Asia-Pacific Cross-Laminated Timber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

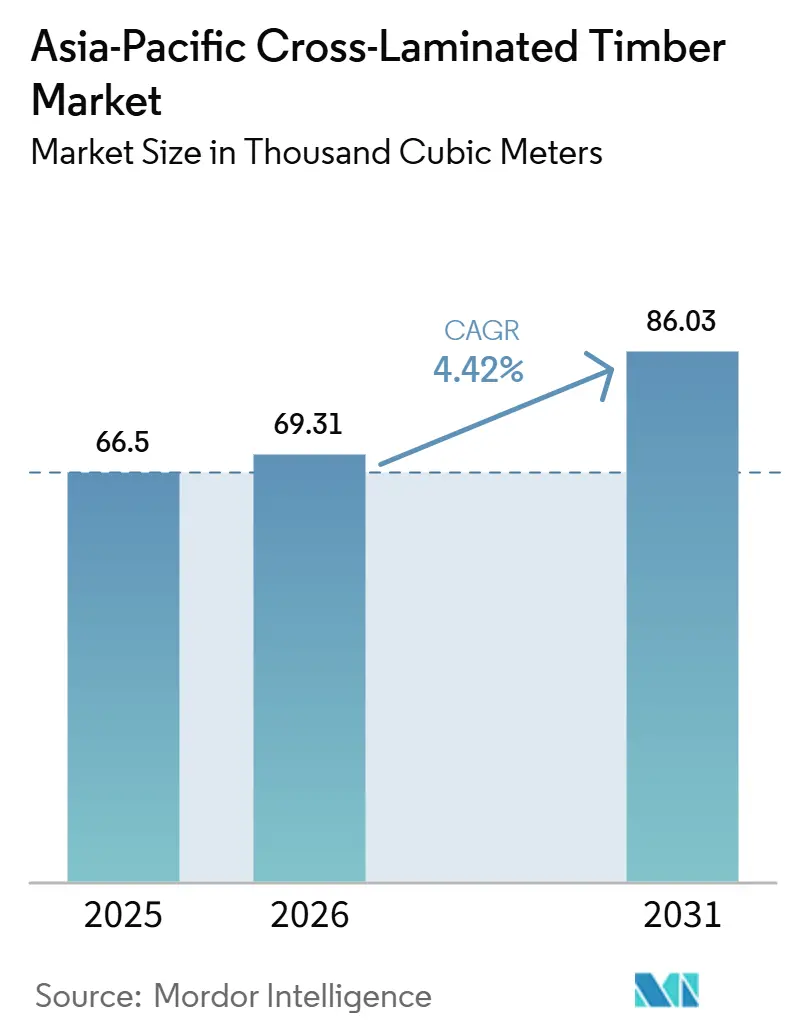

| Base Year Market Size (2025) | 66.5 Thousand cubic meters |

| Market Volume (2026) | 69.31 Thousand cubic meters |

| Market Volume (2031) | 86.03 Thousand cubic meters |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

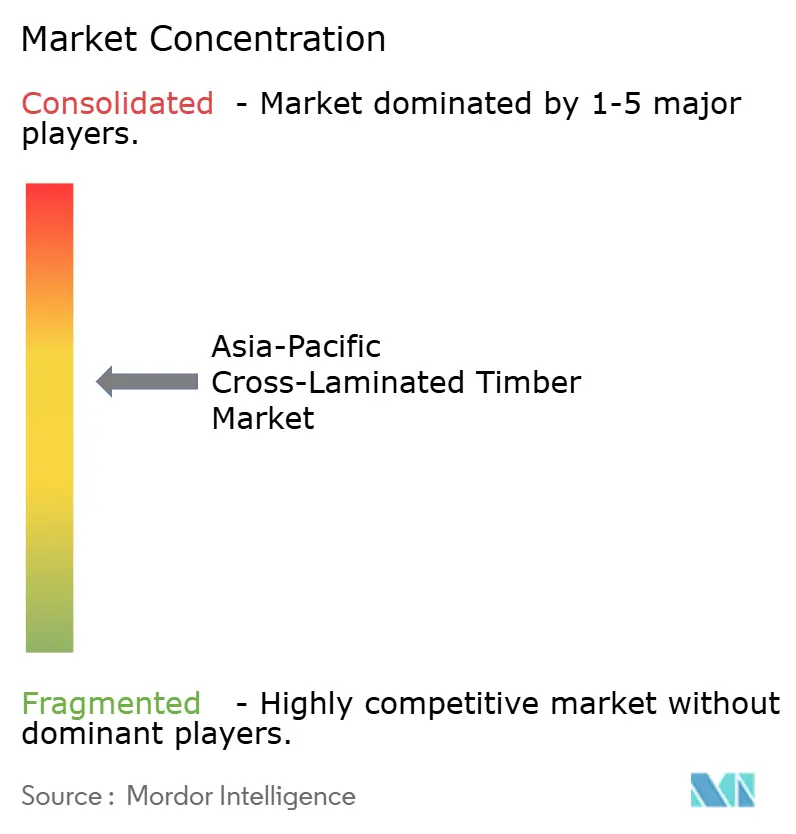

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Cross-Laminated Timber Market Analysis by Mordor Intelligence

The Asia-Pacific Cross-Laminated Timber Market size is expected to increase from 66.5 Thousand cubic meters in 2025 to 69.31 Thousand cubic meters in 2026 and reach 86.03 Thousand cubic meters by 2031, growing at a CAGR of 4.42% over 2026-2031. Mass-timber mandates now appear in building codes from Jiangsu to Seoul, enabling developers to shorten schedules by several months while storing about 1.8 metric tons of CO₂ per cubic meter of panel installed. China led with 46% of 2025 volume, yet India is poised to accelerate fastest as the Goa demonstration house and IIT (Indian Institute of Technology) Roorkee training hub stimulate demand. Adhesive-bonded panels currently dominate, but dowel-laminated systems are scaling because circular-economy credits reward disassembly potential. Hybrid high-rises such as Perth’s 35-storey office and Mitsui Fudosan’s Nihonbashi headquarters validate the structural and commercial logic that is drawing institutional capital toward prefabricated CLT.

Key Report Takeaways

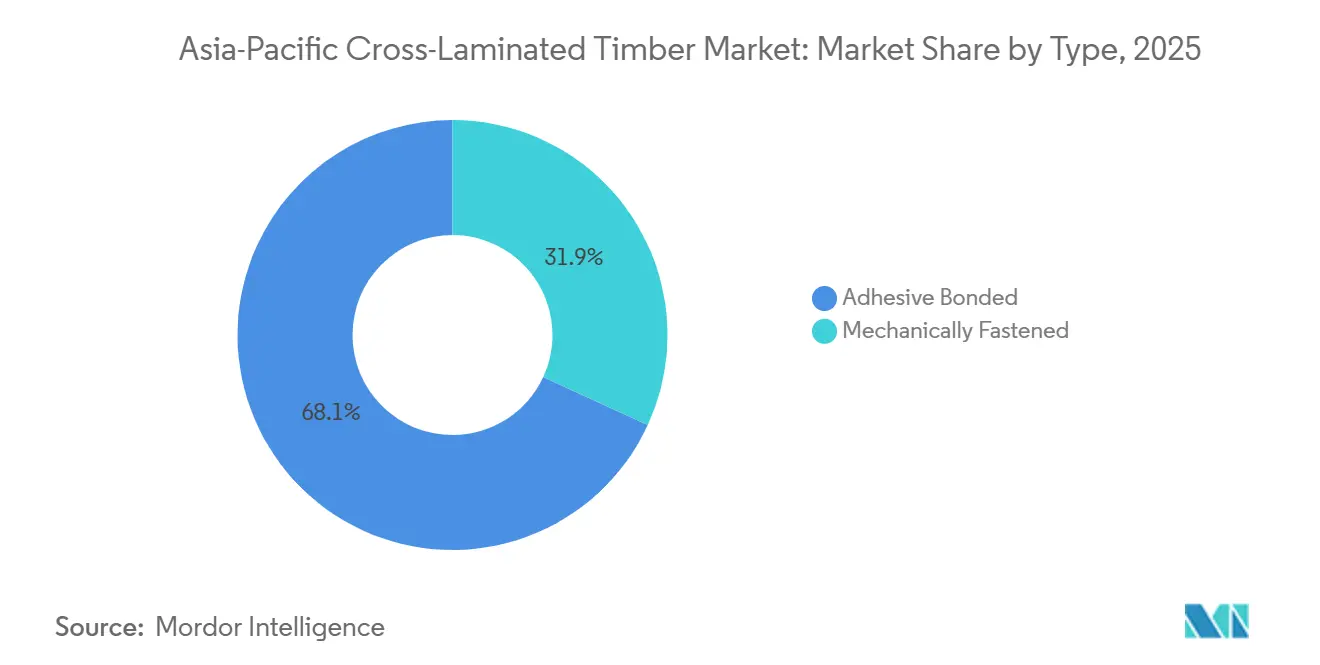

- By type, adhesive-bonded panels held 68.12% of the Asia-Pacific Cross-Laminated Timber market share in 2025, while mechanically fastened ones are projected to register a 7.31% CAGR during the forecast period (2026-2031).

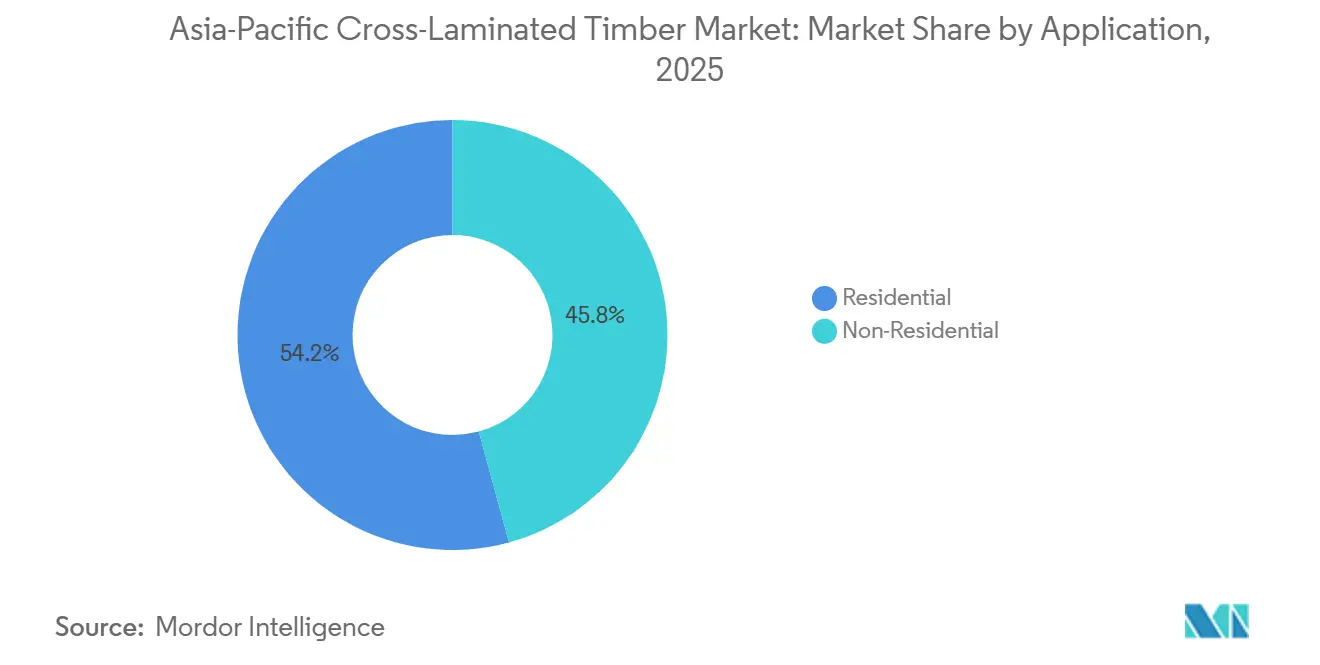

- By application, residential construction accounted for 54.23% of the Asia-Pacific Cross-Laminated Timber market size in 2025, and non-residential demand is advancing at a 7.12% CAGR during the forecast period (2026-2031).

- By geography, China held 46.17% of the Asia-Pacific Cross-Laminated Timber market share in 2025, while India is projected to register a 7.67% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Asia representing one of the more structurally developed among them. The global report on cross laminated timber market by Mordor Intelligence reflects how these regional layers combine into a single system.

Asia-Pacific Cross-Laminated Timber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urban mid-rise construction boom in China and India | +1.2% | China (tier-1 & tier-2 cities), India (Delhi NCR, Bengaluru, Pune) | Medium term (2-4 years) |

| Green-building incentives across Japan, South Korea, Australia | +0.9% | Japan, South Korea, Australia, New Zealand | Long term (≥4 years) |

| Prefabricated mass-timber modular demand post-COVID logistics shift | +0.7% | Global, with concentration in Australia, Japan | Short term (≤2 years) |

| Hybrid timber-steel high-rise approvals unlocking new volume | +0.8% | Australia (Perth, Sydney), Japan (Tokyo, Osaka), China (Shenzhen) | Medium term (2-4 years) |

| Indigenous bamboo-reinforced CLT R&D in China and South-East Asia | +0.5% | China (Jiangsu, Sichuan, Yunnan), Southeast Asia (Vietnam, Thailand) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban Mid-Rise Construction Boom in China and India

China and India together contribute more than 60% of annual mid-rise residential starts, and fresh policy signals are directing a measurable fraction toward modern wood structures. Jiangsu’s January 2026 directive obliges public projects above 5,000 m² to evaluate CLT, adding 8,000-12,000 m³ of yearly demand inside the province[1]China Daily Staff, “Guiding Opinions on Promoting Modern Wood Structure Development,” China Daily, chinadaily.com.cn. India’s first mass-timber residence in Goa and IIT Roorkee’s INR 120 million (USD 1.38 million) training center are creating local design capacity and anchoring supply chains. Builders value CLT’s 20-25% weight advantage because it limits deep foundations in land-scarce metros where plots command premium prices. With engineering talent graduating from new programs by 2028, most incremental volume is expected to appear from 2027 onward.

Green-Building Incentives Across Japan, South Korea, Australia

CASBEE, G-SEED, and Green Star certifications now award extra points for low-embodied-carbon materials validated by Environmental Product Declarations[2]Baker McKenzie Authors, “Green-Building Incentives in APAC,” Baker McKenzie, bakermckenzie.com. Japan’s 2024 guidelines grant up to 10% floor-area-ratio bonuses for domestic CLT, which Mitsui Fudosan used to add an additional storey to its 2025 Nihonbashi project. South Korea mandates Green 2 for all public buildings, effectively making Environmental Product Declaration (EPD) documentation a market-entry requirement for suppliers. Australia’s Clean Energy Finance Corporation has set aside AUD 300 million in low-interest loans for net-zero mass-timber projects, underwriting 42,000 m³ of panels by Q1 2026. These incentives disproportionately support adhesive-bonded CLT today but are likely to persist well beyond 2031 and continue lifting specification rates.

Prefabricated Mass-Timber Modular Demand Post-COVID Logistics Shift

Supply-chain disruptions during the pandemic exposed the fragility of cast-in-place concrete. Timberlink’s NeXTimber line and XLam’s Wodonga factory now ship CNC-routed CLT modules in as little as eight weeks, a timeline that won Sydney’s 13-storey residential tower scheduled for Q3 2026. Japan’s Space Factory produces 120 CLT-framed units per month, targeting post-disaster housing where speed and seismic resilience command higher rents. Modular erection reduces on-site labor needs by roughly 50%, easing skilled-worker shortages in major cities. The uplift is front-loaded into 2026-2028 while lead-time advantages remain pronounced.

Hybrid Timber-Steel High-Rise Approvals Unlocking New Volume

Australia now has three permitted towers that combine CLT floors with steel frames, including Atlassian Central at 40 storeys. Japan amended its Building Standard Law in 2024, allowing timber components in buildings up to 16 storeys if encapsulated for fire resistance, a rule already proven by Sumitomo Forestry’s six-storey apartment completed in June 2025. Shenzhen has published draft guidelines allowing CLT up to 18 storeys in innovation districts. Hybrid construction cuts embodied carbon by 30-40% relative to all-steel alternatives, meeting corporate ESG (Environmental, Social, and Governance) targets while preserving speed. First-wave completions between 2027 and 2030 should unlock more conservative capital pools such as pension funds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Moisture-induced delamination and mold risk in tropical climates | -0.6% | Southeast Asia (Indonesia, Malaysia, Thailand, Vietnam), southern China, northern Australia | Short term (≤2 years) |

| Shortage of CLT-skilled labor and inspection expertise | -0.4% | India, Southeast Asia, tier-2 & tier-3 cities in China | Medium term (2-4 years) |

| Building-code fragmentation slowing project approvals | -0.5% | ASEAN member states, provincial variation in China, state-level differences in Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Moisture-Induced Delamination and Mold Risk in Tropical Climates

Sustained humidity above 75% pushes lamella moisture beyond adhesive tolerance, and field surveys in Malaysia and northern Australia documented delamination in 8-12% of unprotected panels within two years. Mold appeared within one year on 26% of 34 tracked projects across Indonesia, Malaysia, and Thailand, forcing remedial costs that neutralize CLT’s price advantage. Silane-modified polyurethane solves the chemistry but is still 30-40% more expensive and remains uncertified for structural use. Until codes mandate vapor control layers or adhesives improve, tropical humidity will remain a drag on adoption.

Shortage of CLT-Skilled Labor and Inspection Expertise

Asia-Pacific counts fewer than 200 ISO-certified CLT installers, mostly clustered in Sydney, Melbourne, Tokyo, and Osaka. India’s first mass-timber house flew in a six-person Austrian team because no domestic crew knew CLT crane-rigging protocols. Inspectors outside tier-1 Chinese cities reject submissions using concrete checklists that lack moisture criteria, creating costly redesigns. New training programs at IIT Roorkee and Australia’s TAFE (Technical and Further Education) will add capacity by 2028, yet wage inflation near 8% annually keeps labor tight mid-term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dowel-Laminated Panels Gain as Circular Mandates Favor Disassembly

Adhesive-bonded panels command 68.12% share because continuous glue lines deliver higher shear capacity, critical for tall-building cores. Binderholz’s Burgbernheim Plant II now produces lot-size-one CLT panels up to 18 m long, underlining economies of scale that keep bonded systems price-competitive. The Asia-Pacific cross-laminated timber market size for adhesive panels should retain leadership in seismic and long-span applications, yet mechanically fastened formats are on track to reach a higher market share by 2031 as circular-economy standards tighten.

Mechanically fastened laminated timber is forecast to expand at 7.31% CAGR to 2031, outperforming the wider Asia-Pacific cross-laminated timber market. Demand accelerates because Japanese and South Korean rating systems grant extra credits for reversible construction methods that allow post-use disassembly. A University of British Columbia test in 2024 showed five-ply mechanically fastened CLT reached 92% of the bending strength of bonded panels, narrowing performance gaps for residential floors. Builders in Tokyo and Seoul have already substituted mechanically fastened CLT in low-stress diaphragms to secure sustainability bonuses.

By Application: Non-Residential Surge Driven by Hybrid Towers and ESG Mandates

Residential buildings represented 54.23% of 2025 consumption because low-rise apartments in Japan, South Korea, and Australia leverage Type C construction allowances. Yet higher land prices in Chinese and Indian metros are steering developers to mid-rise hybrids where CLT’s lighter weight cuts foundation budgets. The Asia-Pacific cross-laminated timber market share of non-residential projects is therefore set to climb as corporate ESG targets reward embodied-carbon savings and height caps lift through code reforms.

Non-residential demand is projected to grow at 7.12% CAGR during the forecast period (2026-2031), faster than the overall Asia-Pacific Cross-Laminated Timber market. Flagship projects include the 12,000 m³ CLT package for Atlassian’s 40-storey Sydney headquarters and Mitsui Fudosan’s CASBEE-S office in Tokyo, both signaling confidence among institutional investors. Warehouses and university buildings are adopting CLT to unlock earlier tenant fit-outs, with a Melbourne distribution hub saving 8 weeks of schedule and AUD 400,000 (USD 2,63,920) in holding costs.

Geography Analysis

China accounted for 46.17% of 2025 volume, supported by at least four domestic factories each exceeding 60,000 m³ annual capacity and by Jiangsu’s January 2026 directive requiring public projects to assess CLT. The Wuxi Haihe Yuan pilot demonstrated a 40% reduction in structural steel within a seismic Zone 3 context, proving economic viability for commodity housing. Research and development into bamboo-reinforced panels could add up to 200,000 m³ of capacity once ISO 22156 tests conclude after 2029.

India is pacing at a 7.67% CAGR through 2031 due to the Goa showcase house and IIT Roorkee’s mass-timber center, which aims to certify 500 engineers and localize standards. Import dependence keeps landed costs 40-50% above concrete, limiting use to premium residential and institutional builds, but expected domestic plants could narrow that gap.

Japan benefits from mature codes and incentives; the 2024 guideline change delivers 10% floor-area-ratio rewards for domestic CLT, and Sumitomo Forestry plans 50 additional hybrid apartments by 2028. South Korea’s G-SEED compels EPD-certified materials in public projects, funneling steady orders to suppliers with documented carbon footprints. Australia and New Zealand draw on the Clean Energy Finance Corporation’s AUD 300 million (USD 197.94 million) facility, while XLam and Timberlink cut delivery times to eight weeks and catalyze regional adoption.

Southeast Asia continues to lag despite abundant bamboo and rising green-building interest. Indonesia’s permit shift in 2026 lengthened approvals, Malaysia lacks clear fire-test benchmarks, and no domestic production exists, keeping prices high and supply chains thin. The ASEAN Timber Council’s USD 12 million pilot may spur localized bamboo-CLT after 2027, but moisture and regulatory barriers remain material.

Competitive Landscape

The Asia-Pacific Cross-Laminated Timber market is moderately concentrated. Technology differentiation now centers on Industry 4.0 automation and hydrolysis-resistant adhesives. Pfeifer’s Kajaani sawmill doubled to 450,000 m³ of sawn pine in July 2025 and used 970 m³ of its own CLT for plant structures to demonstrate confidence. Tokyo Institute of Technology’s silane-modified polyurethane, though uncertified, signals future competition based on moisture performance rather than volume alone. Competitive intensity is therefore moderate but rising as Chinese capacities scale and Indian entrants emerge post-2028.

Asia-Pacific Cross-Laminated Timber Industry Leaders

Stora Enso

Timberlink Australia & New Zealand

XLAM AUSTRALIA PTY LTD

SEIHOKU CORPORATION

Mercer International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Green Building Council Indonesia (GBCI) honored a research team from Universitas Gadjah Mada (UGM) in Indonesia with the Best Greenship Innovation Award 2025. This accolade celebrates the CLT (cross-laminated timber) Nusantara Pavilion, a wooden structure that pioneers low-emission construction techniques with timber sourced from local suppliers.

- November 2025: In Nihonbashi, Tokyo, Mitsui Fudosan Co., Ltd. wrapped up its hybrid timber-steel office building, earning the CASBEE S-rank certification. Notably, the project incorporated around 2,400 m³ of CLT for its floor plates and cores, helping the growth of the CLT market.

Asia-Pacific Cross-Laminated Timber Market Report Scope

Cross Laminated Timber (CLT) is an engineered wood product, consisting of planks of sawn, glued, and layered wood, where each layer is oriented at right angles to one another and then glued to form structural panels. By joining layers of wood at perpendicular angles, structural rigidity for the panel is obtained in both directions, similar to plywood but with thicker components.

The Asia-Pacific cross-laminated timber market is segmented by type, application, and geography. By type, the market is segmented into adhesive bonded and mechanically fastened. By application, the market is segmented into residential and non-residential (commercial, industrial/institutional, and other applications). The report also covers the size and forecasts for the cross-laminated market in 6 countries across the Asia-Pacific. For each segment, the market sizing and forecasts have been done based on volume (cubic meters).

| Adhesive Bonded |

| Mechanically Fastened |

| Residential | |

| Non-Residential | Commercial |

| Industrial / Institutional | |

| Other Applications |

| China |

| India |

| Japan |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Type | Adhesive Bonded | |

| Mechanically Fastened | ||

| By Application | Residential | |

| Non-Residential | Commercial | |

| Industrial / Institutional | ||

| Other Applications | ||

| By Geography | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How fast is demand growing for cross-laminated timber in Asia-Pacific?

The Asia-Pacific Cross-Laminated Timber Market size is expected to increase from 66.5 Thousand cubic meters in 2025 to 69.31 Thousand cubic meters in 2026 and reach 86.03 Thousand cubic meters by 2031, growing at a CAGR of 4.42% over 2026-2031.

Which countries are driving the next wave of CLT adoption?

China remains the largest market, while India is the fastest-growing with a 7.67% CAGR expected through 2031.

What segments will contribute most to additional volume?

Hybrid timber-steel non-residential projects such as offices and university buildings are forecast to expand at 7.12% CAGR.

What barriers limit CLT uptake in Southeast Asia?

High humidity that promotes delamination, fragmented building codes, limited local production and a shortage of certified installers slow adoption.

Page last updated on: