product | Ordinary Portland Cement |

| Blended Cement | |

| White Cement | |

| Fibre Cement | |

| Other Types | |

| By End-Use Sector | Residential |

| Commercial | |

| Industrial and Institutional | |

| Infrastructure |

Market Definition

- END-USE SECTOR - Cement consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of various types of cement such as ordinary portland cement, blended cement, white cement, fiber cement, etc. are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms