Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

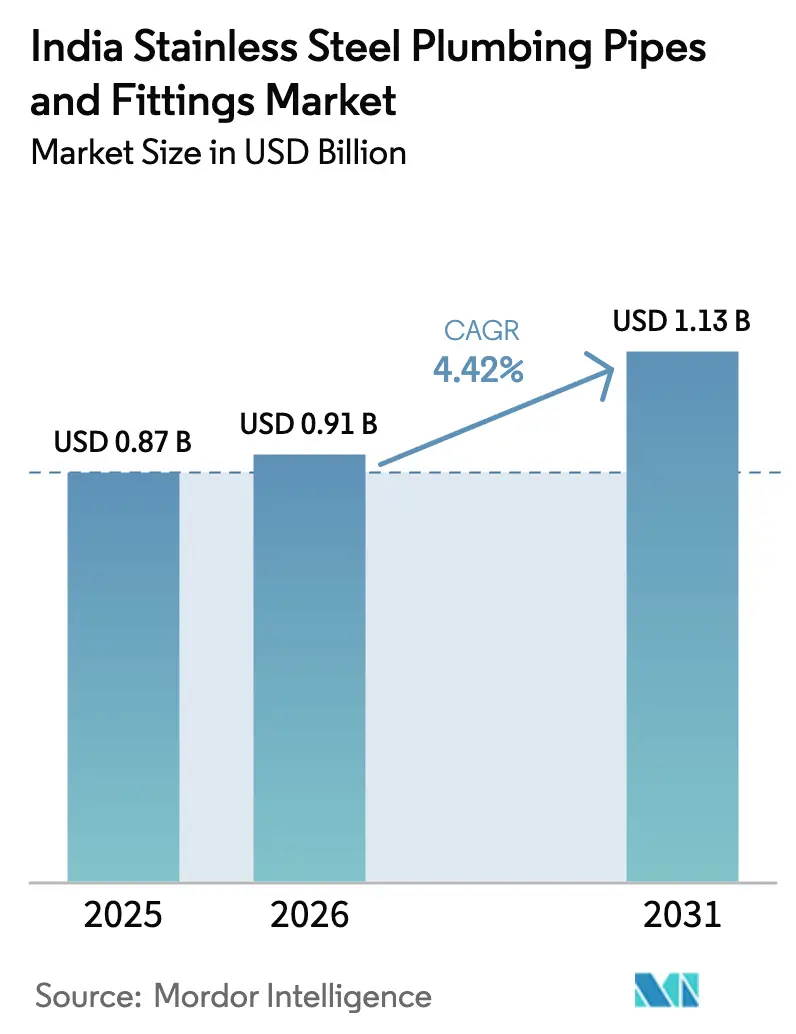

| Base Year Market Size (2025) | USD 0.87 Billion |

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.13 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

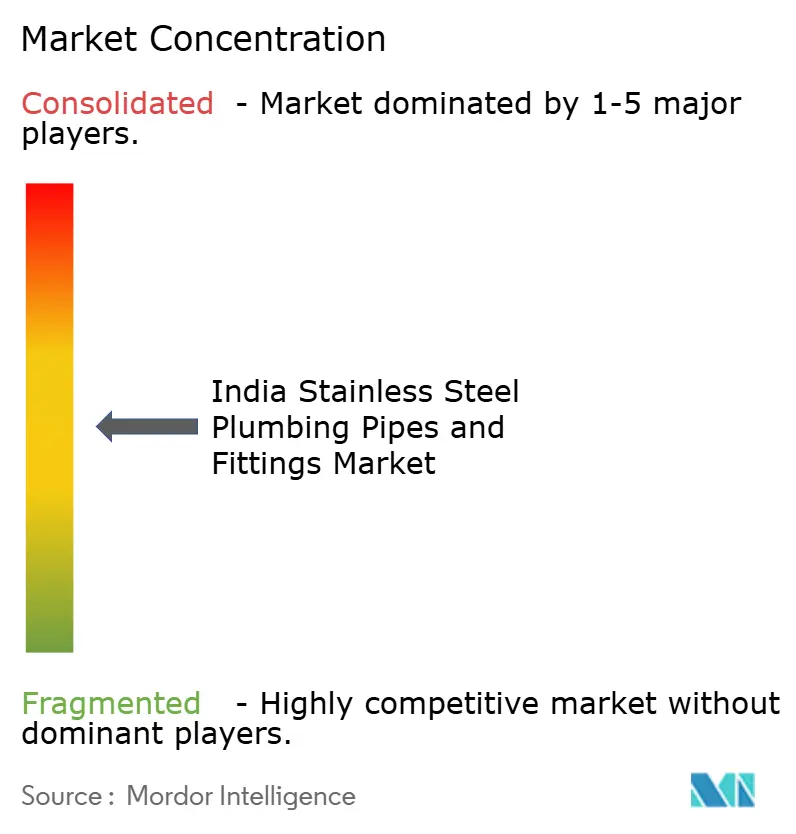

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Stainless Steel Plumbing Pipes And Fittings Market Analysis by Mordor Intelligence

The India Stainless Steel Plumbing Pipes and Fittings Market size in 2026 is estimated at USD 0.91 billion, growing from 2025 value of USD 0.87 billion with 2031 projections showing USD 1.13 billion, growing at 4.42% CAGR over 2026-2031. Quality-driven public programs such as the Jal Jeevan Mission and large private housing projects are shifting demand away from price-only decisions toward total-cost-of-ownership considerations, lifting premium material penetration. Developers cite stainless steel’s resilience against monsoon-driven corrosion, its compatibility with Internet-of-Things water meters, and its compliance with emerging lead-free mandates as the decisive advantages over galvanized iron and plastic rivals. The India stainless steel plumbing pipes and fittings market also benefits from abundant domestic melt capacity, which insulates supply chains from global shortages in the near term while still exposing producers to nickel price swings. Competitive intensity remains moderate because BIS certification and alloy-grade traceability deter opportunistic entrants even as organized players expand distribution into Tier 2 and Tier 3 cities.

Key Report Takeaways

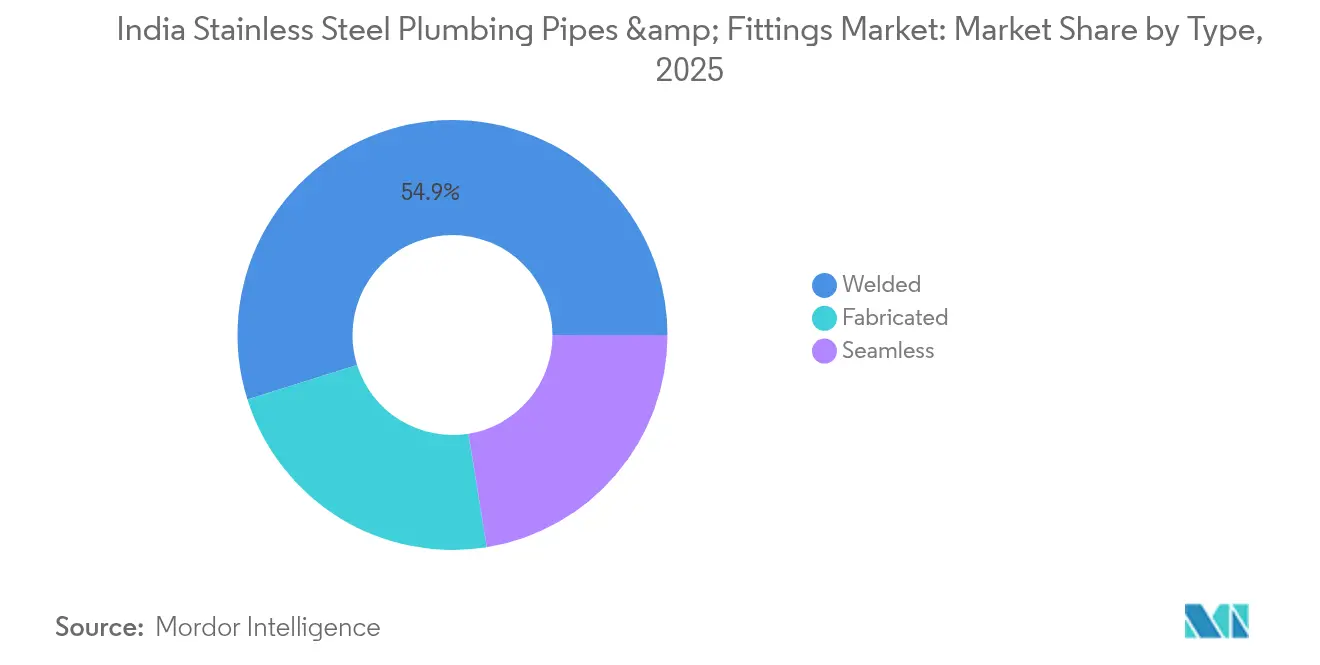

- By type, welded pipes captured 54.85% of the India stainless steel plumbing pipes and fittings market share in 2025, whereas fabricated products are forecast to expand at a 4.93% CAGR to 2031.

- By market structure, organized manufacturers held 59.65% of value in 2025, and the same cohort is projected to grow at a 4.55% CAGR through 2031.

- By diameter, small-bore pipes (less than or equal to 50 mm) made up 44.85% of shipments in 2025, while medium-bore lines (50-100 mm) are forecast to rise at a 4.71% CAGR through 2031.

- By sales channel, retail outlets secured 55.10% of 2025 turnover and are on course for a 5.02% CAGR to 2031 as organized chains penetrate underserved cities.

- By application, potable-water systems led with 40.10% of revenue in 2025; fire-sprinkler and hydrant installations are set to post the fastest 4.88% CAGR through 2031.

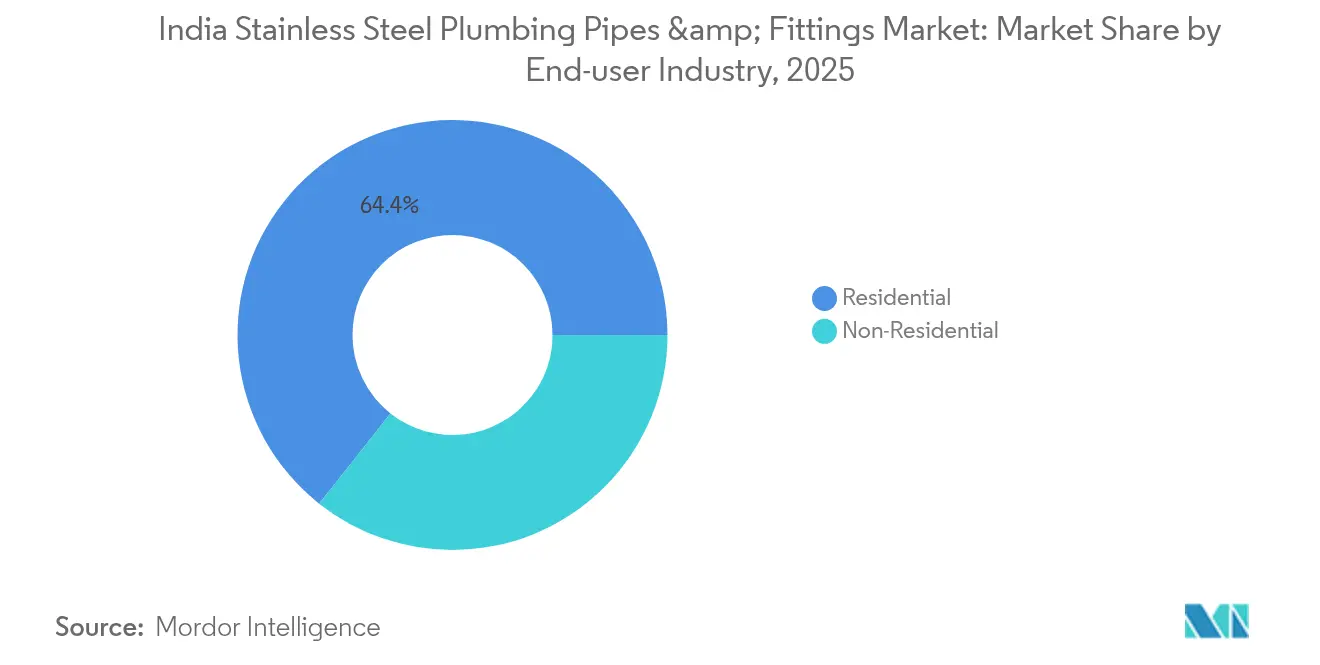

- By end-user industry, residential demand accounted for 64.35% of 2025 revenue, while non-residential applications are advancing at a 4.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Stainless Steel Plumbing Pipes And Fittings Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and smart-city roll-outs | +1.2% | Mumbai, Delhi, Bangalore and emerging satellite towns | Medium term (2-4 years) |

| Surge in large real-estate and infra projects | +0.8% | Maharashtra, Gujarat, Tamil Nadu, Karnataka | Short term (≤2 years) |

| Superior corrosion and temperature resistance | +0.9% | Coastal and high-humidity states | Long term (≥4 years) |

| Mandatory lead-free plumbing (Jal Jeevan) | +1.1% | Rural clusters and peri-urban districts | Medium term (2-4 years) |

| High-rise fire-safety compliance | +0.7% | Metro and Tier 1 cities | Short term (≤2 years) |

| Hygienic solar-water systems in hospitality | +0.6% | Tourism hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Smart-City Roll-Outs

Smart-city blueprints funded under the USD 15 billion national mission allocate nearly one-quarter of budgets to water supply upgrades. Planners now specify stainless steel piping for municipal loops longer than 10 years, citing the alloy’s low electromagnetic interference that safeguards IoT meter accuracy. Pune and Surat have already mandated stainless steel mains above 150 mm, setting procurement precedents that private developers replicate. With India’s urban population swelling at 2.3% annually to 2030, the India stainless steel plumbing pipes and fittings market stands to capture recurring demand from both new districts and brownfield retrofits in satellite towns. Contractors further highlight the alloy’s fire-safety credentials, linking it with higher insurance ratings that improve project viability.

Surge in Large Real-Estate and Infrastructure Projects

Commercial real-estate investment touched USD 5.7 billion in 2024, complemented by a USD 1.4 trillion National Infrastructure Pipeline earmarking 16% for water and sanitation. Developers now preset stainless steel for projects exceeding 500 units because it halves lifetime maintenance outlays versus galvanized iron. LEED and GRIHA certification matrices, which weigh material durability, further amplify this preference. The India stainless steel plumbing pipes and fittings market therefore gains predictable volume from high-rise clusters and industrial parks scheduled through 2028.

Superior Corrosion and Temperature Resistance

Average annual rainfall surpasses 1,000 mm across 70% of India, and chloride-rich groundwater is common in west-coast states. Chromium-rich alloys neutralize these stresses, while PVC and galvanized iron fail within 15 years under similar exposure. Stainless steel also retains ductility across 5 °C to 45 °C swings common in North India, avoiding micro-cracking seen in rigid plastics. Reduced biofilm formation further lowers pump energy by 15-20% over a 25-year cycle.

Mandatory Lead-Free Plumbing (Jal Jeevan Mission)

The government’s USD 50 billion Jal Jeevan Mission bans lead-bearing pipes for 192 million rural household taps[1]Ministry of Jal Shakti, “Jal Jeevan Mission Progress Report 2024,” jaljeevanmission.gov.in. BIS code IS 4985:2019 cites stainless steel Grades 304 and 316L as compliant materials, placing the alloy at the top of procurement shortlists. Because rural service calls are logistically costly, local authorities prefer one-time stainless steel installations that last longer than plastic alternatives susceptible to UV degradation.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-cost PVC/PEX substitution threat | -0.9% | Price-sensitive markets and rural areas | Short term (≤ 2 years) |

| Nickel-price volatility inflates SS costs | -0.7% | National, affecting all manufacturers | Medium term (2-4 years) |

| Installer skill-gap in Tier-2/3 cities | -0.5% | Tier-2/3 cities and rural markets | Medium term (2-4 years) |

| Molybdenum import-supply risk | -0.4% | National, particularly Grade 316L applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low-Cost PVC/PEX Substitution Threat

PVC and PEX systems undercut stainless steel by as much as 50% on upfront cost, drawing budget-constrained homeowners toward plastic. Organized PVC producers expanded 2024 sales by 12% through extended warranties and trade-in schemes. Flexible PEX lines also reduce labor time by 30%, tempting contractors on tight schedules. Marketing campaigns accentuate corrosion immunity but seldom mention PEX’s 65 °C service-temperature ceiling or UV vulnerability.

Nickel-Price Volatility Inflates Stainless Steel Costs

Nickel averaged USD 16,000-28,000 per tonne during 2024, reflecting Indonesian export curbs and EV battery demand. Grade 304 uses 8-10% nickel, so alloy surcharges can swing monthly quotes by 12-15%. Smaller mills lacking hedge cover pass spikes downstream, occasionally ceding share to plastics when quotations overshoot budget thresholds. Molybdenum required for 316L is equally volatile, reinforcing procurement risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Welded Dominance Meets Fabricated Innovation

Welded pipes held 54.85% of 2025 value thanks to standardized dimensions preferred in mass-housing blocks. Fabricated lines are poised for a 4.93% CAGR to 2031 as architects demand bespoke risers in complex HVAC and fire-safety grids. The India stainless steel plumbing pipes and fittings market size for seamless pipes remains smaller but commands premium pricing in gas and high-pressure loops where zero defects are non-negotiable.

Scaling economics favor welded production: Jindal Stainless lifted welded capacity by 40% in 2024 to serve affordable-housing builders aiming for 15-50 mm diameters. Fabrication houses compensate by offering site-specific spools that minimize fit-up errors during retrofits. While BIS certificates apply to all, fabricated assemblies need part-wise testing, extending approval cycles but ensuring traceable quality that contractors welcome.

By Market Structure: Organized Players Consolidate Share

Organized manufacturers owned 59.65% revenue in 2025, and their share is expanding at a 4.55% CAGR to 2031 as GST compliance erodes informal-sector price gaps. Their long-term nickel contracts buffer price shocks, allowing steadier project quotes and reinforcing brand trust. The India stainless steel plumbing pipes and fittings market size in the unorganized tier is shrinking as buyers weigh warranty coverage, which organized labels readily provide.

Quality Stainless exemplifies mid-tier success by occupying the space between high-end brands and untested local fabricators. Organized firms further leverage digital catalogs and engineer hotlines, helping contractors navigate complex alloy-grade charts. As BIS tightens plant audits, entry costs climb, accelerating consolidation.

By Diameter: Medium-Bore Growth Reflects Infrastructure Scale

Small-bore (less than or equal to 50 mm) still captures 44.85% share for everyday household taps, yet medium-bore (50-100 mm) pipelines are climbing at a 4.71% CAGR through 2031. Multi-tower complexes channel higher flow rates across fewer vertical stacks, elevating demand for 65-90 mm diameters that balance pressure drop and material cost.

Tata Steel’s tubes arm crossed the 1 million-tonne milestone in 2024, buoyed by medium-bore shipments that made up 35% of its volume increase. Installation crews favor these sizes because larger borelines cut the number of joints, mitigating leak points and reducing commissioning times.

By Sales Channel: Retail Expansion Drives Market Access

Retail stores controlled 55.10% of 2025 turnover and should log a 5.02% CAGR to 2031 as organized chains move beyond metros. In-store plumbing consultants demystify grade selection, an edge that pure e-commerce lacks. Direct B2B contracts remain entrenched for mega-projects where volumes justify factory-gate shipments.

While online portals like IndiaMART aid price discovery, bulky shipments and onsite inspection needs slow digital adoption for diameters beyond 100 mm. Retail chains, meanwhile, bundle credit facilities and installer networks, attracting small contractors who dominate India’s building sector. The India stainless steel plumbing pipes and fittings industry thus leverages omnichannel reach to stabilize order books.

By Application: Fire Safety Drives Premium Growth

Potable water lines generated 40.10% of turnover in 2025, but fire-sprinkler loops are on track for a 4.88% CAGR through 2031 as metro skylines densify. The India stainless steel plumbing pipes and fittings market size attributed to fire-safety projects gains from mandatory NBC 2016 compliance for any building taller than 15 meters.

Waste-water, HVAC, and fuel-gas loops diversify revenue streams, softening cyclical swings in housing permits. ASHRAE studies confirm stainless steel’s smoother bore trims pump energy by 15-20%, a quantifiable benefit that appeals to green-building scorecards. Sprinkler designers prefer 316L in coastal towers because chloride attack could impair sprinkler integrity in alternatives.

By End-User Industry: Non-Residential Acceleration

Residential construction delivered 64.35% of 2025 demand yet non-residential lines are rising at a 4.63% CAGR to 2031 on the back of office, hospitality, and data-center builds. The India stainless steel plumbing pipes and fittings market share within offices is growing because chilled-water loops favor the alloy’s low friction head.

Hotel chains including Taj and Oberoi mandate stainless steel risers for hygiene and brand protection. Industrial campuses seek 316L to prevent chemical-induced pitting, thereby avoiding unscheduled shutdowns. Healthcare renovations amplify demand too, citing infection-control guidelines that discourage micro-scratched plastics.

Geography Analysis

Maharashtra leads national off-take, buoyed by Mumbai–Pune real-estate corridors and proximity to Jajpur’s melt shops that guarantee steady coil feedstock. Gujarat’s consumption is growing on the back of petrochemical clusters requiring corrosion-resistant process water lines. Tamil Nadu and Karnataka represent the fastest-growing pockets as IT parks in Bangalore and the Chennai auto belt specify premium fire-sprinkler and HVAC piping.

Coastal humidity in western and southern belts accelerates galvanized-iron corrosion, making stainless steel economically compelling over 20-year valuations. Chennai municipal codes now recommend stainless steel for potable mains within 10 km of the seafront, driving rapid substitution. Northern states such as Delhi, Haryana, and Uttar Pradesh are catching up thanks to smart-city pilots in Lucknow and Kanpur and Jal Jeevan rural pipelines that prioritize lead-free materials.

Extreme temperature swings from 5 °C winters to 45 °C summers in the north fracture rigid PVC systems, elevating stainless steel adoption among utility boards. Pharmaceutical and food-processing zones in Uttar Pradesh further lean toward stainless steel for hygiene compliance, widening the regional footprint of organized suppliers.

Competitive Landscape

The India stainless steel plumbing pipes and fittings market shows moderate fragmentation. Jindal Stainless and Tata Steel anchor the field with captive nickel and chromium streams that shave 8-12% off alloy surcharges versus non-integrated rivals. Mid-scale challengers such as Quality Stainless are scaling via regional depots and custom-fabrication cells. Product innovation is another lever: Aeroflex captured niche share with flexible stainless hoses that simplify retrofit jobs in cramped mechanical shafts. BIS Quality Control Orders effective 2022 now make ISI stamping compulsory, raising capex bars for late entrants and validating established players’ research and development outlays.

India Stainless Steel Plumbing Pipes And Fittings Industry Leaders

APL Apollo

Jindal Stainless Ltd

Nippon Steel Corporation

Ratnamani Metals & Tubes Limited

Viega India Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Jindal Stainless committed Rs 5,400 crore (USD 648 million) to lift melt capacity to 4.2 million t by 2027, with a sizable tranche earmarked for downstream plumbing tube mills.

- January 2022: The Ministry of Steel issued Quality Control Orders mandating BIS certification for stainless-steel pipes and tubes under IS 17876:2022, locking in uniform safety thresholds across the supply chain.

India Stainless Steel Plumbing Pipes And Fittings Market Report Scope

Stainless steel plumbing pipes are made from steel alloys containing iron, nickel, chromium, and others primarily used in different plumbing applications to transport fluid. Stainless steel pipe fitting is a part that connects a pipe to another pipe. Its primary purpose is to connect, control, and change the direction, especially in bent pipes, and split, seal, and support various parts and components in the pipeline system. These fittings include pipe elbows, tee, stub end, pipe bending, end caps, reducer, pipe cross, saddle previously, and many others. The India stainless-steel plumbing pipes and fittings market is segmented by type, market structure, end-user industry, and sales channel. The market is segmented by type: seamless, welded, and fabricated. By market structure, the market is segmented into organized and unorganized. By end-user industry, the market is segmented into residential and non-residential. By sales channel, the market is segmented into retail, e-commerce, and direct. The report also covers the market size, and forecasts for each segment have been made based on value (USD Million).

By Type

| Seamless |

| Welded |

| Fabricated |

By Market Structure

| Organised |

| Unorganised |

By Diameter

| Less than or equal to 50 mm (Small-Bore) |

| 50-100 mm (Medium) |

| More than 100 mm (Large-Bore) |

By Sales Channel

| Retail |

| E-commerce |

| Direct Institutional/B2B |

By Application

| Potable Water Supply |

| Waste-water and Drainage |

| Fire-sprinkler and Hydrant |

| Gas and Fuel Lines |

| HVAC and Chilled Water |

By End-User Industry

| Residential |

| Non-Residential |

| By Type | Seamless |

| Welded | |

| Fabricated | |

| By Market Structure | Organised |

| Unorganised | |

| By Diameter | Less than or equal to 50 mm (Small-Bore) |

| 50-100 mm (Medium) | |

| More than 100 mm (Large-Bore) | |

| By Sales Channel | Retail |

| E-commerce | |

| Direct Institutional/B2B | |

| By Application | Potable Water Supply |

| Waste-water and Drainage | |

| Fire-sprinkler and Hydrant | |

| Gas and Fuel Lines | |

| HVAC and Chilled Water | |

| By End-User Industry | Residential |

| Non-Residential |

Key Questions Answered in the Report

What is the current value of the India stainless steel plumbing pipes and fittings market?

The market is valued at USD 0.91 billion in 2026 with a forecast to reach USD 1.13 billion by 2031.

How fast is demand for stainless steel fire-sprinkler systems growing?

Fire-sprinkler and hydrant applications are projected to post a 4.88% CAGR through 2031, the fastest among all end-uses.

Which pipe type holds the largest share today?

Welded stainless steel pipes lead with 54.85% of 2025 revenue.

Why are medium-bore pipes gaining popularity?

Medium-bore (50-100 mm) sizes support higher flow in multi-tower complexes and are forecast to grow at a 4.71% CAGR to 2031.

How are Quality Control Orders affecting market entry?

Mandatory BIS certification under IS 17876:2022 increases compliance costs and favors established producers with accredited testing facilities.

Page last updated on: