India Automotive Wiring Harness Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

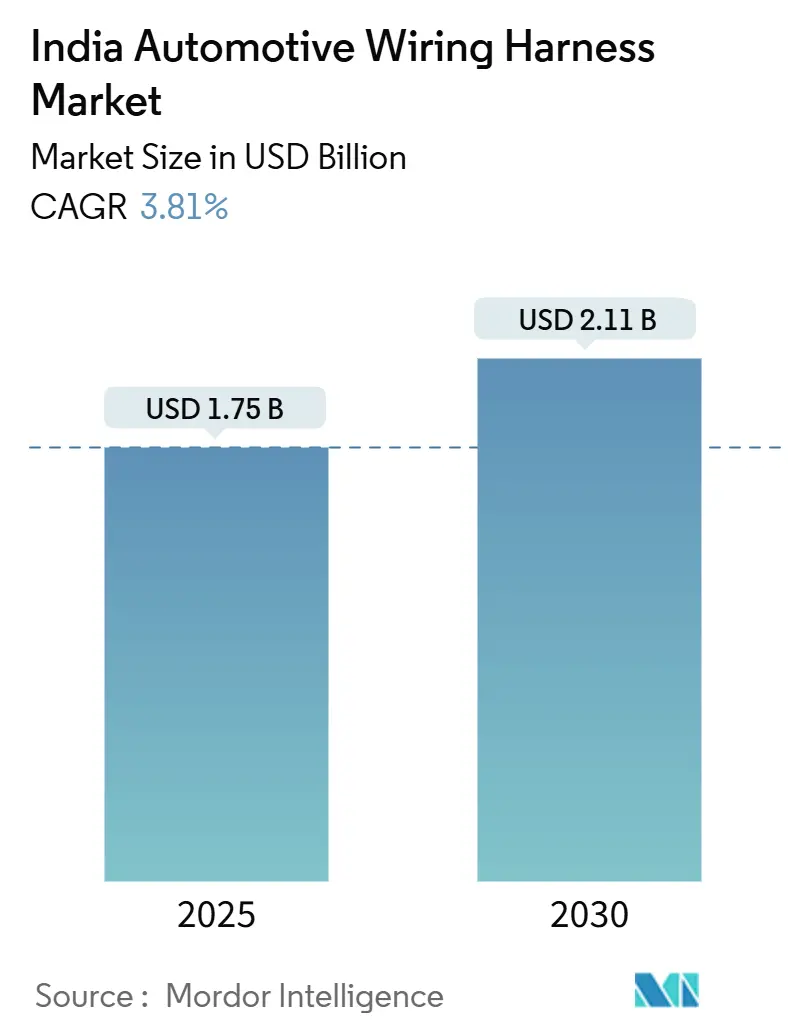

| Market Size (2025) | USD 1.75 Billion |

| Market Size (2030) | USD 2.11 Billion |

| Growth Rate (2025 - 2030) | 3.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automotive Wiring Harness Market Analysis by Mordor Intelligence

The India automotive wiring harness market stood at USD 1.75 billion in 2025 and is forecast to reach USD 2.11 billion by 2030, advancing at a 3.81% CAGR. Sustained passenger-vehicle production, rapid electrification, and rising digital content per car underpin demand, while material substitution and localized supply chains shape the cost curve. Body, lighting, and cabin-comfort harnesses still dominate volumes. Yet, high-voltage traction assemblies record the most vigorous gains because every new battery-electric model multiplies conductor cross-section and insulation requirements. OEMs are also redesigning 12 V looms to carry expanding infotainment, telematics, and advanced driver-assistance systems over a single zonal architecture, delinking future revenue from mere wire counts. On the supply side, entrenched qualification hurdles and just-in-time delivery expectations preserve moderate concentration even as global majors and domestic specialists invest in capacity around Chennai, Pune, and Gujarat hubs.

Key Report Takeaways

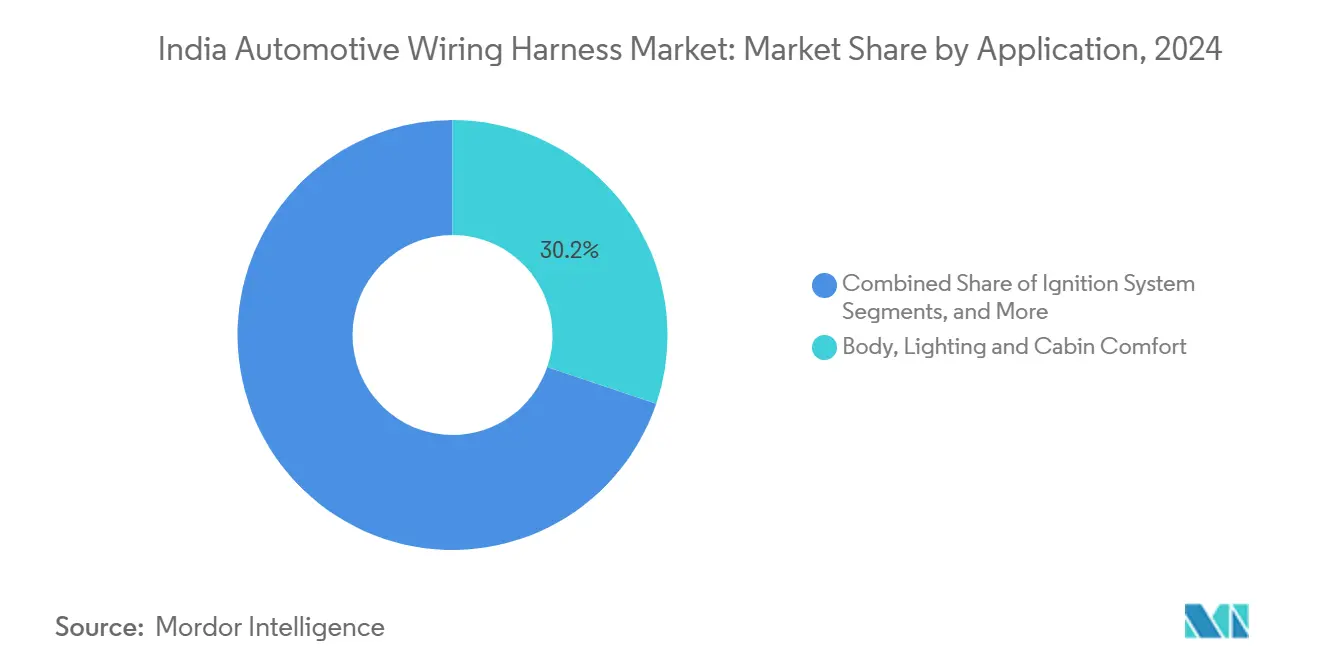

- By application, Body, Lighting & Cabin Comfort led with 30.22% of the Indian automotive wiring harness market share in 2024. In contrast, high-voltage traffic Harnesses will expand by 5.26% CAGR by 2030.

- By conductor material, copper retained 78.31% of the Indian automotive wiring harness market share in 2024; aluminum is forecast to post the fastest 6.41% CAGR through 2030.

- By voltage rating, low-voltage (<60 V) systems accounted for 74.83% of the Indian automotive wiring harness market share in 2024, while high-voltage (60–1,000 V) systems will register a 5.88% CAGR by 2030.

- By propulsion, internal-combustion platforms commanded 83.39% of the Indian automotive wiring harness market share in 2024; battery-electric vehicles will accelerate at a 7.12% CAGR over the forecast horizon.

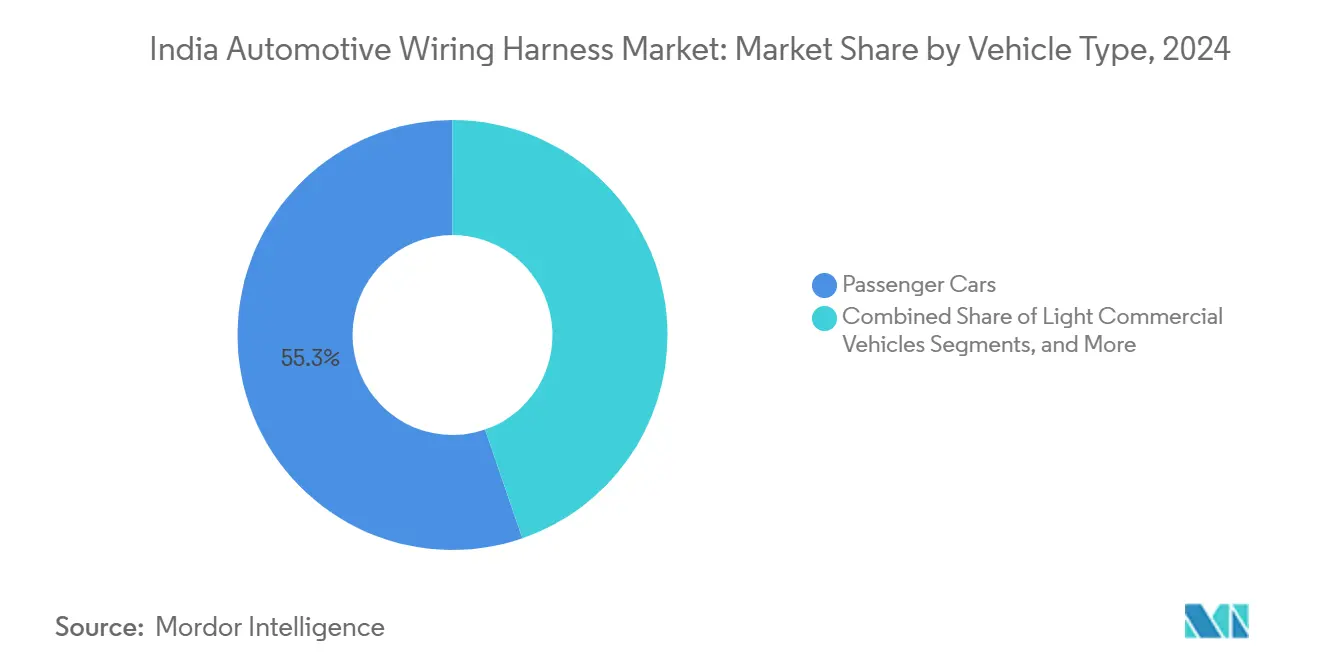

- By vehicle type, passenger cars held a leading 55.28% of the Indian automotive wiring harness market share in 2024, yet the same segment still delivers the highest 6.28% CAGR until 2030.

- By sales channel, OEM procurement captured 84.71% of the Indian automotive wiring harness market share in 2024, whereas the aftermarket is expected to climb at a 5.68% CAGR as retrofit demand rises.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on automotive wiring harness market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Automotive Wiring Harness Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Passenger-Vehicle Build Volumes | +1.0% | National, concentrated in Tamil Nadu, Maharashtra, Gujarat | Medium term (2-4 years) |

| Government E-Mobility Incentives (FAME II, PLI) | +0.8% | National, with early adoption in Delhi, Karnataka, Maharashtra | Long term (≥ 4 years) |

| Infotainment & Telematics Electrification Wave | +0.7% | Urban markets, premium vehicle segments nationwide | Short term (≤ 2 years) |

| High-Speed OTA Diagnostics Mandate | +0.5% | Connected vehicle segments, commercial fleets nationwide | Short term (≤ 2 years) |

| Emerging Tier-II/III Supplier Clusters | +0.4% | Regional clusters in Pune, Chennai, Gujarat, Haryana | Medium term (2-4 years) |

| Shift To Al/CCA Lightweight Conductors | +0.3% | Export-oriented manufacturing hubs, premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Passenger-Vehicle Build Volumes

Passenger-car production hit 4.2 million units in 2024, up 9.8% yearly [1]“Production Statistics FY 2024,”, Society of Indian Automobile Manufacturers, siam.in. Each unit carries 3–5 sub-harnesses, so volume increases translate directly into loom demand. Major suppliers opened satellite plants next to OEM lines to honor takt-time windows, reducing logistics costs and scrap. Content per vehicle is climbing as even entry models integrate rear-view cameras, ESC, and TPMS, lifting conductor length beyond 1.5 km on average. Consequently, the Indian automotive wiring harness market benefits twice—first from unit growth, then from richer electrical architectures.

Government E-Mobility Incentives (FAME II, PLI)

The Production-Linked Incentive program reserves USD 3.5 billion for advanced automotive components, including high-voltage harnesses[2]“PLI Scheme for Auto Components,”, Press Information Bureau, pib.gov.in. Domestic value-addition thresholds persuade multinationals like Yazaki to localize crimping, over-molding, and high-pot testing lines. FAME II subsidies raised electric two-wheeler sales, each requiring 48 V looms with temperature-monitoring leads, opening green-field orders for tier-II suppliers. Long-term policy visibility shields capex decisions, offsetting the higher capital sunk in HV insulation and connector tooling.

Infotainment and Telematics Electrification Wave

Cockpit digitization pushes high-speed data cables alongside conventional power lines. AIS-140 mandates for commercial fleets evolved into subscription-based telematics across personal cars, demanding shielded twisted pairs and ethernet backbones. Harness makers able to co-design wire routing with ECU suppliers win premium margins. The trend also spurs zonal network layouts that cut harness weight by up to 20%, supporting OEM range and fuel-economy targets.

Shift to Al/CCA Lightweight Conductors

The increasing cost of copper is prompting automotive OEMs to use aluminum and copper-clad aluminum wiring in vehicle harnesses. These materials reduce vehicle weight and overall costs but require specialized connector designs to maintain reliability. Although initial testing shows positive results, the materials' long-term durability in demanding automotive environments continues to be a technical barrier to broad implementation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper Price Volatility | -0.6% | National, affecting all manufacturing regions | Short term (≤ 2 years) |

| Shortage Of Certified Harness Technicians | -0.4% | Industrial clusters in Tamil Nadu, Maharashtra, Karnataka | Medium term (2-4 years) |

| Semiconductor-Linked Production Delays | -0.3% | OEM production centers, integrated suppliers | Medium term (2-4 years) |

| Humidity-Driven HV-Joint Corrosion Issues | -0.2% | Coastal manufacturing regions, tropical climate zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Copper Price Volatility

Copper price volatility affects supplier margins, particularly for those with fixed-price contracts. Large companies manage risk through hedging strategies, while small suppliers face greater exposure to price fluctuations. Original equipment manufacturers (OEMs) are adopting indexed pricing models, though contract renegotiation delays impact supplier cash flows. The increased material costs have led to a higher incidence of counterfeit products in aftermarket segments, necessitating enhanced quality verification processes and supplier audits.

Shortage of Certified Harness Technicians

The industry faces a shortage of certified harness technicians, particularly for high-voltage systems that require specialized safety and testing expertise. Major suppliers have established in-house training programs, but onboarding is expensive and time-consuming. Small vendors face challenges retaining skilled workers, who frequently transition to higher-paying positions with OEMs. This talent migration slows production expansion and widens the workforce gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Electrification Drives High-Voltage Growth

Body, lighting, and cabin-comfort assemblies retained 30.22% of India's automotive wiring harness market share in 2024, thanks to their ubiquity across all trims. Yet high-voltage traction looms, essential for battery-electric drivetrains, are forecast to clock a 5.26% CAGR, lifting their slice of the market appreciably by 2030.

The segment mix reflects India’s phased electrification: ICE platforms still need spark, sensor, and fuel-system looms, but every BEV launch adds orange-jacketed 400 V lines. Suppliers able to co-package power and data within shared conduits secure higher ASPs and tighter design lock-ins. Over-the-air updatable infotainment is raising demand for low-latency Ethernet within cockpit clusters, blending with camera and radar harnesses required for emerging Level-2 ADAS features.

By Conductor Material: Aluminum Gains Despite Copper Dominance

Copper controlled 78.31% of the Indian automotive wiring harness market share in 2024, yet aluminum is set to outpace it with a 6.41% CAGR, gradually expanding its slice of the market until 2030.

Aluminum’s lower density trims 0.5 kg per vehicle, an advantage amplified in EVs' chasing range. OEMs specify CCA for branch circuits under 30 A, reserving copper for high-current leads. Crimp, connector redesigns, and anti-galvanic coatings raise switching costs, so early movers enjoy defensible IP. Export-oriented programs weigh container freight savings, further tipping decisions toward lightweight metals.

By Voltage Rating: High-Voltage Segment Emerges

Low-voltage architectures (<60 V) hold 74.83% of the Indian automotive wiring harness market share in 2024. However, high-voltage systems will grow 5.88% annually, nudging their contribution to the Indian automotive wiring harness market size higher by 2030.

Transitioning beyond 60 V triggers creepage-clearance rules and partial-discharge tests, elevating entry barriers. Suppliers installing PD testers and climate chambers in Chennai and Pune plants can quote faster on EV platforms, beating import lead times. AIS 189 and upcoming ISO 21434 mandates embed cybersecurity into HV controller networks, intertwining software validation with loom design.

By Propulsion Type: Electric Transition Accelerates

Internal-combustion vehicles kept an 83.39% of the Indian automotive wiring harness market share in 2024. Still, battery-electric platforms will post a 7.12% CAGR through 2030, widening their revenue share within the Indian automotive wiring harness market by the decade's end.

EV harnesses carry fewer circuits yet higher copper area, raising per-loom value by 1.8 times. OEMs push zonal controllers and daisy-chained sensors to simplify routing. Suppliers offering design-for-manufacture workshops during platform kick-off secure nomination ahead of price negotiations, locking in multiyear volumes.

By Vehicle Type: Passenger Cars Drive Volume

Passenger cars represented 55.28% of the Indian automotive wiring harness market share in 2024 and will continue to expand at a 6.28% CAGR, enlarging their contribution to the market through 2030.

Light commercial vans follow closely, propelled by e-commerce logistics requiring telematics-rich looms. Heavy trucks add value through redundant power feeds and trailer interface harnesses. Mining and port automation pilots need sensor looms with ruggedized connectors, an emerging niche for specialized SMEs.

By Sales Channel: OEM Dominance Persists

OEM contracts covered 84.71% of the Indian automotive wiring harness market share in 2024, leaving the aftermarket a modest but quickening 5.68% CAGR through 2030.

While long development cycles and PPAP submissions provide a protective barrier for established players, the introduction of retrofit kits for fleet telematics and ADAS is paving a new revenue stream, free from the oversight of OEMs. As the average age of vehicles surpasses nine years, the demand for replacements intensifies, prompting distributors to increasingly stock modular sub-harnesses.

Geography Analysis

Production concentrates in the Chennai-Sriperumbudur belt, Pune-Aurangabad corridor, and Gujarat’s Sanand-Mandvi zone. Tamil Nadu alone houses three Yazaki plants and Aptiv’s USD 45 million software-defined cockpit line, leveraging port access and mature supplier ecosystems. Maharashtra’s automotive hub benefits from established Tier-II die-casting and electronics vendors, enabling rapid prototyping and small-batch validation. Gujarat offers SEZ incentives and proximity to Mundra port, slashing export lead times for Japanese and European OEM programs.

Karnataka’s Bengaluru cluster blends IT talent with component manufacturing, making it ideal for high-speed data-loom development and cybersecurity validation under AIS 189. Haryana supports premium passenger-car brands around Gurugram, demanding higher data-rate backbones and ADAS sensor looms. Emerging tier-III towns such as Hosur and Sanand attract labor-intensive crimping shops, dispersing risk yet raising quality-control challenges.

Geographic clustering reduces logistics overhead but heightens exposure to localized shocks such as 2024’s semiconductor shortages, which idled multiple assembler lines simultaneously. Policy makers now float multi-node vendor development schemes to diversify risk without forfeiting economies of scale. Export opportunities broaden as Indian plants receive global Q1 awards from Toyota, Stellantis, and VW, attesting to rising quality parity with ASEAN peers.

Competitive Landscape

India's automotive wiring harness market demonstrates moderate concentration, with international corporations and domestic manufacturers competing. Motherson Sumi maintains market leadership by supplying major automotive manufacturers through its widespread production facilities. Japanese companies Yazaki and Sumitomo Electric provide just-in-time manufacturing solutions, while Aptiv specializes in electrical system architectures. Domestic manufacturers are expanding their capabilities through technical collaborations to enter higher-value market segments[3]“Investor Presentation 2024,”, Aptiv PLC, aptiv.com.

Strategic differentiation hinges on three levers: automation, materials expertise, and software integration. Leaders deploy laser wire-marking, ultrasonic welding, and inline vision inspection to curb rework and address labor scarcity. Aluminum and CCA pioneers secure cost leadership amid copper inflation. Further, suppliers embedding cybersecurity protocols within harness ECUs gain early-mover credibility as AIS 189 takes effect.

M&A and joint ventures characterize 2024-2025 moves. Sumitomo’s share divestment in Samvardhana Motherson and Aptiv’s spin-off plan for its Electrical Distribution Systems unit may reshape bargaining power with OEMs. Investors such as Aavishkaar Capital channel funds into upstream metal-processing firms, underlining supply-chain widening beyond wire cutting and crimping.

India Automotive Wiring Harness Industry Leaders

Yazaki India Pvt Ltd

Lear Corporation

Minda Corporation Limited

Aptiv PLC

Motherson Sumi Wiring India Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Samvardhana Motherson International Limited (SAMIL) has secured board approval for a joint venture agreement with South Korea's Egtronics Co., Ltd. Under the agreement, SAMIL will hold a controlling 51% stake, while Egtronics will possess the remaining 49%. This collaboration empowers SAMIL's Wiring Harness Division to deliver advanced power electronics solutions, catering to the growing demands of clean mobility, including electric and hydrogen vehicles, explicitly targeting the commercial vehicle market.

- April 2025: Yazaki partnered with Horizon Industrial Parks to construct a 316,000-square-foot wiring harness manufacturing facility in Chengalpattu, Chennai. The new plant aims to enhance Yazaki's production capabilities and strengthen its presence in the automotive components sector. This strategic expansion aligns with the region's growing demand for automotive wiring harnesses and demonstrates Yazaki's commitment to serving its customers in the Indian market.

India Automotive Wiring Harness Market Report Scope

| Ignition System |

| Charging & Power Supply System |

| Drivetrain & Powertrain (ICE) |

| High-Voltage Traction Harness (xEV) |

| Infotainment, Cockpit & Telematics |

| ADAS & Safety Control |

| Body, Lighting & Cabin Comfort |

| Copper |

| Aluminum |

| Low-Voltage (Below 60 V) |

| High-Voltage (60 - 1,000 V) |

| Internal Combustion Engine Vehicles |

| Battery Electric Vehicles |

| Plug-in Hybrid & Hybrid Vehicles |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy-Duty Trucks & Buses |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| By Application | Ignition System |

| Charging & Power Supply System | |

| Drivetrain & Powertrain (ICE) | |

| High-Voltage Traction Harness (xEV) | |

| Infotainment, Cockpit & Telematics | |

| ADAS & Safety Control | |

| Body, Lighting & Cabin Comfort | |

| By Conductor Material | Copper |

| Aluminum | |

| By Voltage Rating | Low-Voltage (Below 60 V) |

| High-Voltage (60 - 1,000 V) | |

| By Propulsion Type | Internal Combustion Engine Vehicles |

| Battery Electric Vehicles | |

| Plug-in Hybrid & Hybrid Vehicles | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy-Duty Trucks & Buses | |

| By Sales Channel | Original Equipment Manufacturer (OEM) |

| Aftermarket |

Key Questions Answered in the Report

How big is the India automotive wiring harness market in 2025?

It is valued at USD 1.75 billion in 2025, with a 3.81% forecast CAGR to 2030.

Which segment grows fastest in the next five years?

High-voltage traction harnesses post the quickest 5.26% CAGR as EV volumes rise.

Why are aluminum conductors gaining share?

OEMs adopt aluminum and CCA to trim weight and counter copper-price volatility, driving a 6.41% growth pace for lightweight metals.

How do government incentives affect suppliers?

FAME II and the PLI scheme spur local production of high-voltage looms and attract foreign investment in new Indian plants.

What keeps competition moderate despite many players?

OEM qualification barriers, capital-intensive high-voltage tooling, and long program lifecycles protect incumbents while limiting new entrants.

Page last updated on: