India Flooring Resins Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

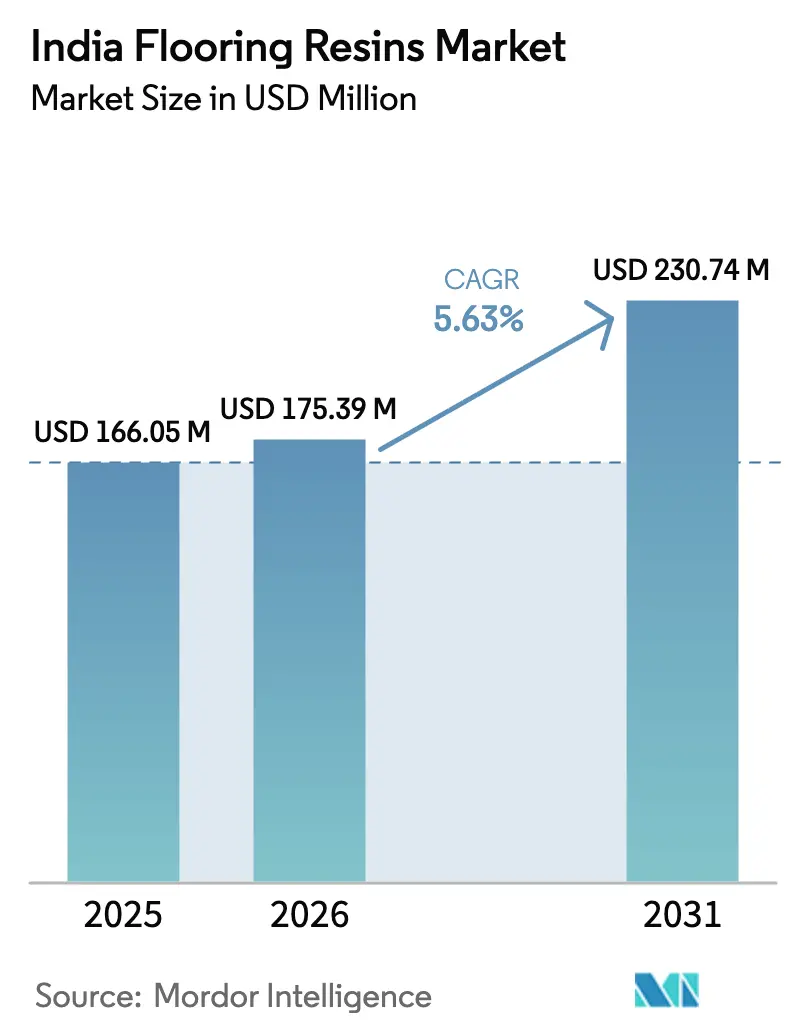

| Base Year Market Size (2025) | USD 166.05 Million |

| Market Size (2026) | USD 175.39 Million |

| Market Size (2031) | USD 230.74 Million |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Flooring Resins Market Analysis by Mordor Intelligence

The India Flooring Resins Market size is expected to grow from USD 166.05 million in 2025 to USD 175.39 million in 2026 and is forecast to reach USD 230.74 million by 2031 at 5.63% CAGR over 2026-2031. Robust public‐sector infrastructure spending, stricter hygiene rules in life-science manufacturing, and growing corporate sustainability mandates collectively fuel demand for advanced resin floors. Developers are switching from cementitious toppings to seamless resin systems because the latter deliver long service life, chemical resistance, and easier compliance with evolving fire-safety and volatile-organic-compound (VOC) limits. Large pharmaceutical expansions around Hyderabad and Pune, together with rising e-commerce warehousing, sustain year-round project pipelines that favor fast-curing or low-VOC chemistries. Meanwhile, global suppliers are localizing production and transferring technology, narrowing the cost gap with conventional tiles and reinforcing customer confidence in high-performance formulations.

Key Report Takeaways

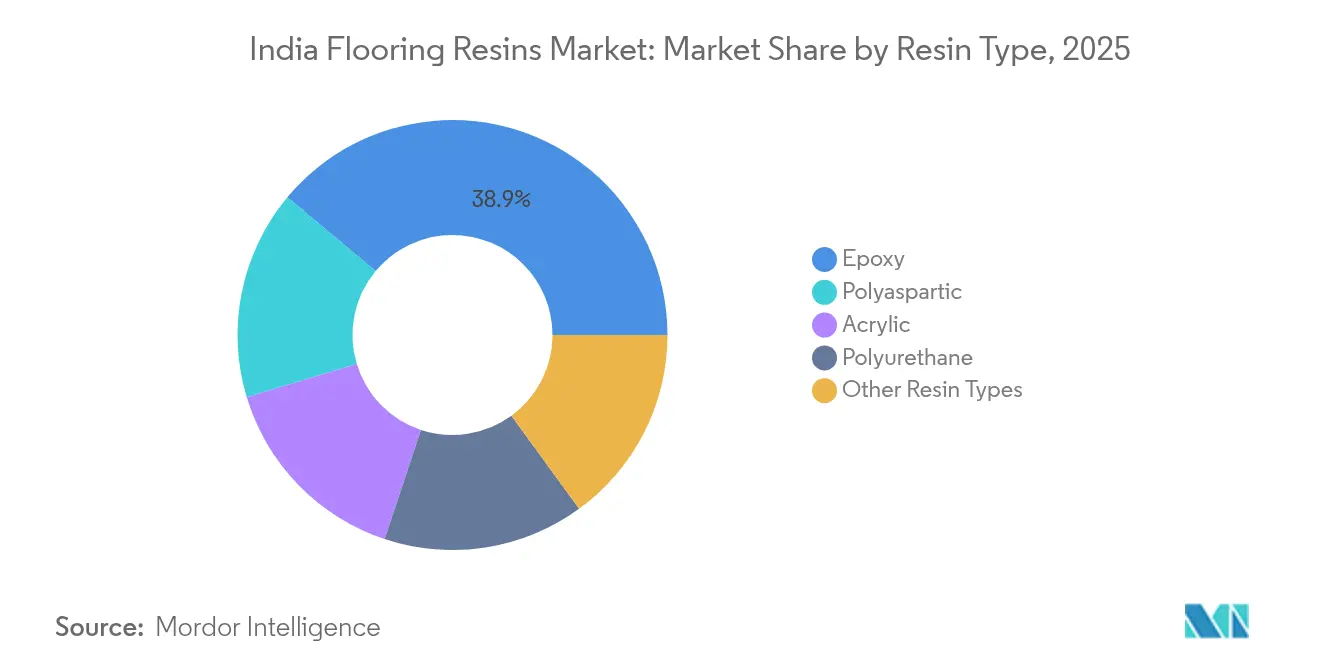

- By resin type, epoxy led with a 38.94% share of the India flooring resins market in 2025. Polyaspartic systems are projected to log the fastest 6.92% CAGR through 2031.

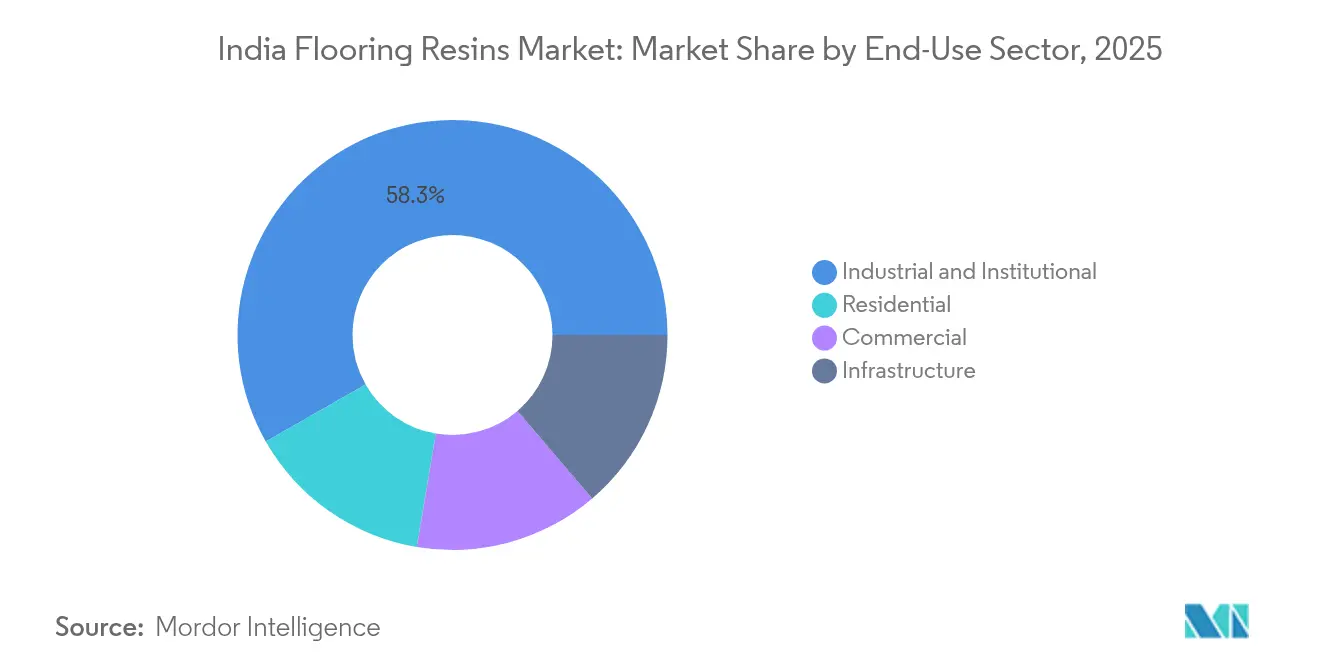

- By end-use sector, industrial and institutional facilities accounted for 58.25% of the India flooring resins market size in 2025 and will expand at a 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Flooring Resins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mega-infrastructure investments | +1.80% | Gujarat, Maharashtra, Tamil Nadu | Long term (≥ 4 years) |

| Expansion of organised retail & warehousing | +1.20% | Metro cities & industrial corridors | Medium term (2-4 years) |

| Pharmaceutical & food-grade hygiene demand | +0.90% | Hyderabad, Pune, Ahmedabad | Medium term (2-4 years) |

| Growing preference for low-VOC green resins | +0.70% | Urban centers with green-building activity | Long term (≥ 4 years) |

| Rapid adoption of fast-curing polyaspartics | +0.50% | Industrial zones seeking minimal downtime | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mega-infrastructure investments across the nation

The central government’s national logistics corridors, airports, and metro extensions require floor finishes that can withstand constant mechanical stress and chemical cleaning. Specifications cite seamless membranes that remain serviceable for decades without joint failures. Gujarat and Maharashtra industrial estates now specify epoxy or polyurethane screeds for chemical drums storage, while Chennai’s airport modernisation program mandates flame-retardant underlayments that meet Class 1 spread-of-flame ratings. International contractors further drive uniform product standards, encouraging domestic applicators to adopt global best practices in surface preparation and moisture testing. As project pipelines extend beyond 2029, resin suppliers benefit from predictable, high-volume demand that cushions cyclical swings in private real estate construction.

Expansion of organized retail and warehousing space

The rapid penetration of shopping malls and fulfillment centers intensifies the need for resilient, aesthetically appealing floors. Decorative flakes or metallic pigments embedded in resin layers enable brand-aligned color schemes, while slip-resistant topcoats enhance shopper safety[1]Mapei Construction Products India, “Benefits of Using Epoxy Flooring in India,” mapei.com . Warehouse operators prefer high-gloss epoxy systems that resist forklift abrasion yet remain easy to recoat during scheduled maintenance windows. Polyaspartic topcoats enable overnight renovations, letting retailers reopen by morning and avoid revenue loss. Because modern logistics hubs rely on automated guided vehicles, flatness tolerances under F-MIN standards are easier to achieve with poured resins than with tile finishes, cementing their preference in new big-box facilities.

Increasing pharmaceutical and food-grade hygiene compliance demand

Good Manufacturing Practice (GMP) audits require impermeable, pinhole-free surfaces that tolerate aggressive sanitizers. Seamless epoxy toppings with coved skirtings eliminate microbial niches at wall junctions and withstand repeated steam cleaning. Static-dissipative options prevent electrostatic discharge in cleanrooms, safeguarding sensitive formulations. India’s production-linked incentive (PLI) programs accelerate capacity additions for active pharmaceutical ingredients, keeping demand for conductive floor systems elevated through 2030. Food processors equally upgrade to polyurethane cement systems that remain stable under thermal shock from wash-down regimes, ensuring compliance with Food Safety and Standards Authority of India (FSSAI) guidelines.

Growing preference for low-VOC and green resins

Corporate environmental reports increasingly cite VOC inventories, pushing specifiers toward water-borne epoxies or bio-based polyols. Asian Paints’ Green Assure portfolio keeps VOC content below 100 g/L, enabling LEED or IGBC credit accrual[2]Asian Paints, “Green Assure VOC Standard Compliance,” kadiscoasianpaints.com. Multinational brands demand third-party emission certificates before awarding fit-out contracts, creating pull-through demand for compliant resin chemistries. Although green formulations cost more upfront, total lifecycle analyses show lower ventilation expenses and improved indoor-air quality, swaying facility managers in IT parks and hospitals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-derived raw-material prices | -1.10% | National, higher in import-dependent West & North | Short term (≤ 2 years) |

| Competition from conventional tile floors | -0.80% | Price-sensitive residential & low-end commercial segments | Medium term (2-4 years) |

| Stringent fire-safety norms limiting some chemistries | -0.60% | National, with stricter enforcement in metro cities and institutional projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile crude-derived raw-material prices

Epoxy resins, isocyanates, and specialty solvents track crude-oil price swings. Because feedstocks represent roughly half the finished-goods cost, rapid commodity fluctuations compress margins. Local producers partially hedge with long-term contracts, yet small formulators often carry higher inventory costs, limiting price flexibility. Exchange-rate volatility compounds the challenge for import-dependent northern applicators who source hardeners from Europe. The larger suppliers mitigate risk by integrating upstream or expanding local plants to reduce freight expenses. Nevertheless, unpredictable raw-material curves remain a headwind through 2027.

Competition from conventional tile and cement floors

India manufactures more than 3 billion m² of ceramic tiles annually, with Morbi in Gujarat supplying over 90% of domestic demand. Continuous kiln upgrades have lowered tile prices, keeping unit costs at roughly one-tenth of premium resin toppings. Printed vitrified slabs replicate stone patterns, attracting price-conscious developers and slowing resin penetration in mid-tier residential projects. Resin vendors respond by emphasizing lifecycle benefits—no grout maintenance, faster installation, and reduced downtime—yet initial-cost-focused buyers still gravitate toward tiles and polished concrete.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy leadership faces polyaspartic disruption

The India flooring resins market size for epoxies captured 38.94% in 2025, underpinned by decades-long acceptance in heavy-duty industrial environments. Antimicrobial and static-dissipative grades extend their relevance in pharmaceuticals, data centers, and healthcare. Polyurethane products are prized for impact resilience and thermal shock tolerance inside food and beverage plants. Acrylic systems target budget-driven commercial upgrades where moderate chemical resistance suffices.

Contractors increasingly specify polyaspartic hybrids, propelling this category to a forecast 6.92% CAGR—the fastest within the India flooring resins market. Cure-time savings shorten site programs and shrink client downtime penalties, tipping specification decisions in time-critical logistics hubs. Hybrid blends that overlay epoxy primers with polyaspartic top-sealers marry adhesion with weatherability, showcasing the industry’s shift toward multi-chemistry solutions that balance performance and cost.

By End-Use Sector: Industrial leadership drives market evolution

Industrial and institutional facilities accounted for 58.25% of India's flooring resins market share in 2025 while charting a robust 6.05% CAGR to 2031. Cleanroom projects, chemical warehouses, and heavy machinery assembly lines all require seamless toppings that resist corrosive spills and wheeled traffic. Pharmaceutical complexes specify conductive layers, coves, and epoxy terrazzo corridors to meet U.S. FDA audit expectations.

Commercial real estate—encompassing shopping malls, airports, and corporate campuses—forms the significant end-use segment. Here, design freedom provided by pigmentable resins intersects with functional needs such as skid resistance and acoustic dampening.

Infrastructure segments, notably metro stations and sports arenas, are increasingly standardizing on polyurethane cement for concourse slabs that can withstand footfall peaks. Residential uptake remains niche but shows promise in premium villas, where homeowners appreciate custom glossy finishes free of grout lines.

Geography Analysis

Western India leads consumption owing to Gujarat’s chemical complexes and Maharashtra’s pharmaceutical belt. Proximity to Dahej’s petrochemical feedstocks grants epoxy formulators supply security and lower freight costs, reinforcing competitive advantage. Mumbai–Pune expressway logistics parks demand abrasion-resistant coatings on warehouse slabs to protect against pallet jack traffic.

Southern growth centers such as Tamil Nadu benefit from sustained automotive investments around Chennai. Car plants specify oil-resistant polyurethane screeds across assembly zones, while component manufacturers adopt conductive epoxy in battery lines. Karnataka surfaces as an emerging pocket driven by Bengaluru’s biotech expansion; here, installers deploy antistatic self-leveling floors in vaccine filling suites and polyurethane mats in cold-chain chambers.

Northern adoption accelerates along the Delhi–NCR cluster, where metro extensions and data-center corridors require Class 1 flame-spread systems meeting the National Building Code Part IV. Uttar Pradesh’s industrial parks near Noida integrate epoxy terrazzo lobbies in electronics factories, reflecting a shift toward aesthetics alongside performance. Eastern states remain smaller contributors but record double-digit growth as port modernization plans in Odisha incorporate chemically resistant quay-side coatings.

Competitive Landscape

The India flooring resins market displays moderate consolidation. Large incumbents exploit integrated supply chains and proprietary formulations. Saint-Gobain’s USD 1.025 billion purchase of Fosroc adds construction chemicals breadth, enabling bundled offers that combine adhesives, grouts, and resin floors. RPM International’s new local plant strengthens distribution reach, reducing lead times for project-specific tint packs.

Technology differentiation remains central. Sika offers low-odor water-borne epoxies suited for hospital retrofits, while Asian Paints markets bio-based hardeners under its Green Assure line. Domestic challenger Master Builders Solutions re-enters with a Taloja plant and R&D hub aimed at custom blends for India’s unique climatic and regulatory conditions. Niche specialists focus on conductive or antimicrobial variants, targeting high-margin pharmaceutical and semiconductor clients. Across the landscape, service capabilities—site inspection, moisture testing, and applicator training—prove as decisive as material science in winning specification battles.

India Flooring Resins Industry Leaders

RPM International Inc.

Sika AG

Thermax Limited

Mapei S.p.A

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BASF and Sika have announced the joint development of a new amine building block for curing epoxy resins, now available commercially under BASF's Baxxodur EC 151 brand. This advancement is particularly suited for flooring applications, such as in production plants, storage and assembly halls, and parking decks.

- August 2025: CHIMIQUE SOL, with over a decade of expertise and more than 10 million square feet of epoxy flooring completed, announced its global expansion. As a trusted Indian manufacturer of industrial epoxy flooring materials, floor coatings, epoxy adhesives, and art resin products, the company aims to lead in high-performance resin systems while staying rooted in Indian values.

India Flooring Resins Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Acrylic, Epoxy, Polyaspartic, Polyurethane are covered as segments by Sub Product.| Acrylic |

| Epoxy |

| Polyaspartic |

| Polyurethane |

| Other Resin Types |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyaspartic | |

| Polyurethane | |

| Other Resin Types | |

| By End-use Sector | Commercial |

| Industrial and Institutional | |

| Infrastructure | |

| Residential |

Market Definition

- END-USE SECTOR - Flooring resins consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of flooring resin products based on epoxy, polyaspartic, polyurethane, acrylic, and other resins are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms